Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- The world can’t have enough of copper

- A nightmare quarter for Indigo

The world can’t have enough of copper

If you’ve been seeing copper prices surge lately, you might have been wondering: what’s so special about good old copper?

Well, copper’s best trait is that it carries electricity very efficiently, while not corroding easily. It’s effective and long-lasting, which is perhaps why it’s used in every modern electrical appliance today, from a light to a toaster to a smartphone.

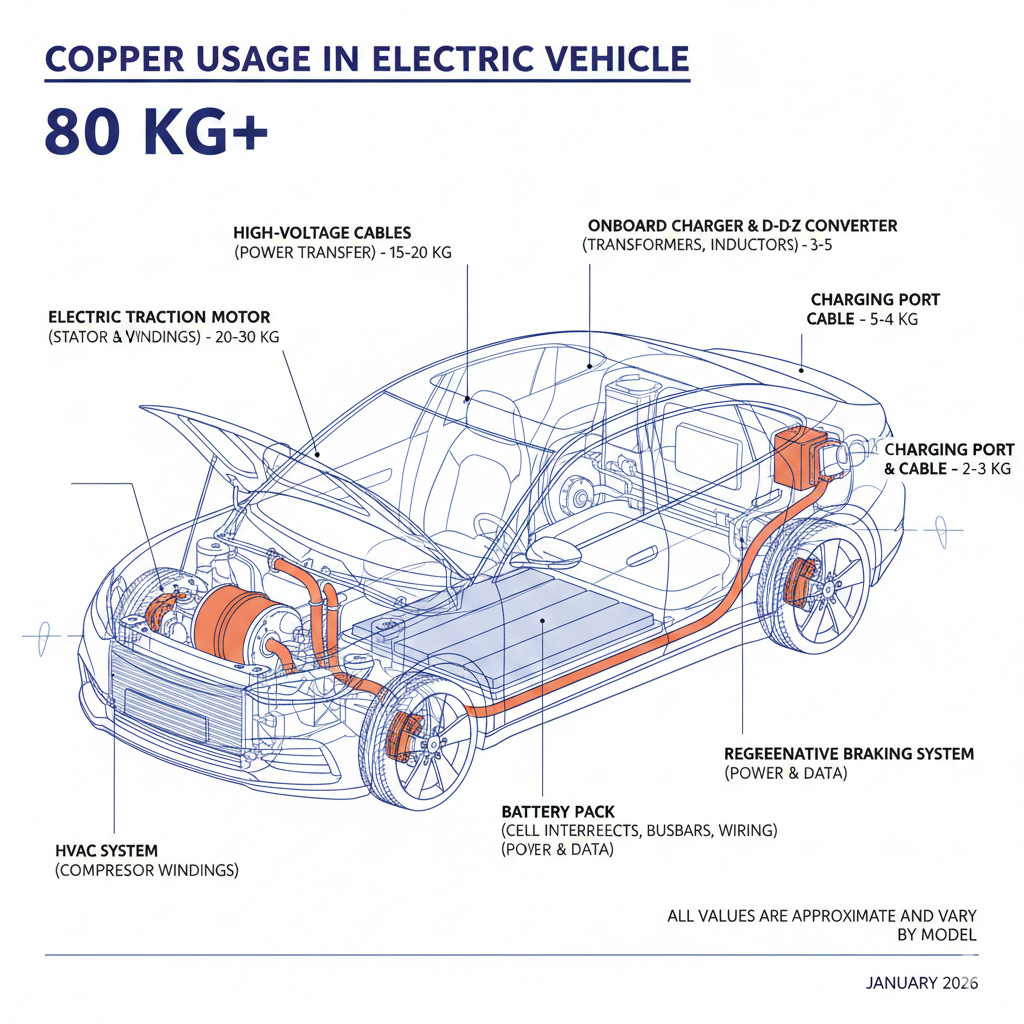

But beyond that, copper has also become a foundational metal for many new technologies: like EVs, wind turbines, solar panels, power grids, data centres, and so on. An EV, for instance, uses a whopping 80-90 kg of copper on average: 4 times that of a normal car.

Generated by Gemini

Every country in the world is trying to electrify transport, decarbonise power, and digitise its economy, which ends up demanding more copper. There is no easy substitute for it. Some make the argument that aluminium can replace copper, but that’s difficult. In high-performance electrical systems, where efficiency and heat resistance matter, aluminium can’t do what copper can. Silver might be the best alternative to it, but it is too expensive for everyday use. On top of that, silver prices are having their own moment anyway.

