Hi, I have been searching for details on Upfront / Trail commission charged for ELSS Funds and also how does it reflect in my account.

Context : I have purchased units in 3 ELSS funds in last financial year and while my broker HDFC Securities confirms that I have not been charged any Commission / Charges for this transaction and this will be the case even after 3 years when I am eligible to sell these units.

My Queries -

Is Entry Load / Exit Load different from Upfront Commission / Trail Commmission

Who actually earns these commissions ? (for e.g. does HDFC Security gets it or the fund e.g. Birla Sunlife '96 Tax Saver Plan)

How does it reflect in my portfolio ? (e.g. is my NAV adjusted down to reflect these charges or its deducted from my initial investment and then units are purchased )

How can I keep track of these expenses on Mutual Funds / ELSS ? I checked the Fact Sheet / Brochure of Birla Sunlife and there is no mention of Upfront / Trail Commission, so how they charge my investment ?

The key benefit of Zerodha Coin is that we’re absolved of these commission, if we invest through Coin. If Upfront / Trail Commission are not charged for ELSS funds, does it then make sense to not purchase through Coin ?

Entry load is no longer applicable on any scheme so I won’t talk about this.

To explain exit load I would take the scenario of a bank FD, when you get the FD created in the Bank, you tell them that you will keep the funds with them for say a period of 2 years, now once the FD is created, the bank expects you to come back to them for the money only after 2 years and so commit to pay you say 8% per annum, but there is also a possibility that you may need this fund in case of an emergency before that, so the banker would let you withdraw it on demand, but will cut some penalty and pay you the principal and an interest. Similarly, in mutual funds, the fund managers collect money expecting that you will stay in the scheme for sometime, if you decide to go ask for your money before that certain period he will charge you the exit load. So this is charged only if you pull out your units before it completes a year or two in case of some funds.

The upfront and trail commision is the commision that a mutual fund distributor earns from the AMC(Asset management company) for getting the business to him. Mutual funds till sometime back used to be sold just like insurance products were sold, not many people wanted to. So when someone, in your case HDFC securities is the distributor, gets the commision as soon as you invest, this is called upfront and, every year, a trail commision.

The upfront and trail commision will not be visible to you upfront, but these are together expressed and included in the expense ratio.

The expense ratio is the cost involved in managing a fund. Now people who invest through a distributor gets the money invested in Regular mutual funds, where the expense ratio is higher and hence the returns will be lower, also the NAV will be lower than if you invested in the same fund using the direct option.

