Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- How Indian Banks Thrived in 2023-24

- The Role of Credit in Economic Growth

How Indian Banks Thrived in 2023-24

The Reserve Bank of India recently released its Trend and Progress of Banking in India 2023-24 report. If you’re wondering why this matters, think of banks as the heart of our financial system. They’re where money flows in as deposits, and they’re the source from which loans pour out to fuel everything from businesses to personal dreams. When banks thrive, the economy follows suit. But when they falter, the ripple effects are hard to ignore.

So, what’s happening with Indian banks? Let’s break it down, piece by piece, and start with the basics.

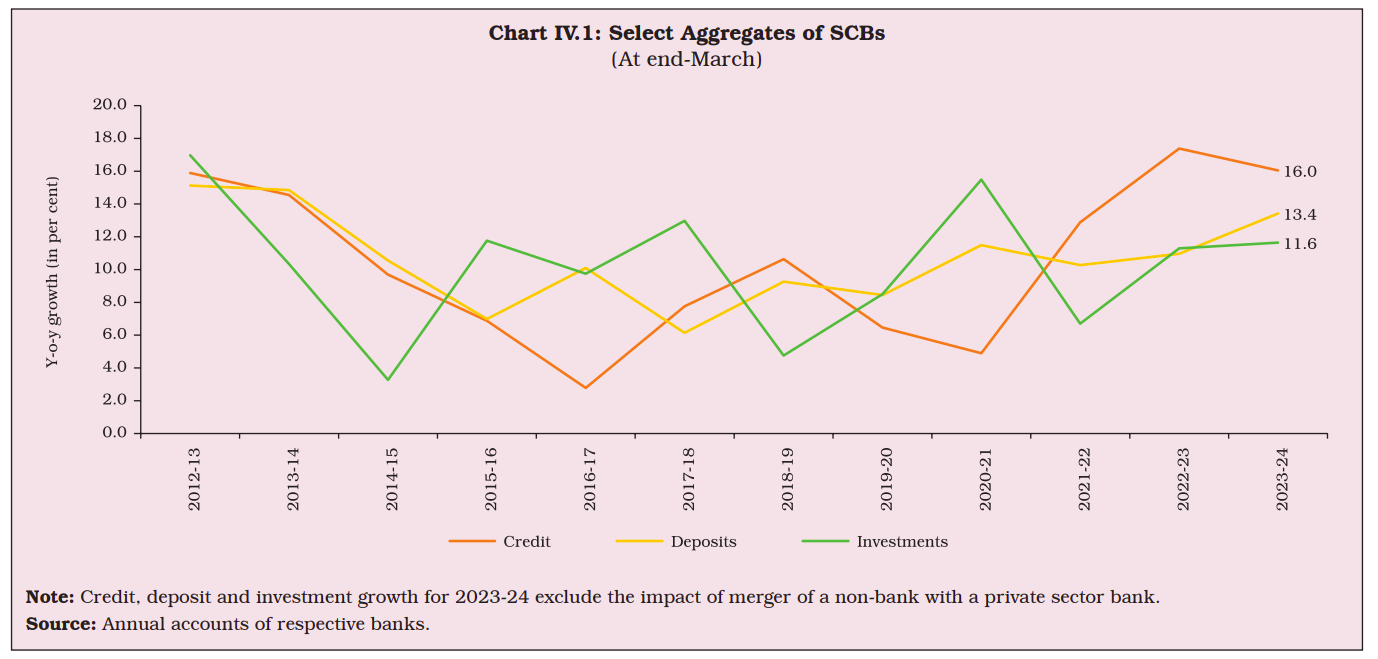

The first thing to know is that deposits and loans—or advances, as bankers call them—are two of the most critical numbers to watch in banking. Deposits are essentially the money people and businesses park in banks, while advances are the loans banks give out. Both are lifelines for the economy.

In the financial year 2023-24, deposits grew by 13.4%, while advances expanded by an even larger 16%. This means banks lent money at a faster rate than they collected it—a sign of an economy that’s hungry for credit. However, this has narrowed the gap between credit growth and deposit growth to just 3.4 percentage points, signaling tighter competition for funds.

