Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Behind the Pharma Rep Ban Saga

- India’s Tyre Giants Navigate a Bumpy Ride

Behind the Pharma Rep Ban Saga

The Indian Pharmaceutical Alliance (IPA) and the Directorate General of Health Services (DGHS) are locking horns over a new rule: which bans medical representatives (MRs) from government hospital premises.

In plain terms, the Health Ministry (via DGHS) told all central government hospitals, “No pharma sales reps allowed inside, period .” The idea is to stop any interference with patient care – representatives can no longer hang around clinics, pitch drugs, or influence prescriptions while patients wait in line.

As you might expect, the IPA — a lobby of big domestic drug companies — isn’t happy. They’ve called this a ‘’blanket ban**’** that could do more harm than good, and are urging the government to think again.

We’re here to unpack why this tussle is happening, what’s at stake, and what it means for doctors, patients, and the pharma industry.

Who are MRs, and why do pharma companies need them?

Medical representatives (MRs) are kind of a big deal for the pharma industry. They play a dual-role: part educator , part salesperson . An MR’s job is to visit doctors — armed with brochures and drug samples — and tell them about the latest drugs or treatments their company offers.

For example, if a company just launched a new blood pressure pill, their MR will drop by a hospital to chat with cardiologists about why this pill is great. Next time the doctor writes a prescription, this might just nudge them to remember the pill.

This isn’t necessarily a bad thing. As long as pharma companies are principled, in theory , everyone benefits when doctors are up to date on treatments. In practice, however, the fact that these interactions double as marketing opportunities for pharma companies can create problems.

Essentially, when an MR builds a relationship with doctors, that can be a double edged sword. While they might provide genuine medical updates to doctors, in less scrupulous cases, they might affect the medical judgement of a doctor with the freebies and perks they offer, inducing them to choose their drug, even if it isn’t the best choice for the patient. They’re essentially straddling a fine line between education and promotion .

There are ethics at stake

The big worry, here, is what happens when profit takes precedence over patient interest. If a doctor prescribes a medicine solely because an MR offered them a sweet perk — say a fancy dinner — that’s a serious problem. It could mean patients end up with pricier or less-suitable drugs, all because of invisible pressure on the doctor.

Health authorities and watchdogs fear that without rules to prohibit such behaviour, MRs could turn hospital corridors into bazaars of influence. This is why there are ethical codes in place around the world to keep pharma marketing in check. In the United States, pharma firms follow the PhRMA Code – guidelines that similarly ban giving out anything that isn’t primarily for patient benefit. Europe has the EFPIA Code of Practice, which does the same for EU countries.

Fundamentally, these codes draw a clear line: Share knowledge? Yes . Throw money or gifts at doctors? No . They exist to make sure that when your doctor prescribes something, it’s because you need it – not because a salesperson asked them to.

Similarly, India has the ‘Uniform Code of Pharmaceutical Marketing Practices’ (UCPMP), first introduced in 2015 as a set of do’s and don’ts for drug marketing. It basically tells pharma companies not to bribe doctors with lavish gifts, travel junkets, or goodies – keeping it professional and informative.

You know what’s funny, though? For years, UCPMP was voluntary . It was more of a gentleman’s agreement than a law. Essentially, pharma companies had the choice to not be unethical in how they approached doctors.

New code, new ban, and industry pushback

To further clean up these practices, the Indian government updated the UCPMP in early 2024 — giving it more teeth. What was once entirely voluntary was now given a “quasi-statutory” status. The code now officially applied to pharma associations and companies, and an oversight committee was put in place as a watchdog. The updated code banned obvious freebies, like sponsored foreign junkets, luxury hotel stays, or personal gifts.

But then, the Health Ministry went even further. In its latest move, it passed an outright ban on MRs from entering central government hospitals. In late May 2025, the DGHS issued a circular to all these hospitals — in essence asking them not to give entry to any medical representatives. Any information they needed to share could be sent over email, or through other digital channels.

The government wanted to indicate a ‘zero tolerance’ policy towards medical representatives. Having drug reps popping into wards and OPDs was causing disruption — doctors’ time was being eaten up, patients were kept waiting, and there was potential for “ undue influence ” on prescriptions. And so, they would be banned outright. Any information they needed to share could be sent over email.

The IPA quickly raised its voice in protest. The alliance argued that the ban overshot its mark. Even if there was a case that these representatives should maintain discipline, they shouldn’t shut out interactions completely . In a letter to the Health Ministry, the IPA stressed that MRs actually serve a ‘ critical educational role**’** in healthcare. A blanket ban, it warned, could “impact the growth of the pharmaceutical sector” and lead to job losses for thousands of MRs.

Instead, they suggested a compromise: allow MRs in, but create a structure around their visits: like setting specific days or hours for these interactions, so they don’t interrupt clinics.

Loopholes, gray areas, and why the policy might not stick

Here’s where things get tricky: On paper, banning MRs from hospitals and enforcing marketing codes sounds great. In practice, they come with major weak spots:

- Enforcement remains a challenge: Our parliament itself hasn’t passed a law on pharmaceutical marketing. The UCPMP still isn’t law — it’s functionally just a government circular. Its “quasi-statutory” means it’s kind of enforceable, but its scope is limited. It doesn’t have a strong monitoring mechanism, or a regulator that can prescribe heavy penalties. Its enforcement still relies on industry bodies policing themselves.