This insatiable demand for copper shows up in its sky-high prices. The global benchmark price for copper is set on the London Metal Exchange, commonly referred to as LME copper. Over the past year, copper prices have risen sharply and even crossed the $13,000 per tonne mark. As of January 23, prices hover around $12,800 per tonne, levels that were once considered extreme.

And, these prices are not being driven by speculation alone. They reflect a deeper structural tension between how much copper the world needs and how difficult it is to produce more of it.

To understand why this tension exists, it helps to look closely at how copper moves from deep underground into the objects we use every day.

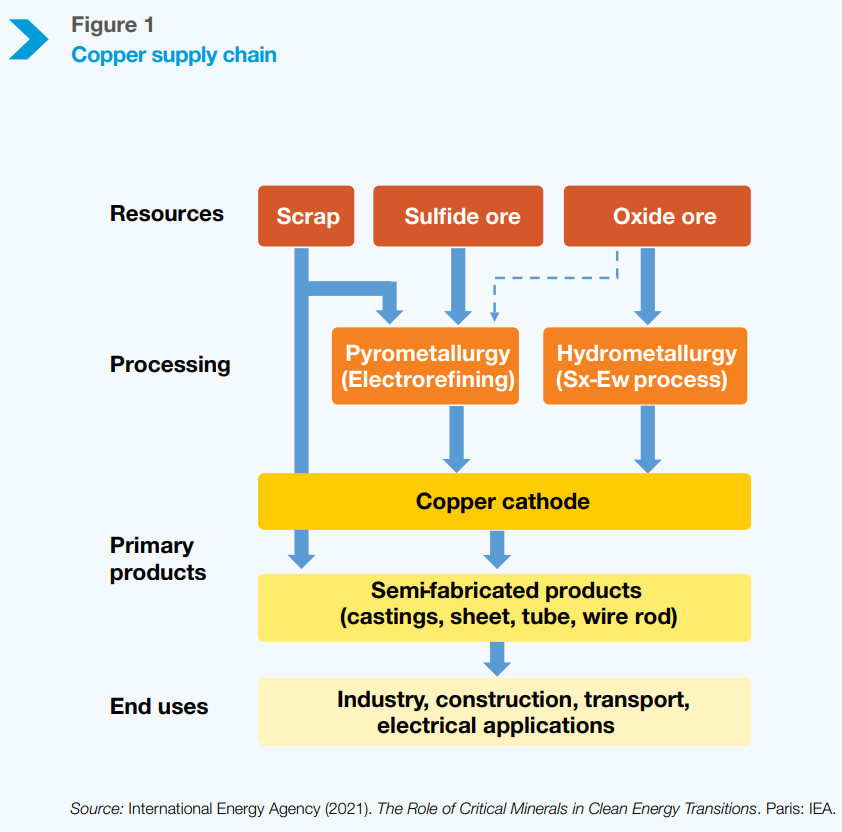

The value chain

Copper begins its life deep in the earth, as part of a rock.

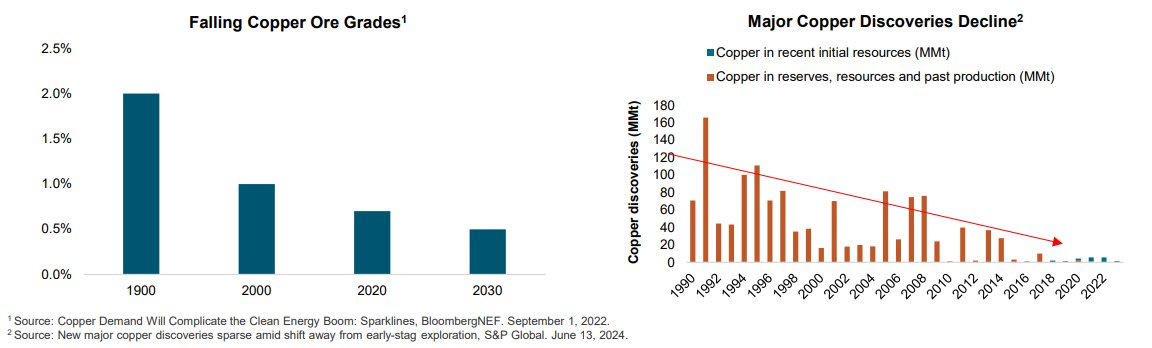

Copper is usually spread thinly through vast quantities of ore. The concentration of copper in this rock is known as the ore grade. Decades ago, some of the world’s best copper mines operated at ore grades of 1.5% or higher. That meant 1.5 kilograms of copper for every 100 kilograms of rock. Today, many new mines operate at grades closer to 0.6% or even lower. Far more rock has to be dug up and processed to extract the same amount of copper.