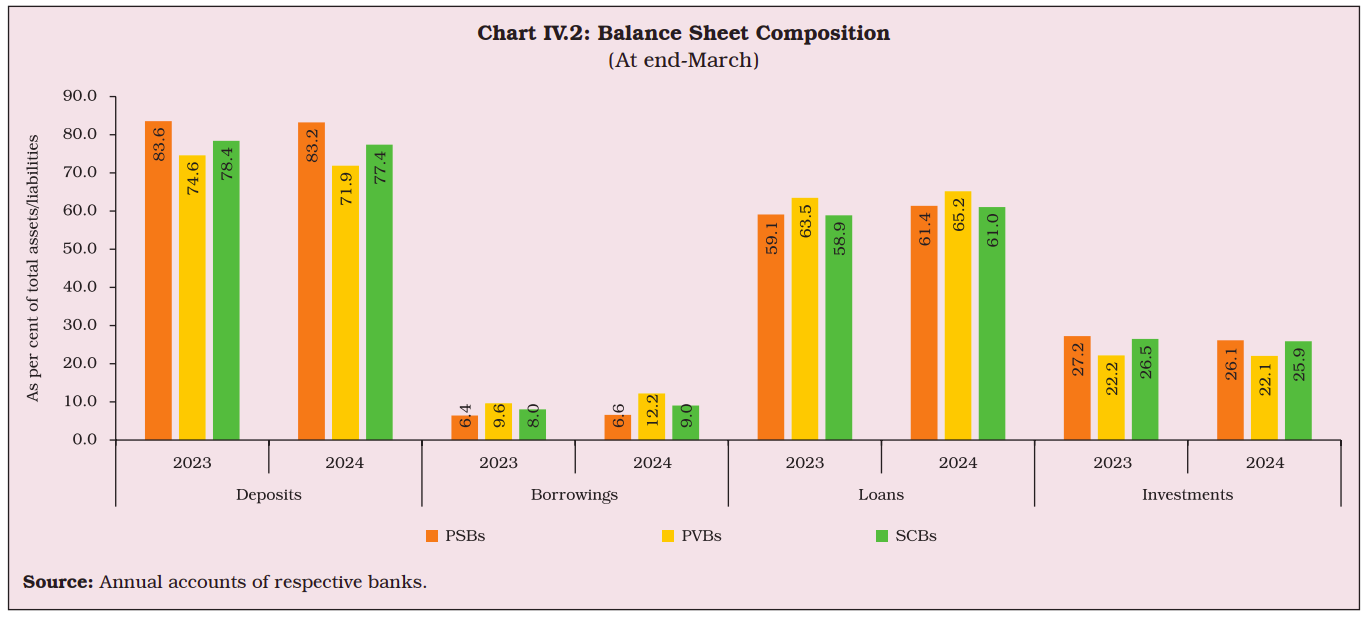

But here’s where things get interesting: while deposits still form the bulk of a bank’s liabilities (the money they owe to customers and lenders), their share has slightly declined. Borrowings, on the other hand, have picked up, increasing from 8% to 9% of liabilities.

Why is this happening? It’s partly because banks are chasing higher profits. Lending money earns them more than parking funds in government securities, which are safe but offer lower returns. Loans and advances now make up 61% of total bank assets, while investments in government bonds have fallen to 26%. This is a calculated risk—more loans mean more income, but it also increases vulnerability to bad loans if borrowers default.

