I had written a few things earlier about investing in gold. Seema all the more relevant today given that Gold seems to be cooling off after that parabolic rally in the last year. While most people think of gold from a returns perspective, it also pays to think of it from a diversification point of view.

Tickertape

Came across this report by the World Gold Council on the diversification aspect of gold. Few highlights

Gold seems to gaining acceptance as an alternative asset among big pools of money

Investors increasingly recognise gold as a mainstream investment; global investment demand has grown by an average of 15% per year since 2001 and the gold price has increased almost seven-fold over the same period.7

A strategic hedge

Our analysis shows gold is a clear complement to equities, bonds and broad-based portfolios. A store of wealth and a hedge against systemic risk, currency depreciation and inflation, gold has historically improved portfolios’ risk-adjusted returns, delivered positive returns, and provided liquidity to meet liabilities in times of market stress.

Gold has outperformed most broad-based portfolio components over the past two decades

Gold as an inflation hedge

Gold also protects investors against high and extreme inflation. In years when inflation was higher than 3%, gold’s price increased 15% per year on average (Chart 4). Over the long term, therefore, gold has not just preserved capital but helped it grow.

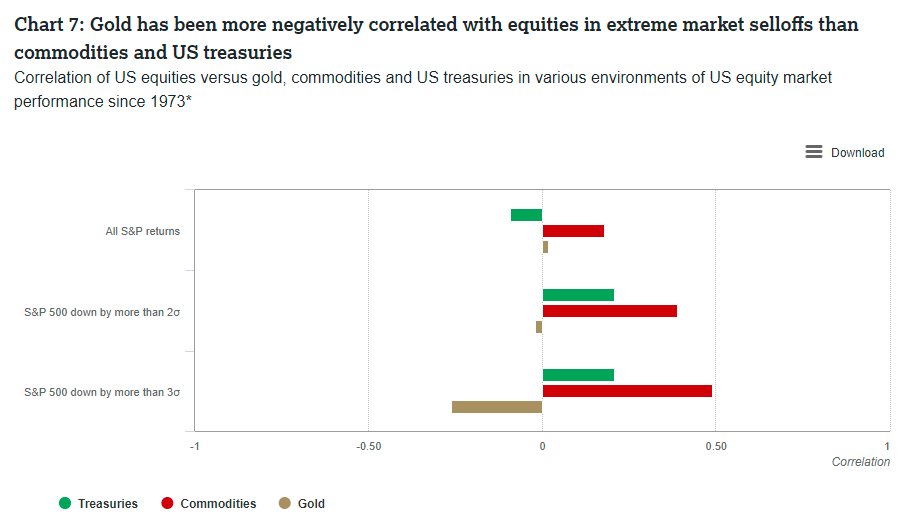

Correlations

Gold is different in that its negative correlation to equities and other risk assets generally increases as these assets sell off (Chart 7). The GFC is a case in point. Equities and other risk assets tumbled in value, as did hedge funds, real estate and most commodities, which were long deemed portfolio diversifiers. Gold, by contrast, held its own and increased in price, rising 21% in US dollars from December 2007 to February 2009.18 And in the most recent sharp equity market pullbacks of 2018 and 2020, gold performance remained positive.19

Huge market

We estimate that physical gold holdings by investors and central banks are worth approximately US$4.8tn, with an additional US$1.1tn in open interest through derivatives traded on exchanges or the over-the-counter (OTC) market (Chart 16a p12).

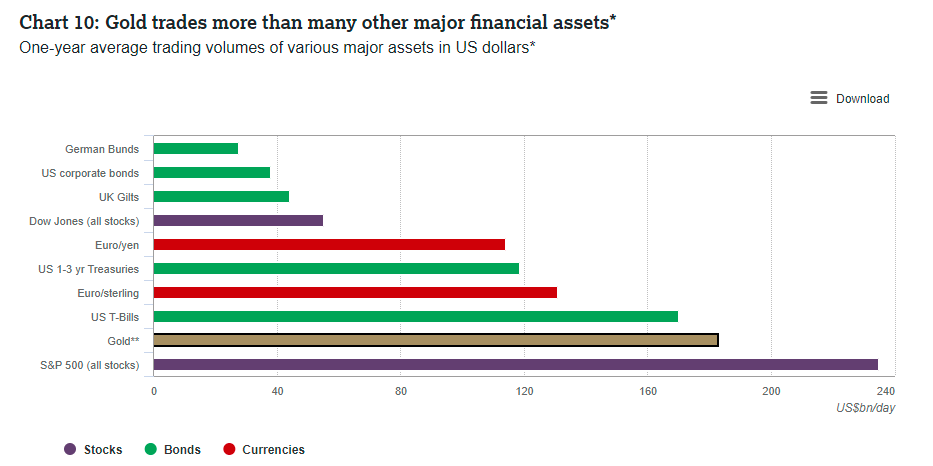

Gold is one of the most traded assets

The gold market is also more liquid than several major financial markets, including US T-bills, euro/yen and the Dow Jones Industrial Average, while trading volumes are similar to those of the S&P 500 (Chart 10). Gold’s trading volumes averaged approximately US$180bn per day in 2020. During that period, OTC spot and derivatives contracts accounted for US$110bn and gold futures traded US$69bn per day across various global exchanges. Gold-backed ETFs (gold ETFs) offer an additional source of liquidity, with the largest US-listed funds trading an average of US$3bn per day (Chart 11).

Gold can enhance risk-adjusted returns

Understanding risk adjusted returns

In addition to traditional back-testing, a more robust optimisation analysis based on ‘re-sampled efficiency’ 20 suggests that an allocation to gold may result in a material enhancement to portfolio performance. For example, gold allocations between 2% and 10% across well-diversified US dollar-based portfolios with varying levels of risk could result in higher risk-adjusted returns (Chart 14, p10).