Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- India eases its border investment wall

- In defence, brains are worth more than shells

India eases its border investment wall

Last week, the Union Cabinet approved its first big relaxation to the storied “Press Note 3” of 2020 — the sweeping restrictions India imposed back in April 2020, just as the COVID-19 crisis had hit us, on foreign investment that was coming in from any of our bordering countries.

In practice, Press Note 3 was targeted at a single country: it was India’s China investment wall . It forced any investment with even a trace of Chinese beneficial ownership to seek government approval, no matter its size, sector, or intent. And with our relationship with China soon turning rocky, this is how things remained over the next six years. Until this amendment came in, that is.

Only, immediately after the relaxation, the government had to clarify: this easing was “not meant for Chinese firms.” After all, the media had already rushed out stories on how this marked a thaw between India and China, while politicians painted pictures of India capitulating to external pressure.

Reality was hardly as spicy. This is actually a story about how well-intentioned policies, drawn clumsily, can have consequences their drafters never imagined. You might want to stop opportunists from taking advantage of a temporary weakness, but you could accidentally lock your own economy out of some of the world’s most liquid pools of money, or some of its most advanced technologies.

Press Note 3

Until April 2020, Chinese investors could put their money into India freely, just like American or Japanese ones could. The only investments we scrutinised were those from Pakistan and Bangladesh.

But then, COVID fell upon us. The markets tanked, and they stayed down for more than a month.

It felt like an apocalypse had descended on us. Everyone rushed to withdraw their money. But to some, this looked like a once-in-a-lifetime opportunity.

The problem of Chinese investments

On April 12, 2020, a regulatory disclosure revealed that the People’s Bank of China — China’s central bank — hiked its stake in HDFC from 0.8% to 1.01%.

This felt off. HDFC controlled a sprawling empire: India’s largest private bank, a massive AMC, and an insurance firm. It was a gateway to India’s financial plumbing. Why was China’s central bank putting so much money here, even as the broader market had crashed 40%? Surely, they weren’t just seeking returns. Right now, critical assets were selling at distressed prices, and the Chinese government was on a buying spree.

By all accounts, in fact, China was planning to do more. At that very moment, Chinese state-linked entities were gathering over $600 million to buy stakes in India’s financial services.

China, in fact, had already accumulated a remarkable amount of control over India’s new age businesses. At that very moment, two Chinese companies — Alibaba and Tencent — backed nearly half of India’s 31 unicorns between them. This included massive stakes in some of our biggest start-ups, from PayTM, to Swiggy, to Flipkart. Most of these investments were practically invisible. They had come in from Singapore, Mauritius, and Hong Kong, through shell entities, without the government being in the know.

China had the power to reshape India’s start-up ecosystem on a whim. And we hardly knew how.

And so, within five days of HDFC’s disclosure, Press Note 3 was in place.

The restrictions kick in

To that point, any investments that came from Bangladesh and Pakistan would have to go through the “approval route” — that is, it was only if the government gave its thumbs up to the investment could it enter India. If you were from anywhere else, though, there were many sectors in which you could invest freely.

Press Note 3 expanded that list, rather vaguely, to “countries sharing a land border with India “. Nobody had any doubts on who we were targeting, though. Our focus was clearly not on investments from Nepal and Bhutan. It was squarely on China .

But it wasn’t enough to stop investments from China. Formally, China just had $2.51 billion in Indian investments. In reality, there was almost twice as much coming in every year — only, it was passing through other countries. And so, we introduced a “beneficial ownership” provision. That is, it didn’t matter where an investment itself came from; if it was ultimately for the benefit of someone from a neighboring country, it would be caught in the net.

This made sense. It also had a critical design flaw, however. It didn’t actually specify what a “beneficial owner” was. It didn’t define how far up you would look for one. It didn’t define how much ownership was a problem. Other Indian laws that talked about beneficial ownership clearly did so. Under the Companies Act, for instance, you would only start worrying about “beneficial ownership” once someone indirectly owned more than 10% of an entity.

Press Note 3, on the other hand, specified nothing. If you wanted to read this conservatively, even if a Chinese person owned a negligible number of shares somewhere up the ownership chain of an investor, its investment could get stuck.

