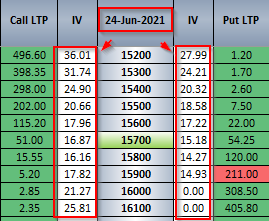

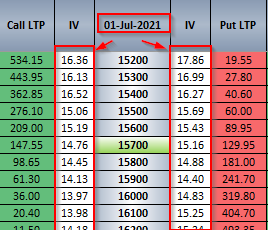

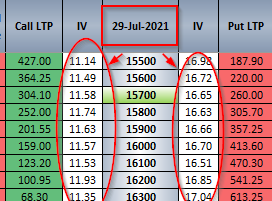

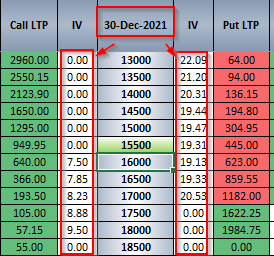

Three Questions:

-

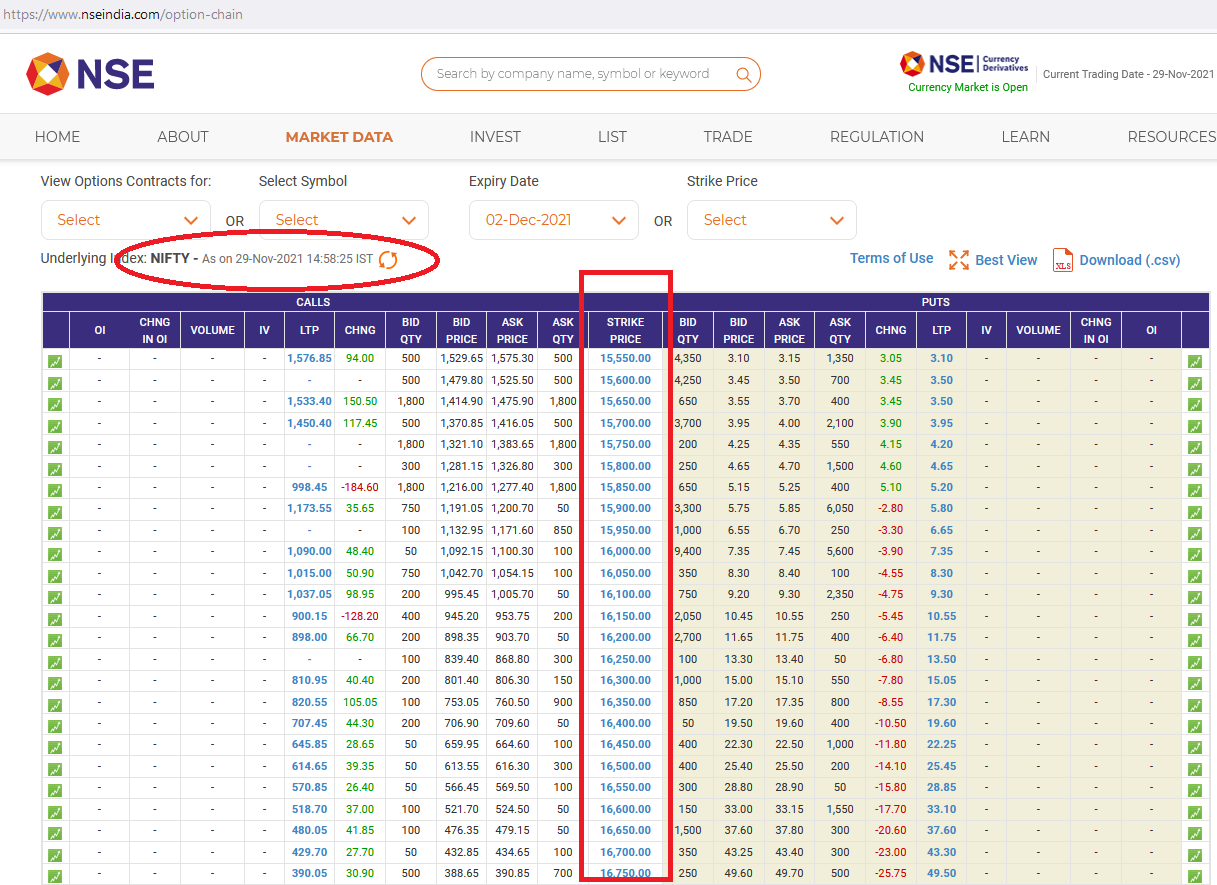

Why Call IV is increasing and becoming almost equal to put IV when contracts are near to expire?

-

For far Expiry contracts, Why IV of put contract are almost 1.5/2/2.5 times call contract’s IV?

-

Put contracts of near expiry and put contracts of far expiry has almost same IV. Then why Call contract of near expiry and call contract of far expiry doesn’t have similar pattern.?