PPFAS Asset Management is setting up a GIFT City subsidiary to offer dollar-denominated products, targeting NRIs and foreign investors seeking easier access to Indian equities without complex paperwork. Rajeev Thakkar, CIO, sees GIFT City as a strategic move to tap into a new customer base.

He notes Foreign Portfolio Investors (FPIs) have been selling due to valuation concerns and reallocations, with ‘Sell India, Buy China’ among potential reasons. Despite FPI selling and rising IPO activity, Thakkar is confident in India’s long-term growth story.

NSE has extended the inactivity period for trading accounts from 12 to 24 months, allowing more transaction types (e.g., IPOs, mutual funds) to count as active trades. Inactive accounts require in-person verification and updated client details for reactivation, a move aimed at enhancing client service, security, and operational efficiency for brokers.

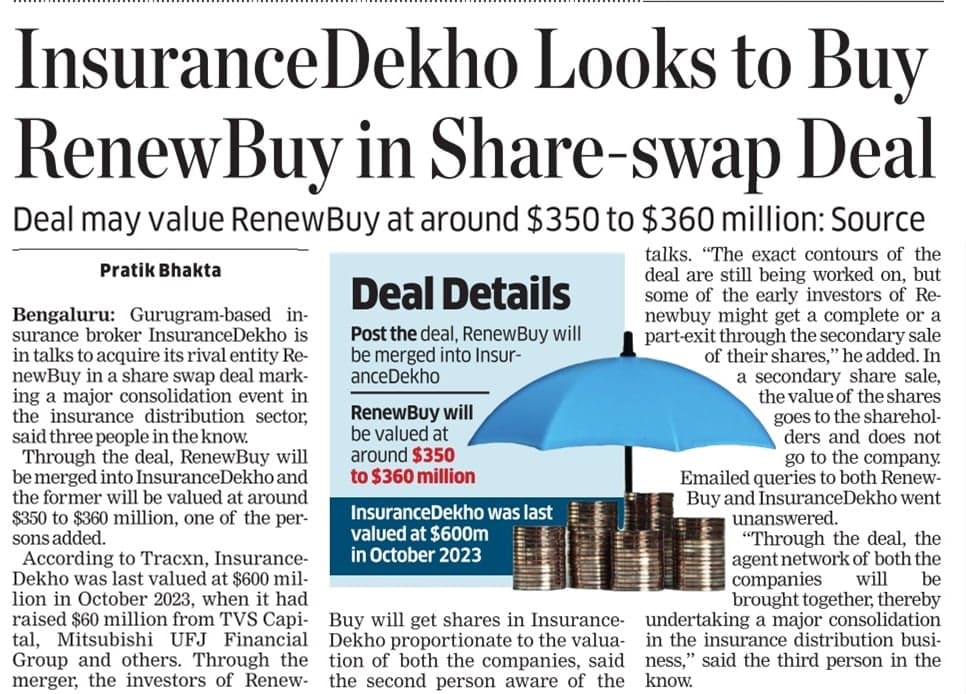

InsuranceDekho is set to acquire rival RenewBuy in a share swap deal, valuing RenewBuy at $350-360 million. This merger will consolidate their agent networks, and some RenewBuy investors may get partial exits through secondary share sales.

But how will it be helpful for NRIs… I understand the fund will be denominated in USD, but ultimately the underlying asset will be India in INR. So how will this benefit NRI.

NRI invest in USD. This gets converted to INR to invest in companies and everyday the NAV gets re converted back to USD. So not sure how will it benefit.

When a resident Indian invest in Nasdaq 100 fund where the underlying are US stocks, INR get converted to USD and it remains. There is double benefit i.e price increase in Nasdaq stocks plus INR currency depreciation.

When you do the opposite, USD gets converted to INR, currency depreciates and then reconverted back to USD. It will be lower.

Am I going nuts or is my logic correct. Why would PPFAS do this. What is the benefit. I can understand if it is for foreign nationals who wish to invest in India.

Can someone guide us here please.

I would agree if the underlying is US Stocks like Nasdaq 100 etc.

Between 2023 and 2024 inr depreciation is 1 rupee. Suppose assume a person sold usd stocks and gained $8000 in profits. Thr additional amount adds to 8000 rupees due to the usd inr conversion. It could only cover the expenses (brokerages + outward remittance cost at the US + inward remittance cost in the India).

The appreciation shows up if one has substantial amount of USD (few millions) and the appreciation is like that of 2014-2020. This time we had 30 rupee depreciation. This means the amount must be larger and it has to take something to have rupee get depreciated hard.

So my understanding is that the American equities must beat Indian equities substantially like covering the charges and the slab taxes on the FOFs. Otherwise Indian equities is ok’ish .