Source: RBI

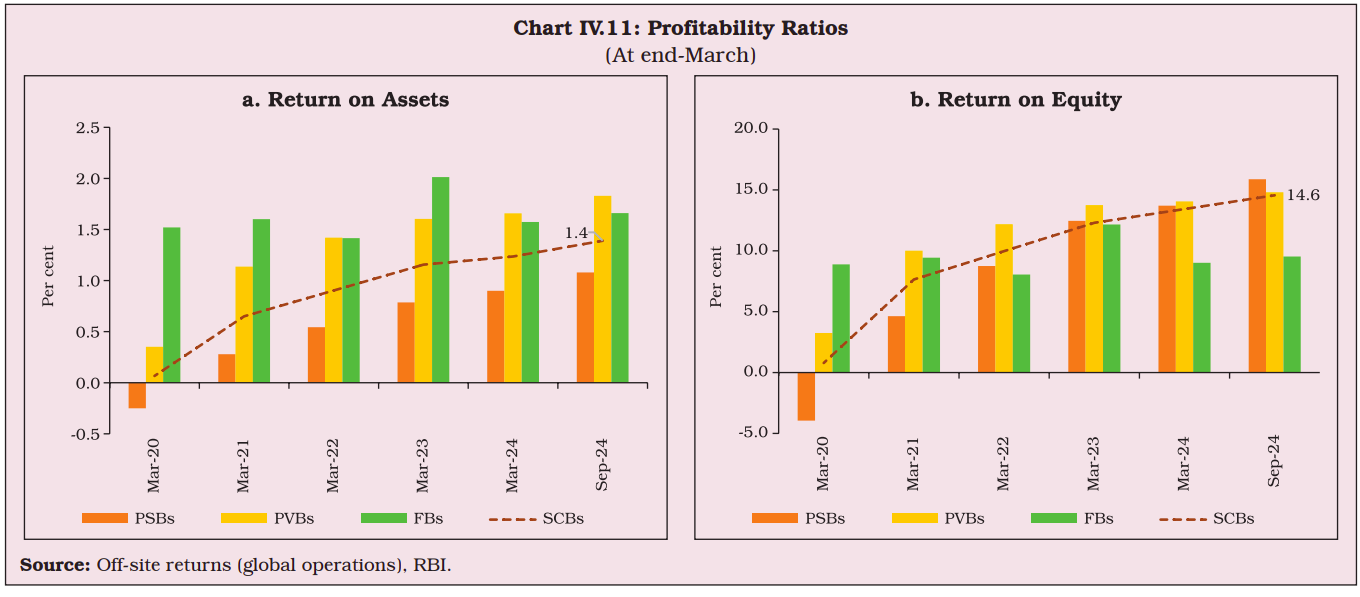

Indian banks are not just surviving—they’re thriving. For six straight years, their profitability has grown. In 2023-24, two key measures of efficiency—Return on Assets (RoA) and Return on Equity (RoE)—improved to 1.4% and 14.6%, respectively. These may sound like small numbers, but in the banking world, they reflect significant gains.

Source: RBI

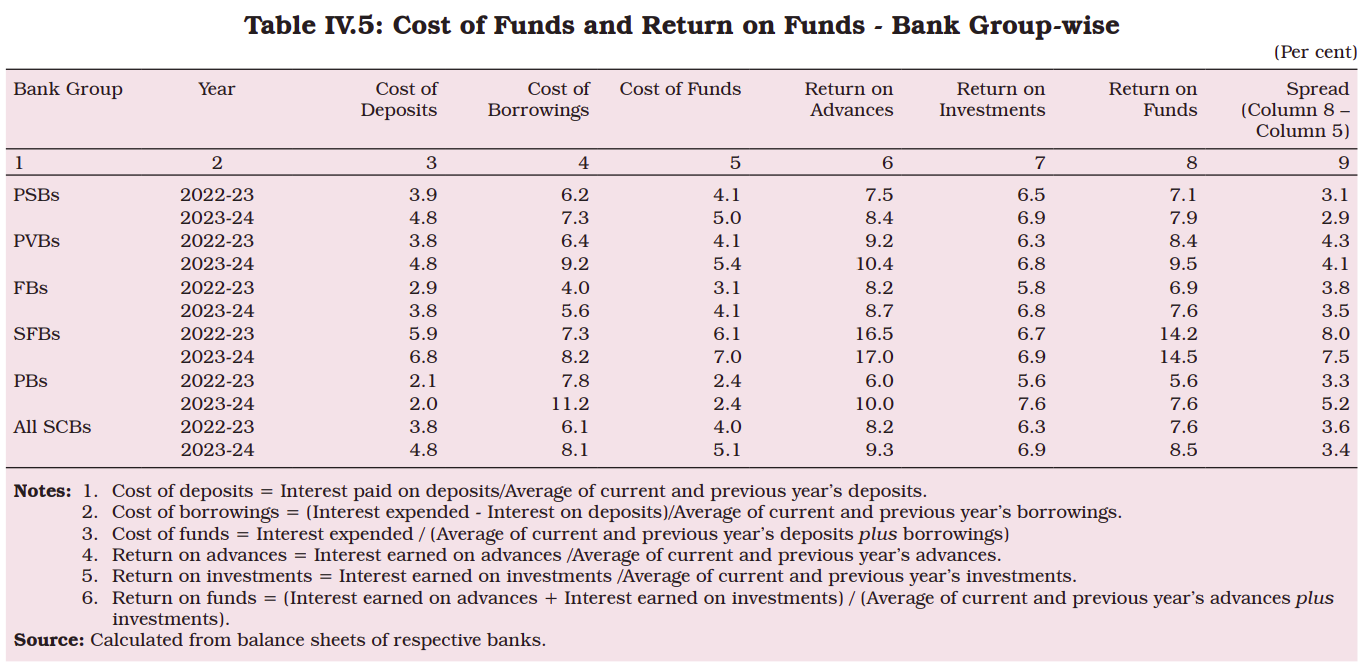

At the same time, banks faced rising costs. The cost of funds—the average interest banks pay to gather money from depositors and lenders—jumped by 104 basis points to 5.1%. Private banks felt this pinch more acutely, with their costs rising to 5.4%, compared to 5.0% for public sector banks. Small finance banks, which operate in niche markets, saw the highest costs at 7%.

Yet, private banks managed to maintain a comfortable lead in profitability. Their spread—the difference between what they earn on loans and what they pay on deposits—stood at 4.1%, far higher than the 2.9% spread of public sector banks. This gap highlights the private sector’s focus on high-yield lending, like personal and unsecured loans, which bring in higher returns but also come with greater risks.

To address the credit-deposit gap, banks offered higher rates on term deposits. By March 2024, private banks’ average rate for new term deposits reached 6.6%, up from 4.5% two years earlier. This led to a 42.9% rise in interest expenses, which grew faster than the 29.9% increase in interest income.

