Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- The metal of the century?

- Is Europe in deep trouble?

The metal of the century?

Coal India spent seven decades digging through different parts of India for coal. But all of a sudden, it’s trying to play a new game. Recently, it’s been trying to get its hands on salty lakes in Argentina.

We get it: that’s a weird pivot to make.

But it makes sense. The thing it’s after could be the most important metal of this century: Lithium. That’s what we’re going to talk about today.

Lithium has been around for ages. We first discovered it two centuries ago and found some minor uses for it. It can help calm down severe mental disorders. It makes glass-working easier. All this while, it was considered a nifty, but not revolutionary metal.

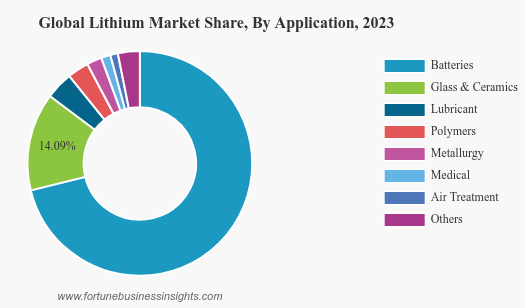

That’s changed in the last decade. We found a new use case for Lithium that’s overpowered everything else: batteries.

Source: Fortune Business Insights

If we want to escape climate change, we’ll have to run everything from cars to homes to factories on electricity. For that, we’ll need batteries: lots of batteries, of every size imaginable.

Most of those batteries will rely on Lithium. It’s easy to see why. The “charge” in a battery, at the end of the day, comes from tiny, charged particles. The smaller these particles are, the more charge a battery can hold. And Lithium particles are really small. It’s the lightest metal in existence — it even floats on water. It’s physically impossible to store charge more efficiently.

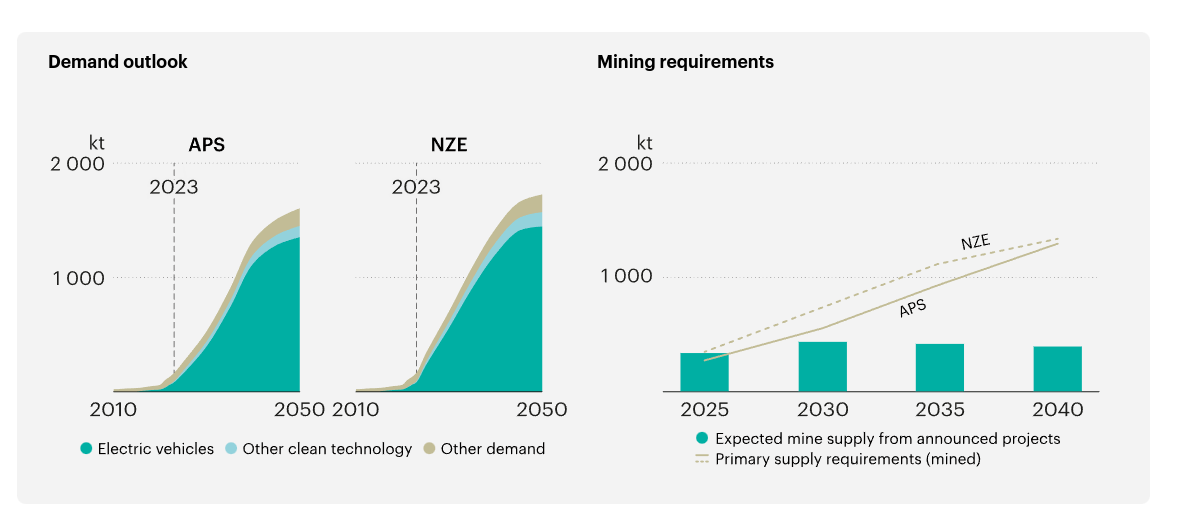

This is why we’re going to need lots of Lithium in the years to come. Most of this demand will come from electric vehicles (EVs) — and for good reason. Car batteries need to be powerful enough to move an actual car around for hundreds of kilometers while being compact enough to still fit in one. Lithium alone can deliver on those fronts. At least until the early 2030s, the demand for Lithium is projected to grow substantially.

