People usually diversify their portfolio or allocate their capital to different asset classes. One of the subscriber from our telegram channel asked us, if there is a way to reduce his risk exposure to mutual funds without using hedging techniques.

But so far, people haven’t tried a quantitative approach to reduce the risk with mutual fund investments.

We have tried various parameters with quantitative techniques, ran many complex simulations to come up with a risk management model. None of them worked, later I figured that a simple parameter can reduce the risk considerably.

Its what we call it as MA10,which is nothing but a 10 month moving average. 10 Month moving average is almost equal to 200 days moving average, but why not 200 day MA? Why should we use 10 month MA?

Because, the daily moving average contains so much of noise due to daily fluctuations that we see in the market, using 10 month moving average will remove these noise.

Let’s see how it can help us in reducing the risk.

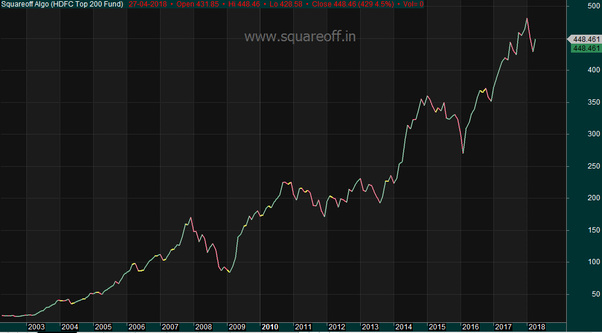

The above chart shows the chart of NAV of HDFC TOP 200 fund since inception.

Rs. 1 lakh Invested in 2002 at the time of inception has grown to Rs.25.9 lakhs by 2018.

That’s a CAGR of about 22.5%.

Sound great! What about the risk involved? Remember the period 2008? When market collapsed, 50% of your capital would have wiped out, whatever you gained prior to that would have been lost in the financial crisis?

How many investors can tolerate such downside fluctuation?

We tried implementing the MA10 rule.

Whenever NAV of a mutual fund goes below 10 month moving average, just exit from it. Re invest again in it,only when the NAV goes above 10 month moving average.

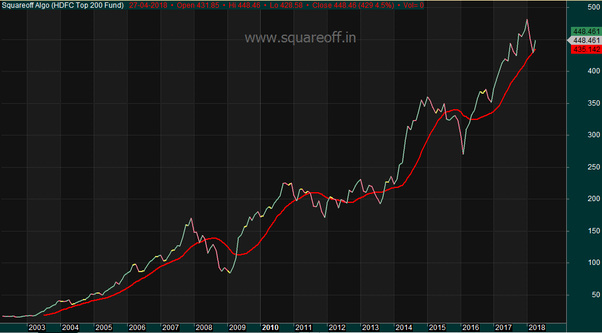

The above chart shows the NAV of HDFC TOP 200 fund. The red line is the 10 month moving average value plotted.

Rs. 1 lakh Invested in 2002 at the time of inception has grown to Rs.20 lakhs by 2018.

That’s a CAGR of about 20.5%.

Our CAGR dropped by 2%, how about the risk?

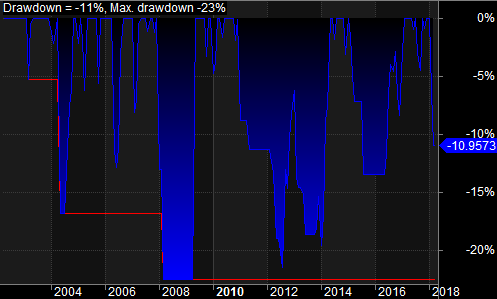

Risk reduced drastically.

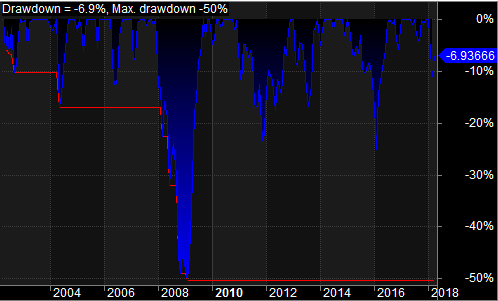

As you can see, the maximum drawdown was just 20% in 2008, when the whole world markets were crashing more than -55% in that year, your investments would have been down only by -20%.

During the other years, the average downside was just -5%.

We are able to reduce the risk in mutual fund investments by more than 60% by simply implementing a moving average with NAV of a fund.

Simple but very effective! try it out.