- It is not the first time: This isn’t the first time the government has tried to curb MRs in hospitals. A very similar order also went out in 2023 — essentially telling central hospitals to completely curtail MR visits, while information on new therapies would have to be sent via email. The very fact that we’re again seeing the same directive in 2025 suggests the 2023 order was largely ignored.

- Other types of measures have failed too: There’s already a rule (dating back years via the Medical Council of India, now NMC) that government doctors must prescribe medicines by their generic name, not by brand. In theory, this should have solved the problem already. For instance, if a doctor can only write something like “ibuprofen 400mg” instead of a specific brand to look for, they couldn’t possibly show bias toward any one company. Only, enforcement of this rule, too, has been patchy. Government doctors caught pushing brands could technically face action, but in reality, this seldom happens.

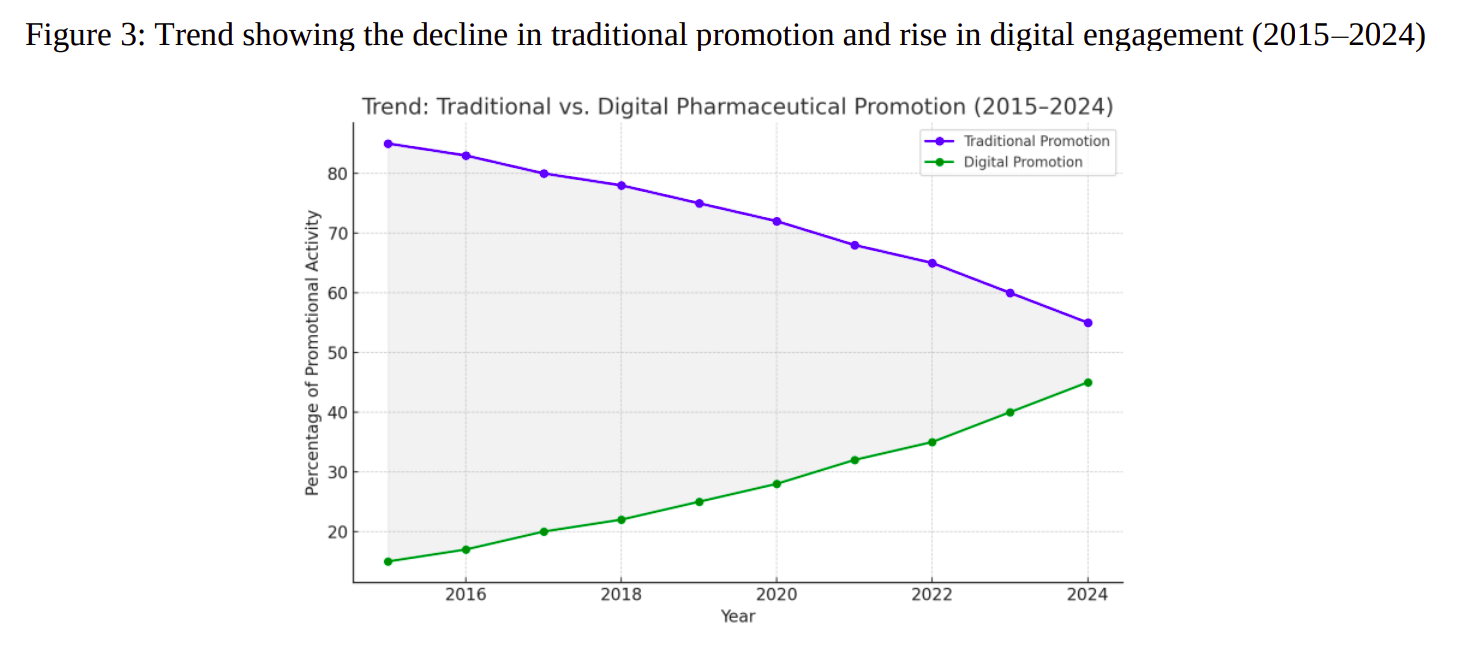

- Digital influence is influence too: Banning physical visits by reps doesn’t eliminate pharma influence. It merely changes the channel through which doctors are influenced. The 2025 directive itself acknowledges that MRs can still share info digitally — via emails, Zoom calls, or WhatsApp groups. And that’s precisely what they’re doing. In fact, modes of digital promotion are slowly becoming more and more prominent, as per a recent study.

Influence, in short, finds a way. The playing field may shift, but the game of getting a doctor’s attention isn’t going to vanish.

Because of all of this, some see the ban as more performative than practical . It’s a bold announcement, it’s hard to actually implement. Without strong follow-through, both the UCPMP guidelines and the hospital rep ban could end up as well-intentioned memos that gather dust, while the real dynamics of drug promotion continue with a few tweaks.

But there’s one more thing: all of this might be besides the point .

Why access matters more

We spoke to a few folks in the industry while trying to understand this story. And that gave us a completely different perspective on this: when it comes to government hospitals, the presence or absence of MRs might not matter too much anyway. The availability of medicines in such hospitals runs on a completely different system, after all.