Source: IEA

So Lithium will be of crucial importance. But that doesn’t mean investing in Lithium is straightforward. The global Lithium market is still young and volatile, and there are many surprises ahead. If you want to figure out how things are moving, here are a few ideas to keep in mind.

One, the Lithium market is still bumpy .

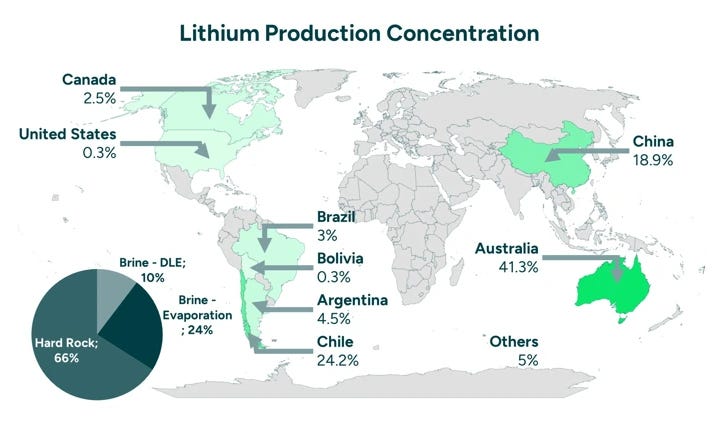

We’re still in the early stages of mining Lithium. Today, the industry is heavily concentrated in the hands of a few early movers. 90% of the world’s Lithium supply comes from just four countries — Australia, Chile, Argentina, and China. More than half of that is controlled by five companies.

But new sources are being added. And every time a new source of Lithium becomes active, the entire market changes. There’s a sudden surge in supply, creating a glut. Prices crash.

Back in 2021-22, there was a big ramp-up in the demand for EVs. It took some time for suppliers to adjust to this demand, and in the meantime, prices soared. But then, when new supply came in, prices suddenly cratered — falling by 86%. They have never really recovered since. Many mines have been closed because of this collapse in prices.

Source: Trading Economics

We’re likely to see this trend play out repeatedly until the market matures. How price trends play out, over this time, is anyone’s guess: it’s a race between how much Lithium we can mine, and how many batteries we need. The volatility in both demand and supply is likely to only come down by the end of this decade.

Two, we’re yet to completely figure extraction out.

Lithium is either found in rocks in the ground — like most other metals — or in salty lakes. We’re good at extracting Lithium from rocks. More than two-thirds of our supply currently comes from there.

But we’re still really bad at extracting Lithium from lakes. That process is still extremely inefficient and time-consuming. There are some promising technologies in the works, but nothing that we can really deploy at scale.

That’s a problem, for two reasons. One, it means a lot of the Earth’s Lithium is inaccessible to us. Two, mining is a controversial process, with tremendous political and regulatory risks. Small changes in the law can completely wreck decade-long mining plans. Mining requires political stability and predictable environmental compliance regimes — which need not always be around.

The future of our Lithium supply depends greatly on the extent to which we’re able to diversify away from rock-based mining.

Three, the Lithium market is actually two products: Lithium Carbonate and Lithium Hydroxide.

Lithium Carbonate is cheaper to extract, easier to handle, and easier to work with. Most new refineries begin with extracting Lithium Carbonate. On the other hand, Lithium Hydroxide is volatile, and can’t be moved around too much after extraction. It’s generally just a harder chemical to work with.

But here’s the catch: Lithium Hydroxide makes better batteries that hold their charge for longer.

Both chemicals are currently in use. High-end electric vehicles tend to use Lithium Hydroxide. On the other hand, some cheap Chinese manufacturers are experimenting with Lithium Carbonate batteries. How will things look five years from now? We don’t really know.

