The period from 2014 to 2020 was dominated by the stock market success of the FAANG stocks. What perpetuated this game so long were four things. 1) The uninterrupted nature of their sales growth, 2) an extended and historic bull market in stocks, 3) a substantial downward movement of interest rates, and 4) the way the COVID-19 lockdowns accelerated their sales growth with home imprisoned customers.

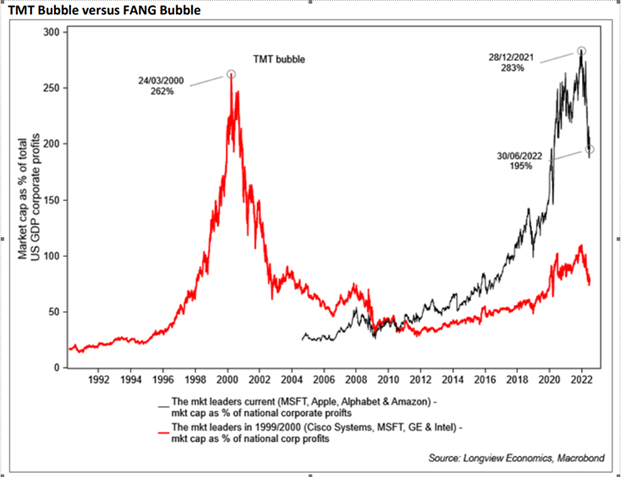

It took years for the tech bubble stocks of 1999 to get interesting. Microsoft (MSFT) peaked at around $58 per share and was $28.50 per share in 2012. Intel (INTC) and Cisco Systems (CSCO) have never made it back to their 2000 highs. Will Amazon (AMZN), Facebook (FB/META), Netflix (NFLX), Alphabet (GOOGL), and Apple (APPL) be any different?

At some point, persistently high inflation will hit demand harder than it already has. At some point, revenue growth and earnings growth will be much harder to come by as consumers push back or retrench. Tightening financial conditions will contribute to this pulling back. It’s a certainty – the only question is when and how high interest rates have to go for this to happen. The stock market knows this, hence the record volatility seen during the first nine months of this year.

History is filled with almosts. With those who almost adventured, who almost achieved, but ultimately, for them it proved to be too much. Then, there are others. The ones who embrace the moment, and commit. And in these moments of truth . . . they calm their minds and steel their nerves with four simple words that have been whispered by the intrepid since the time of the Romans. Fortune favours the brave.

Four decades of falling inflation and declining interest rates have come to an abrupt halt—and that’s changed the calculus on a fistful of financial decisions.

Zero-interest rate policy began after the Great Financial Crisis and only ended with the September Fed hike. Europe even toyed around with negative interest rates for a while. It was wild.

ZIRP is not the normal state of the monetary system. Where we are today is normal. Savers should be paid to wait, and the risk-free interest rate should not be zero. That was insane. Everyone got so high on the supply of free money that we forgot the basics of how money works. Unwilling to park cash in zero-interest savings accounts, investors went on a mad dash of risk-taking.

“Much of the wealth in the world is hypothetical. Notional. One might even say imaginary.”

Non-finance

“Our relentless chase for status (and the showboating of it) is a cancer that masquerades as success. It reinforces the worst incentive structures that humanity has ever thought of, and furthers the narrative of self-interest and groupthink to all those who thirst for it.”