Government hospitals typically procure their medicines through a tender system. Essentially, they invite bids for drugs — based on the chemical , instead of the brand . These purchases are made in bulk from whichever company offers the best price while meeting quality standards. That means for each medicine (say, paracetamol), the hospital might stock one or two selected brands that won the supply contract. These drugs are then given free or at very low cost to patients via the hospital pharmacy / dispensary.

Now, we aren’t saying nobody tries to game this system: only that sending MRs to doctors would do little in this regard.

If a doctor in a public hospital writes a prescription, they usually either use the generic name or the name of whatever brand is stocked in-house for that medicine. Most patients at these hospitals will get the medicine right there, free of charge.

Consider what that means for an MR: If their company’s brand isn’t the one the hospital stocks, no amount of schmoozing with doctors will get patients that brand – it’s simply not available in the building.

Companies know this. There’s little point in heavily marketing a brand to doctors if their hospital doesn’t stock it. If a government hospital only carries ABC’s diabetes drug, for instance (because ABC won the tender), an MR from XYZ Co. might try to promote their version — but it would make no sense. Doctors simply can’t prescribe it for in-hospital use. Poorer patients that rely on free medicines are unlikely to go outside and buy a different brand. In fact, our source told us that many pharma firms don’t even bother sending reps to some government hospitals if they aren’t suppliers there. It’s not worth the effort.

What this means is that where public hospitals are concerned, access and availability trump promotion. Pharma companies make their money at the point of procurement , not prescription . If a pharma company wants its drug used there, winning the tender or getting on the hospital’s formulary is the real prize – not chatting up doctors.

The bottomline

At the end of the day, this back-and-forth between the government and the pharma industry feels a bit like running in circles.

The government is banning something that, in theory, it already banned before and arguably can’t fully police. The IPA is pushing back to protect a practice that might not be as critical in government settings as they claim. Both sides insist they have patient interest at heart – the government cites ethics and unclogging hospital hallways, while pharma companies talk about keeping doctors informed for better patient care.

To us, though, it looks like both sides are talking past each other.

The core issues, meanwhile, remain in limbo: How do we ensure doctors get unbiased information on new treatments? How do we enforce ethical marketing without real legal teeth? How do we make sure patients, especially in public hospitals, get the best medicines without hidden commercial agendas creeping in?

Unfortunately, for this story, we have more questions than answers.

India’s Tyre Giants Navigate a Bumpy Ride

There’s something brutal about the tyre business.

This is a sector that we looked at for the first time, and we found it extremely fascinating. And that’s because of just how dependent these businesses are on what’s happening outside. See, if you’re a tyre manufacturer, your two biggest cost inputs — natural rubber and crude oil derivatives — can swing by as much as 30% in price in just a few months. You can do nothing to control that, short of some smart hedging. You’re also playing second fiddle in an industry where car manufacturers, and not tyre manufacturers, call the shots.

And yet, you’re expected to make decade-long bets on factory locations, technology platforms, and market positioning that will determine whether your company thrives or struggles for years to come.

This fundamental tension defines India’s ₹90,000+ crore tyre industry turnover. Companies must navigate quarterly commodity price shocks while simultaneously making massive strategic choices about the future of Indian mobility. Do you bet big on electric vehicle tyres when EVs are still under 2% of sales? Should you invest heavily in truck radials when global freight demand is flagging? Can you double down on exports in an era when trade policies can change overnight?

The interesting part isn’t just that these companies face this challenge — it’s how differently each major player is choosing to navigate it. While they all make tyres, they’re essentially making very different bets about what Indian transportation will look like in 2030. And those choices are already showing up in their results.

What’s happening in the tyre industry

Before we go into the individual companies, let’s set some context.

The tyre business is particularly challenging because of just how many crucial factors lie completely outside management control, and yet can make or break annual performance. Here are just some of what the industry is seeing:

The raw material roulette

Tyres businesses are heavily dependent on commodity prices . 80-85% of a tyre’s raw material costs come from natural rubber, synthetic rubber, carbon black, and steel wire.

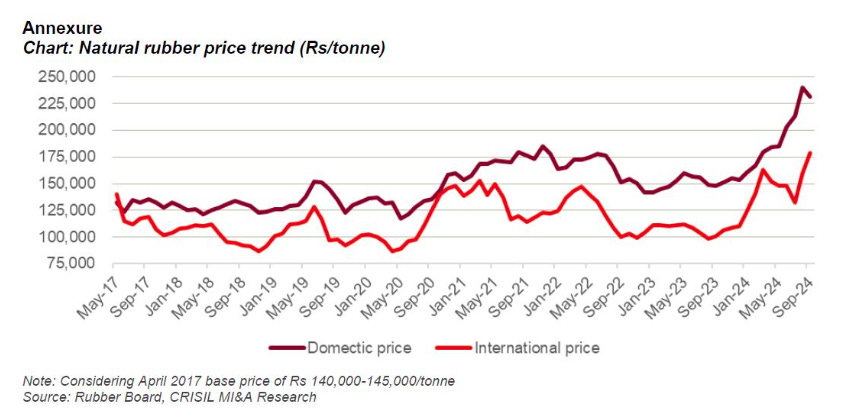

Rubber, specifically, is a big deal. If you want a quick-and-dirty metric to track this sector, look at natural rubber prices in Kerala, and you’ll get a good sense of where its margins might be. That said, Kerala alone can’t produce enough rubber to feed the industry. India produces only ~800,000 tonnes of natural rubber against the consumption of ~1.3 million tonnes. That means the tyre industry’s fate is driven, to a great degree, by global rubber prices.