Why this became a problem

Press Note 3 was meant to stop opportunistic COVID-era attempts at taking over a major part of our industry for cheap. In practice, though, it applied to every investment.

Was that what we wanted? That isn’t clear. But two months later, Indian and Chinese forces clashed at the Galwan border, and twenty Indian soldiers were killed. The relationships between our two countries hardened instantly.

Galwan ensured that any changes to the Press Note would be politically radioactive for years . The policy calcified.

It did create some difficulty for Indian companies, however. On the ground, it was banks that actually processed incoming investments from abroad. And with such little clarity on what the Press Note was trying to catch, many chose to be as conservative as they could. Different banks applied different thresholds; they demanded different promises from any company receiving an investment. The same transaction would be seen differently, depending on which bank processed them.

As this happened, many investments were routinely held up.

For one, many global PE and VC funds — those run by BlackRock, Carlyle, Sequoia, and the like — typically have Chinese “limited partners”. These were investors that gave their money for the fund to manage; they passively held single digit percentages of these funds, with little control over where the money went. This was clearly money that India wanted. And yet, these investments could get entangled in Press Note 3’s requirements.

Similarly, there were Chinese investments that could have been good for India; bringing in world-class technology. China, after all, was the factory of the world, and Indian manufacturers would benefit from Chinese technical partners, who could give us equipment and know-how. The standard way of doing this was to set up joint ventures, where the Chinese entity would get a stake in exchange for what it brought to the partnership.

Only, these joint ventures came under the Press Note’s scanner, and approvals could drag on endlessly. For instance, when Dixon Technologies tried to set up a smartphone JV with Longcheer, the partnership was only approved only after huge delays, even though Dixon owned three-fourth’s of the partnership. BYD’s billion dollar investment plans into India, similarly, practically died because the necessary approvals weren’t forthcoming.

We needed a middle-ground: even if it was important to take a hard look at Chinese investments, these wanton rejections hurt India itself. The capital and knowledge we needed to become a manufacturing powerhouse had been locked away. According to media reports, of the 526 proposals filed until April 2024, just 124 went through — or less than a quarter. More than 200 were rejected outright, while another 200 were stuck in the system. Decisions typically took six to ten months to come through, and in some cases, remained pending for years.

The new reset

The cabinet’s recent decision, now, tries to ease the load in two distinct ways.

For one, it clarifies what a “beneficial owner” even is: tying it to how the term is seen under money laundering laws. And it cordones off where the scrutiny will go: we would look at the investor entity , instead of an endless chase through every upstream layer.

Having pinned this definition in place, it opens two channels of relief.

An investment into India is safe, as long as someone from a neighbouring country owns less than 10% of the investor, and can’t control it. Then, standard investment laws apply. So, if there is an American VC fund, 6% of the capital of which comes from a Chinese entity, the VC can still put money into India. It wouldn’t have to face the threat of a protracted delay, or outright rejection.

Now, this channel does nothing for investors incorporated in China or Hong Kong. If you’re a fund from a neighbouring country, things are exactly where they were before. It’s simply for anyone that became collateral damage because of a minor Chinese stake.

But there’s another channel of relief.

Let’s say an Indian company genuinely needs Chinese support, and plans to set up a joint venture. The investment will still need approvals, of course. But now, the government is creating a new channel for these applications. As long as the Indian entity controls the joint venture, finally, those approvals will be expedited within 60 days.

For now, this route is limited to just seven sectors: advanced battery components, rare earth processing, electronic components, and the like. These are the spaces where India most needs Chinese equipment and process technology to build domestic manufacturing capacity. We’re trying to find a middle ground here; one where we’re trying to maintain some scrutiny, even as we invite Chinese technical partnerships.

Everything else, though, remains exactly as before.

A necessary compromise

Unlike so many bombastic claims in public, to us, this seems like a sensible compromise.

This removes the blockers on a highly liquid pool of blocked capital — global institutional money that never posed a security concern. It also opens the gates for Chinese technology, across seven sectors where we need it the most. These are, broadly, sensible ideas.

