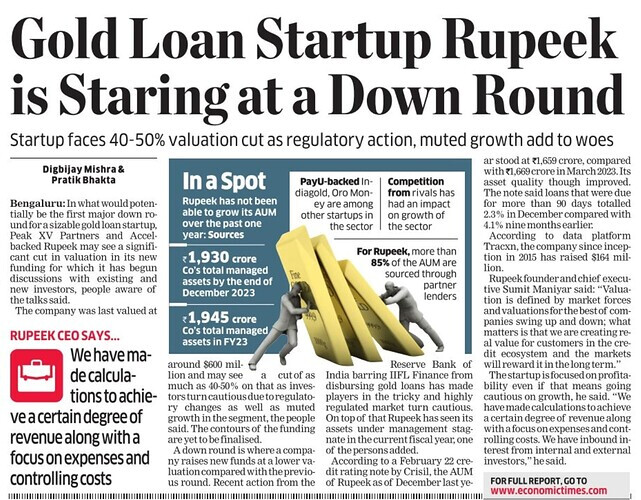

Rupeek, a gold loan startup is reportedly facing discussions for new funding rounds with both existing and new investors. However, the company may witness a significant devaluation of up to 40-50% from its last valuation of $600 million due to cautious investor sentiment stemming from regulatory changes and sluggish growth in the segment.

The recent RBI actions restricting IIFL Finance’s gold loan disbursements have contributed to market apprehension, coupled with Rupeek’s stagnant assets under management in the current fiscal year. Despite these challenges, Rupeek’s asset quality has improved, as indicated by a recent Crisil credit rating note.

NPCI granted permission to One 97 Communications, to operate as a third-party application provider on the UPI infrastructure. This move allows Paytm to offer UPI payment services through a multi-bank model, diverging from its exclusive partnership with Paytm Payments Bank Ltd.

Axis Bank, HDFC Bank, State Bank of India, and Yes Bank will serve as payment system providers for One 97 Communications, with Yes Bank acting as the merchant acquiring bank. This ensures uninterrupted UPI transactions and autopay mandates for existing users and merchants. One 97 Communications is urged to swiftly migrate existing handles and mandates to new PSP banks as needed.

RBI may need to reconsider its foreign ownership caps on government debt due to expected sizable inflows over the next few years from global bond index inclusion. Introduced in March 2020, the Fully Accessible Category (FAR) allows unrestricted foreign investment in central government bonds, rendering the existing 6% cap potentially obsolete.

With significant investments pouring into the FAR bracket following announcements by JP Morgan and Bloomberg regarding index inclusion, clarity on the cap’s future is crucial. The RBI has reportedly discussed the matter internally and is expected to provide clarification soon.

NBFCs anticipate stricter regulations from the RBI regarding financing for IPOs. Expected changes include implementing a standard minimum upfront margin requirement for customers borrowing funds from NBFCs for IPO applications. The recent directive to JM Financial to halt IPO and debenture financing underscores concerns over shallow credit assessments and thin margins.

Despite charging up to 13 percent interest for IPO financing, NBFCs find it lucrative due to minimal risk, especially with oversubscribed IPOs. However, regulators are scrutinizing practices such as inflating bids through multiple applications, posing risks for NBFCs if market sentiment shifts.

This scrutiny may lead to defined limits for IPO financing and stricter oversight of bidding practices, potentially impacting NBFCs’ margins of safety.