The likely reason why Yes Bank couldn’t write-off their Tier 2 bonds was because those bonds were Basel II - Upper Tier II bonds. Those bonds do have some loss absorption capacity (like delaying interest payments) but can’t be written off completely. This CRISIL document briefly explains about it -

Upper Tier II capital (under Basel II): These instruments have a minimum maturity of 15 years. In conjunction with lower Tier II capital, upper Tier II capital cannot exceed 100% of Tier I capital. Interest and principal payments on upper Tier II capital will not be made on time if the bank’s capital adequacy falls below 9% or if RBI refuses permission to pay interest when the bank declares losses, or will declare losses if the interest is paid. As a result, upper Tier II capital has good loss absorption capacity. Such a default can be cured subsequently by paying past overdues. The issuer can call back the instrument with prior approval of RBI 10 years after the date of issue. At the same time, the issuer can also offer to step up the coupon by 100 basis points. No put options are provided on the instrument. The issue of upper Tier II capital is allowed by RBI (unless it is in the nature of preference shares, which are currently not permitted).

But in the case of LVB, their Tier 2 bonds were Basel III Tier-2 bonds. Those bonds have a Point of Non-Viability (PONV) trigger which allows for the write-off. This CRISIL document briefly explains about it -

Basel III-compliant Tier II capital instruments have additional features that distinguish them from such instruments under Basel II.

The key distinguishing feature is the PONV trigger, the occurrence of which may result in loss of principal to the investor and hence, in a default on the instrument. However, CRISIL believes the PONV trigger is a remote possibility in the Indian context—a robust regulatory and supervisory framework and the systemic importance of the banking sector are expected to ensure adequate and timely intervention by RBI to avoid a situation wherein a bank becomes non-viable. The inherent risk associated with the PONV feature is adequately factored in the bank’s CCR.

Hence, CRISIL’s rating on Basel III-compliant Tier II capital instruments could typically be the same or one notch lower than the CCR of the bank.

Even though the document states that “PONV trigger is a remote possibility in the Indian context” but LVB Basel III Tier-2 bond write-off is the first time it has been used.

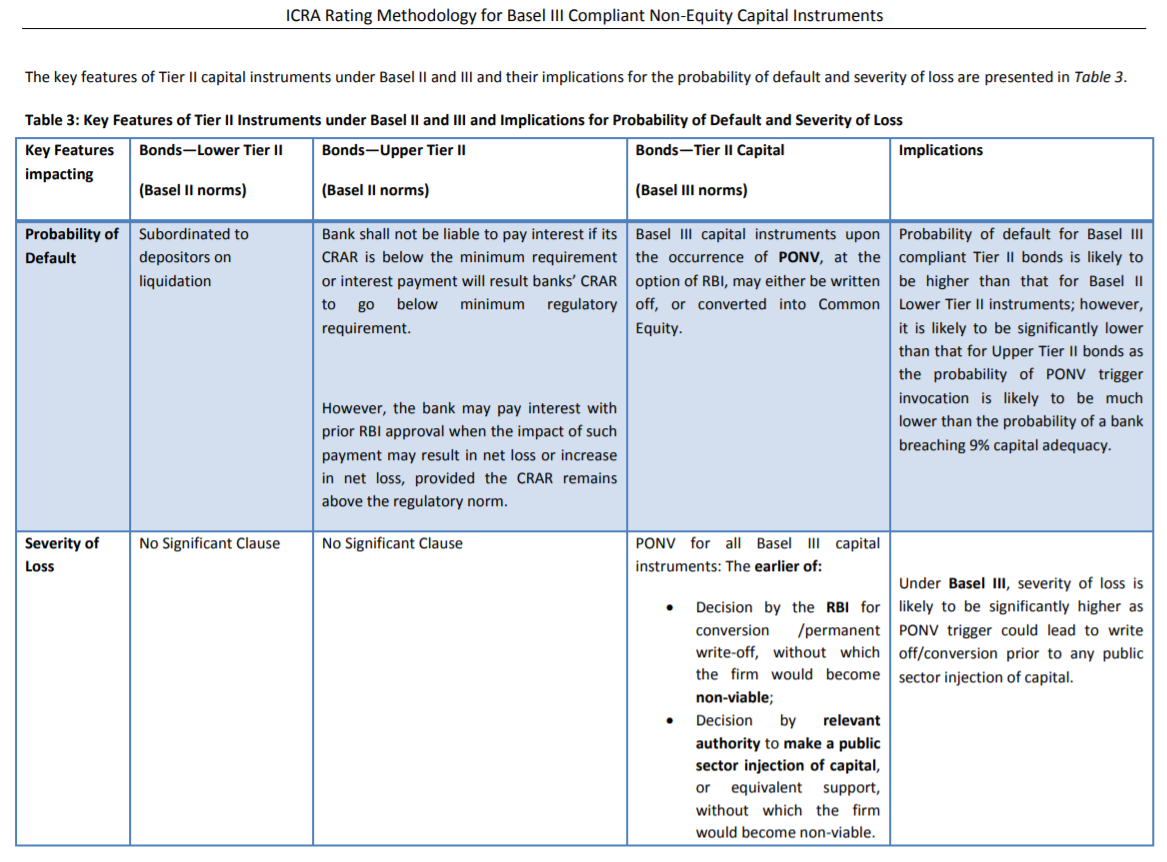

This table from a ICRA document briefly compares Basel II and Basel III Tier-2 bonds side by side -

Equity shares can be written off because the rules allow for that. The CRISIL document that I shared above, says the following about it -

Equity: Part of Tier I capital, equity is perpetual, with no put or call options. There are no contractual payments to be made, and equity has the maximum loss-absorption capacity of all classes of capital.

The following post by @Karthik in a different forum thread explains this in much more detail -

Also, this article speculates about other reasons why RBI might have decided to write-off LVB shares.