India spent the last five years learning just how blunt simple, broad FDI screening laws are. Capital flows far too easily for one to get one’s policies exactly right. You can either catch too much, as we did in the last five years, or too little, as we did before. The new amendments are a serious attempt to calibrate them better. They try bringing in more capital and technology for India’s businesses, while holding off Chinese strategic interests.

This is a necessary compromise, not a big thaw.

In defence, brains are worth more than shells

We’ve written about India’s defence sector a few times now — the history of how India buys weapons, the evolving procurement framework, the state of the industry as it stands. Those pieces spent a lot of time on the macro picture: rising budgets, geopolitical tensions, the Atmanirbhar Bharat push. All of that still holds true — perhaps more so now, with a war in West Asia, and the resulting global security (dis)order.

But we’re not here to talk about that today.

Instead, we want to zoom into the internal economics of India’s defence industry: where that money actually goes, who captures it, and what kinds of businesses are emerging inside the sector. A recent HDFC Securities thematic report on the sector is a useful starting point to get a sense of the industry-level architecture.

The short version of the story is this: India’s defence industry is gradually becoming a business of sensors, software, integration, and lifetime support economics far more than a business of just building big physical platforms (we’ll get to explaining what it means).

For the longer version, keep reading.

A value shift

When you think of defence manufacturing, the image that comes to mind is probably a factory floor producing fighter jet airframes, warship hulls, or tank chassis.