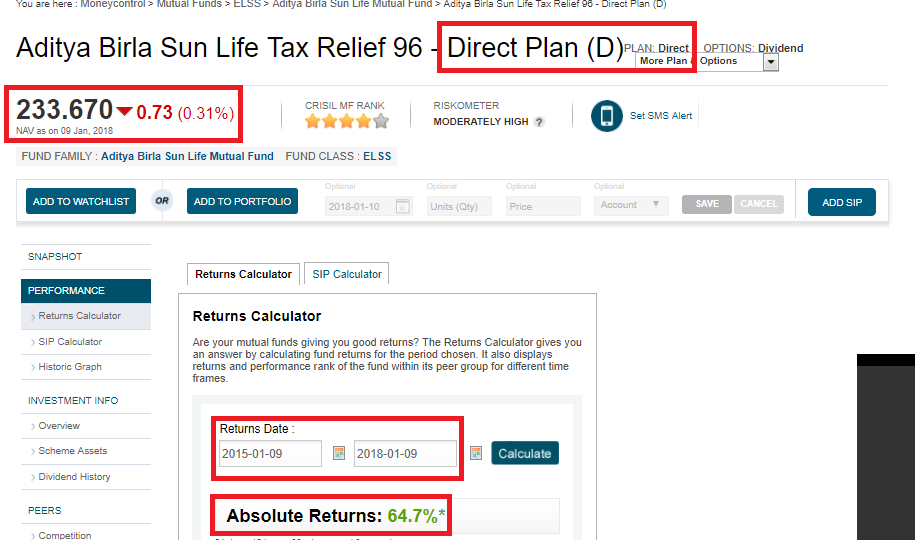

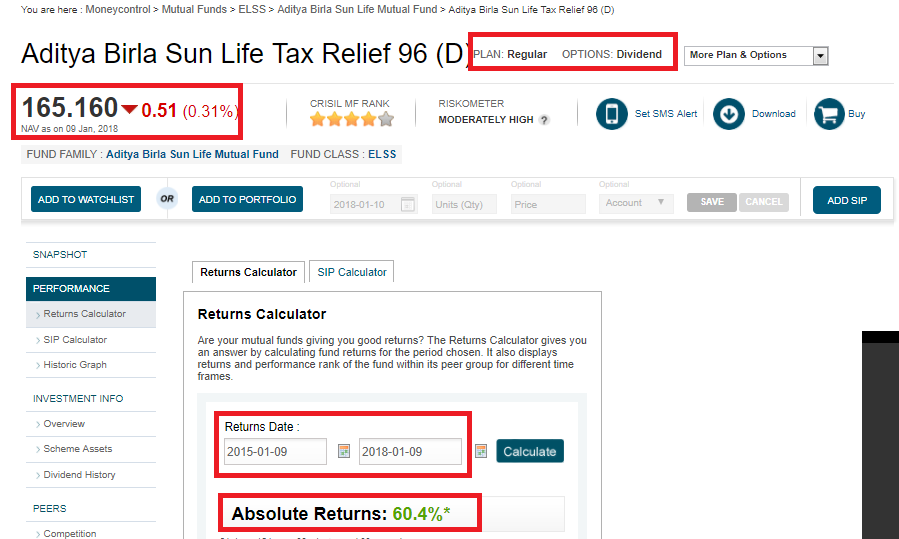

More than 85% of the mutual funds that are sold in India are regular mutual funds because people are not aware of this. Coin from Zerodha is one of the few platforms in India where you can invest on direct mutual funds. As you can see below, in the screenshot you can see the difference in the Expense ratios.

This is the revenue for HDFC securities(Distributor) and adjusted from the NAV. So in the screenshots above you can see the NAV in case of Direct fund is greater as lower deductions are happening before NAV is declared.

-Unfortunately you cannot see this, the way it is formaulated, you will not be able to see this as the adjustment is happening in the NAV declared on a daily basis.

You will have to look at the Expense ratio in the scheme information document that is available on the AMC site.

Thanks you so much for taking time to answer my queries. I appreciate it.

Few follow ups -

I read on some portal (not able to find the link), that ELSS are exempt from Upfront / Trail commission ? Am I mistaken ?

My contract note from HDFC Sec shows no commission and charges to me. The conversion of my Investment in Rs. to the Units is exact as per the NAV at the end of that day. While there is a lock-in of 3 years, but if I could sell the units today, it would fetch me the NAV effective today. So I am still not able to ascertain how these commissions were collected by HDFC. I can only assume that it was adjusted in the the actual NAV. i.e. Expense Ratio is integral part of the NAV.

Or that, once I sell these units it might reflect in the Contract Note.

It was surprising to me when you said that the Expense Ratio is actually earned by Distributor i.e. HDFC Securities. I called a senior person today and she wasn’t aware of these terms of (Upfront / Trail). I was just told that there are no charges at all that levied on the customers for purchasing MF.

Anyways, thanks so much. I think I have got some clarity on this.

what ELSS schemes do not have is entry load and exit load. All mutual funds have expense ratios, this is essentially the expense incurred in managing the funds, this will include the fund manager’s salary, the advertising costs the distribution costs etc.

Now look at it from from distributors angle(HDFC securities) do you think they are letting you invest in mutual funds for free? They have to pay their employees salaries too right so, essentially when these distributors sell mutual funds to you these are regular mutual funds where expense ratio is higher, the other way to invest is in direct mutual funds( this can be done directly through the AMC{asset management company} or through coin.zerodha.com)

Check the screenshots I have attached in my previous answer, I have chosen the Birla 96 tax savings fund. You are currently investing in this I guess, if you notice properly this investment is in regular mutual funds. If you had invested the equal amounts in both the funds 2 years back, to this date, your investment in direct option of the Birla 96 tax saver scheme would have given you a return of 64.7% compared to a return of 60.4% for the case of investment in regular mutual funds( through HDFC securities)

Expense ratio as a whole doesn’t go to the distributor, in case of direct mutual funds (there is no commission paid out, lower expense ratio) in case of regular mutual funds( the distributor has to get a commission for selling the mutual funds, so a part of expense ratio is given to the distributor, hence expense ratio is higher than the direct option of the same fund).

Check out the first screenshot that I have attached of coin. You can see the difference in the expense ratios of the regular plan and the direct plan. Also coin offers you an option to see how much your savings would be if you invested in direct option when compared to the regular option