Paytm has experienced a significant decline in its unified payments interface (UPI) market share, dropping from 13.3% in April 2023 to 8.4% in April 2024. This decrease, attributed to various factors including regulatory restrictions on its associated company, Paytm Payments Bank Limited (PPBL), has affected its ability to onboard new customers.

Paytm’s reliance on UPI for a significant portion of its gross merchandise value (GMV) underscores the importance of maintaining its relevance in the payments platform. Meanwhile, PhonePe, the UPI market leader, has seen its market share rise to around 48-49%, with consistent dominance in transaction value.

Paytm’s efforts to mitigate this decline include transitioning to a third-party app model and partnering with banks like Axis Bank, Yes Bank, SBI, and HDFC Bank for its payment services.

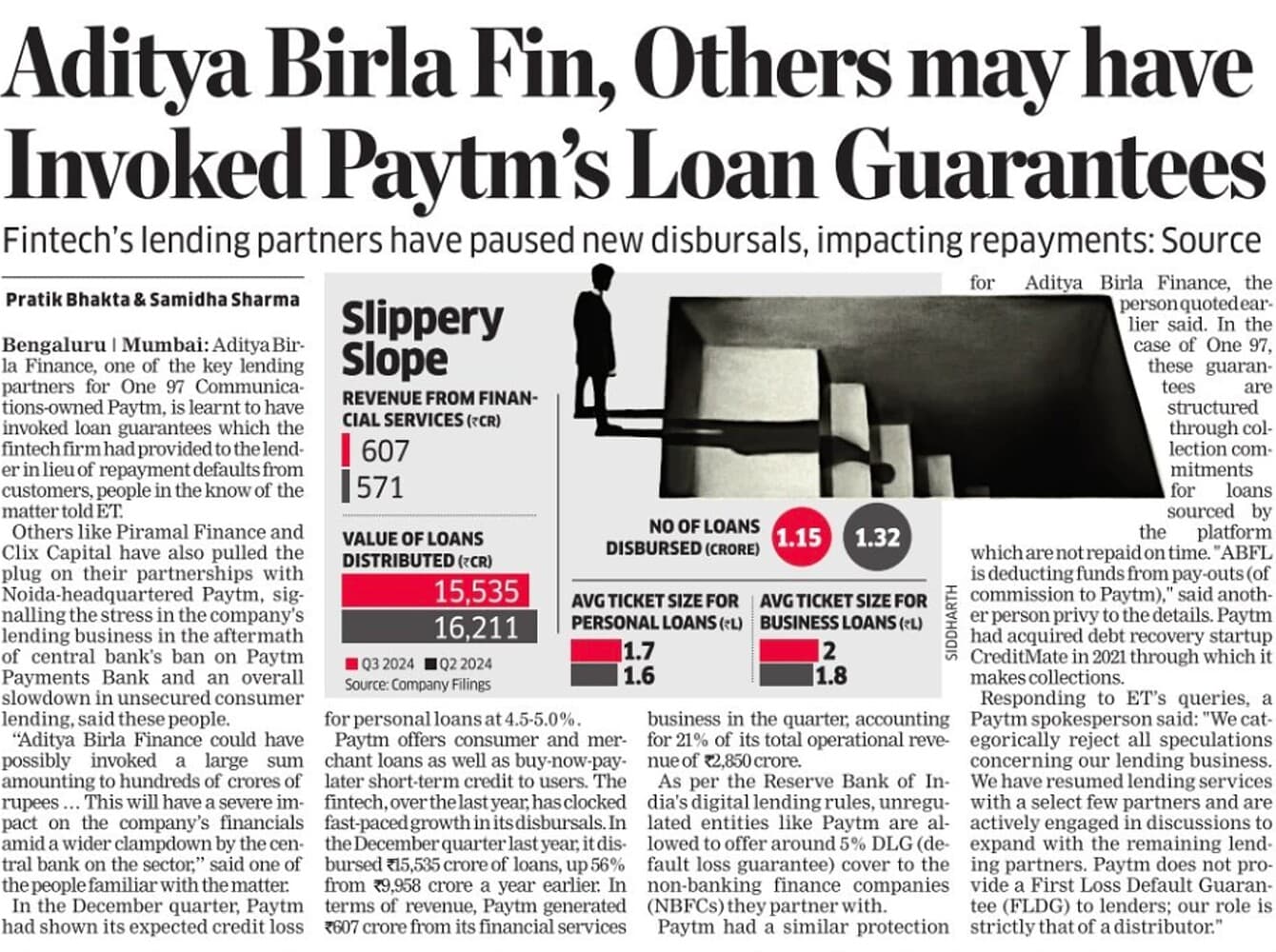

Aditya Birla Finance, a key lending partner for Paytm, has reportedly invoked loan guarantees due to repayment defaults from Paytm’s customers. Other partners like Piramal Finance and Clix Capital have also ended their partnerships with Paytm, indicating stress in Paytm’s lending business following regulatory actions against Paytm Payments Bank and a general slowdown in unsecured consumer lending.

The invocation of guarantees by Aditya Birla Finance, possibly amounting to hundreds of crores of rupees, is expected to severely impact Paytm’s financials. Paytm, which offers consumer and merchant loans, as well as short-term credit, saw significant growth in loan disbursals and generated revenue of ₹607 crore from its financial services business in the December quarter.

