What is it?

What is it?

The Trump Child Savings Account—part of the proposed “One Big, Beautiful Bill”—is a tax-deferred investment account for newborns designed to build early-life financial assets via stock market exposure.

Who is eligible?

-

Children born between Jan 1, 2025 and Dec 31, 2028

-

Must be U.S. citizens

-

At least one parent/guardian must have a work-eligible Social Security Number

-

Each eligible child receives one account only

How much will the government contribute?

-

A one-time $1,000 seed will be automatically deposited by the Treasury

-

This applies only to eligible newborns in the 2025–2028 window

How do contributions work?

-

Families can make after-tax contributions up to $5,000 per year per child

-

Contributions grow tax-deferred and are invested in a U.S. stock index fund

-

Government/corporate matching is allowed and does not count toward the $5,000 cap

When can funds be accessed?

-

No access before age 18

-

At age 18: Withdraw up to 50% for qualified uses (education, business, first home)

-

At age 25: Withdraw 100% for qualified uses

-

At age 30: Withdraw for any purpose; account must be closed

What are qualified uses?

-

Post-secondary education or training

-

First-time home purchase

-

Starting a small business or family farm

What about taxes?

-

No taxes while money grows

-

Withdrawals for qualified purposes taxed at long-term capital gains rate

-

Non-qualified uses before age 30 taxed at ordinary income rates, may face penalties

Can the account be transferred to another child?

No. The account is permanently tied to the named child. It cannot be reassigned or reused.

Who controls the account?

-

Parents/guardians act as custodians until the child turns 18

-

After that, the child gains phased control

How much will the Trump savings program cost taxpayers?

The program’s $1,000 government-funded seed contribution for each eligible child is projected to cost approximately $3.6 billion, based on 3.6 million U.S. births in 2023 (data from the National Center for Health Statistics).

However, former President Trump claims the initiative will have “absolutely no cost” to taxpayers, stating that the funds will be sourced from other provisions within the “Big Beautiful Bill”—notably a proposed 3.5% tax on remittances sent abroad.

How much could the $1,000 grow over time?

If invested in a broad market index like the SPDR S&P 500 ETF (SPY):

-

A $1,000 investment made 18 years ago (as of June 9, 2007) would have grown to $5,590, assuming reinvested dividends.

-

The same investment made 31 years ago would be worth approximately $22,770 today.

These figures illustrate the power of long-term compounding in equity markets—something the Trump account aims to harness by investing from birth.

Some financial experts have expressed skepticism about the Trump savings program, noting that its benefits may be limited when compared to more established, tax-advantaged options like 529 college savings plans. Here’s a comparison of key features between the two:

Quick Comparison: Trump Account vs 529 Plan

Quick Comparison: Trump Account vs 529 Plan

| Feature | Trump Child Savings Account | 529 Education Savings Plan |

|---|---|---|

| Purpose | Broader: Education, home, business | Primarily education |

| Government Seed | $1,000 (one-time for 2025–2028 births) | None |

| Annual Contribution Limit | $5,000/year (after-tax) | No federal limit; state caps ~$300k–$500k+ |

| Tax Benefit | Tax-deferred; gains taxed at withdrawal | Tax-free growth and withdrawals for education |

| Qualified Uses | Education, first home, small business | Education (K–12, college, loans, apprenticeships) |

| Control | Custodial till 18; child-owned thereafter | Parent-owned; flexible beneficiary change |

| Aid Impact (FAFSA) | Likely treated as student asset (less aid) | Parent asset (minimal aid impact) |

| Access Timing | 18+ (partial), 25+ (full for qualified), 30+ (any) | Any time for education |

| Transfer to Others? |

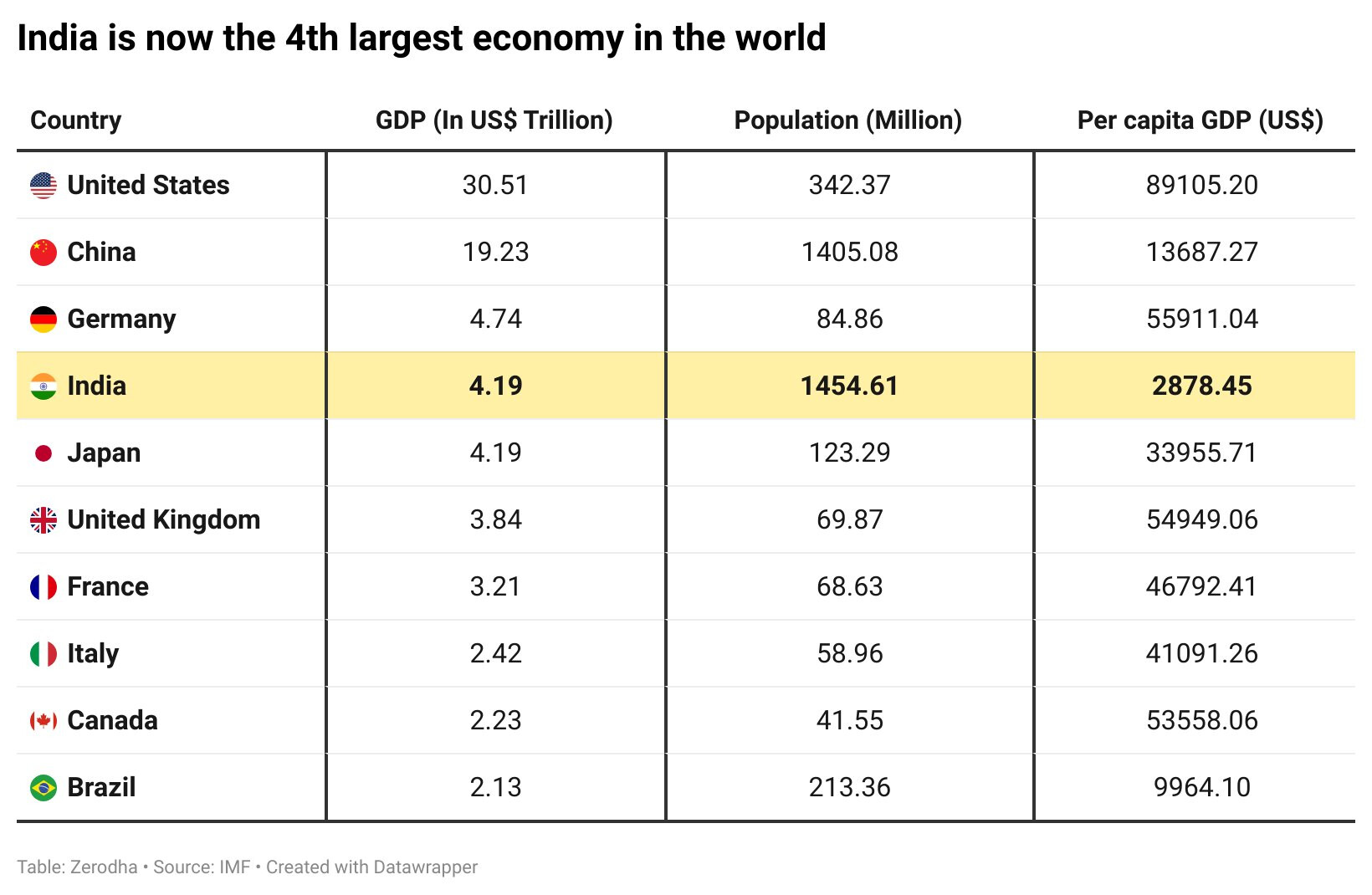

Do we have something similar in India? This looks like nice thing to do for kids future