On December 18, SEBI is expected to approve key regulatory changes. For SME IPOs, the minimum application size may rise to ₹2-4 lakh, eligibility norms will tighten, and promoter lock-in may increase to five years. The ambit of Unpublished Price Sensitive Information (UPSI) could expand to include restructuring plans, fundraising, and bank settlements. Angel funds may be limited to accredited investors, with minimum investment lowered to ₹10 lakh and maximum raised to ₹25 crore.

SEBI may also introduce net worth-based categories for investment bankers and revise rules for appointing public interest directors on market infrastructure institution boards.

SEBI has proposed a platform called MITRA (Mutual Fund Investment Tracing and Retrieval Assistant) to help investors locate inactive mutual fund folios (no transactions for 10+ years). Developed by registrar and transfer agents, MITRA aims to reduce unclaimed folios, encourage updated KYC compliance, and prevent fraudulent redemptions.

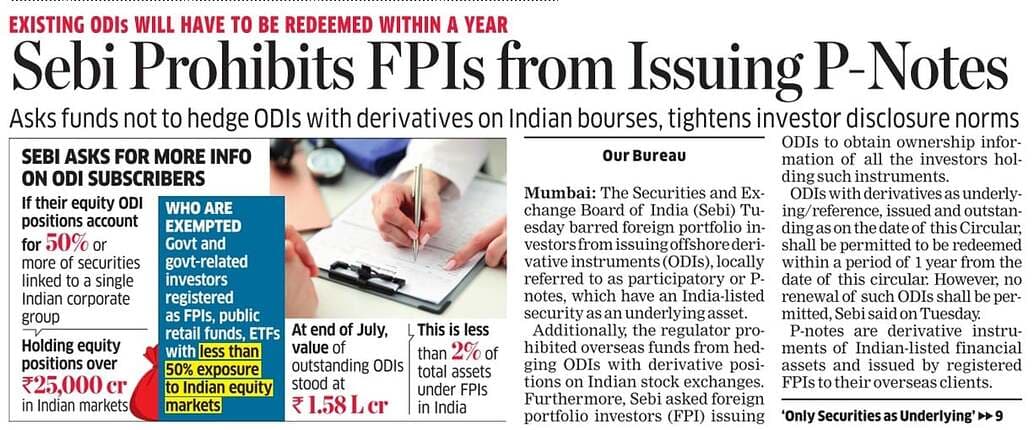

SEBI has prohibited Foreign Portfolio Investors (FPIs) from issuing Participatory Notes (P-notes) that have derivatives as their underlying assets. This means FPIs can no longer offer these instruments to foreign investors seeking exposure to Indian derivatives without direct registration. Existing P-notes with derivative underlyings must be redeemed within a year, and no renewals are permitted.

Additionally, FPIs are barred from hedging these instruments with derivative positions on Indian stock exchanges. Going forward, P-notes can only have securities (excluding derivatives) as underlying assets and must be fully hedged with the same securities on a one-to-one basis throughout their tenure.

Razorpay plans to shift its parent company’s domicile from the US to India, incurring a $200 million tax payout, aiming for an IPO in two years. Its core payments business is profitable, but overall profitability is expected in 1.5 years. The company processes $180 billion annually and earned ₹2,501 crore revenue in FY24. Razorpay seeks to expand non-payments businesses, despite challenges from mandatory full KYC regulations.

With the RBI raising concerns over unsecured loans, fintechs are shifting focus to secured lending, including micro loans, property loans, and green financing. This pivot involves physical verification, branches, and on-ground staff, but is more cumbersome. RBI measures, like increased risk weights, have slowed consumer loan and credit card growth significantly.