HAL Helicopter Facility in Tumakuru

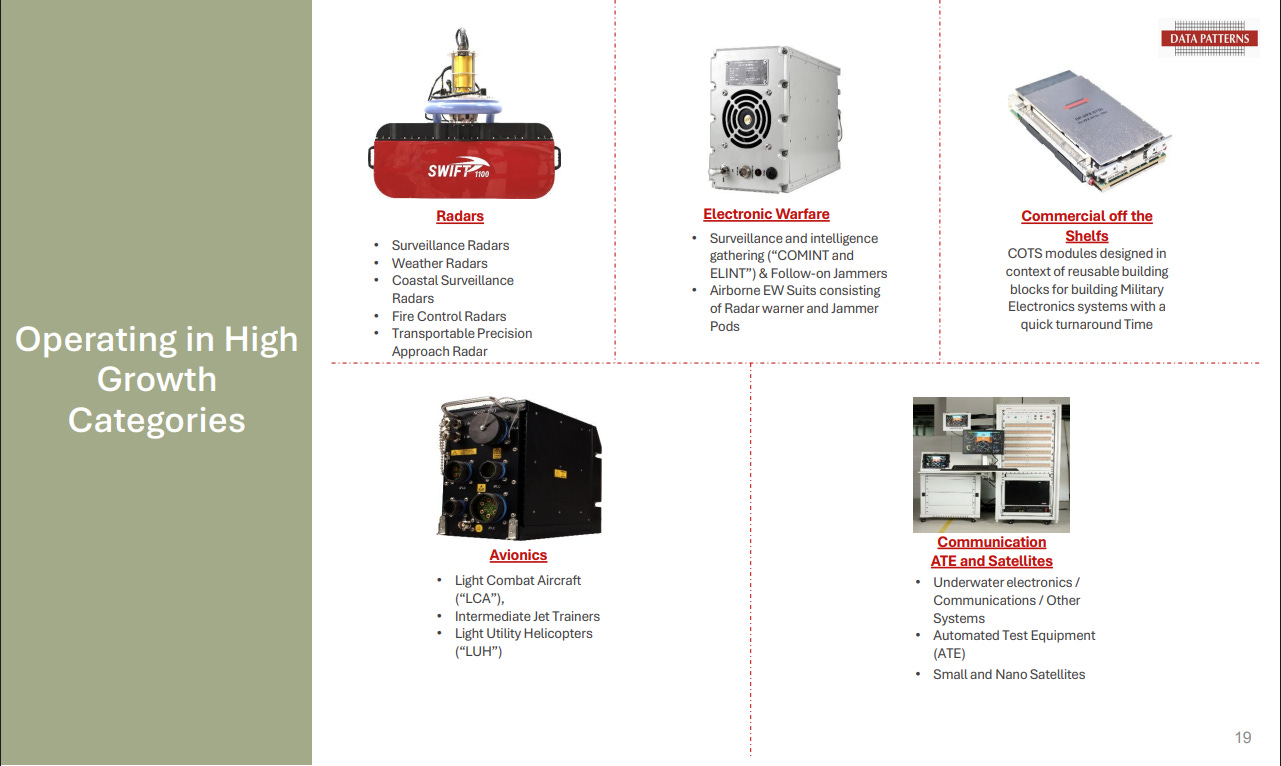

But the most valuable part of modern weapons systems is no longer the metal and machinery. In the defence industry, these systems are often called “platforms ” — which simply means large equipment like fighter jets, warships, or missile batteries.

What really matters now are the electronics inside them — sensors, radars, communication systems, electronic warfare gear, and software. The report estimates these electronics already account for about 40% of a platform’s total value. And that share keeps rising.

This isn’t an India-specific phenomenon. Back in 2006, electronic systems already made up 31% of the cost of the American F-35 fighter jet and that number has only gone up since, while the cost of building the airframe has actually come down. The same pattern is playing out across navies and armies globally: the physical shell is becoming a smaller share of the bill, while the digital brain is becoming a larger one.

In essence, this shifts the centre of gravity in the industry from metal fabricators to firms that own technology, radar design, avionics, electronic warfare capability, and system integration expertise.

It also changes what gets sold and how often . When a platform’s value sits primarily in its physical structure, you sell it once and that’s that — a 30-year asset. But when the value sits in electronics and software, you sell the initial platform, and then keep selling upgrades like software refreshes and radar replacements — every few years, across the platform’s entire 30-year life. The industry starts to look less like traditional heavy manufacturing and more like enterprise software with recurring revenue from an installed base.

The industry is also changing how it builds things.

Traditionally, defence electronics were bespoke, as every program got its components designed from scratch. That’s expensive and slow. Increasingly, companies are shifting to what’s called COTS, or “Commercial Off-The-Shelf” architecture. Here, you build a library of standard, reusable electronic building blocks, and then assemble them in different configurations for different uses — just like Jenga blocks or LEGO bricks.

The R&D is paid for once, and every reuse after that is essentially free engineering. That’s why this approach lets companies bid lower on contracts while actually earning higher margins when the expensive work was already done.

BEL, for instance, does this with its sonar systems. The same modular core can be used for a frigate, a destroyer, or a coastal patrol vessel, all which are different types of ships. Data Patterns, meanwhile, does it with its circuit boards. The same military-grade computer board goes into a missile tester, a bomb guidance checker, and a radar system.