When a copper deposit is discovered, the richest and most concentrated parts of the ore body are usually closest to the surface and easiest to access. These high-grade zones are mined first because they deliver more copper with less effort. Over time, those zones get depleted, which is why new ore grades are declining in copper material. The deeper you go, it seems, the lower the copper concentration gets.

As mining goes deeper, the amount of surrounding waste rock — often called overburden — also increases. For every tonne of copper extracted, miners must drill, blast, haul, and process much larger volumes of rock. The visible result is more debris, larger waste dumps, and bigger tailings ponds, even though the final copper output may remain the same.

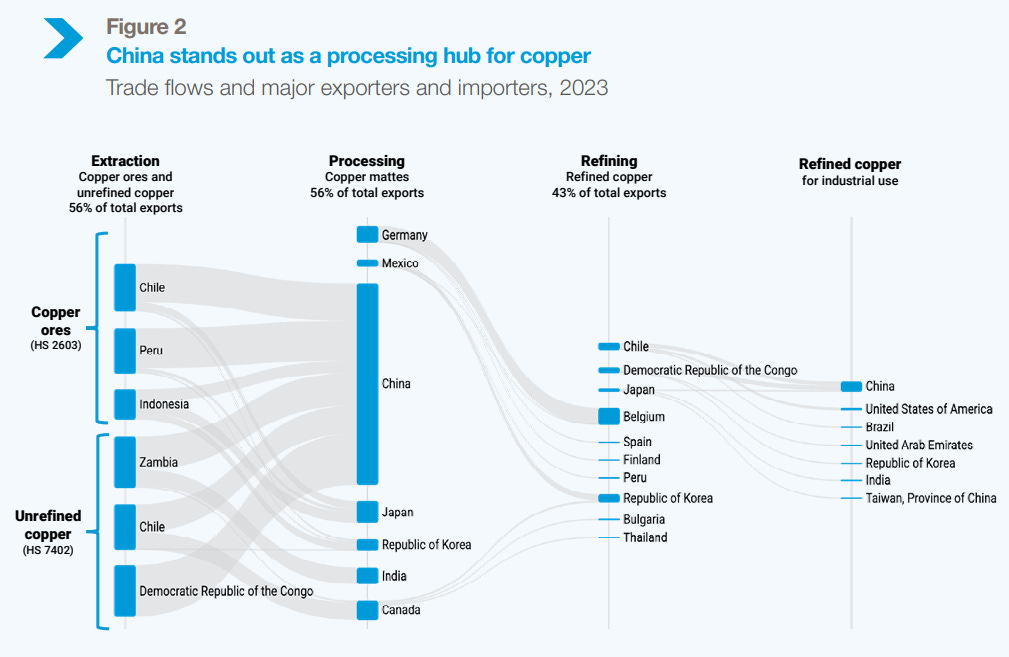

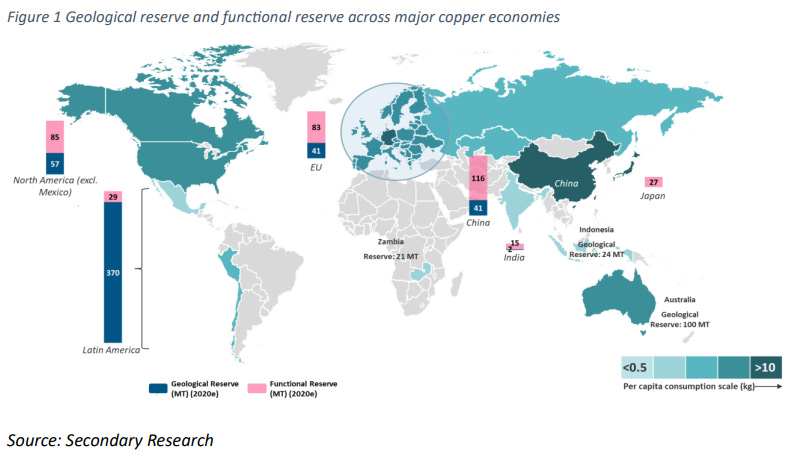

Globally, copper reserves are concentrated in a few regions. Chile is the undisputed leader, followed by Peru, the Democratic Republic of Congo, China, and the US.