The compound that wins out, in the long run, will shape the entire industry. The economics of the industry, its supply chains, and the products it allows for will all be driven by this race.

Four, Lithium doesn’t yet behave like a commodities market.

Rechargeable batteries require extremely pure Lithium. That’s really hard to extract.

Because the Lithium market is extremely young, there are no industry-wide standards that you can blindly rely on just yet. Each battery manufacturer has tremendous market power, and they all impose their own specifications. They maintain their own quality control checks, each of which is likely to be stringent.

A Lithium refiner is somehow expected to navigate this entire maze. Because of this, at the moment, the Lithium market behaves both like a commodities market and a specialty chemicals market.

Refining Lithium is a very specialized function at the moment. It requires a lot of expertise. Most of this expertise — two-thirds of it, in fact — sits in China. The way this expertise is diffused to the rest of the world will shape the future supply chains of the industry.

These are just some of the dynamics in play right now. There are many other complexities that we have neither the time nor the expertise to dive into. But this should give you a flavour of just how many things are currently in flux.

Lithium is certain to have a massive impact on the future of energy and mobility. Given its importance to the green transition, it’s probably the most important metal of the 21st century. From powering your phone to moving an entire car, this tiny element will find its way everywhere.

But this process will not be straightforward. It shall be as volatile as the markets it drives. Prices will rise and fall, technologies will clash, and supply chains will shift. If you’re watching the Lithium market, you’re not just tracking a commodity; you’re watching the future take shape, one charge at a time.

Is Europe in Deep Trouble?

Let’s talk about something that’s been brewing for a while but isn’t making headlines as much as it should: Europe. And spoiler alert, things aren’t looking good for our friends across the pond.

We’re talking about an economy that’s struggling to keep up, and the numbers are pretty damning. But it wasn’t always the case. Post-World War II, Europe was on fire — not literally this time, thankfully — with its labour productivity climbing from 22% of the US level in 1945 to a staggering 95% by 1995. Impressive, right? But fast forward to today, and the European economy feels like it’s hit a wall.

