Welcome to another edition of Weekly Market Metrics. I am Sandeep Rao. We’re in Week 10 of 2026, and it’s only March — but it already feels like May. The heat is rising, both in terms of weather and markets.

NIFTY is now down nearly 7% from its all-time high, and even traditionally defensive pockets like gold aren’t offering much comfort this week. There’s nowhere to hide. What’s also striking is that despite rising geopolitical tensions in West Asia — so close to our own subcontinent — markets appear relatively calm. In fact, markets reacted far more sharply to tariff news earlier this year than to this war-related uncertainty. Make of that what you will.

Let’s get into the charts.

NIFTY

Weekly

NIFTY gapped down on Monday, and the gap between last week’s low and this week’s high remained unfilled throughout. The index lost 728 points (–2.89%) to close at 24,450 . The weekly range expanded to 684 points (2.81%) — the highest since the eventful first week of February, which saw the Budget and the India–US trade deal announcement.

Resistance lies in the gap zone between 25,000 and 25,150 , and above that at 25,900 . Support sits at this week’s low of 24,300 , followed by 23,900 . The bias for next week remains negative to sideways, with the possibility of sharp pullbacks — but structurally, this continues to look like a sell-on-rise market.

Daily

All four trading days this week saw moves of 1.15% or more on a close-to-close basis — three red, one green. The intraday ranges were even larger. Monday and Wednesday opened with gap-downs; Thursday saw a gap-up that was entirely reversed on Friday — textbook downtrend behavior. Contra-long bets in this environment can be costly; staying with the trend remains the safer approach.

Support is placed at the 24,350–24,300 zone, followed by 23,935 . Resistance lies in the 25,000–25,150 gap zone, then at 25,500 and 25,900 .

Hourly

NIFTY spent the entire week below the 50 EMA. Short-term trend-following setups are beginning to offer some MTM gains — the question, as always in trending-but-volatile conditions, is how much of those gains can be realized. The 50 EMA currently sits at 24,900 , above which the short-term bias would turn bullish.

Range Till Expiry (10-Mar, Tuesday)

Moving to NIFTY’s expected range till the upcoming weekly expiry on 10-Mar, Tuesday.

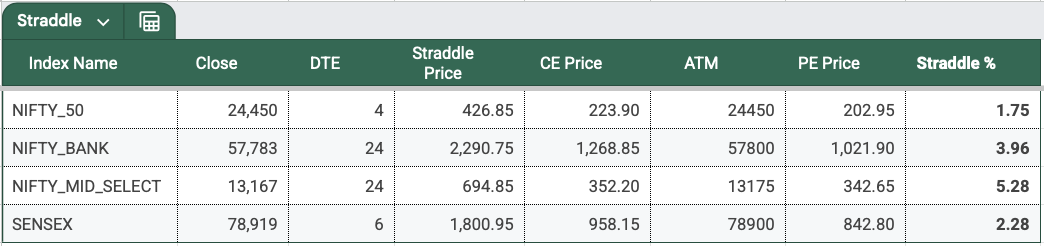

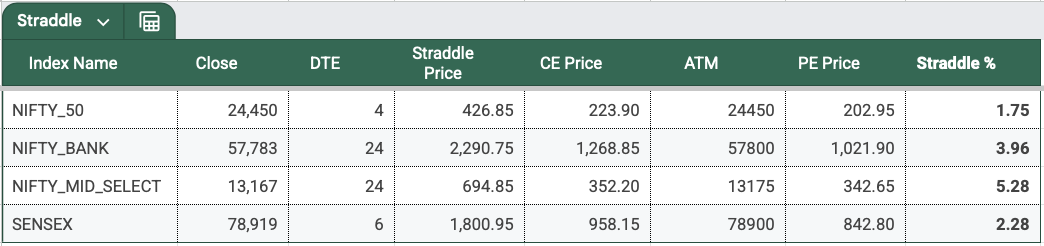

NIFTY’s 1DTE ATM straddle premium closed at 427 points — a hefty premium, partly reflecting weekend risk. The straddle is implying a 1.75% move on either side.

