Indian P2P lending platforms, including Liquiloans and Faircent, are halting instant withdrawal products for customers following regulatory concerns raised by RBI. This move, initiated by the Association of P2P Lending Platforms, aims to address the central bank’s disapproval of high-risk schemes resembling fixed deposits.

The decision comes after RBI officials criticized such offerings during inspections of NBFC-P2Ps. Fintech partners like Cred and BharatPe will also need to cease instant withdrawal features, aligning with the industry’s self-regulation.

The Ministry of Information and Broadcasting has cautioned social media influencers against promoting offshore online betting and gambling platforms, advising intermediaries to refrain from publishing such content targeting Indian audiences.

The advisory, issued ahead of the IPL starting on March 22, follows concerns raised by the Central Consumer Protection Authority (CCPA) about celebrity endorsements of these platforms, citing their illegality and guidelines on misleading advertisements.

Despite recent stock market volatility, individual investors are increasingly borrowing to invest in shares, particularly mid-cap stocks hit hard by the recent sell-off. Margin funding, short-term loans for share purchases, has risen to ₹59,300 crore as of March 20 compared to ₹58,400 crore on February 29. Notable stocks bought using margin funding include NHPC, Yes Bank, and Zee Entertainment, with bets ranging from ₹400 crore to ₹760 crore.

SEBI has instructed Indian mutual fund managers to halt accepting investments in plans that invest in overseas ETFs due to nearing a $1-billion sectoral limit.

AMFI, acting on SEBI’s directive, has directed fund houses to cease accepting lumpsum investments in such plans from April 1, with existing systematic investment plans to be paused. While the overall industry limit for investments in overseas mutual funds is $7 billion, there’s an additional $1-billion limit for foreign ETFs.

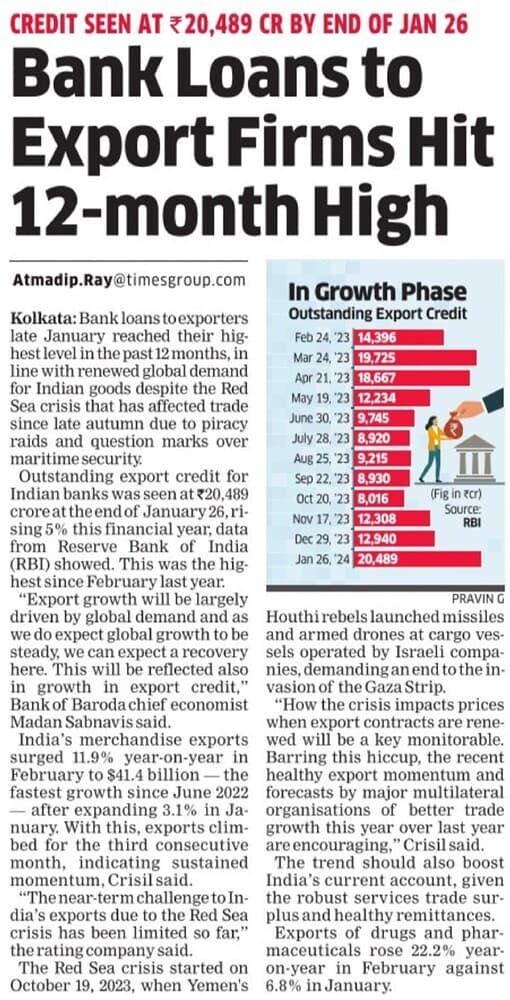

Despite challenges posed by the Red Sea crisis, Indian bank loans to exporters hit a 12-month high at ₹20,489 crore by late January, reflecting renewed global demand for Indian goods.

This surge, up 5% from the previous year, aligns with India’s merchandise exports growth of 11.9% year-on-year in February to $41.4 billion, the fastest since June 2022. The sustained momentum in exports, including a notable increase in exports of drugs and pharmaceuticals, signals resilience amidst the crisis, with forecasts suggesting continued growth.

Banks, insurers, and broking firms are actively recruiting talent from uncertain tech startups to bolster their digital capabilities. Recent months have seen numerous executive movements from companies like Paytm, Byju’s, and Swiggy to organizations such as Kotak Mahindra Bank, HDFC Bank, and Bajaj Finserv.

What are you reading today? Drop your suggestions here ![]()