Even with these challenges, profits surged. Overall, net profits jumped 32.8% to ₹349,603 crore. Private banks led the way with a 41.2% increase, while public sector banks saw a 34.9% rise, thanks to better efficiency and improved asset quality.

Source: RBI

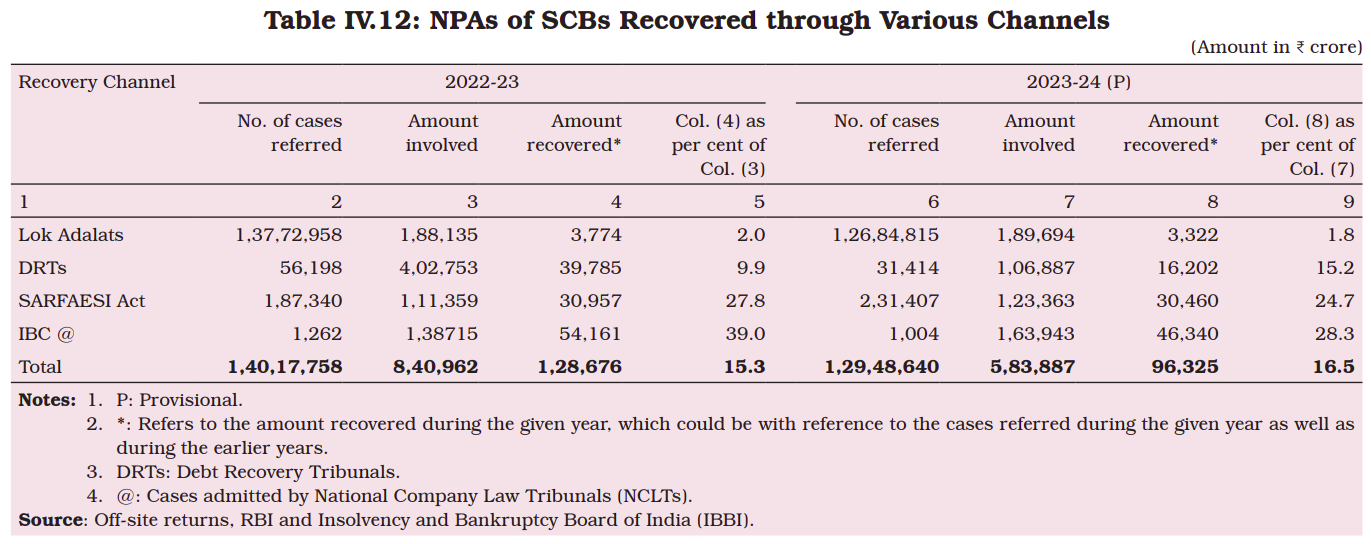

One of the standout achievements for Indian banks this year was the sharp reduction in bad loans. Gross Non-Performing Assets (NPAs)—loans that borrowers fail to repay—dropped to 2.7%, the lowest in 13 years. Net NPAs, which account for provisions already set aside for bad loans, hit a decade-low of 0.62%.

How did this happen? Banks got serious about recovering their dues. They used multiple strategies:

- The SARFAESI Act allows banks to seize and sell assets that borrowers pledged as collateral. This method is quick and effective for smaller loans backed by assets like property.

- The Insolvency and Bankruptcy Code (IBC) focuses on large and complex cases. Companies in financial trouble are restructured or liquidated through legal tribunals. While this process can be slow, it has been instrumental in recovering nearly 28.3% of the total amounts involved in insolvency cases.