Expected expiry range: 24,877 on the upside | 24,023 on the downside — broadly, a 24,000–24,900 band.

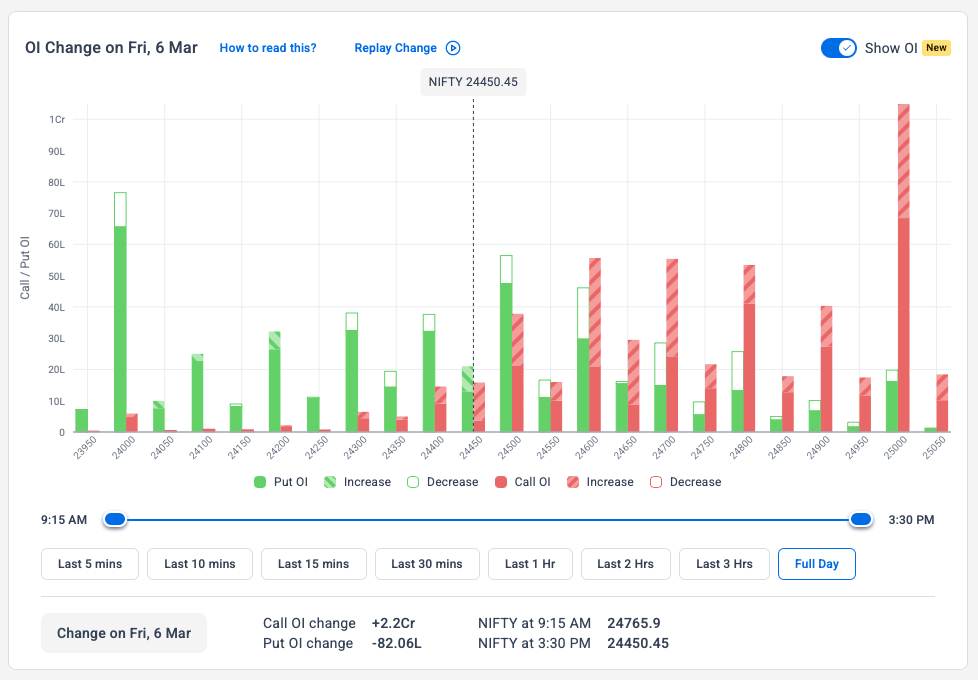

Open Interest

The only notable OI build-up is at the 25,000 CE and 24,000 PE strikes. Some PE strikes are being unwound. Given how wildly the market is moving, OI-based signals are less reliable this week than usual.

SENSEX

Weekly

SENSEX printed an inverted hammer candle this week — generally considered a bullish reversal signal, though confirmation requires a follow-through candle. The index lost 2,368 points (–2.91%) to close at 78,919 , with a weekly range of 2,189 points (~2.8%).

Nearest support is at 78,500 , followed by the 76,400–75,400 zone. Resistance lies in the 80,600–81,150 gap zone. The bias remains bearish to sideways, though the candlestick pattern leaves some room open for a potential reversal.

Daily

Support levels are at 78,500 and 76,400 . Resistance sits at the gap zone of 80,632–81,159 .

Range Till Expiry (12-Mar, Thursday)

The next SENSEX weekly expiry is on 12-Feb, Thursday.

ATM straddle closed at 1,801 points , implying a 2.28% move on either side — 75%, or 755 points, higher than last week’s premium.

Expected expiry range: 80,720 on the upside | 77,118 on the downside — broadly 77,100–80,700 .

BANKNIFTY

Daily

BANKNIFTY lost 2,746 points (–4.54%) for the week — its largest weekly fall since December 2024, ending a run of relative outperformance. The index is sitting right at a critical support of 57,783 ; below that, the next support is around 57,000 . Resistance lies in the 60,177–60,439 zone. Weekly range: 2,481 points (4.12%) — more than double the previous week.

