Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

Just a quick heads-up before we dive in. The Meesho IPO is open now. We wrote about them earlier — you can read the full story on Meesho here.

In today’s edition of The Daily Brief:

- Is Wakefit a new-age business, or an old-school one?

- Is the transformer business ready to explode?

Is Wakefit a new-age business, or an old-school one?

When Wakefit began in 2016, it was a mattress brand that only ran online. It would sell Indians comfortable memory‑foam mattresses, without middlemen. The product was so good, the promise went, that Wakefit would let you return your mattress if you didn’t like it in the first 100 days.

Today, the company is on the verge of its IPO. But the business is meaningfully different from what it was back in 2016. For one, it is slowly growing into a “full home solutions ” brand, selling everything from sofas to yoga mats. Two, in its quest for growth, it is becoming a more conventional, offline brand with large showrooms across big cities. Most of the n ew money it’s raising is actually meant to fund its offline expansion.

These changes are probably paying off. In the recent past, the company has grown its revenue at roughly 25% a year. Over the last half-year, it even turned its first profit.

But what are you really getting, if you buy a piece of this company? Should you see it as a new-age, digital-first business with explosive potential? Or is it closer to a traditional, physical business — one that earns on its mastery of operations and logistics rather than its innovation chops?

That’s what we’re going to try and understand, today.

Disrupting home furnishing

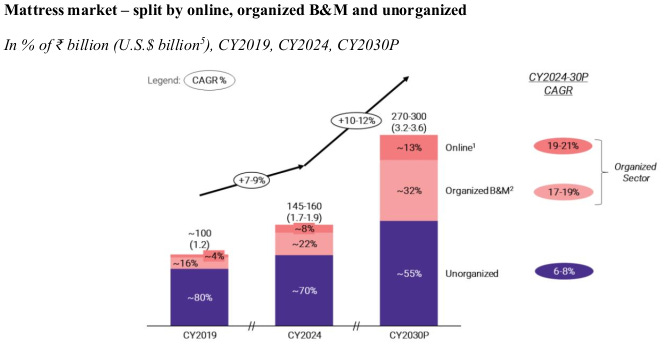

India’s home furnishings market is growing at a healthy pace of 11-13% a year. It isn’t an easy market to dominate, either. People only buy a new bed or mattress so often, leaving little room for loyal, repeat customers. When they do make these purchases, the sheer cost makes them care more about prices than brands.

Why, then, does this space have room for an “investible” business?

Wakefit’s bet is that it can ride a sea-change in how Indians furnish their homes. At the moment, most of this market is made of small, unorganised players. Most Indians buy their furniture from small stores nearby, or have it made by a local carpenter. Their mattresses are often a commodity purchase from a neighbourhood store. Products are rarely standardised, suppliers hardly use data in decision-making, and there’s little brand differentiation.

But that’s changing. There are segments of the market, particularly its premium or “mass-prestige” end, that’s switching to organised players they trust, particularly for mattresses. Back in 2019, 20% of the mattress market belonged to organised players. Within five years, they grabbed 30% of the market. There are similar — though less dramatic — shifts in furniture and decor, too.

Meanwhile, people are also increasingly making their home purchases online — which favours branded players that can deal with e-commerce logistics.

That’s a shift Wakefit hopes to be at the heart of. It’s positioning itself as a brand for any “value premium” purchase you may need to set up your home. It runs three key verticals:

- Mattresses , the core of the business, bringing in ~60% of the company’s revenue

- Furniture , the fastest-growing part of its business, with sales growing by a CAGR of 34% over the last two years

- Miscellaneous furnishings and decor offerings, which include lighting, bed linens, kitchenware, and more. This is the slowest-growing end of its business. But, where Wakefit’s other products almost never need replacement, décor can bring repeat customers.

From a mattress seller, in short, Wakefit is now turning itself into a one-stop shop for home needs of all sorts — somewhat like a homegrown Ikea. Going by its marketing, that’s definitely how the company sees itself.