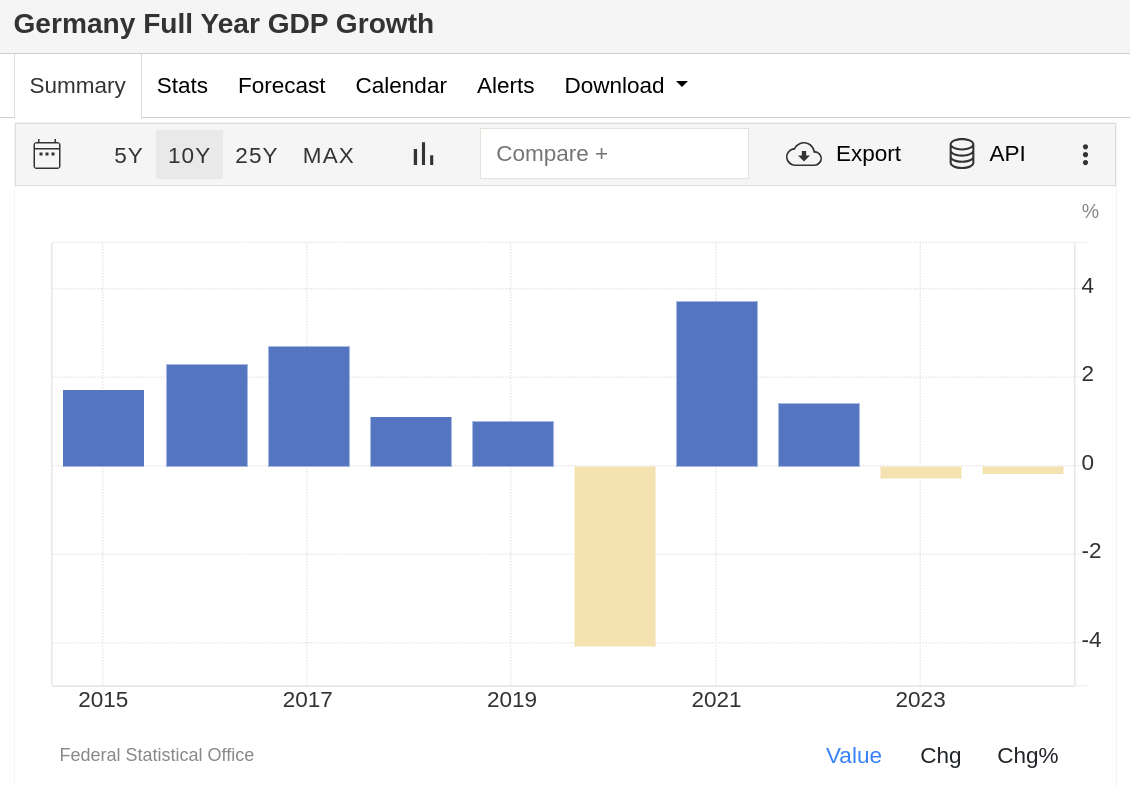

Take Germany, the poster child of European efficiency and innovation. Official figures showed gross domestic product fell by 0.2% last year after dropping by 0.3% in 2023. That is two consecutive years of GDP degrowth.

Source: Trading Economics

Late last year, one of the country’s biggest employers, Volkswagen, agreed with unions to cut more than 35,000 jobs by 2030 after a slump in demand – although the carmaker scrapped plans to close plants for the first time.

Meanwhile, the broader euro area has been stuck with stagnant GDP growth, and real wages have barely moved for over a decade. Compare that to the US, where wage growth is nearly four times higher. Europe’s productivity, incomes, and consumption have been in the slow lane since the 2000s, and the gap with the US is widening. In short: Europe is struggling to grow, and the numbers paint a grim picture.

So, how did it get so bad? Let’s dig into the reasons, and luckily, we have Mario Draghi, former ECB president, to guide us. He recently spoke about this, and his insights are eye-opening.

Why is Europe in a Mess? Two Big Reasons

Draghi points to two big turning points: technology and falling consumption . And while both are serious, the second one — falling consumption — is the real heart of the problem. Let’s take them one by one.

1. The Tech Shock

In the late 1990s, something massive happened: the internet revolution. The US tech sector exploded, creating companies like Google, Amazon, and Facebook that reshaped the global economy. But Europe? It missed the train. While American companies leaned into innovation, Europe’s industrial-heavy economies, like Germany and France, stuck to what they knew: cars, machinery, and old-school manufacturing.

And this matters because tech doesn’t just build shiny apps; it boosts productivity. The US saw its productivity skyrocket, while Europe’s stalled. Draghi highlights that this tech gap has been a major driver of the growing economic divergence between the two regions.

2. Falling Consumption

Now, this is where things get really interesting — and depressing. European households started saving more and spending less. Back in the day, this wasn’t a huge problem because the government and companies made up for it. Here’s how:

- Households saved (a surplus) : Instead of spending their hard-earned money, Europeans preferred to stash it away. Maybe they were cautious, or maybe it’s cultural. Either way, their savings didn’t translate into demand for goods and services.

- Governments and companies compensated (deficits) : To keep the economy running, governments borrowed and spent more, and companies took on debt to invest and expand.

This delicate balancing act worked for a while. But then 2008 hit and everything changed.

The 2008 Turning Point

When the global financial crisis rocked the world, both the EU and the US faced a choice: How do we recover? The US did not hesitate to spend on stimulus. The government poured money into the economy, and the Federal Reserve kept interest rates low to encourage borrowing and spending. The result? American consumers kept spending, businesses recovered, and the economy bounced back.

Europe, on the other hand, took the opposite route: austerity.