Recently, this became a major issue for the industry. In late 2024, rubber prices suddenly rose by 33% to cross ₹200 per kg for the first time in a decade. Within a single quarter, tyre company margins saw terrible pressure. You can see the impact of this spike clearly in their results, with most of them seeing margins fall.

The industry’s many mood swings

Tyre companies don’t have a primary market of their own. 30% of their business comes from new vehicle fitment, which is directly dependent on the plans of automotive companies. And so, tyre companies constantly try to predict and ride the automotive industry’s cycles. This makes the business uniquely difficult to manage.

The other 70% of tyre revenue comes from replacement demand, which is inherently unpredictable. That depends on how long tyres last in real-world conditions — something influenced by everything from usage patterns, to road quality, to weather. Different companies might look at different dynamics to run their business. For instance, while JK Tyre, with its heavy commercial vehicle focus, is more sensitive to freight and infrastructure cycles. CEAT, strong in two-wheelers, correlates with fuel prices and urban mobility patterns.

Lately, there’s a new game these companies must play. As people transition to electric vehicles, they need to develop entirely new tyre technologies. After all, EVs are heavier, quieter, and deliver instant torque. But the question is: how do you plan investments into EVs? After all, EVs still represent a small fraction of car sales today, and it’s hard to predict when adoption will accelerate. Bad timing, here, could hurt a company’s prospects.

Tyre protectionism

India’s regulatory regime does a lot to shape the industry.

In June 2020, India moved tyres to the “restricted” import category. Effectively, companies now require licenses for tyre imports. Until this point, Chinese tyres had captured 12-15% of India’s replacement market pre-2020. But this policy insulated our market, protecting India’s domestic tyre manufacturers from cheap Chinese imports. We also placed anti-dumping duties on Chinese truck and bus tyres, helping our domestic industry corner the market even further.

At the same time, though, the government has also made Indian tyres expensive, which could cut down demand. The GST rate on tyres is 28%, making replacement tyres expensive. Users, as a result, are pushed to delay tyre changes. This is a safety concern that the industry continues lobbying against.

Four companies, four strategic approaches

To understand how India’s tyre sector is handling this complexity, we picked four companies that together control 70-75% of the market. Each represents a different strategic approach to the industry.

- There’s MRF, the undisputed king with nearly 30% market share, built on dominating India’s domestic replacement market.

- Apollo Tyres is a global sophisticate, generating significant revenue from Europe through a genuinely international manufacturing presence.

- JK Tyre is a commercial vehicle specialist, with most of its 15% market share coming from truck and bus tyres.

- CEAT is the innovation-focused challenger, which is pushing up its 10-15% market share with Industry 4.0 manufacturing and smart tyre technologies.

Together, these four offer different answers to the same fundamental question: how do you anticipate and survive India’s rapidly evolving mobility landscape?

MRF: The Fortress India Strategy

MRF, arguably India’s tyre incumbent, has essentially built itself a strong domestic fortress. The company operates nine plants across India and can pump out 85 million tyres annually. More than 90% of its revenue comes from domestic sales. It relies on the country’s largest dealer network for the job — with 5,000+ dedicated dealers — and it perhaps has the strongest brand equity in replacement markets.

Last quarter was a reasonably strong one for the company. MRF closed Q4 with a revenue of ₹7,075 crore — up 11% year-on-year. Of this, ₹512 crore came to the company as its net profit, a rebound of 29% from the previous quarter. Over the full year, MRF crossed ₹25,000 crore in revenue while maintaining solid profitability.

Unfortunately, we’re flying slightly blind while trying to decode MRF’s business. While its rivals rolled out elaborate investor presentations with colourful charts and graphics, and then followed those up with lengthy investor calls, from what we can see, MRF did none of that this quarter. It just put out the raw numbers and little else.

If you’ve come across any management commentary, though, let us know in the comments!

That said, here’s what we can tell.

Impressively, MRF kept profitability high this year despite rubber prices jumping by over 33% over the year. Perhaps because of MRF’s premium positioning, it weathered this storm better than its peers.

From what we can tell, the company isn’t thinking of reinventing itself or changing its business very significantly. The company is doubling down on what they do best — expanding domestic capacity and maintaining its performance testing capabilities. Their ₹4,500 crore investment in a new plant in Gujarat signals this continuity — while the company is expanding its manufacturing base outside South India, its core operations remain the same. India’s market is big enough to sustain focused growth, they believe, and by catering to domestic replacement demand, they can hold on to where they are.

Although MRF recently began catering to electric vehicles as well, this presence is fairly nascent at the moment. It even seems to be waiting to see which EV segments take off before committing completely to the segment.