-

Source: RBI

-

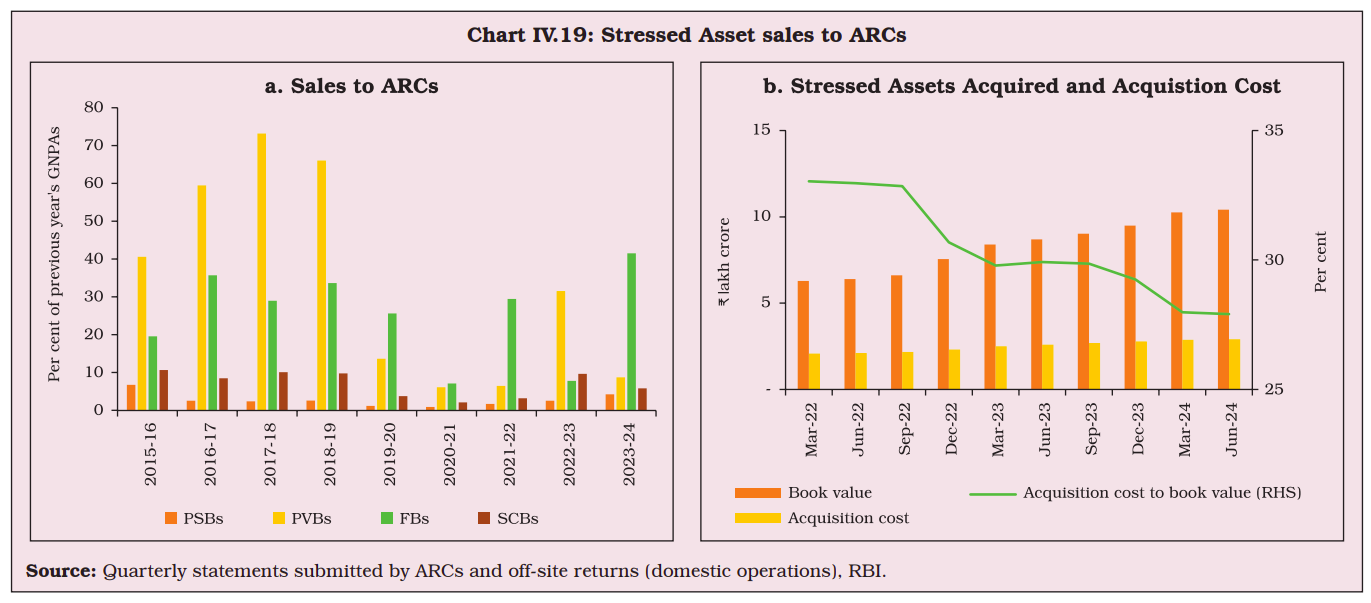

Sales to Asset Reconstruction Companies (ARCs) allow banks to sell bad loans to specialized firms that attempt to recover the money. Although this method accounted for only 5.8% of recoveries this year, it remains an important tool for clearing bad loans off the books.

- Source: RBI

Together, these mechanisms have helped banks clean up their balance sheets, freeing up resources for fresh lending.

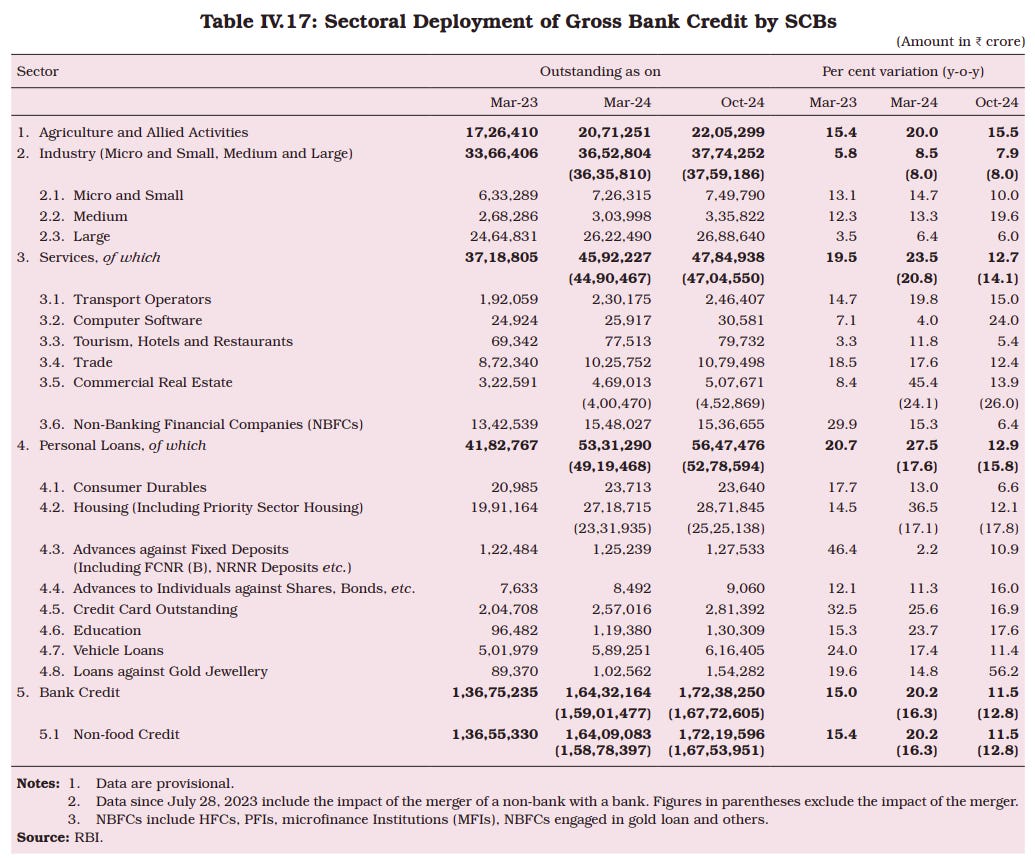

Banks’ lending patterns also reveal a lot about the economy. Retail loans—personal loans, home loans, and vehicle financing—saw robust growth, reflecting strong consumer demand. Credit to Micro, Small, and Medium Enterprises (MSMEs) also grew significantly, aided by government schemes like the Emergency Credit Line Guarantee Scheme (ECLGS).