Many mines in these countries are aging. As mines get deeper and ore grades fall, costs rise, and environmental challenges increase. Mines are also increasingly shut or delayed due to water shortages, environmental protests, labour disputes, or changes in government policy. This has made copper supply far more fragile than it appears on paper.

Once copper ore is mined, it is crushed into smaller pieces and processed to separate the copper-bearing material from the rock. In most large deposits, copper is present as a sulphide mineral. This material undergoes a process called flotation , which uses water, chemicals, and air to separate copper concentrate from the rest of the rock. This stage is extremely water-intensive. In dry regions like Chile, water scarcity has strongly constrained copper production.

The output of this stage is copper concentrate, usually containing 25–30% copper. This is not yet usable metal. It must be transported, often across continents, to a smelter to be processed.

At the smelter, the concentrate is heated to very high temperatures to remove sulphur and other impurities. This process produces blister copper, which is ~98% pure. The blister copper is then refined, typically using electrolysis, to produce copper cathodes with nearly-perfect purity. These cathodes are reddish metal plates that weigh 50-80 kg each. This is the form in which copper is traded globally and priced on exchanges like the LME.

From cathodes, copper is drawn into rods, wires, tubes, and sheets, eventually ending up inside homes, factories, vehicles, and power infrastructure.

Is there money in this business?

Now, where’s the money in this entire chain of activities?

Copper mining is one of the most capital-intensive and time-consuming industrial activities in the world. The whole process from discovering a deposit to producing the first tonne of copper can take up to 20 years. Besides enormous amounts of capital, it also involves geological surveys, environmental approvals, land acquisition, drilling, and so on. A miner might spend billions of dollars for years — even decades — before earning a single rupee.

Perhaps it’s because of these huge risks that most companies only get interested in mining when copper prices are high. By that point, the economics look attractive on paper. But mining projects take many years to build. By the time new supply finally comes online, copper prices often have cooled, leaving companies with large investments that arrive too late in the cycle.

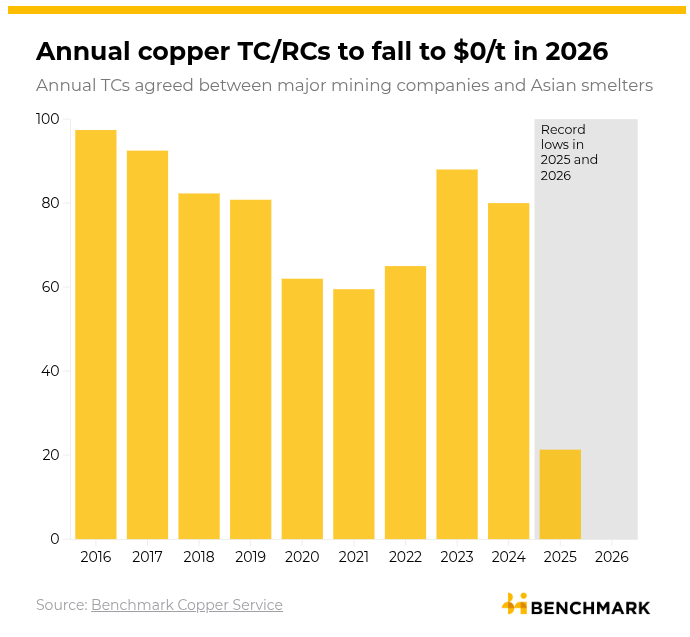

The economics of copper smelting, on the other hand, don’t benefit as much from high copper prices. Their margins depend on something called treatment charges and refining charges, known collectively as TC/RC.

When a miner produces copper concentrate, it sells that concentrate to a smelter. The smelter charges the miner a fee for processing the concentrate into refined copper. This fee is the TC/RC. When there are many mines and limited smelting capacity, smelters have bargaining power and can charge higher TC/RC. But with many smelters chasing limited concentrate, miners gain the upper hand, suppressing TC/RC.

In today’s world, smelting capacity has expanded faster than mining capacity. China, India, and parts of Southeast Asia have built large smelters, but new mines have lagged. As a result, smelters are competing aggressively for concentrate. This has pushed TC/RC to bedrock-low levels, squeezing smelter margins even with high copper prices. In the last 10 years, TC/RC rates have fallen from ~$100 to ~$20.

