@Meher_Smaran and I were discussing ways to share our small little knowledge with traders and readers by covering trading concepts, margin requirements, and even arbitrage opportunities. This is the very first post in that series. The theoretical part has been put together with the help of GPT, while we’ve worked on the calculations ourselves. We’re eager to learn and grow along with you as we explore these topics.

Let’s dive into the topic.

A synthetic futures position is a powerful options strategy that perfectly replicates the risk and reward profile of a traditional futures contract. It’s created by combining a long call option and a short put option on the same underlying asset, with the same strike price and the same expiration date. This strategy is particularly useful for traders who want to gain exposure to the underlying asset’s price movements without directly buying or selling a futures contract, often with capital efficiency and lower costs.

The core principle behind this strategy is put-call parity, which states that the value of a synthetic long future (Long Call + Short Put) is equivalent to the value of a long futures contract. This allows traders to replicate the unlimited profit and loss potential of a future, creating a symmetric payoff.

Constructing a Synthetic Long Future

To create a position that mimics a long futures contract, a trader must execute two simultaneous option trades:

Synthetic Long Future = Long At-The-Money (ATM) Call Option + Short At-The-Money (ATM) Put Option

The following conditions are critical for an accurate replication:

- Same Underlying: Both the call and put options must be on the same asset (e.g., NIFTY 50).

- Same Expiration Date: Both options must have the identical expiry date.

- Same Strike Price: Both options must share the same strike price. For the purest replication of a futures contract’s delta (price sensitivity), the at-the-money (ATM) strike—the strike price closest to the current futures priceis typically chosen.

The long call leg provides the position with its unlimited upside potential, gaining value as the underlying asset’s price rises. The short put leg creates an obligation to buy the underlying asset if its price falls below the strike, thus generating the downside risk profile that is characteristic of a long futures position.

Deconstructing the Payoff Profile

While individual options have non-linear, asymmetric payoff profiles, combining them in a synthetic structure results in a linear, symmetric payoff identical to that of a futures contract. The non-linear components of the options (gamma and vega) effectively cancel each other out, leaving a position that is primarily sensitive to direction (delta).

A crucial nuance often overlooked is the position’s breakeven point. Unlike a standard futures contract where the breakeven is simply the entry price, the breakeven for a synthetic future is adjusted by the net premium paid or received at the time of initiation.

When buying a call (premium paid) and selling a put (premium received), there is a net cash flow. If the call premium is higher than the put premium, it results in a net debit. The position only becomes profitable after the underlying asset’s price rises enough to cover this initial cost.

Therefore, the breakeven formula is: Breakeven Point = Strike Price + Net Debit Paid

Conversely, if the put premium received is greater than the call premium paid, it results in a net credit, and the breakeven point would be Strike Price - Net Credit Received.

Futures vs. Synthetic Futures: A Detailed Comparison

While both strategies offer similar payoffs, they differ significantly in their mechanics and the associated charges and risks.

| Feature | Traditional Futures | Synthetic Futures (Long Call + Short Put) |

|---|---|---|

| Position | A single contract | Two simultaneous positions (long call, short put) |

| MTM | Applicable. Daily Mark-to-Market (MTM) settlement of profits and losses. | Not applicable. Only premium is paid/received upfront. |

| Margin | Higher. Requires an initial margin (SPAN + Exposure) and a maintenance margin. | Potentially lower. Margin is required only for the short put, which can be slighly less. |

| Charges | Higher due to Securities Transaction Tax (STT) on the contract’s total turnover. | Lower. STT is only on the sell side (in-the-money options) and not on the entire turnover, leading to substantial savings. |

| Expiry | Available only for near, next, and far-month contracts. | Can be created using far-month options, offering more flexibility and a longer time horizon. |

| Liquidity | Generally high for all contract months. | Liquidity depends on the individual options (call and put) and can be a challenge for far-month or out-of-the-money options. |

The Role of Mark-to-Market (MTM)

Mark-to-Market (MTM) is a daily settlement process used exclusively in futures trading. At the end of each trading day, the exchange values your open futures position at the closing price. If you have made a profit, the amount is credited to your trading account. If you have incurred a loss, the amount is debited from your account. This process continues until you square off the position or the contract expires.

For example, if you buy a Nifty future at ₹24,000 and it closes at ₹24,050 on day one, you will be credited with the profit for that day. If it closes at ₹23,980 on day two, the loss will be debited from your account. This means you must have enough cash in your trading account to cover daily losses, or the RMS may square off your position.

In contrast, synthetic futures, being an options strategy, do not have this daily MTM settlement. The cash outflow is limited to the initial premium paid for the long call and the margin required for the short put. You are not required to bring in cash daily to cover notional losses.

Live Example with Nifty and Zerodha Brokerage Calculator

Let’s use a hypothetical example for a Nifty Futures contract to illustrate the difference in charges.

Scenario: A trader wants to go long on Nifty with a lot size of 75.