However, not all sectors are doing equally well. Agriculture loans grew modestly, but the sector continues to struggle with high NPAs—8.5% of total loans to agriculture remain unpaid. Infrastructure and power sectors, while stable, are still grappling with legacy issues, including high levels of bad loans.

This paints a mixed picture: credit is flowing freely into high-growth areas like retail and MSMEs, but old challenges in sectors like agriculture and infrastructure persist.

Source: RBI

The Indian banking system is stronger today than it has been in years. Profits are rising, bad loans are falling, and efficiency metrics are improving. But the risks can’t be ignored. Banks are taking on more borrowings, which could squeeze their margins. They’re also betting heavily on lending, which makes them more vulnerable to defaults if the economy slows down.

It’s a delicate balancing act. On one hand, the banking sector’s performance shows a healthy appetite for growth. On the other, it’s a reminder that growth always comes with risks. Banks are walking a tightrope, and their success or failure will have far-reaching consequences for the economy as a whole.

As we watch these trends unfold, one thing is clear: the story of Indian banks is not just about numbers. It’s a story of how money moves, how risks are managed, and how the economy evolves. And in that story, every deposit and every loan tells a tale of its own.

The Role of Credit in Economic Growth

Something is fascinating about how credit—the money people and businesses borrow—interacts with economic growth. It’s not just about how much credit is floating around in the system; it’s about how effectively it’s used. A recent RBI report delved into this delicate balance and brought up some intriguing insights. Let’s break it down step by step.

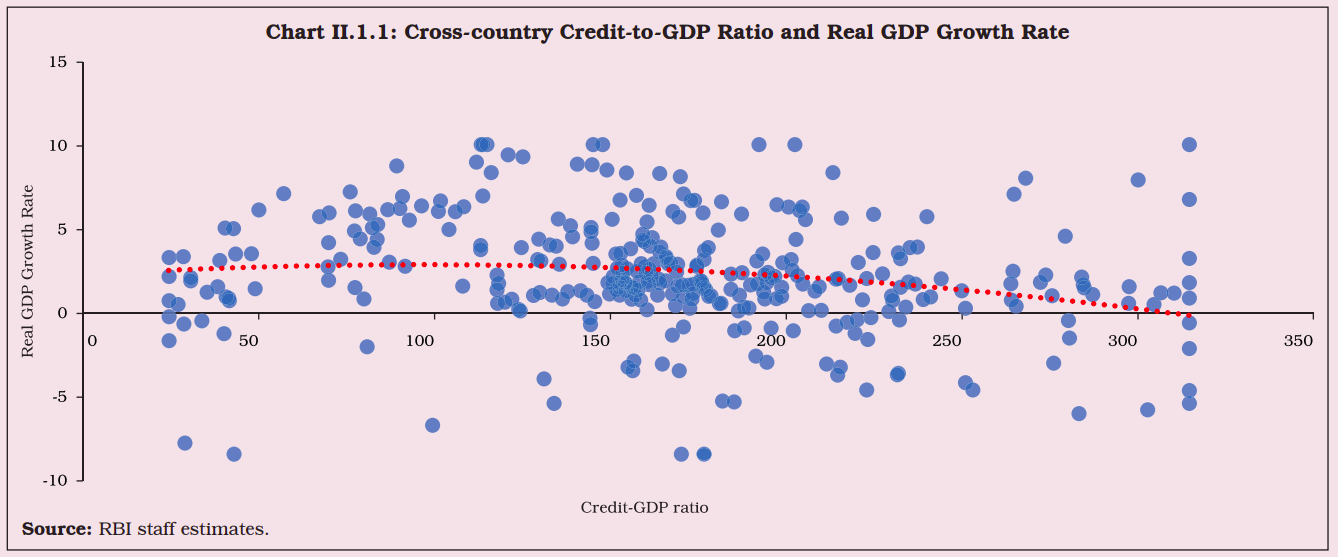

The core idea is this: credit fuels economic growth, but only up to a certain point. Beyond that, it can lead to more harm than good. This insight is based on an analysis of data from 16 countries, which shows an interesting pattern. As the credit-to-GDP ratio (essentially the amount of credit in the economy compared to the country’s total economic output) increases, it creates a virtuous cycle at first. Businesses borrow to invest in new projects, households take loans to spend on homes or goods, and the economy grows faster.

But there’s a catch. This growth isn’t unlimited. The relationship between credit and GDP growth follows what’s called an inverted U-pattern. Imagine a curve that rises steadily, reaches a peak, and then starts to decline. The “peak” of this curve is where credit growth is most productive—where it adds the most to the economy. According to the study, this sweet spot for credit lies at a credit-to-GDP ratio of 113%. Beyond this point, the benefits start to diminish. Credit begins to flow into less productive or even risky activities, such as speculative investments, and the economy slows down instead of speeding up.