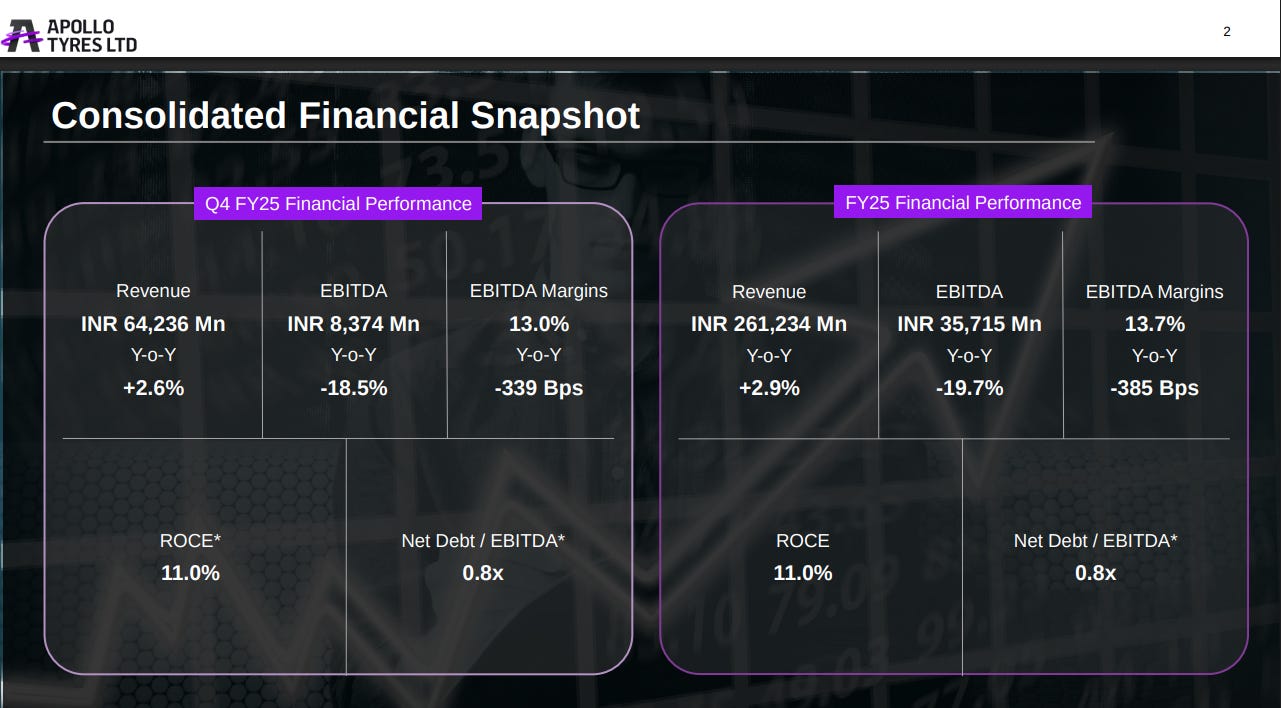

Apollo Tyres: The global integration play

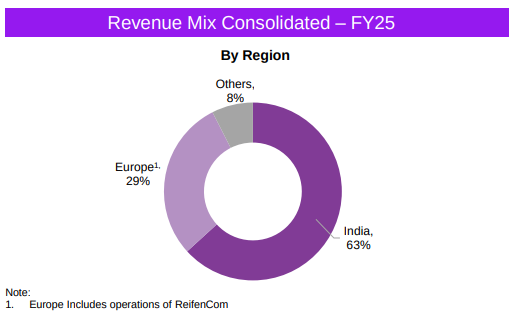

In contrast to MRF, Apollo isn’t fixated on the Indian market. It has a ‘dual-continent’ approach — its business is split between India and Europe, allowing them to serve premium European markets with local production, while leveraging Indian cost advantages to reach emerging markets.

Mind you, Apollo isn’t just exporting to Europe; they have a genuinely international manufacturing presence. Beyond its five plants in India, the company runs two plants in Europe — in the Netherlands and Hungary. 63% of its revenue comes from India, while 29% comes in from Europe.

Recently, the company’s performance has been decidedly subdued. Apollo saw a Q4 revenue of ₹6,424 crore, with a net profit of ~₹185 crore. This is a little more than half its ₹354 crore profit in the same quarter last year. For FY 2024-25, Apollo’s revenue grew slightly, by 3%, to ₹26,123 crore. Its profitability took a hit, however, with annual profits falling from ₹1,722 crore to ₹1,121 crore — largely because its costs shot up.

Apollo candidly acknowledged its below-average performance in its earnings call. According to its Managing Director, Neeraj Kanwar:

“So like I mentioned to you, yes, this year has been very, very challenging. We have underperformed, but the green light is that we have put a lot of initiatives in the field.”

What held it back?

There are a few things that Apollo was shuffling around this quarter. For one, the company pulled back its low-margin OEM business. It also faced capacity constraints in Hungary, which impacted European volumes. Most interestingly, though, the company spent some time reorienting itself. It shifted from what it described as a ‘regional’ to a ‘global’ operating model — something that was a long time coming. If that assessment is right, this underperformance could just be a slight hiccup.

“We have restructured in the month of May, June, where we went from being a regional company to more global. And it has taken us time. And that’s why maybe one of the reasons for the underperformance is there.”