The “D2C” promise

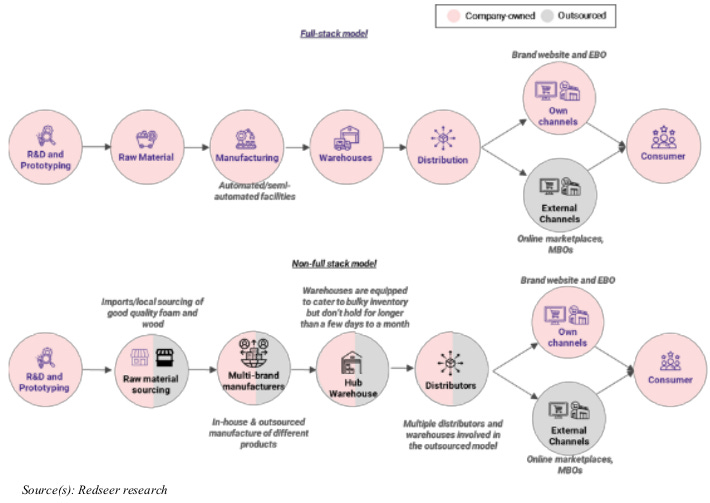

Wakefit is trying to make a direct-to-customer , or “D2C” play in the space. At its heart, Wakefit is trying to keep as much of its value chain as it can for itself. By cutting out middlemen and taking charge of everything, the promise goes, you can get better margins, more data, and a tighter grip on the brand experience.

That means Wakefit has built most physical parts of its business in-house, running everything from manufacturing, to supply chains, to distribution.

Manufacturing

Most “home brands” don’t actually make what they sell. They often design their own products — but then outsource manufacturing to someone else.

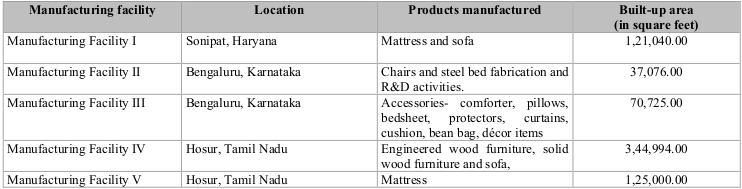

Like others, Wakefit develops its own products — and it’s been rather prolific. In FY25, for instance, it added 3,070 new SKUs to its portfolio. Unlike many of its peers, however, the company makes most of its products in-house .

It does so through five big plants that the company has leased and fitted out with imported machinery. A manufacturing footprint like this is expensive to set up. But if you can run at anything close to full capacity, it can give you far better margins than if you were trading goods made by someone else. That’s something Wakefit has managed — all its factories run at more than 70% capacity.

Running your own factories presents a trade-off . It ordinarily means better margins, and more control. For instance, by being smarter about its procurement decisions, the company pushed its gross margins from ~43% to the mid-50s in just two years. But it also creates risk . With all those assets on your books, you need to sell much more just to stay afloat. And you have to monitor all sorts of fluctuations.

Take raw materials — the company takes on the full brunt of swings in the price of raw materials. It’s exposed to everything from global chemical cycles, to freight costs, to currency swings. On the other hand, its value-conscious customers may not accept frequent or sharp price rises, which means the company may have to absorb those fluctuations. The cost of the company’s raw material imports has risen dramatically over the last two years — from the low-20s, they now make up over 38% of its total raw material costs.

Logistics

The next sphere where Wakefit pushes middlemen out is logistics . It runs a tight network — with a central “mother warehouse”, that sends goods out to a series of nodes across India. The company’s own fleets take care of most deliveries, with third parties only coming in when a package needs to reach a remote area.

Mastering this is easier said than done. This is an industry where you’re almost exclusively dealing with bulky items like furniture and mattresses, which can be awkward to move. The success of such a business can hinge on its ability to move them at a reasonable price.

But Wakefit shines here. The company has mastered the art of compressing its products in a way that permits easy shipping. Indeed, many of them are built for easy transportation. For instance, it “roll-packs” its mattresses — compressing them into tight “spherocubes”, allowing them to ship large mattresses in a box that a single person could carry.

Similarly, it ships most of its furniture in “flat-packs” — as a compact arrangement of components that are assembled in a customer’s house. Arrangements like this allow the company to fit more units in a truck or warehouse, and ensure limited damage during transit.

Distribution

As a customer, the most visible part of Wakefit’s D2C model is probably distribution . While the company lists its products on e-commerce and quick commerce websites, a majority of its sales happen through its own channels. This is another trade-off: while selling through third parties can bring you visibility , by outsourcing distribution, you might surrender 20-25% of your margins to intermediaries.