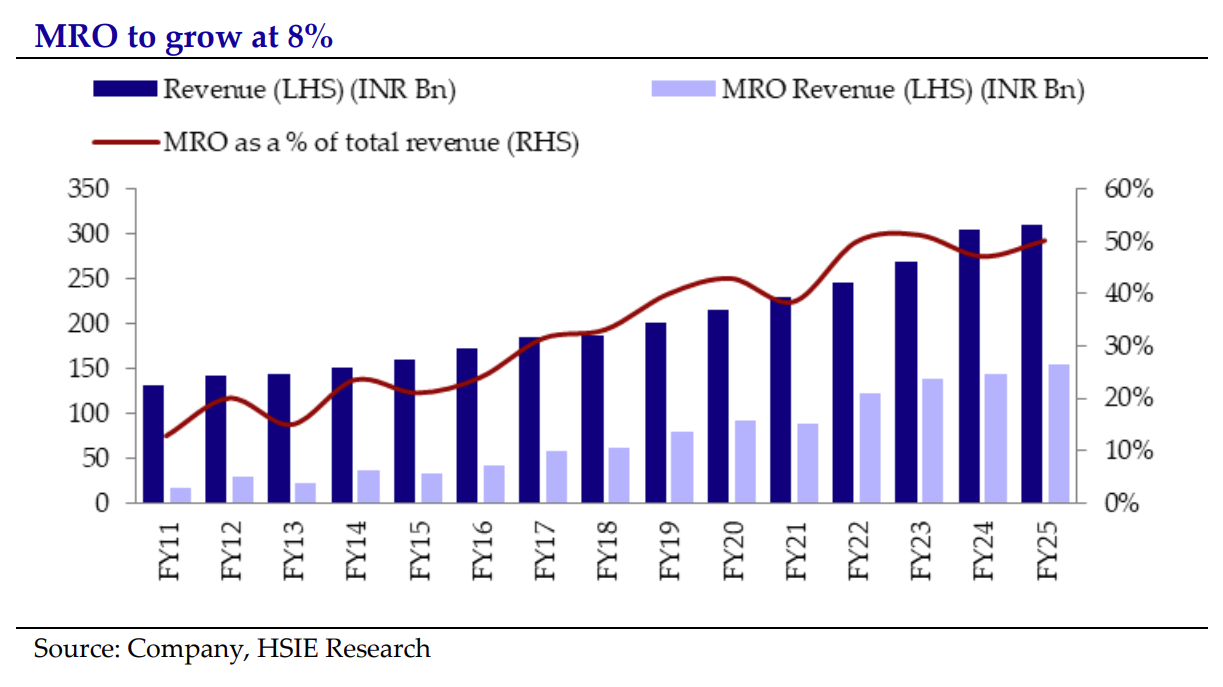

The end-of-life cash cow

If electronics are where the value sits within a platform, the tail-end of the lifecycle of a platform is where the profit sits within the business.

See, the initial sale of a defence platform — delivering a new fighter jet or warship — grabs the headlines. But after that first delivery, the platform needs spares, periodic repair, major overhauls, and eventually a mid-life upgrade where you rip out aging systems and install modern ones.

This “long tail “ of lifecycle services runs for decades, and it carries structurally higher margins than the initial hardware delivery. That’s because it doesn’t require huge capital investment, has more predictable demand, and also creates stickier customer relationships. In some ways, this isn’t all that different from auto ancillaries, where after-sales and service earn higher margins than the core parts themselves.

For instance, when we talk about HAL, you’ll probably imagine a company that makes fighter jets, and of course you should. But, for HAL, repairing, maintaining and supplying spares for those jets have together account for around half of its revenue today.

Upgrading an aging aircraft costs roughly 35% of the price of a brand-new platform. India is currently retrofitting 30-to-40-year-old jets and tanks with advanced radars, glass cockpits, and night-vision fire control systems. That’s steady, high-margin work that doesn’t depend on new orders coming in.

This gives us signals to understand who exactly captures this long-term revenue.

Under the old import-heavy model, Indian companies mostly worked as low-margin assembly hubs for foreign-designed equipment. The more profitable part — spares, software updates, and long maintenance contracts — usually went back to the foreign companies that owned the design.

But now, with the design and intellectual property being developed locally, Indian firms keep much of this revenue for themselves. Owning the design gives you near-exclusive control over decades of support work that follow. However, while real, this localization is still incomplete, as India still is one of the world’s largest arms importers.