Elsewhere, Apollo has made a few moves. It was first among its peers to come out with EV-specific tyres, for instance. It came out with its ‘Amperion’ range for cars and ‘WAV’ for two-wheelers — earning a 5-star fuel efficiency rating. While this is partly to stay relevant in Europe, which is far ahead of India in shifting to EVs, Apollo also seems to have a long bet that urban India will adopt EVs.

This is also evident in its approach to innovation. Apollo has been investing in dual R&D centres — in Chennai and the Netherlands — to bridge European technology with India’s manufacturing economics. If this bet works out, it could compete with global players on technology and quality, and not just price alone.

All in all, Apollo’s quarterly performance has been sub-par, but it points to some reasons for hope next time around:

“we have recently hired a chief supply chain officer. He is Indian, coming from a very large German company. We have recently hired Rajeev Kumar Sinha, who has come as a chief of manufacturing, who comes with an expertise of Cipla for the past nine years. So, these are the two new joinees that have come in. And with that, it does take time for people to settle in and to start performing.

So, like I said in my earlier answer, Q1 is going to be our quarter. Hopefully, we will come back with double digit growth.”

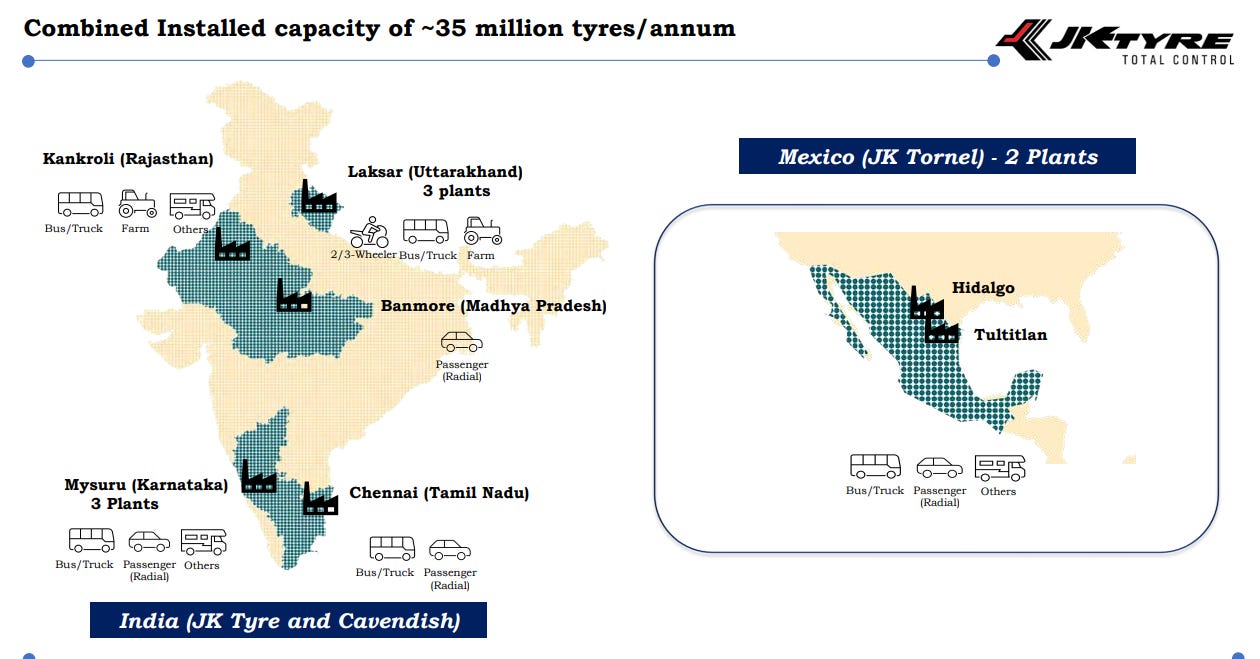

JK Tyre: The Americas bridge strategy

JK Tyres has positioned itself very differently from either MRF or Apollo: it’s a commercial vehicle specialist. In fact, JK Tyre was among India’s first companies to produce truck radials.

Like Apollo, JK Tyres has diversified its geographic market too: serving India and the Americas simultaneously. The company operates eleven manufacturing plants, and while nine are in India, two of those, housed under the JK Tornel brand, are in Mexico . This gives JK Tyre a unique bridge to markets across the Americas.

This is why it has such a formidable export presence. The company exports to over 100 countries and has specialised in giving global market access to cost-effective Indian manufacturing.

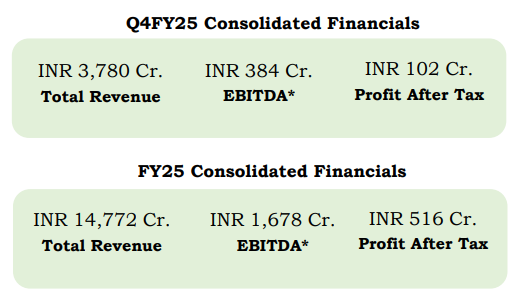

More immediately, the quarter gone by, for JK Tyre, was a dismal one. It reported Q4 revenue of ₹3,780 crore with net profit of ₹102 crore, down about 31.4% year-on-year. The quarter that came before was even worse — profits had plunged 62% due to rubber price spikes. It recovered somewhat from those lows by year-end. Its full-year revenue, eventually, was roughly ₹14,772 crore.