- Governments cut spending to control debt.

- Companies tightened their belts.

- Households, already cautious, saved even more.

The result? Europe’s recovery was slow, uneven, and painful. Household consumption never picked up the way it did in the US. And because people weren’t spending, businesses had little incentive to invest. It’s been a vicious cycle ever since.

The Export Reliance Trap

So, if people in Europe weren’t spending, where did growth come from? Exports. Europe leaned heavily on selling goods to the rest of the world. Germany, in particular, became the world’s factory for high-quality cars and machinery. But this strategy had its limits, and now, even exports are in trouble.

Why Exports are Failing

Draghi points out that Europe’s export engine is sputtering, and much of this has to do with Germany. Let’s talk about why:

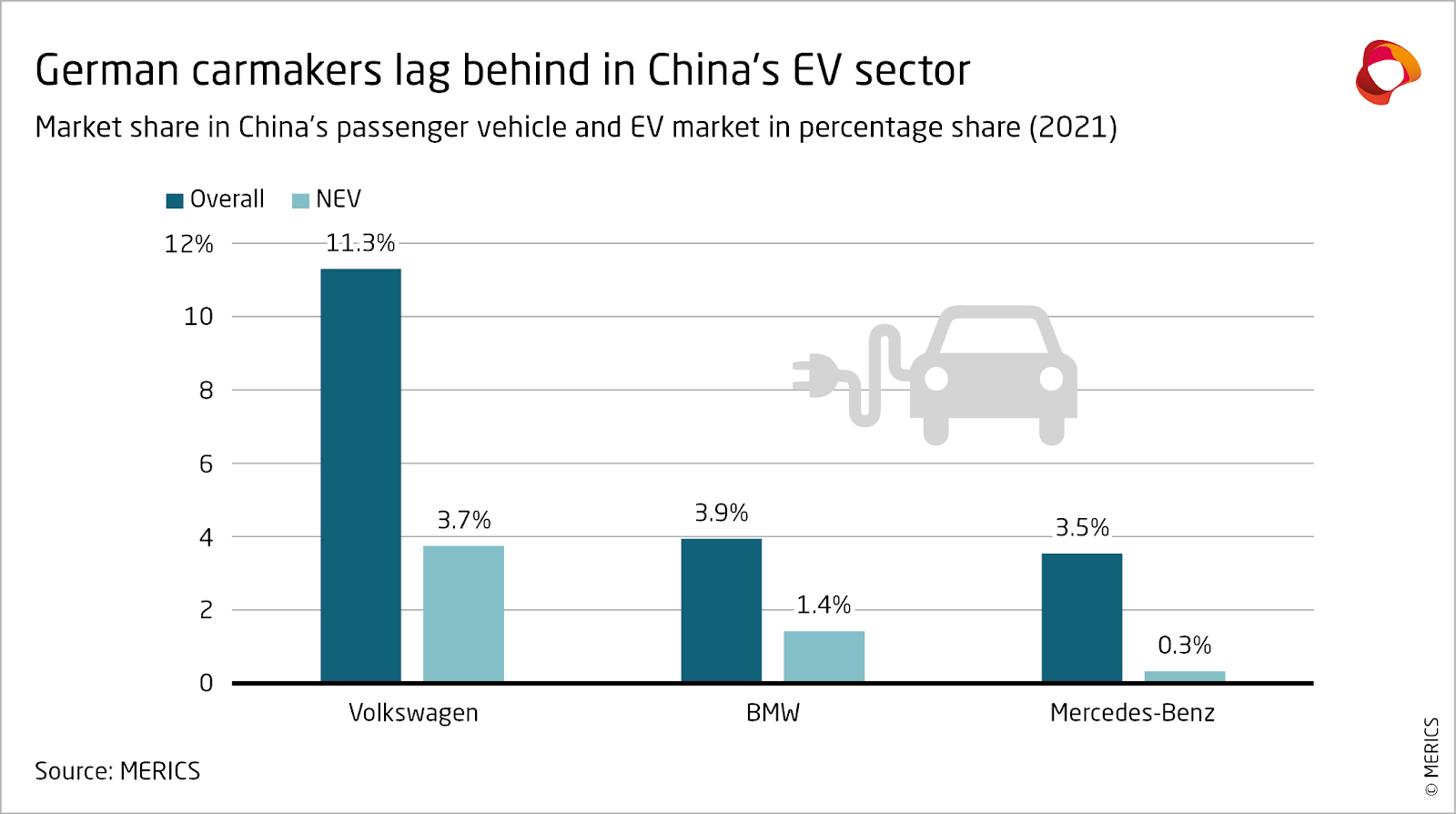

- China’s Evolution : Germany’s car industry relied heavily on exports to China. But over the past decade, China’s domestic car industry has exploded. Today, China produces electric vehicles that are cheaper and often better than what Germany offers. So, not only is China buying fewer German cars, but it’s also competing with Germany in global markets.

Source: Merics.org

- De-Globalization : The world is moving toward de-globalization. Countries like the US are focusing on domestic production and reducing reliance on foreign imports. For Europe, which depends on exports, this is a nightmare scenario.

And here’s the kicker: Germany’s struggles aren’t just its own. Germany’s economy is so central to Europe that when it falters, the entire region feels the impact. If Germany’s industrial base weakens, it’s like taking the engine out of a car.

What Does This Mean for Europe?

So, let’s recap:

- Europe’s household consumption is weak.

- Governments and companies stopped spending after 2008 because of austerity.

- The export engine, which Europe relied on, is now sputtering thanks to China and de-globalization.

Draghi’s conclusion? Europe is in a tough spot. It’s trapped in a cycle of low consumption, weak investment, and now, falling exports. And fixing this isn’t easy.

Why This Matters