Case 1: Traditional Nifty Futures

- Nifty Futures Price: ₹24,600

- Contract Value: 75 quantity * ₹24,600 = ₹18,75,000

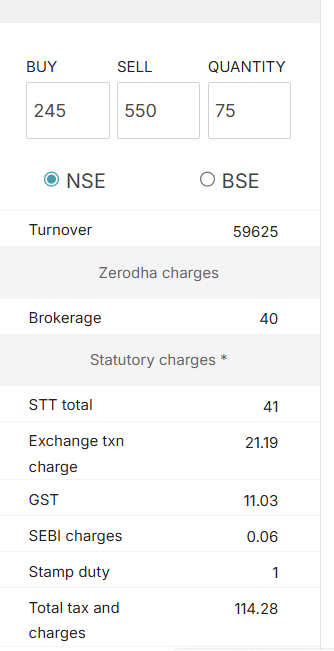

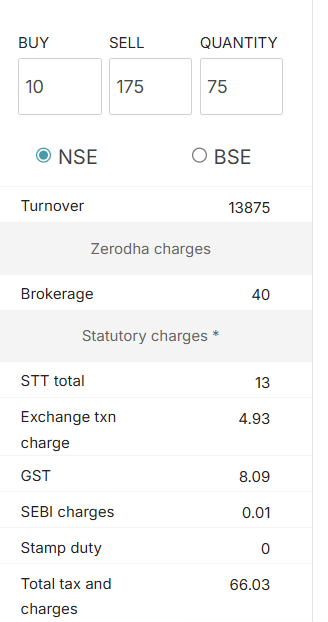

Case 2: Synthetic Futures

- Nifty ATM Call Option (Strike 24600): Buy at ₹245

- Nifty ATM Put Option (Strike 24600): Sell at ₹175

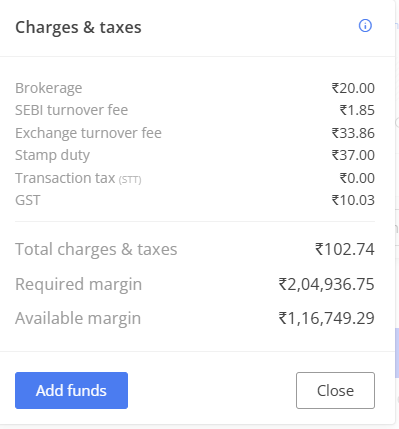

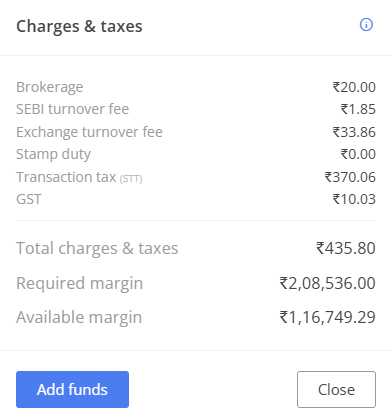

1. Charges for Traditional Futures

Using Zerodha’s brokerage calculator, the charges for a buy trade come to about ₹102.74. On the sell side, the charges are approximately ₹435.80. So, if the trader squares off the position at the same price, the total cost of the round trip (buy + sell) would be:

₹102.74 + ₹435.80 = ₹538.54

2. Charges for Synthetic Futures

In the synthetic futures strategy, there are two legs: buying a call and selling a put. The total charges, including brokerage for both legs, come to ₹180.31

The key point to notice is that the major difference in charges between futures and synthetic

futures arise mainly due to STT (Securities Transaction Tax).

As you can see, the charges for synthetic futures are significantly lower than traditional futures, offering a substantial saving in transaction costs.

Table: Final Cost & Capital Comparison and Net Savings Analysis

| Metric | Direct Future (₹) | Synthetic Future (₹) | Absolute Saving (₹) | Percentage Saving (%) |

|---|---|---|---|---|

| Total Transactional Charges (Round Trip) | 538.54 | 180.31 | 358 | 66.476% |

Note: The calculations shown here are based on imaginary entry and exit points. They may vary depending on your actual trades.

Margin and Far-Month Options

Margin: The margin requirement for a traditional futures contract is high because it is an outright position. It includes SPAN margin and Exposure margin, which can tie up a significant amount of capital. For a synthetic futures position, comparatively less but almost the same.

Far-month Options: Futures contracts are standardized and have specific expiry dates (near, next, far). If you want to hold a position for a longer duration, you must “roll over” your futures contract, which involves additional costs and slippage. With synthetic futures, you can use far-month options (options with a longer expiry date, like 3 or 6 months out) to create the synthetic position. This allows you to hold the position for an extended period without the hassle and cost of frequent rollovers, which is not possible in the traditional futures market.

Summary of Qualitative Findings

These quantitative benefits are balanced by significant qualitative trade-offs. The synthetic futures strategy introduces layers of complexity and risk not present in a direct futures trade. The primary risks include the potential for early assignment on the short option leg, the need to actively manage a portfolio of option Greeks (Vega, Theta, Gamma) beyond simple direction (Delta), and potentially higher execution costs due to wider cumulative bid-ask spreads across two option legs. The “savings” are therefore not a free lunch but rather a market-driven compensation for taking on and managing these additional complexities.

Synthetic futures are most powerful when a trader wishes to express a view that incorporates factors beyond mere direction. For instance, if a trader is bullish on NIFTY but also expects volatility to decrease, a synthetic long position may be more advantageous than a direct future. Furthermore, it is the ideal tool for creating a futures-like exposure with a customized strike price or a very long-dated expiry that is not available in the standard futures market.

Ultimately, the synthetic future is a powerful tool in the arsenal of an advanced F&O trader. It offers quantifiable benefits in cost and capital, but demands a commensurate level of skill and diligence in risk management.

Thank you for reading! Feel free to share your thoughts or comments below. This is just the beginning of our series, and we look forward to exploring many more opportunities together.