Hi so for today’s market there is a short straddle trade which was executed it ended in overall loss would want to know your thoughts on what could have been better and any other advise that you would have

nifty 17100 CE @ 131

nifty 17100 pe @ 127

As market went down sl hit for pe at 191

holding the ce till full market end hours finally exited it at 125 overall a loss

Let me know what could have been better and any advise that you would have

No i was aware that opstra is for backtesting only and for live data you need to pay subscription

Let me know if i need to update myself and include in my daily strategies and will surely add

What I think is as options are risky, it is better to check the strategies before deploying in real time. We will know how much we can gain or lose before market opens. Of course, as the premiums change, the gain and loss will change too, but we will have good idea before hand.

And we can even try different adjustment scenarios to either increase the gain or decrease the loss before and can be ready when market opens, not that market will not surprise us, but we will have some idea about the loss at least, particularly when we are selling.

I use Sensibull, so I am saying this. I don’t know about Opstra.

so how i got to this is i had bought the subscription of opstra there it had the option simulator in that i rigorously tested straddles purely intraday and it showed good results in log terms payoff was positive so after that i did paper trades and then executed it

from the first day of real deployment out of 17 trading days red are only 2

Problem is that when in green i exited it very early and like the example of today when in red i tend to hold it as per the rules that i had backtested result is that thse two days have eaten up the green days and net now in 0

So I wrote this here hoping to seek some advise on probably something that i was doing wrong

So you are not taking positional trades and are deploying these strategies intraday only, and booked profits early and waited till EOD for the market to reverse? Why are you booking profits early, did you not have target and stop loss before taking the trade?

I don’t know if back testing rules work 100% the same in live market, particularly when market is unpredictable with calls and puts both going up and down.

And what was your view for today, did you choose short straddle thinking market will be range bound?

On a side note, no gain or no loss after 17 trades does not look that bad, compared to the experience you got in the market.

Probably you are right i should still to green days as i stick to red and today yes i was aiming it to be range bound and the premiums were good so 100 points plus minus i was good but I guess probably the gamma spiked and it resulted in this

It will work most of times but one good gap up or down will erode entire profits made . And also it depends on which day you take it . Might not work from Thursday to Friday on many days . Plus it is assuming premium decay but what if premiums are building up before any event or volatility grows . And there is something we can’t measure ie market sentiment, one value may increase and other won’t bulge . Bottomline lot of understanding is required before you you do it naked . Till then hedge positions with option buy at otm, but it will eat away much of the profit, though you can take more lots due margin benefit but more lots means it kinda becomes leveraged and beats the purpose of risk management

Option selling is best done intraday near expiry day or on expiry day. Always use stop or hedge. Also with hedges you can reduce your margin requirements.

There are now multiple platforms where you can backtest option strategies for free like

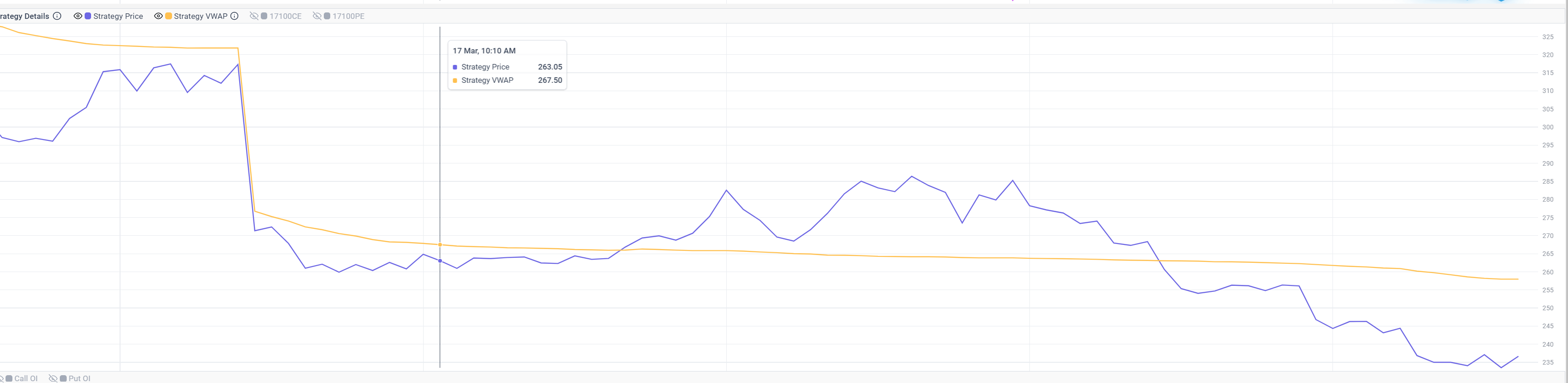

Can explore this Sensibull - India’s Largest Options Trading Platform . Seeing this chart , you probably entered at lowest point in the day . Prev day .Straddle close was 312 and you entered at 258. So , your entry was at very bad point.

Straddle is toughest to handle , also ROI wise( transaction charges is quite high). But if it’s done very specialized than it can be lucrative as well.

I use 1:2 risk reward based upon premium . So , I usually do 1-2 hr straddle keep 5 points SL and 10 points target and Trailing SL.

Entry can be at IV Spike is good Risk Reward. You need to have IV and Direction understanding.

Overall , i don’t do Straddle anymore as its very risky to handle in positional . Intraday wise it can be good but you can do only few adjustments and gamma risk is huge.

Straddle is very good if you have good sense of direction and one of the best hedging technique in IV fall and Direction Straddle scenarios.

Hi I tried th sensibull vwap and option price which you had shared and had a few questions to it like this is the logic of you buy the spikes and then exit on the cools as we are on the short side and would want to collect Max premium,

Also if you have a detailed video somewhere or an article that you could share for this which explains it step by step i think that would be a good start for me to actually have the comparison in real market hours as well and then i can tie this back to my exiting strategy for effectiveness

There is no one size fits all shirt.its upto your risk profile, duration of strategy of what you want to do.For youtube i doesn’t have any channel but if you type Straddle there will be 1000s of videos as its the most sold strategy on the planet .Every tom dick and harry is selling courses on Straddles with 100s of varieties.

Bottom line is Risk management, Position sizes, IVs and Direction. No fix formula

Just one quick question and let me know if my understanding is correct

Given spot is at 17000 then if i look for a otm option which has approx delta of .16 and approx theta of say 5 so this would mean that irrespective of where the market goes i can expect roughy about 3 points coming from thins taking the other points to go away for when the gamma spikes just in case

Then just see option chain ,price and delta . Read about synthetic future, Analyse sum of Atm premium over time ,difference in premium between 2 strikes etc.Rest you will understand yourself,also do paper trading.

It never does.

It’s not linear. It’s based on the second order of derivatives. [Simplier words - You don’t do risk-reward in Adani when there is news on it. News = Fear = Premiums High = Why High? Think in greek’s perspective!]

If you tell just about any greeks, the risk-to-reward ratio is fairly complex.

But if you just tell the basic Option Premium stuff. Then Yes, it is same risk reward concept.