Looking ahead, though, JK Tyre believes it’s heading into FY26 with an optimistic demand outlook — especially for tyre replacements and exports. But its numbers might not look too good. The company’s sitting on particularly expensive inventories, and that could make it look less profitable. As the company said on its earnings call:

“In Q1 and Q2, we had taken some strategic stocking of the material which helped us to evade some of the cost in Q2. But then that strategic inventory had depleted and Q3 saw the full impact of the raw material. Yes, there has been a major impact on EBITDA margins due to higher raw material cost in Q3. It’s only in the short term — the working capital borrowings have gone up in the last nine months period and this is to maintain the strategic inventory and also some finished goods inventory were accumulated. But this is going to get corrected in next one or two quarters.”

The company’s capacity utilisation is rather high, especially in passenger car radials. If it wants to grow its volumes, it must focus on quickly commissioning upcoming expansion projects. Additionally, the firm’s Mexico operations face foreign exchange headwinds, though management plans to boost exports to North America to offset local softness.

The company is exploring EV applications for commercial vehicles and has been working on smart tyre technologies and premium material applications for its commercial vehicle focus. Their bet: commercial vehicle growth and export markets will drive long-term value, leveraging their early expertise in truck radials.

CEAT: The Smart Manufacturing Bet

CEAT is a company built around a focus on manufacturing excellence rather than scale. It does have decent scale — the company operates six plants in India, producing 41+ million tyres annually. Their Chennai plant (opened 2020) was designed from the ground up for passenger car and two-wheeler radials, targeting OEM customers like Hyundai and Kia.

CEAT delivered a strong quarter this March, despite taking a small dent to its profitability. CEAT managed Q4 revenue of ₹3,421 crore — up 14.3% year-on-year. Its net profit for the quarter fell marginally, however, from ₹102.3 crore to ₹98.7 crore. The full year saw revenue growth of 10.7% to ₹13,218 crore, though annual profit dropped to ₹471 crore from ₹635 crore last year, as its margins fell.

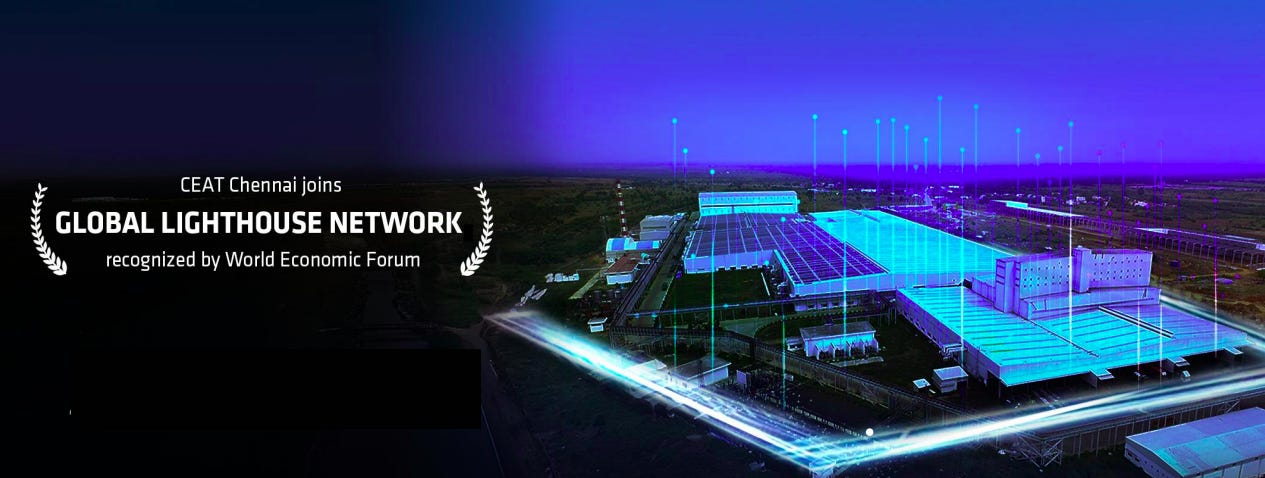

Elsewhere, though, there was more exciting news for the company. CEAT became the first tyre company globally to receive the World Economic Forum’s “Lighthouse” certification. Both its Halol and Chennai plants were inducted into the ‘Global Lighthouse Network’ — a recognition that it was using ‘Industry 4.0’ technologies like advanced analytics, machine learning, and predictive maintenance.

Through this technology push, CEAT’s trying to compete with global giants on their own turf. It is essentially betting that superior manufacturing and innovation can overcome scale disadvantages, allowing them to punch above their weight, in an industry where bigger has traditionally meant better.

The company also pulled off a big acquisition recently, acquiring ‘CAMSO’ to strengthen its off-highway tyre portfolio. That said, the results won’t show up immediately. CEAT’s management noted that full benefits from the integration will take up to two years:

“With the integration of Camso right away in FY '26, we’ll hit the target of 25% - 26% saliency of international business. So, integration is progressing well, but we believe the full benefits in terms of cost efficiencies and portfolio synergy will likely play out over the next 18 to 24 months.”