But curiously, the company’s own channels are going through a major shift.

Historically, Wakefit’s own website was the biggest pillar of its business. It was key to the company’s D2C appeal — it could be run at negligible overhead costs, scaled indefinitely, and the data it generated could be mined for insights.

Increasingly, however, the heart of the company’s business is shifting to its expanding network of “company owned, company operated” (COCO) stores. Curiously, customers seem much more comfortable making their large purchases from physical stores. In the first six months of this year, the company’s “average order value” (‘AOV’) from its physical stores was ~79% higher than from its website.

This realisation seems to have pushed the company to greatly expand its offline presence. From just 23 stores in March 2023, the company spread to 125 stores by September 2025, across 62 cities. As this happens, an increasing share of the company’s sales are going offline. From 11% in FY23, offline sales have leapt up to 41% of the company’s revenue.

And it’s now doubling down. A lot of its IPO money has been earmarked for another 117 physical stores — many of which will be smaller than what it currently has. On the other end, the company is planning two Ikea-like jumbo stores in Bengaluru — another new format. As it does so, Wakefit is adding another layer of complexity to its business. Every offline store comes with rent, staff, fit-outs and local marketing.

How things are working out

We’ve only described some of the things the company does in-house. There are facets we don’t have the space to cover — from its extensive reverse logistics system, to a fleet of furniture installers that assemble furniture at the homes of customers.

Repeatedly, however, the same motif shows up: the company has made capital-heavy choices that give it tighter control and better unit economics, alongside more operational and financial risk. Are these good choices to make? It’s hard to say. This is still a young business, which is only just fiIs the transformer business ready to explode?nding its way into profitability.

But there are some good signs. For one, the company is still growing rapidly. Over FY23–FY25, its revenue grew by ~25% a year — 1.6 times as fast as its organised competitors. The company is clearly winning market share, that too without relying too heavily on marketing. If anything, its promotion expenses have dropped from ~11.8% of revenue in FY23, to just over 5% in the first half of this year. This is the mark of a maturing brand.

Meanwhile, the company’s unit economics is improving. The company went through an inflection point somewhere after FY 2023 — with its EBITDA going from negative (-)10.6% to over 6% over the course of a single year. In the first half of this year, it reached the mid-teens, at 14%. That surge in profitability brought the company its first ever after-tax profit, of ₹35 crore.

There’s a catch, however: all those capital-intensive choices weigh its books down, despite not having debt on its books. Last financial year, over 60% of the cash the company made from its core business went into setting up new facilities. Its depreciation costs have nearly doubled in two years. It has made massive commitments to pay its leases into the future. These commitments — over ₹350 crore in total — drag the books down.

The bet

Wakefit’s IPO presents an interesting bet.

The company has demonstrated that it’s genuinely able to break into an unorganized category, win market share, and steadily improve its unit economics. It could well evolve from here into a cash-generating machine.

But that isn’t guaranteed. The company is building out a hugely asset-heavy business, which has to monitor hundreds of variables along its complex value chain. Any of these — from a particularly bad Rupee depreciation, to a land dispute around a jumbo store — could suddenly send its business awry. With thousands of new SKUs a year, things will only grow in complexity. Meanwhile, the sheer weight of the company’s commitments could strain its flexibility.

Can the merits of this business model carry the weight of these risks? That’s what you need to ask yourself.

Is the transformer business ready to explode?

In India, during rain or hailstorms, we often lose power for long periods of time. Sometimes, this happens violently, as the power cut is accompanied by a loud noise outside, as if a bomb went off. However, that noise is probably common to all of us. It’s an understanding that the transformer has burst .

But, we realized that, while we get that transformers are essential to power transmission, we never truly asked ourselves what they actually do that make them so important. All the while, the world is running on a painful shortage of them, as old transformers require replacing immediately to make way for our current, vast energy needs.

So, to quench our curiosities, we decided to do a primer on this interesting industry, and where India comes in. Let’s get into it.