Paytm’s guarantees to lenders are structured through collection commitments for loans not repaid on time, with Aditya Birla Finance deducting funds from Paytm’s payouts. Paytm denies providing First Loss Default Guarantee (FLDG) to lenders and states its role is strictly as a distributor.

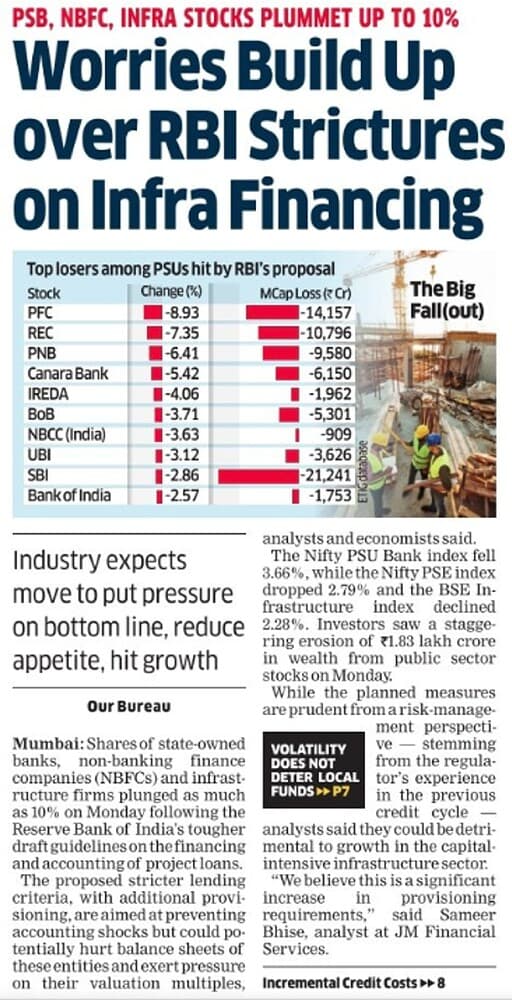

RBI proposed new rules for banks and financial companies, as well as infrastructure firms that makes it tougher for them lend money for big projects and require them to set aside more money as a safety measure. These might hinder growth in the capital-intensive infrastructure sector, at least that what the markets thought because the shares of these entities plummeted 10% yesterday because of this draft guidelines.

Venture investors and startup founders note a scarcity of new unicorn sightings among early-to-mid-stage startups, attributing it to the absence of substantial investment known as ‘leap of faith capital.’ While early-stage deals continue across sectors, major investors like SoftBank and Tiger Global primarily support established startups or those nearing potential IPOs.

Only two startups, Perfios and Krutrim AI, have achieved unicorn status in 2024, compared to two in the entirety of 2023.

Investors are cautious, re-evaluating previously passed-on companies due to skepticism. Late-stage deals are increasing, with 10 happening last month, up from four in April 2023, signaling a gradual improvement in investment sentiment. Despite this, funding largely targets fast-growing and profitable companies, with the total venture funding for the January to March quarter down compared to the previous year.

Early-stage startups, including those founded by former senior executives at large unicorns, are managing to attract investment.