This dynamic explains why mining companies often benefit more directly from rising copper prices than smelters do. It also explains why countries that lack domestic copper mines remain vulnerable even if they have large refining capacity.

Smelting, by contrast, is faster and easier to scale. A smelter can be built in three to four years. This has led many countries, including India, to focus on refining rather than mining. But without secure access to concentrate, smelters remain exposed to global supply disruptions.

This brings us to India’s position in the copper ecosystem.

How is India doing?

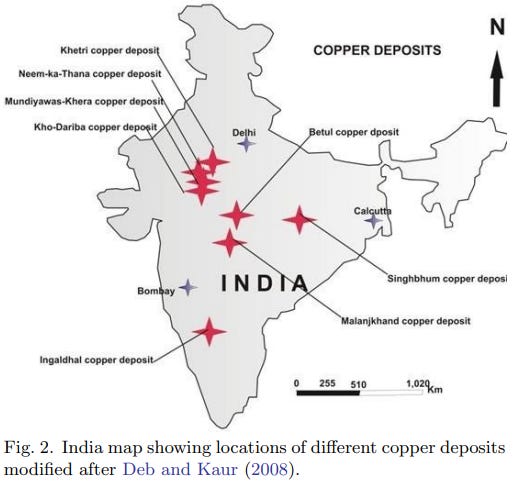

India consumes around 1.8 million tonnes of copper each year. And demand is growing steadily as the country builds power grids, rail networks, renewable energy capacity, and electric vehicles. However, India has very limited copper reserves. Our known deposits are small, low-grade, and geologically complex. As a result, domestic mining produces only ~50,000 tonnes of copper annually, a tiny fraction of national demand.

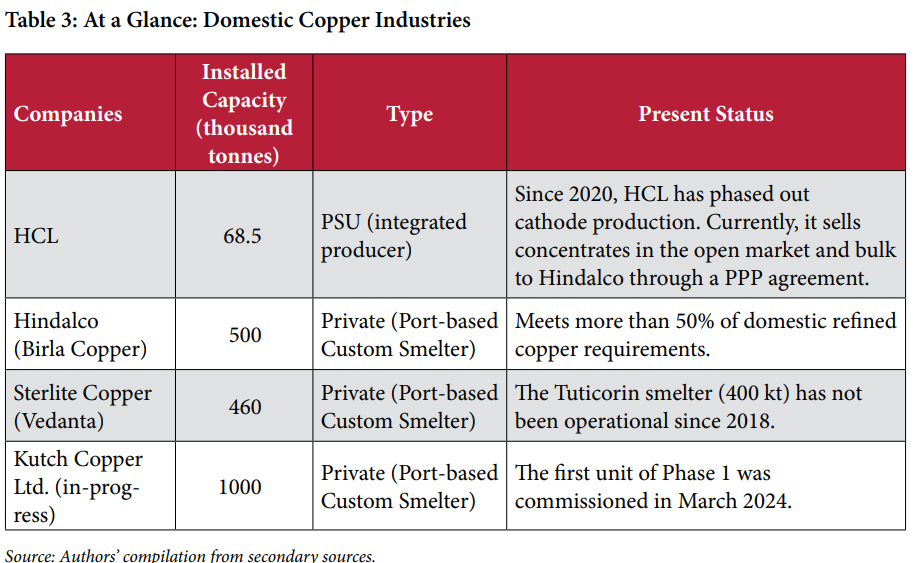

Hindustan Copper Limited, or HCL, a PSU, is the only vertically-integrated copper player in India. It owns most of the country’s operating copper mines, accounting for half of India’s known reserves. However, HCL has long struggled with operational inefficiency. A detailed report by the CAG highlighted issues ranging from delayed mine development to poor capacity utilisation and cost overruns. Despite owning valuable assets, HCL has not been able to scale production meaningfully.

