The biggest change in myself is being able to stick to a strategy. Been consistently trading a single strategy the past 4 months. Jan as of now is a complete dry month. Hope, other traders share their experiences too.

My losses rate are higher than winning rate, so I see losses quite too often. Max losing streak size is 9%.

But as they say, you are always one day behind in your losing streak. I am always too cautious.

So, anyone depends on stats like expectancy to keep track of your progress. Share your techniques.

Love this and like this. Couldn’t have put much better. Being a day trader, emotions will always be the biggest demon which will wreck discipline, sabotage plans. Hence, the need for a tight clean risk attitude.

We never know when the drawdown will happen. Even if the God of trading comes, or someone has a 99% win rate, the next trade can be a loser.

Talking about win rate. Win rate is always overrated. And with the law of large numbers, your win rate comes down drastically. Evidently, one can make money with a 40% win rate. You have to know your stats and learn to take bigger wins.

And glad to know, you are on a path of consistency. That’s a tough character and hard to nail.

This is, more often than not, the biggest challenge. Second only to making a good trading strategy.

This is the normal scene in almost all trading strategies. My strike ratio, since last 3 years, is around 43.2%. The average profit to average loss ratio is around 1:2. I guess, this makes up for the low strike rate.

My max drawdown was around 21%. It was from 6 Aug 2020 to 28 Aug 2020 (Literal trading hell. Almost lost confidence in the system. I don’t know what kept me on during those days). Funny part was it recovered in 1 day on 31 Aug 2020. Ended the month with 10.76% gain.

The worst time DD was in May 21. Started from 5 May 21 (Around 13% DD). Saw equity high on 18 Jun 21. Frustrating time, but managed to hold on.

Current DD started on 23 Dec 21. Around 11%. Still 5.6% remaining to be recovered. Again testing patience

Sticking to a working strategy is super important. Good to know that you have been nailing that aspect for last 4 months. This shows that you have fair trust in your strategy which is great.

I used to track regularly the metrics when I started trading. Now its mostly once in a year. Just testing the metrics with live trading against backtester metrics. This is just to figure out how well I have stuck to the plan. Expectancy is important but also is max trade and system drawdown. Trade slippage & cost would be another thing to watch out for especially if the goal is to make small profits like in scalping systems.

Mostly I just focus on the process and let the outcome find me. The trust in the process comes from the objective data of 30 year back test and now 5 year Live trading results as well.

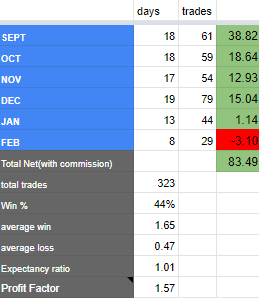

This is my stats for the last 5 months and current. As you can see, net returns starts to dwindle.

How often do you tweak parameters? Has anyone traded a system throughout without changing any parameters? I know if I changed one parameter, say time frame , I am resetting everything.

My biggest challenge here is that win rate for the current system I trade is pretty low. means I see straight loss flushes for days.

Never changed a parameter. If a system is backtested well

with data spanning considerable period of time and across instruments there is no real need to change anything.

I trade with a 47% accurate system and do see loosing streaks. There can also be about 30% drawdown relative to my capital. But I have a trend following system. This is expected behaviour of a trend following system. It doesn’t warrant a change.

As I see 5 out of 6 months you were profitable. That is pretty good. Average win is much higher than avg loss and that should cover for the accuracy part. Better to check the drawdowns though.

There is no picture perfect trading strategy out there. All strategies have tradeoffs. E.g:- I can naked sell a far OTM option and hope to generate consistent income with very high accuracy. But one black swan day could wipe all that gains and land the account in red. If you strategy tradeoffs are workable for you stick with it. If not tweak it to shift the trade offs.

appreciate your response. I am more into forward testing as of now. And talking about backtesting, the only way for me, is to go back to individual charts and go bar by bar, which is pretty slow.

I day trade in fno stocks, and fno stock population have altered much in the past which again creates a wrong data in backtesting.

On the other hand,you have talked about backtesting for enormous amount of time, which is a skill I truly admire. I know less about options, well infact nothing, to generate an edge there.

Infact, I at times, wonder the so called strategy doesn’t seem to make any sense. Have you ever felt that way? Like how do my strategy fits in the market, or is just a temporary illusion.

Anyway, I just keep my risk tight, indeed very tight, and aim for bigger profits.

Note–

I never have trailed my profits. I aim for a 3R profit. And the challenge here, attimes I get more than 2R and got SL thereafter. the only logic is, everything will play out to be fine in the longer run.