Looking ahead, CEAT enters FY26 with a cautious outlook. It anticipates high single-digit revenue growth and stable margins, amidst major headwinds. Export demand remains soft, while recent price corrections in key segments like truck/bus radials and two-wheelers put pressure on what it can earn. And so, despite its ongoing investments in capacity and technology, the company’s near-term growth is expected to be gradual.

The Bottom Line

If you’re trying to figure out how to invest in any of these companies, it’s not enough to just look at three months’ results. You need to evaluate how prescient each of these are in how they see the auto industry years from now.

MRF is betting that domestic replacement demand will remain king, and India’s market is big enough to sustain focused growth. Apollo is betting that Indian tyre companies can be global players, competing on technology and quality. JK Tyre is setting itself apart, betting on commercial vehicle growth and export markets. CEAT is betting that technology and manufacturing excellence will differentiate them in an increasingly competitive market.

In a country adding millions of vehicles annually, transitioning (slowly) to electric mobility, and expanding road infrastructure, all four companies are wrestling with the same strategic puzzle: which parts of the tyre value chain will be most profitable to own over the next decade?

The rubber, quite literally, is still hitting the road on that answer.

Tidbits

- Apple Vendors in India Cross 20% Local Value Addition as iPhone Exports Touch ₹1.5 Trillion

Source: Business Standard

Apple’s key vendors in India — Tata Electronics, Foxconn, Pegatron, and Wistron — have surpassed the 20% domestic value addition (DVA) mark, signaling a shift in the country’s role in global electronics manufacturing. According to government records, this threshold was achieved as the companies ramped up local operations including assembly, testing, and localisation of accessories. In FY25, iPhone exports from India reached ₹1.5 trillion, reflecting a 76% year-on-year increase. This implies approximately ₹30,000 crore of value was generated within India, assuming a 20% DVA. Other players like Samsung India and Padget Electronics have also crossed this 20% benchmark. The development marks a notable improvement from just a few years ago, when most vendors had DVA levels in low single digits. While China and Vietnam continue to have higher DVA percentages in some categories, India’s progress underlines growing local capabilities.

- JLR Cuts FY26 Margin Forecast to 5–7%, Tata Motors Shares Drop Nearly 5%

Source: Reuters

Jaguar Land Rover has revised its EBIT margin guidance for fiscal 2026 to 5–7%, down from its earlier forecast of 10%. This updated outlook also falls below the 8.5% margin the company reported in the previous fiscal year. The downgrade comes amid rising uncertainty in the global auto market, particularly due to potential 25% tariffs on foreign-made vehicles in the U.S. market—where JLR generates over a quarter of its sales. In response to the tariff threat, the company has temporarily paused shipments to the U.S., its second-largest market. Notably, JLR has no manufacturing presence in the U.S., unlike rivals such as BMW and Mercedes-Benz. The announcement has raised concerns over the near-term profitability of Tata Motors, which relies significantly on JLR for its consolidated earnings.

- Godrej Properties Acquires 14-Acre Bengaluru Land for ₹1,500 Crore Housing Project

Source: Business Standard

Godrej Properties has acquired a 14-acre land parcel in Hoskote, East Bengaluru, for the development of a premium residential project. The company expects to generate approximately ₹1,500 crore in revenue from this project, which will offer around 1.5 million square feet of saleable area. This acquisition strengthens Godrej’s presence in East Bengaluru, a market the company considers strategically important. The announcement follows a similar move earlier this month, where Godrej acquired another 14-acre parcel in Pune for ₹800 crore, targeting a revenue potential of ₹4,200 crore across 3.7 million square feet. The company has not disclosed the cost of the Bengaluru land acquisition.

- This edition of the newsletter was written by Kashish and Vignesh.

Join our book club

Join our book club

We’ve started a book club where we meet each week in JP Nagar, Bangalore to read and talk about books we find fascinating.

If you think you’d be serious about this and would like to join us, we’d love to have you along! Join in here.

Have you checked out The Chatter?

Have you checked out The Chatter?

Every week we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Go check out The Chatter here.

“What the hell is happening?”

We’ve been thinking a lot about how to make sense of a world that feels increasingly unhinged - where everything seems to be happening at once and our usual frameworks for understanding reality feel completely inadequate. This week, we dove deep into three massive shifts reshaping our world, using what historian Adam Tooze calls “polycrisis” thinking to connect the dots.

Frames for a Fractured Reality - We’re struggling to understand the present not from ignorance, but from poverty of frames - the mental shortcuts we use to make sense of chaos. Historian Adam Tooze’s “polycrisis” concept captures our moment of multiple interlocking crises better than traditional analytical frameworks.

The Hidden Financial System - A $113 trillion FX swap market operates off-balance-sheet, creating systemic risks regulators barely understand. Currency hedging by global insurers has fundamentally changed how financial crises spread worldwide.

AI and Human Identity - We’re facing humanity’s most profound identity crisis as AI matches our cognitive abilities. Using “disruption by default” as a frame, we assume AI reshapes everything rather than living in denial about job displacement that’s already happening.

What the hell is happening?

What the hell is happening?Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()