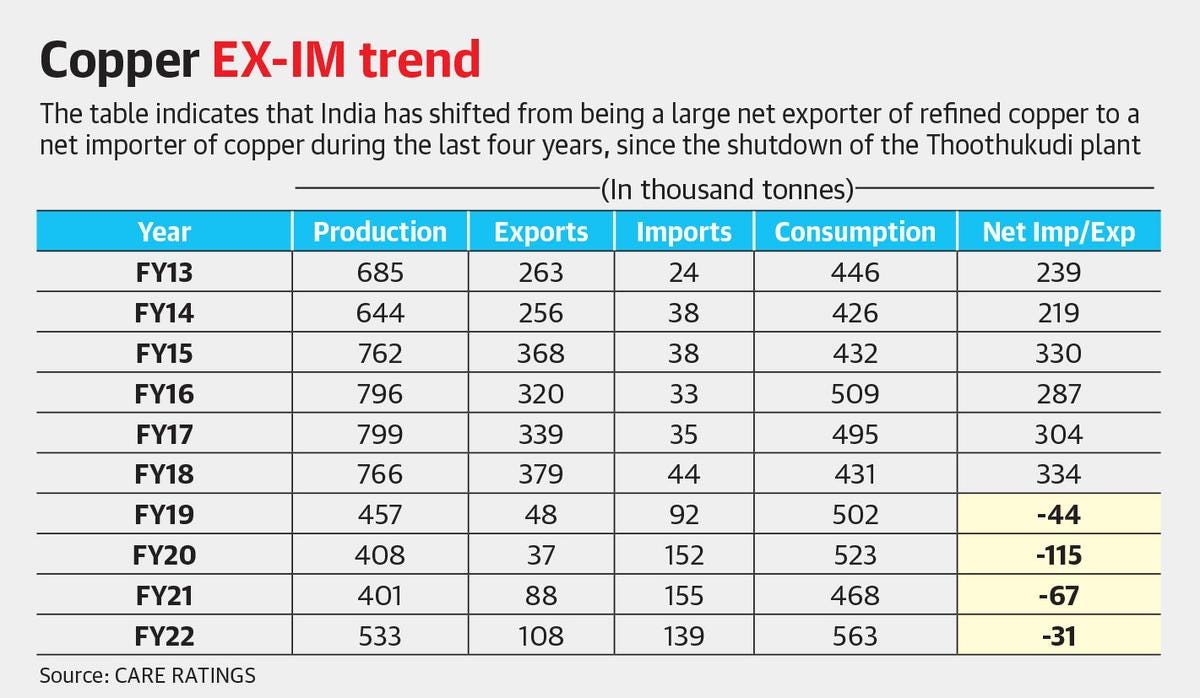

For years, India compensated for weak mining by importing copper concentrate and refining it domestically. This allowed the country to be a net exporter of refined copper even without a strong domestic ore supply — similar to how we refine oil. That changed dramatically in 2018, when the Sterlite Copper smelter in Thoothukudi, India’s largest copper smelter at the time, was shut down following protests and prolonged legal challenges. The plant had a capacity of ~ 4 lakh tonnes per year.

With Sterlite gone, India lost a significant portion of its midstream capacity almost overnight. Since then, the country has turned into a net importer of copper cathodes, relying on overseas suppliers to meet a gap that domestic production could no longer fill.

Then there’s Hindalco, the metals flagship of Aditya Birla Group. It operates a large, important smelter at Dahej, but its capacity alone has not been sufficient to bridge the gap. Meanwhile, HCL’s smelting and refining operations are relatively small compared to its mining.

More recently, Adani has announced plans to enter copper refining with a large smelter project targeting an eventual capacity of 1 million tonnes per year. While this could significantly reshape India’s copper landscape, such projects take time to ramp up and will still depend heavily on imported concentrate.

The world can’t get enough of this

Even with this primer on how the global copper supply chain works, we’ve barely scratched the surface.

Globally, the copper industry is entering a period of consolidation and strategic repositioning. Major miners are merging, governments are reassessing resource policies, and even technology companies are getting involved. Hyperscalers like Amazon, which build massive data centres packed with copper-intensive equipment, are exploring long-term supply agreements and even direct exposure to mining assets.

At the same time, recycling is gaining importance. Copper is infinitely recyclable, and recycled copper requires far less energy than primary production. However, in countries like India, recycling remains fragmented and informal, limiting its ability to meaningfully offset import dependence.

The world needs more copper than ever before, and producing it is getting harder, slower, and more expensive. For India, the challenge is sharper. Our appetite for copper is too high for our current capabilities. Unless mining efficiency improves or overseas partnerships expand, India will remain exposed to global supply shocks.

A nightmare quarter for Indigo

We’ve been covering Indigo’s quarterly results for a while. In none of those rounds, however, did we come to it with the sort of morbid curiosity that we did, this time around. To this point, the airline was the unquestioned star of Indian aviation, with a market share so high that it became a proxy for the entire sector. But then, it went through the worst crisis it had ever seen. As the airline learnt the hard way, a reputation built across decades can evaporate in the space of mere days .