Now, here’s why this is particularly interesting for India. Our credit-to-GDP ratio currently stands at 90%, well below the 113% threshold. On paper, this suggests there’s a lot of room for credit expansion to drive more growth. But—and this is a big but—we can’t take the 113% figure as an absolute rule. Why? Because this number comes from a relatively small set of countries, and their financial systems are very different from India’s. For instance, India has large informal credit markets, significant regional disparities, and varying levels of financial literacy. All these factors make it tricky to directly apply this threshold to our economy. What matters more is the principle: credit, when used wisely, can be a powerful driver of growth.

Source: RBI

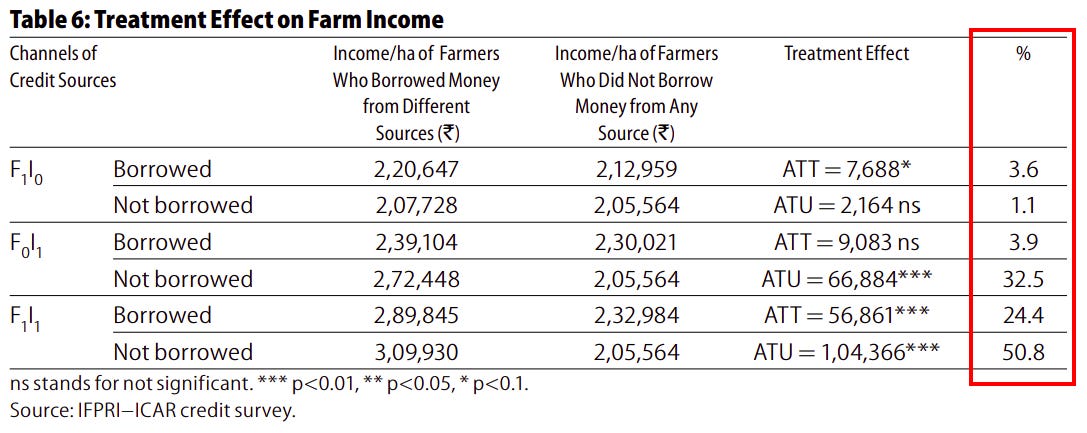

Let’s zoom in on why credit is so important. Take agriculture as an example. For millions of farmers, access to credit can mean the difference between just surviving and actually thriving. A study in eastern India found that farmers who borrowed money—both from banks and informal sources like friends or moneylenders—earned more from their farms compared to those who didn’t borrow at all. On average, their incomes increased by anywhere from 3% to 24%. The biggest gains came when they used a mix of formal (bank) and informal loans. Why? Because having access to funds allowed them to invest in tools, seeds, fertilizers, and other resources that boosted productivity.

Source: EPW

But not all credit is created equal. Informal loans often come with a steep cost—interest rates that can be as high as 27% per year, compared to the much lower 12% charged by banks. Unfortunately, about half of India’s agricultural households still rely on informal credit, which eats into their profits and keeps them stuck in a cycle of debt. If more farmers had access to cheaper, formal loans, it could transform rural economies.

Credit doesn’t just help individuals; it’s also a game-changer for businesses. Take micro, small, and medium enterprises (MSMEs), which contribute about 30% to India’s GDP. Despite their importance, these businesses face a massive credit gap, estimated to be ₹20-25 lakh crore. Bridging this gap could unlock tremendous economic potential. Global research shows that when people have better access to credit, they’re more likely to start businesses, create jobs, and earn higher incomes. For instance, in the U.S., individuals with improved access to credit after bankruptcy were 33% more likely to start capital-intensive businesses. These ventures didn’t just succeed; they also boosted job creation and increased entrepreneurs’ earnings by 4% on average.

Credit’s benefits don’t stop at income or business growth. It also cushions families against uncertainties. A 2018 survey showed that households with access to formal credit were 21% more likely to invest in education and healthcare. This isn’t just about spending money; it’s about creating long-term opportunities. Families that borrowed for education saw their children’s future earnings rise by 15-20%, thanks to better schooling.

Yet, the picture isn’t entirely rosy. Around 190 million Indians remain unbanked, and 50% of rural households still depend on informal credit. This limits their ability to improve their lives and escape poverty. And when credit is mismanaged, the consequences can be severe. The 2010 Andhra Pradesh microfinance crisis is a stark reminder. Excessive lending led to widespread defaults. The government’s crackdown on microfinance institutions then cut off access to credit, leading to falling rural wages, reduced consumption, and struggling small businesses.