The strangest P&L you’ll ever read

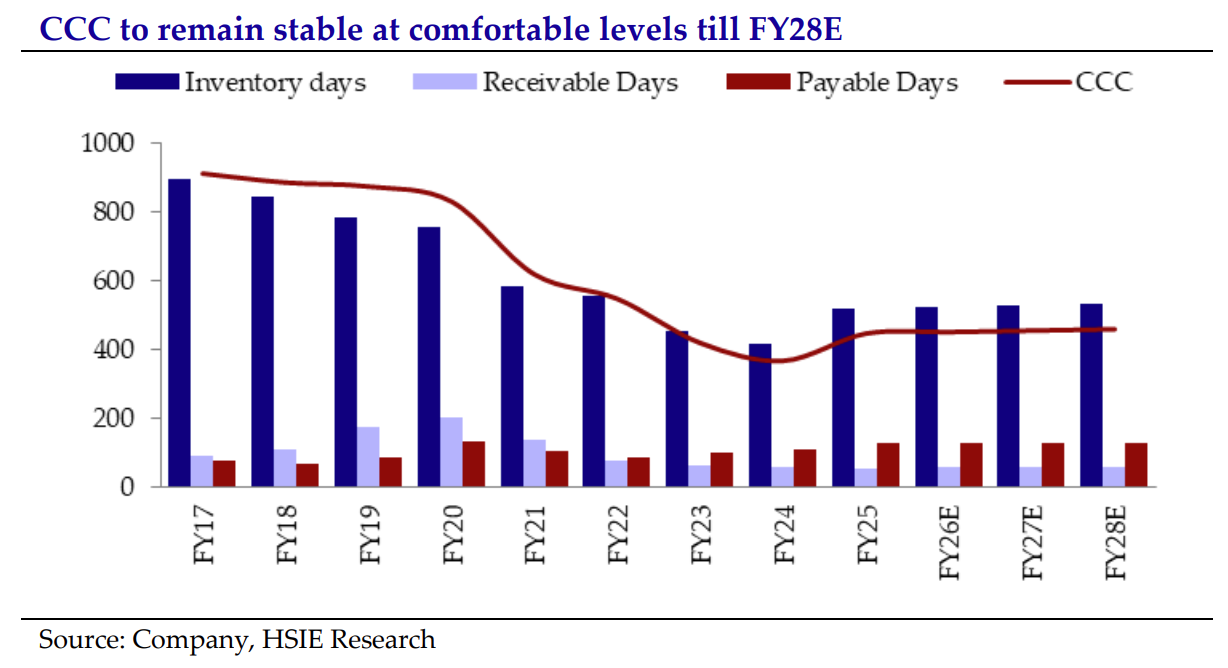

The defence sector is what economists call a monopsony — or a market with essentially one buyer. In India, that’s the Ministry of Defence.

Development cycles are 12-18 months long, sometimes even longer. Then, they’re followed by extensive field trials and certification processes before a single unit can be delivered. All of this traps capital in inventory and work-in-progress for a very long time. The cash conversion cycle — which is the time between spending money on inputs and receiving payment for outputs — commonly runs to 400-600 days in this industry.

On one level, that looks like a devastating cash crunch for defence firms. But interestingly, none of this means defence companies are actually starved for cash.

See, companies negotiate milestone-based payments, receiving massive customer advances when contracts are signed and when development benchmarks are hit — well before the final product is delivered. These advances don’t make the inventory move faster or the trials shorter, and the operational cycle stays brutal. But importantly, they give companies the cash to survive while that long cycle plays out — without needing to borrow. HAL, for instance, had ₹52,219 crore in customer advances as of March 2025, and it is virtually debt-free .

Now, this advance cash is often parked in banks to earn non-business income in the form of interest. For instance, HAL’s “other income” grew from ~7.5% of profit-before-tax (PBT) in FY20 to ~24% in FY25. Their customer advances grew at a 14.5% CAGR, strongly outpacing revenue growth of 7.6%. Meanwhile, for Mazagon Dock Shipbuilders, “other income” at one point constituted 77% of total PBT. Most of their profit was just interest on government money.

If there’s a takeaway here, it’s that two firms with identical operating capability can show very different reported profitability depending on their advance payment structures, interest rates, and cash discipline. On the flip side, when advance growth slows or interest rates fall, profit margins can normalize even if the operating business is doing fine.

Not all defence revenue is equal

India’s defence exports hit a record ₹23,622 crore in FY2024-25 — roughly 34 times the level from a decade ago. That sounds like an unqualified success story. But the headline number hides a crucial distinction about how much value is really captured in exports.

Take Astra Microwave Products, which makes radar and electronic warfare subsystems. Its domestic defence orders — built on in-house developed technology — carry 40-45% gross margins. But its export orders, which are mostly offset and “build-to-print “ work (where you manufacture someone else’s design under licence), carry gross margins of just 8-10%. That’s a nearly five-fold margin gap.

Recognizing this, Astra made a hard turn towards the domestic market, with the share of exports in its order book falling from 59% in FY20 to just 9% in FY25.

Why is the gap so large? Well, intellectual property is ~70% of the cost of a defence product. You only capture the lion’s share of the value if you own the design and architecture. But if you’re assembling someone else’s blueprints, you’re only capturing commoditized margins, because many others can do the same assembly.