Naturally, going into this quarter’s results, we had many questions. Would the company really talk about what happened? What is the scale of impact that an incident like this has on an airline of Indigo’s size? And looking out ahead from here, should you adjust your assessment of the company?

We’re not sure we have all the answers. But here’s what we learnt.

What the numbers tell us

On paper, Indigo’s operating revenue grew last quarter — rising by a little more than 6.2% since last year, to around ₹23,500 crore. Its operating cash flow, too, was in roughly the same territory as last year. The company’s EBITDAR — the cash it earned before paying tax, interest payments, leases, and wear-and-tear costs — dropped by just 0.8% to roughly ₹6,000 crore.

Its profit numbers*,* however, is where the dents begin to show. They collapsed by nearly 78% compared to last year, coming to just ₹550 crore. The company claims that if everything had run according to plan, it would have earned a profit of over ₹3,100 crore. But it took three severe hits.

The biggest of these was the one that, perhaps, made the least noise: exchange rates . Indigo has major payment obligations in dollars. For instance, many of its planes have been leased , and these leases are priced in Dollars. With the Rupee declining massively over the quarter, its future payment obligations ballooned. Taking that into account, the company had to book a massive paper loss, as a result, of over ₹1,000 crore.

Then, there were the labour codes. As we’ve written before, the new labour codes changed how most companies calculated the “wages” they pay. Suddenly, the amounts that they had previously kept aside for gratuity and leave encashment were no longer enough, and they now had to keep aside a lot more money. This was another paper loss — a one-time provision of roughly ₹960 crore.

The lowest hit of the three, though still massive, came from the airline’s December crisis. The company has provisioned a loss of roughly ₹580 crore. We’ll come back to that soon.

These are one-time hits, all things considered. For all the bad news around the airline, it isn’t in any sort of existential crisis. If this quarter is a disappointment, it is so because of what was expected , going in.

As recently as November, Indigo expected to grow in the high teens in this quarter. It was on track to add tremendous amounts of capacity, to meet all the new festive season demand it thought it would see. Meanwhile its costs seemed under control. All else staying the same, this should have been a quarter of sharp growth.

As it turned out, that expansion did come to be. Indigo added 23 new aircraft to its fleet. This meant that its “average seat kilometers” — a unit of how many people it could fly for how long — went up 11%. Its unit costs barely rose, and its fuel costs, relative to how much it flew, actually came down a little. In theory, its revenues should have grown substantially.

But perhaps because of all the chaos of the quarter, the passengers didn’t show up. The company admitted to a “subdued booking curve” after the incident ripped through its operations. Compared to the 11% jump in flight capacity, its passenger numbers were up by less than 3%. As a result, the airline flew emptier planes, with its “passenger load factor” dropping by 2.4%.

Indigo’s December nightmare

This brings us to the elephant in the room — the catastrophic failure that kept the airline in the headlines for weeks at an end.

The crisis: what we know

At the height of the crisis, in less than ten days between December 2 and December 10, 2025, the airline cancelled approximately 4,500 flights. The worst of these was December 5, when less than 4% of the airline’s flights reached their destination on time. Indigo’s dominance in India’s aviation market, in good times, gives it incredible strength. But in this case, it backfired severely. As the airline’s operations broke down, it turned into a nation-wide transit emergency, leaving over five lakh passengers stranded.

Chaos at the Bengaluru airport

How did things get this bad?

This topic has drawn a lot of speculation and innuendo over the last couple of months. You’ve probably seen most of it elsewhere. Most of it is hard to verify, so we’ll avoid mud-raking. But there are a few things we do know for a fact.

Back in January 2024, the Director General of Civil Aviation (DGCA) revised its norms around pilots’ working hours, through what are called the “FDTL Regulations”. Among other things, these regulations added an extra twelve hours to pilots’ weekly rest hours. They also drastically cut down on the number of night flights a pilot could be expected to fly. To maintain the same scale of operations, it would seem, any airline would have to greatly increase the number of pilots on its roster.

In all, airlines had until November 2025 — the better part of two years — to adjust to these norms.

It isn’t clear where, across this adjustment period, the failure actually took hold. Even early last November, the airline thought the new regulations would do little more than causing a “slight uptick” in costs. When Indigo first planned its schedule for the winter of 2025, it hoped to fly 10% more flights than last year, despite the new norms choking its pilot supply.