So, what’s the takeaway here? Credit is undoubtedly a powerful tool for growth, but its effectiveness depends on how and where it’s used. For India, the focus should be on two things. First, we need to expand access to formal credit, especially in sectors like agriculture and MSMEs, where it can have the most impact. Second, we need to ensure responsible lending practices to avoid overextending credit into unproductive or risky areas.

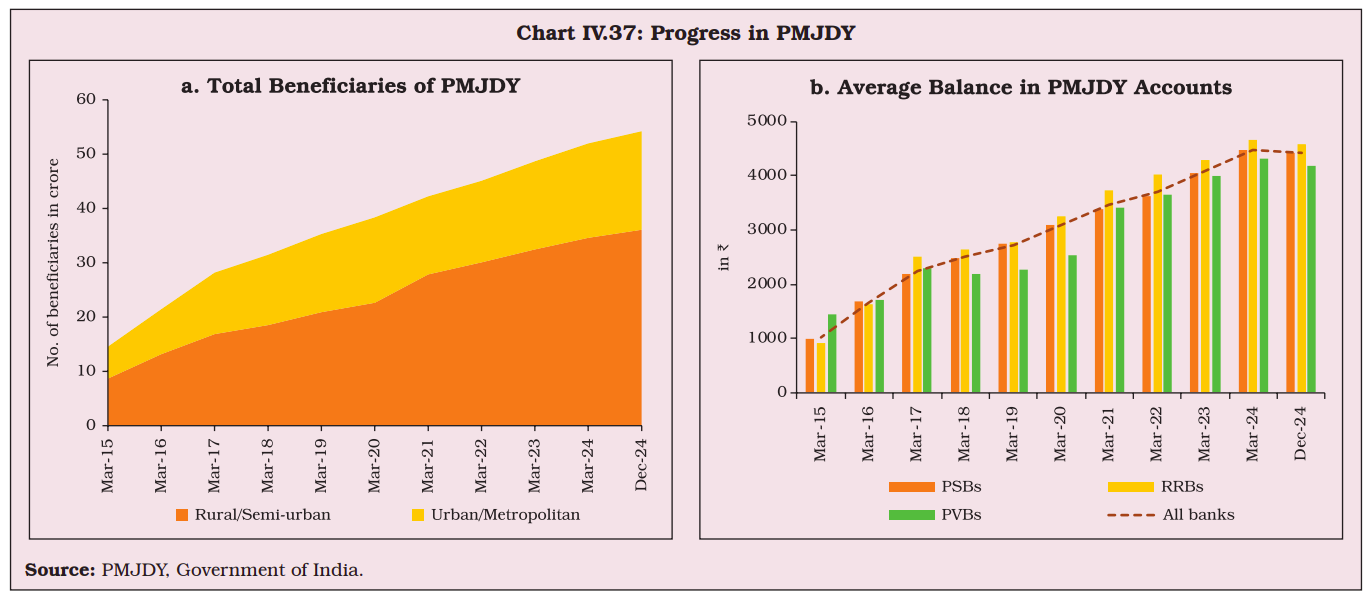

At the end of the day, it’s not about chasing an arbitrary credit-to-GDP number like 113%. It’s about using credit strategically to drive sustainable and inclusive growth. And while there’s a lot of work to be done, India has made significant strides in the right direction. Initiatives like the Pradhan Mantri Jan Dhan Yojana have brought millions of people into the formal banking system, and schemes like the Kisan Credit Card are making affordable loans available to farmers. But there’s still a long way to go. The challenge—and the opportunity—is to ensure that credit becomes a tool for empowerment, not exploitation.

Source: RBI

Tidbits

Adani Exits Adani Wilmar

Adani Enterprises is fully exiting Adani Wilmar by selling its 44% stake in two phases. Wilmar’s subsidiary will buy 31.06% at up to ₹305 per share, with another ~13% sold to meet public shareholding rules. Adani plans to reinvest in core businesses like energy and transport. After the announcement, Adani Enterprises’ shares rose 7.65%, while Adani Wilmar’s stock saw some volatility.

PSB Workforce Hits 13-Year Low

Public sector banks’ workforce fell to 756,015 in FY24, the lowest in 13 years, down 12% from FY17. Mergers like Dena and Vijaya Bank into Bank of Baroda, slower branch expansions, and declining clerical roles have driven this drop. Meanwhile, private banks doubled their workforce to 845,841 during this period, attracting talent with better pay and rapid growth.

JSW Gears Up for EV Market with Chinese Partners

JSW Group is in talks with Chinese firms to strengthen its EV strategy, bringing advanced tech and cost efficiencies. This partnership aims to position JSW as a strong contender in India’s growing EV market, driven by rising demand and supportive policies. The collaboration could reshape JSW’s role in green mobility and boost investor interest.

-This edition of the newsletter was written by Kashish

Thank you for reading. Do share this with your friends and make them as smart as you are ![]() Join the discussion on today’s edition here.

Join the discussion on today’s edition here.