The Berkshire Hathaway 2021 letter by Warren Buffett just came out, and it’s mandatory reading. A few highlights from the letter

On what you own

Whatever our form of ownership, our goal is to have meaningful investments in businesses with both durable economic advantages and a first-class CEO. Please note particularly that we own stocks based upon our expectations about their long-term business performance and not because we view them as vehicles for timely market moves. That point is crucial: Charlie and I are not stock-pickers; we are business-pickers.

Berkshire as an infra business

Many people perceive Berkshire as a large and somewhat strange collection of financial assets. In truth, Berkshire owns and operates more U.S.-based “infrastructure” assets – classified on our balance sheet as property, plant and equipment – than are owned and operated by any other American corporation. That supremacy has never been our goal. It has, however, become a fact.

At yearend, those domestic infrastructure assets were carried on Berkshire’s balance sheet at $158 billion. That number increased last year and will continue to increase. Berkshire always will be building.

Reasonable compounding

Berkshire, these shareholders would sometimes acknowledge, might be far from the best selection they could have made. But they would add that Berkshire would rank high among those with which they would be most comfortable. And people who are comfortable with their investments will, on average, achieve better results than those who are motivated by ever-changing headlines, chatter and promises.

On float

From an $8.6 million purchase of National Indemnity in 1967, Berkshire has become the world leader in insurance “float” – money we hold and can invest but that does not belong to us. Including a relatively small sum derived from life insurance, Berkshire’s total float has grown from $19 million when we entered the insurance business to $147 billion

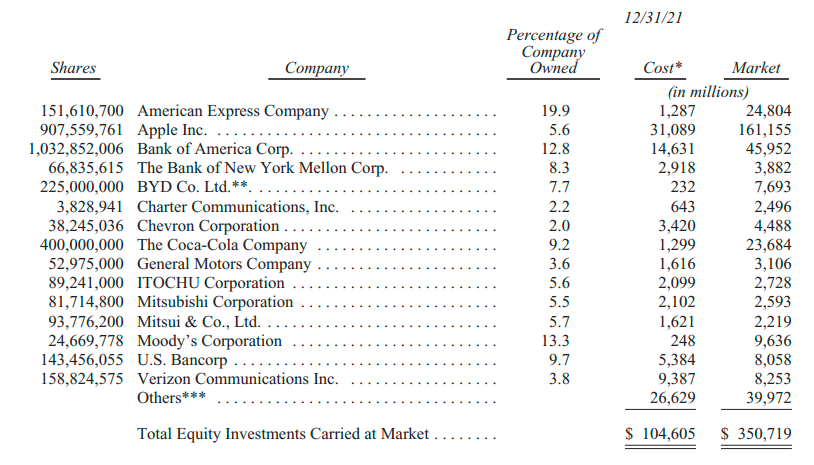

Apple – our runner-up Giant as measured by its yearend market value – is a different sort of holding. Here, our ownership is a mere 5.55%, up from 5.39% a year earlier. That increase sounds like small potatoes. But consider that each 0.1% of Apple’s 2021 earnings amounted to $100 million. We spent no Berkshire funds to gain our accretion. Apple’s repurchases did the job.

Berkshire’s financial holdings

15 of the largest stocks picked by Todd Combs and Ted Weschler

Charlie and I have pledged that Berkshire (along with our subsidiaries other than BNSF and BHE) will always hold more than $30 billion of cash and equivalents. We want your company to be financially impregnable and never dependent on the kindness of strangers (or even that of friends). Both of us like to sleep soundly, and we want our creditors, insurance claimants and you to do so as wel

On Berkshire’s huge cash position

But $144 billion?

That imposing sum, I assure you, is not some deranged expression of patriotism. Nor have Charlie and I lost our overwhelming preference for business ownership. Indeed, I first manifested my enthusiasm for that 80 years ago, on March 11, 1942, when I purchased three shares of Cities Services preferred stock. Their cost was $114.75 and required all of my savings. (The Dow Jones Industrial Average that day closed at 99, a fact that should scream to you: Never bet against America.)

After my initial plunge, I always kept at least 80% of my net worth in equities. My favored status throughout that period was 100% – and still is. Berkshire’s current 80%-or-so position in businesses is a consequence of my failure to find entire companies or small portions thereof (that is, marketable stocks) which meet our criteria for longterm holding.

Charlie and I have endured similar cash-heavy positions from time to time in the past. These periods are never pleasant; they are also never permanent. And, fortunately, we have had a mildly attractive alternative during 2020 and 2021 for deploying capital. Read on.

On creating value

Our second choice is to buy non-controlling part-interests in the many good or great businesses that are publicly traded. From time to time, such possibilities are both numerous and blatantly attractive. Today, though, we find little that excites us.

That’s largely because of a truism: Long-term interest rates that are low push the prices of all productive investments upward, whether these are stocks, apartments, farms, oil wells, whatever. Other factors influence valuations as well, but interest rates will always be important.

On teaching

Teaching, like writing, has helped me develop and clarify my own thoughts. Charlie calls this phenomenon the orangutan effect: If you sit down with an orangutan and carefully explain to it one of your cherished ideas, you may leave behind a puzzled primate, but will yourself exit thinking more clearly

On doing what you love and working with good people

Talking to university students is far superior. I have urged that they seek employment in (1) the field and (2) with the kind of people they would select, if they had no need for money. Economic realities, I acknowledge, may interfere with that kind of search. Even so, I urge the students never to give up the quest, for when they find that sort of job, they will no longer be “working.”

Finally, at Berkshire, we found what we love to do. With very few exceptions, we have now “worked” for many decades with people whom we like and trust. It’s a joy in life to join with managers such as Paul Andrews or the Berkshire families I told you about last year. In our home office, we employ decent and talented people – no jerks. Turnover averages, perhaps, one person per year

Fiduciaries

I wish more financial services business thought like this

I would like, however, to emphasize a further item that turns our jobs into fun and satisfaction - - - - working for you. There is nothing more rewarding to Charlie and me than enjoying the trust of individual long-term shareholders who, for many decades, have joined us with the expectation that we would be a reliable custodian of their funds.