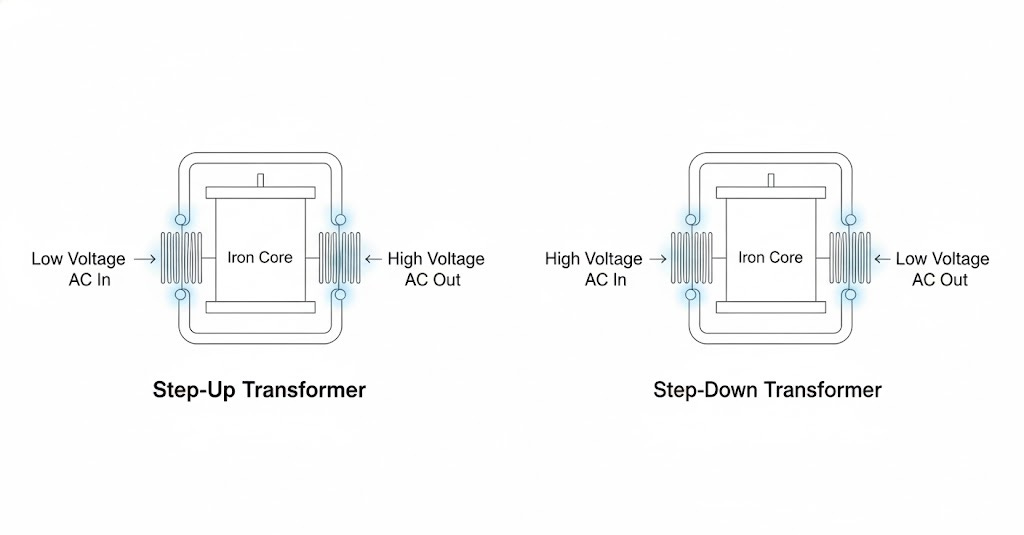

How a transformer actually works

Let’s try to understand how a transformer works through an example. Say you want to send water from a dam to a town. You can either send it as a thick, lazy flow through a fat pipe. Or as a thinner and sharper jet through a narrower pipe. If you adjust the speed, the amount of water reaching the town each second can be the same in both cases.

Electric power behaves in a very similar way. The “amount” of power is shared between voltage and current. Voltage is like the pressure, while current is how much charge flows per second. For a given amount of power, you can run at low voltage and high current, or high voltage and low current.

But why does the choice even matter? That’s because whenever energy is transmitted through wires or cables, energy is wasted. The more current you push through them, the hotter they get. A little extra current creates a lot of extra heat. Over hundreds of kilometres of transmission, that heat is power you’ve simply thrown away.

So, grid designers do something clever here. For long-distance travel, they keep the pressure high and the flow low. That keeps the wires cool and the losses small. Near your home or office, they flip things around: pressure drops to safe levels, and more flow becomes available so your devices can draw what they need. The transformer is what makes this swap even possible.

A transformer works by either stepping the voltage up or down. Apart from some small losses, the power going in and the power coming out are the same. So whenever you raise the voltage, the current drops by the same proportion, and vice versa.

That’s the entire trick. A transformer lets you repackage power as high-voltage, low-current electricity for long journeys and low-voltage, high-current electricity where people actually live and work. Between a power plant and your charger, electricity will pass through several of them, changing shape each time, so that it can travel across the country efficiently and still be gentle enough to sit inside a wall socket without burning the wires.

Many flavours of the same idea

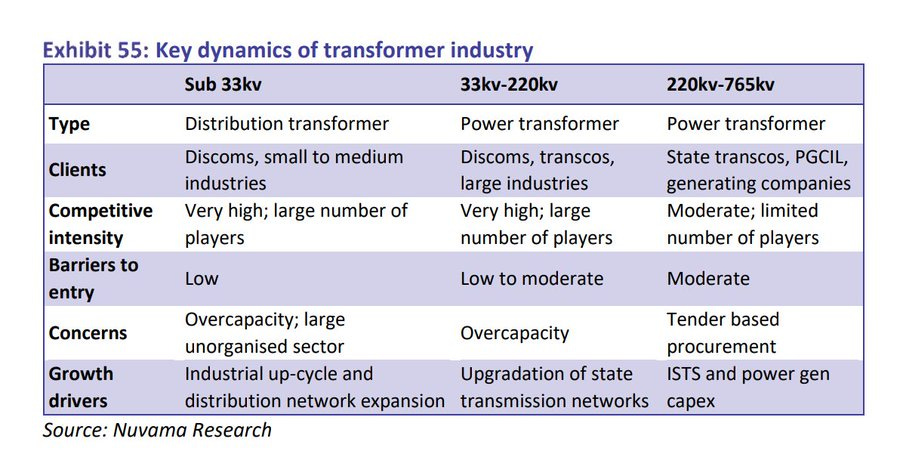

Even though the physics is the same everywhere, the business is not. The transformer world is split into layers, and each layer has its own economics and its own set of Indian companies living there.