I have a simple one SL one target logic. But deep inside, I know, is it being too lazy or do people trail profits and have a bigger benefit in the longer run?

Visual backtesting is a pain and inferences are often misleading. Today we have coded and codeless platforms to backtest. Codeless platforms are pretty simple to do basic testing.

Since I developed the strategy I know it inside out. I know the kind of patterns it will profit from and the kind it will not profit from. 30yrs of backtest and 5 yrs of live trading means there is no questioning it unless I see something drastically different in the market than what I expect.

Stop loss is a double edged sword. It protects but if you keep it too close you get stopped out too soon. It really depends on the strategy how a stop should be - fixed, trail and how far these should be.

Beside everything, keep things as simple as possible which will make it easy to follow.

Backtesting results can be misleading. I myself have been guilty of overfitting for long, but it didnt kill me because I only used them on the top nifty stocks and almost never booked loss (instead chose to wait). But once I got interested in F&O I knew I had work to do - I quickly adapted and learnt.

I spent months backtesting and did it vigorously. Sample size is very important for statistical significance. I now don’t trust any results unless I get around 1000+ trades. I only backtest and run strategies on index (nifty and bank nifty). Curve-fitting is dangerous and its easy to get caught in its illusion. Infact you can curve fit even rubbish strategies to produce good results.

Oh and if you optimize values of 5+ different parameters and have a complicated strategy with hotch potch of values, you are almost guaranteed to produce overfitted models thats unlikely to give similar results ‘out of sample’ and ‘live testing’.

i don’t constrain myself with any rules like - certain % for month or X number of trades a day

what i simply do is, if i feel the probability of happening this is high, then only i trade

I also find the reasons to not take a trade as well

& I don’t like the idea of things like systematic trading, Bots, Algo, beacuse one will eventually move to investing even if they did systematic trading in initial days considering they have substantial fund for it

if the whole idea of systematic trading is to make process so called process then why not consider investing?

Understanding market =/= Prediction

sice the feel of actuall interacting with market comes from direct interaction, which automated strategies lack

Simple things work better. Easier to understand, easier to fix, easier to backtest closer to reality. 5+ parameters is bit of overkill that is unlikely to yield any performance benefits.

As you noted curve fitting does create mirages of earth shattering results. Better to optimize systems to plateaus of profitability rather than peaks of profitability that hangs by the cliff.

thanks for all the responses and inputs. It really was helpful.

I feel pretty disabled when it comes to backtesting. What I am doing as of now is collect the EOD data, filter the FNO stocklist and then apply my parameters. Then I go to the required date, and go chart by chart through 5 min TF. That’s so cumbersome and it takes a whole day to backtest 1 week worth of charts.

My question–

Is there a way to backtest faster?

If I apply my strategy to niftycontract, say, NIFTYFEB22FUT, how do I fetch the past contracts EOD files? I have never traded fut contracts anyway.

Continuous future data is available and so you may not need to go monthwise. If you are working EOD then you should get around 5 yrs data as per streak documentation. If you go for a coding platform like Tradingview you will get significantly more data around 14 yrs. But then you need to code.

Futures contracts have near month, current month and far month contracts at any point of time.

Datafeed providers / stock brokers in order to ease analysis concatenate current month data over different months and create a composite continuous future symbol. We can use it for analysis as if it is a single symbol with price quotes spread over as much into history as supported by the platform we use.

9% is my personal opinion. I am saying 9% yearly returns. It just shows you are pretty consistent and discipline. Current bank interest rates are around 5.5 to 6% . If you look at reality very few people actually make more than bank FD. Even Nithin tweeted out Tweet that only 1% of traders make more than 3 years more than bank FD.

logically if s&p 500 gives averages 10% and trading over a year gives me less or equal to any index fund then why would I waste my time trading , it’s way better off just buying any index fund.

I would probably say that if returns are less , figure out proper risk management & money management and use leverage to increase odds. But that same leverage is what finishes people too. Learn to take calculative risks.

I sort of agree, although trading with decent edge can do a lot better than 9% and with DD much better than index - but its hard work.

Still, one reason for someone with mediocre system to still trade it could be to diversify and reduce dd at portfolio level. So Maybe you make less than index but DD is much better than index. Yes can use leverage to increase returns, depending on how much leverage is available, but someone maybe does not want extra returns and is only looking at risk reduction. Also perhaps this system needs very little effort ( say once a month decision etc) and that could make it worthwhile.