But as the season’s operations began, the strain was visible immediately. In November itself, the airline cancelled over 1,200 flights. Its on-time performance took a severe beating.

Early in December, though, a few additional ingredients turned this strain into a full-blown crisis. For one, the airline’s IT systems couldn’t handle the new regulations’ requirements, and kept creating illegal rosters. If Indigo needed a workable schedule, it would have to prepare one manually. Meanwhile, two other crises — a global Microsoft Windows outage and a bad spell of fog across North India — completely scrambled the airline’s running operations.

The FDTL Regulations had already stretched the airline, leaving no room for error. These new challenges became a knock-out punch. For days, the airline was effectively flying blind — it completely lost track of its crew, where they were, and how much they could be asked to work. That was when things fell apart.

The company’s view

A large part of the company’s investor call, as one would expect, revolved around the incident.

The company acknowledged the mishap, but didn’t go into the details of what went wrong. It merely noted that it was carrying out an “in-depth review” of the episode, and how it could make its processes more robust. Many analysts asked whether the company had a shortage of pilots, or whether it planned to hire more, but the company refused to say anything concrete.

Instead, the company’s focus was on what it did to recover from the mishap.

Its focus, the company claims, was to expand its customer support. Its ground staff, operations teams and customer service teams were brought in to work around the clock — to ensure that things were up and running as soon as possible. This brought the airline back on track, and by December 9, the worst was behind it. Soon, it was flying over 2,100 flights a day once again — carrying roughly 3.8 lakh passengers a day.

How convincing is this? We aren’t sure. The company claims that its “on-time performance”, or OTP, was good by mid-December. But it doesn’t actually give any numbers for the month. In its financial press release, it only gave OTP data between October and November — which looked reasonable at 76.6%. December’s data was omitted entirely.

Either way, the episode put a serious dent on the airline’s numbers for the quarter. It had to process a large number of refunds for their cancelled flights. It also gave out lakhs of vouchers for future flights, in what it called “gestures of care‘. Some stranded customers were given accommodation and meals. And soon afterwards, the DGCA added a ₹22 crore penalty on the company.

The exact hit the company took from this episode isn’t entirely clear. It was probably settling claims from irate customers well into January, and the vouchers it has given out could hit its earnings repeatedly over the next many quarters. Based on its estimates, though, the company made a provision of around ₹580 crore to “book” all those losses in the December quarter itself.

The landing strip

The incident, in all likelihood, will haunt the company into the future.

Already, the DGCA has asked the company to fly 10% fewer flights, dampening the rapid expansion it had planned. It was also forced to vacate its take-off and landing slots across many airports, so that other airlines could take over. It isn’t clear how long the pain will last. According to its management, Indigo’s sole focus, right now, is to make it smoothly through to February, despite all the hits it has taken. Even the coming summer, it says, is too far ahead to plan for.

It would be foolish to write the airline off, however. It is still, by far , India’s biggest carrier. It continues to fly thousands of flights every single day, ferrying crores of passengers over the course of a year. December’s incident might be an embarrassment, but it is not a fatal blow.

Tidbits

- Micron Technology will start commercial semiconductor production by February-end at its $2.75 billion Sanand, Gujarat plant, marking a key milestone in India’s chip-manufacturing push.

Source: ET - Indian drugmakers including Sun Pharma, Zydus and Alkem have received regulatory approval to launch cheaper generic versions of Novo Nordisk’s Wegovy and Ozempic ahead of the semaglutide patent expiry, intensifying India’s obesity-drug race.

Source: Reuters - Renault is rebooting its India strategy by relaunching the Duster and shifting focus to higher-margin, middle-class SUV buyers as part of its global growth push beyond Europe.

Source: Reuters

- This edition of the newsletter was written by Krishna and Pranav.

Tired of trying to predict the next miracle? Just track the market cheaply instead.

It isn’t our style to use this newsletter to sell you on something, but we’re going to make an exception; this just makes sense.

Many people ask us how to start their investment journey. Perhaps the easiest, most sensible way of doing so is to invest in low-cost index mutual funds. These aren’t meant to perform magic, but that’s the point. They just follow the market’s trajectory as cheaply and cleanly as possible. You get to partake in the market’s growth without paying through your nose in fees. That’s as good a deal as you’ll get.

Curious? Head on over to Coin by Zerodha to start investing. And if you don’t know where to put your money, we’re making it easy with simple-to-understand index funds from our own AMC.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()