At the very bottom of the staircase are the distribution transformers. These are the small pole-mounted or ground-mounted units that feed homes, shops, and small workshops. Every new feeder, every new housing project, every village electrification scheme needs some of these, making it a high-volume game.

In fact, the industry is highly commoditized: the designs are fairly standard, and there are dozens of manufacturers competing for tenders, including a large unorganised base. That makes margins very thin. Some of the leading Indian firms in this space are Shilchar Technologies and Voltamp.

Climb one level up, and you reach medium-voltage power transformers. These work between 33-220 kilo-volts (or kV) and serve industrial parks, city substations, refineries and renewable parks. These units are larger and more customised. You do not buy a hundred of them at a time; but rather for specific substations and projects. Competition is narrower than in distribution transformers. And as the testing requirements are stricter here, the margins are better. Voltamp and Bharat Bijlee do a lot of their business in this band.

From 220 kV upwards, you enter the world of high-voltage and extra-high-voltage transformers. These are the big grid transformers at 220, 400 and 765 kV that sit inside state transmission and Power Grid Corporation yards, and at the switchyards of large power stations. Here, volumes are small, but each unit is enormously valuable and high-margin. Only a handful of companies have the design teams, factories, and test rooms to build them and prove to utilities that they will survive decades of operation and serious fault events.

This is where a few Indian specialists like Transformers & Rectifiers India (or TRIL) operate. Most of TRIL’s revenue in particular comes from power transformers at 132–400 kV, including generator step-up transformers for plants, and interconnecting transformers.

Then there are the special-duty transformers that live outside the grid, and serve steel plants, smelters, solar parks, and railways. They are lower in volume but higher in margin, as the designs are highly-customised and fewer companies are qualified. TRIL, for instance, has leaned into this niche, claiming to be “one of only two qualified vendors “ worldwide for certain rectifier and furnace applications.

Put all of this together and you get a simple mental map. Most of the physical units in the country are small distribution transformers made by a crowded field of suppliers, where pricing is fierce and margins are modest. Most of the value and profitability, however, sits in a much smaller number of high-voltage grid transformers and special-duty machines, where engineering, reputation and testing capability count for more than just lowest price.

How the world ran short of them

However, right now, the world as a whole is running painfully short of higher-value transformers. The shortage wasn’t caused by one particular event, but it was the result of a long build-up that owed itself broadly to two forces clashing with each other.

The renewable energy transition

For a long time, the transformer industry lived in a slow, predictable rhythm. Grids in the US and Europe expanded a little each year, utilities replaced a few ageing units every season, and manufacturers planned their production around steady, almost boring demand. Most of the big transformers in those countries were installed in the 1970s and 80s, and even though their rated lives were around 25–30 years, utilities simply kept stretching them. If nothing urgent was happening, there was no rush to replace anything.

That comfortable pace hid a problem: the entire system was ageing together. The world was sitting on a huge stock of transformers that were quietly moving past their useful lives, but because they were still working, nobody treated it as an emergency.

Then the energy transition arrived. Countries began adding renewable power at a speed the grid had never seen. Every new solar park needed collector transformers. Every wind farm needed step-up transformers. Rooftop solar meant more stress on local distribution transformers. Data centres and AI clusters needed rock-solid, high-capacity connections. Electric vehicles and their fast-charging networks added their own load. Suddenly, the grid wasn’t just expanding; it needed a full makeover.

Raw material

Additionally, on top of this, it’s hard to make a transformer, because it depends on some speciality material.

At the heart of every transformer is a stack of thin, precisely cut sheets of a special steel called cold-rolled grain-oriented electrical steel , or CRGO — a material that India does not produce, and only a handful of mills in the world can make. Around that core sit tightly wound copper conductors, layers of insulation, high-voltage bushings, tap changers and a tank filled with insulating oil, all of which need their own small ecosystem of suppliers. These parts come around easier for low-value units, but specialized transformers need speciality copper.