Why should you care about Europe’s economic troubles? Well, for one, Europe’s economy is massive. When it struggles, it impacts global trade, investment flows, and even geopolitical stability. Plus, Europe’s challenges offer lessons for other regions, including the US and Asia.

Here’s the big takeaway: An economy cannot thrive without strong domestic demand. Relying too much on exports or government spending is risky because those crutches can disappear. At the end of the day, a healthy economy needs people who are willing and able to spend.

So, what’s next for Europe? Draghi believes the region needs serious structural reforms. That means removing barriers within the EU, improving productivity, and finding ways to boost household consumption. But these changes take time, and Europe doesn’t have the luxury of waiting.

Final Thoughts

Europe’s story is a cautionary tale about what happens when economies fail to adapt. The region missed the tech revolution, leaned too heavily on exports, and chose austerity when it needed stimulus. Now, it’s paying the price.

But hey, let’s not count Europe out just yet. The region has faced tough challenges before and come out stronger. Whether it can do so again depends on its willingness to change.

Let us know what you think: Can Europe turn things around, or is it stuck in this downward spiral? Until next time, take care!

Tidbits

- India’s merchandise trade deficit fell to $21.94 billion in December 2024, aided by $38.01 billion in exports. Sectors like electronics and agriculture outperformed, bolstering April–December exports to $321.71 billion, up 1.6% YoY, signaling resilience despite global challenges.

- The Maha Kumbh Mela is projected to generate ₹2 lakh crore in revenue as 40 crore visitors flock to Prayagraj. Tourism, hospitality, and local businesses like dairy and groceries are set to benefit, highlighting cultural tourism’s role in economic growth.

- Indian companies’ foreign borrowings fell 20.2% in 2024 to $23.33 billion as the rupee depreciated 4.4% and borrowing costs surged. Export-focused firms like Reliance benefit from natural hedges, while others turn to domestic credit amidst rising financial pressures.

-This edition of the newsletter was written by Pranav and Kashish

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]() Join the discussion on today’s edition here.

Join the discussion on today’s edition here.