Hi @dipen01

Entry load is no longer applicable on any scheme so I won’t talk about this.

To explain exit load I would take the scenario of a bank FD, when you get the FD created in the Bank, you tell them that you will keep the funds with them for say a period of 2 years, now once the FD is created, the bank expects you to come back to them for the money only after 2 years and so commit to pay you say 8% per annum, but there is also a possibility that you may need this fund in case of an emergency before that, so the banker would let you withdraw it on demand, but will cut some penalty and pay you the principal and an interest. Similarly, in mutual funds, the fund managers collect money expecting that you will stay in the scheme for sometime, if you decide to go ask for your money before that certain period he will charge you the exit load. So this is charged only if you pull out your units before it completes a year or two in case of some funds.

The upfront and trail commision is the commision that a mutual fund distributor earns from the AMC(Asset management company) for getting the business to him. Mutual funds till sometime back used to be sold just like insurance products were sold, not many people wanted to. So when someone, in your case HDFC securities is the distributor, gets the commision as soon as you invest, this is called upfront and, every year, a trail commision.

The upfront and trail commision will not be visible to you upfront, but these are together expressed and included in the expense ratio.

The expense ratio is the cost involved in managing a fund. Now people who invest through a distributor gets the money invested in Regular mutual funds, where the expense ratio is higher and hence the returns will be lower, also the NAV will be lower than if you invested in the same fund using the direct option.

More than 85% of the mutual funds that are sold in India are regular mutual funds because people are not aware of this.

Coin from Zerodha is one of the few platforms in India where you can invest on direct mutual funds. As you can see below, in the screenshot you can see the difference in the Expense ratios.

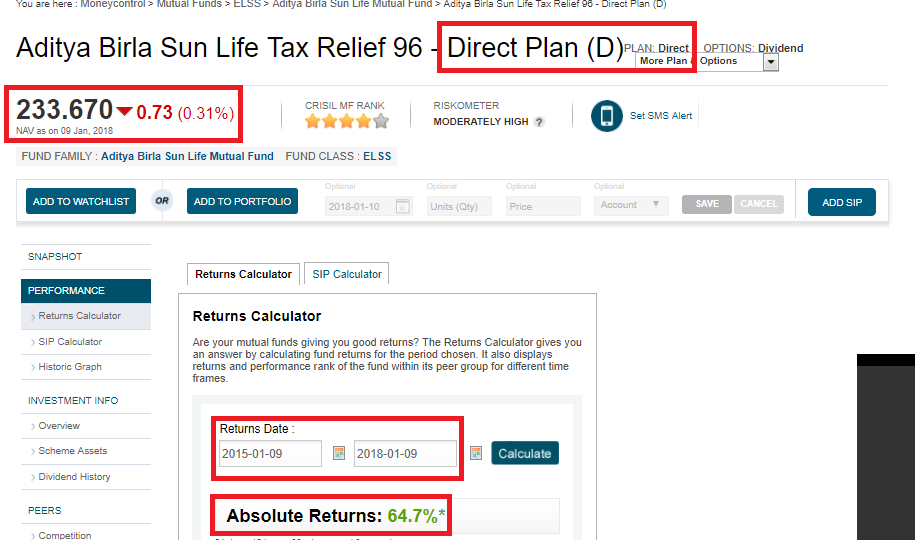

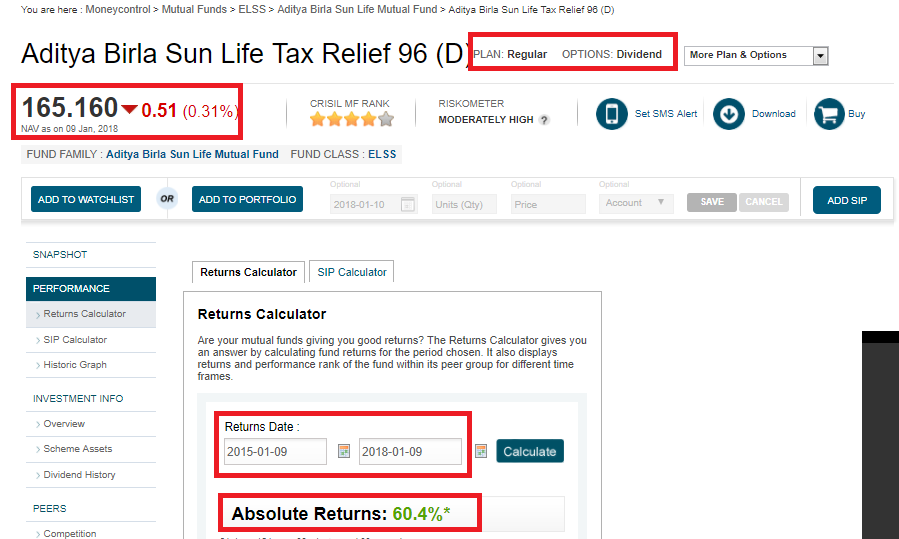

An comparison of direct and regular mutual funds, using moneycontrol.com

Direct:

Regular:

This is the revenue for HDFC securities(Distributor) and adjusted from the NAV. So in the screenshots above you can see the NAV in case of Direct fund is greater as lower deductions are happening before NAV is declared.

-Unfortunately you cannot see this, the way it is formaulated, you will not be able to see this as the adjustment is happening in the NAV declared on a daily basis.

- You will have to look at the Expense ratio in the scheme information document that is available on the AMC site.

- Since I have told that the expense ratio and exit load is as different as chalk and cheese, you have the benefit of your returns being more when you invest in direct mutual funds when compared to investing in regular mutual funds.

The following is an interesting read:

Benefit in coin zerodha? If I get more units investing in regular MF, why should I invest direct?

cheers,

Lindo