This means India’s export growth can be misleading if the composition isn’t examined. If most exports are assembly-for-export, the value capture is thin. Growing exports is only strategically meaningful when you’re exporting your own intellectual property.

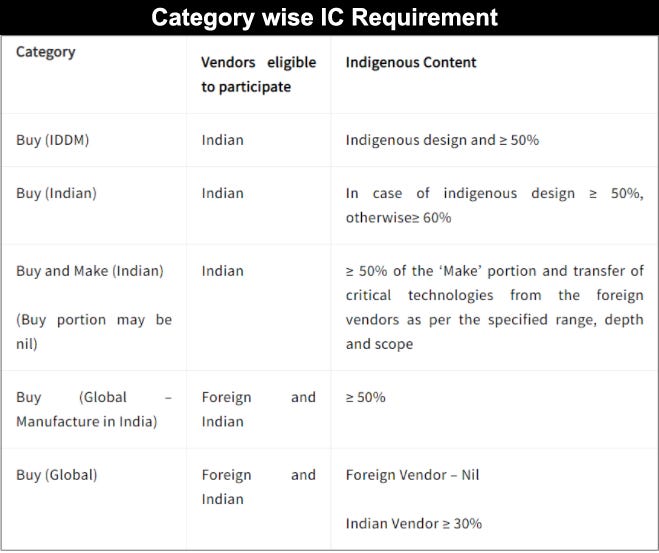

To be fair, India’s procurement framework does try to protect indigenous players. As we’ve covered before, the Defence Acquisition Procedure ranks procurement categories in a strict hierarchy. At the top sits IDDM — products that are indigenously designed, developed, and manufactured in India — where only Indian companies can bid, and at least 50% of the contract value must come from domestic content. Below that is Buy (Indian), where the product is made in India but not necessarily designed here, with a higher 60% domestic content bar. The government is required to exhaust the higher categories before opening up to lower ones.

The problem is what happens after you’re through the gate. Once two companies both cross the 50% IDDM threshold, the lowest bidder wins. A company at 51% indigenous content competes on the same footing as one at 80%. There’s no reward for going deeper. The firm that invested more in indigenous R&D has higher costs to recover; the one that barely cleared the bar doesn’t.

A recent analysis of the draft DAP 2026 flagged a further risk: that companies which purchased foreign design licences could potentially qualify as IDDM, diluting the category altogether. The framework rewards indigenous capability up to a point — but past that point, price takes over.

The bottom line

India’s defence sector is becoming a brain business, not a brawn business. The companies that define the next decade will be the ones that own the electronics, the integration authority, and the lifecycle tail.

But the question worth watching is whether the procurement machinery can keep pace with the industry’s own evolution. If the framework keeps rewarding lowest-cost assembly over indigenous R&D, the economic transformation might be real — but the strategic one could stall.

Tidbits

- India’s retail inflation rose to 3.21% in February 2026, up from 2.74% in January, driven by price hikes in food, personal care and precious metals. Despite the uptick, inflation has now stayed below the RBI’s medium-term target of 4%. However, it will be under strict watch as companies have already begun raising gas prices in the wake of the Israel-Iran conflict.

Source: Reuters - India’s packaged water industry is facing rising costs as the Iran war disrupts global supply chains, and making bottle caps, labels — anything that uses plastics — more expensive Around 2,000 smaller bottled water makers have already hiked prices for resellers by roughly ₹1 per bottle — a 5% increase — with a further 10% rise expected in the coming days, while larger companies are absorbing costs for now.

Source: ET - Over half of Maharashtra’s sugar mills may not operate in the next crushing season, due to a decline in sugarcane availability and mounting financial pressure on mill operators. The FRP (Fair and Remunerative Price) for sugarcane has been raised six times in the past six years, but the MSP for sugar has remained frozen at ₹31/kg since 2019 — squeezing mill margins. To break even on administrative costs, mills need to run for at least 150 days, but most are currently operating for only about 90 days.

Source: The Hindu Business Line

- This edition of the newsletter was written by Pranav and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Subtext by Zerodha

Subtext by ZerodhaWe’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()