It turned out that, just as the energy transition came around, the few CRGO steel mills that do exist were already running tight. Component makers for bushings, tap changers, and specialised copper conductors ran on long lead times. And since demand had been sleepy for decades, hardly anyone had built new transformer factories or expanded significantly.

So when the old transformers finally needed replacing, and the new energy systems all needed new transformers at the same time, the industry simply didn’t have enough capacity. Lead times that used to be a few months stretched into a year, then two. Prices rose. And global majors like Hitachi Energy and Siemens suddenly found themselves facing more orders than their factories could physically produce. Hitachi has said publicly that its order book has more than tripled since 2020 and that demand is rising “at an unprecedented scale.”

India’s transformer moment

So, how is India, one of the biggest players in the transition to renewables, handling all of this?

Our push for 500 gigawatts of non-fossil, renewable power by 2030 means moving huge amounts of electricity from remote wind and solar zones to cities. Our grid is expanding at a pace the country hasn’t seen in decades, with tens of thousands of kilometres of new lines and a massive addition of substation capacity being built.

On top of new demand, there’s also old demand. Visweswara Reddy, the chairman of Shirdi Sai Electricals estimated that about 20 per cent of the transformers already in service are overloaded or past their intended life, so they need replacing now. At the high-voltage end, Indian manufacturers are already “saddled with orders for almost two years,” and that even the medium-range units used in solar parks are booked more than a year ahead.

There is a lot of demand for medium and high-voltage transformers to handle all this, but India is struggling to ramp up supply accordingly. The biggest bottleneck there is our extremely-limited capacity to create most of the raw material required to make transformers. And global supply is already tight (and expensive) as things stand right now.

Take TRIL, for instance, which had a soft quarter recently. But that had nothing to do with their order book, which was strong. The issue was that they couldn’t source enough specialized copper conductors on time, and some shipments got stuck in customs when new BIS rules were introduced. Even when equipment is ready, dispatches can slip if monsoon delays hold up substation sites.

Right now, with India’s energy mix changing, our transformer cycle is not a simple story of just building more factories that make more transformers. It’s a deep, structural demand wave sitting on top of a supply chain that has some hard global limits. And manufacturers are learning that the real challenge is not getting orders, but delivering them.

Tidbits

-

Amazon Now ramps up with two new centres a day

Amazon is supercharging its ultra-fast delivery arm Amazon Now, opening two micro-fulfilment centres a day across Bengaluru, Delhi and Mumbai. The service already crossed 100 centres, set to exceed 300 by year-end, as Prime customers triple usage. The move tightens the battle with Blinkit, Instamart and Reliance’s quick-commerce networks.

Source: BusinessLine -

Meesho’s Valmo overtakes Delhivery in Q2 shipments

Meesho’s logistics arm Valmo delivered 399.7 million orders in Q2 FY26, surpassing Delhivery’s 246 million, marking a major shift as Meesho internalized deliveries. Valmo now handles 65% of Meesho’s volumes and could rise to 75–80%, tightening the pool of shipments available to third-party logistics firms.

Source: Moneycontrol -

Govt relaxes ‘small company’ norms to widen coverage

India has eased rules to let more firms qualify as small companies, aligning with labour reforms that expand social security coverage. Minister Mansukh Mandaviya said India now covers 64.3% of workers, up from 19% in 2015, with a target of 100 crore workers by March 2026—second only to China.

Source:Economic Times

- This edition of the newsletter was written by Pranav and Krishna.

Tired of trying to predict the next miracle? Just track the market cheaply instead.

It isn’t our style to use this newsletter to sell you on something, but we’re going to make an exception; this just makes sense.

Many people ask us how to start their investment journey. Perhaps the easiest, most sensible way of doing so is to invest in low-cost index mutual funds. These aren’t meant to perform magic, but that’s the point. They just follow the market’s trajectory as cheaply and cleanly as possible. You get to partake in the market’s growth without paying through your nose in fees. That’s as good a deal as you’ll get.

Curious? Head on over to Coin by Zerodha to start investing. And if you don’t know where to put your money, we’re making it easy with simple-to-understand index funds from our own AMC.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()