Hourly

Unlike the prior weeks, BANKNIFTY offered a cleaner short-side trend for most of the week, giving short-term trend followers a more readable setup. That said, high volatility is not easy to handle in real time. In hindsight, holding a short below the EMA looks straightforward — in practice, it isn’t. Proper position sizing remains the only sustainable way to survive a volatile trend and stay in the game long-term.

Rate of Change (ROC) — Weekly Snapshot

Week 10 was deep red across the board. NIFTY fell 2.89% , BANKNIFTY 4.54% , MIDCPNIFTY 2.41% , and SENSEX 2.91% . BANKNIFTY, which had been the relative bright spot in prior weeks, was the biggest loser this week.

Year-to-date: NIFTY –6.43% , BANKNIFTY –3.02% , MIDCPNIFTY –4.43% , SENSEX –7.39% . After red Januaries and Februaries, March is shaping up similarly.

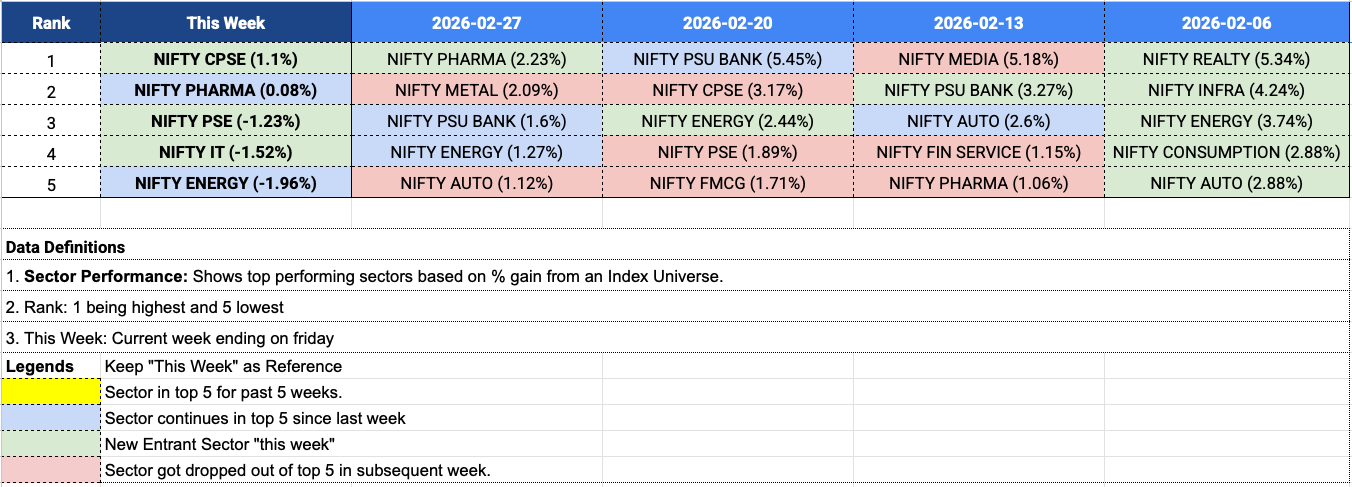

Sectors

NIFTY CPSE was the lone standout with a +1.10% gain. PHARMA followed with a near-flat +0.08% . Every other sector ended negative — PSE (–1.23%), IT (–1.52%), and ENERGY (–1.96%) rounded out the top five. Broad-based weakness was the defining theme of the week.

Ranges & Expiries

NIFTY’s average daily range rose from 242 points last week to 325 points this week — the highest in four weeks. All four trading sessions saw 1%+ intraday ranges, with Monday (1.56%) and Thursday (1.32%) leading. Friday once again delivered a wide range, continuing a pattern seen across recent weeks. Range expansion was not limited to NIFTY — all major indices saw it.

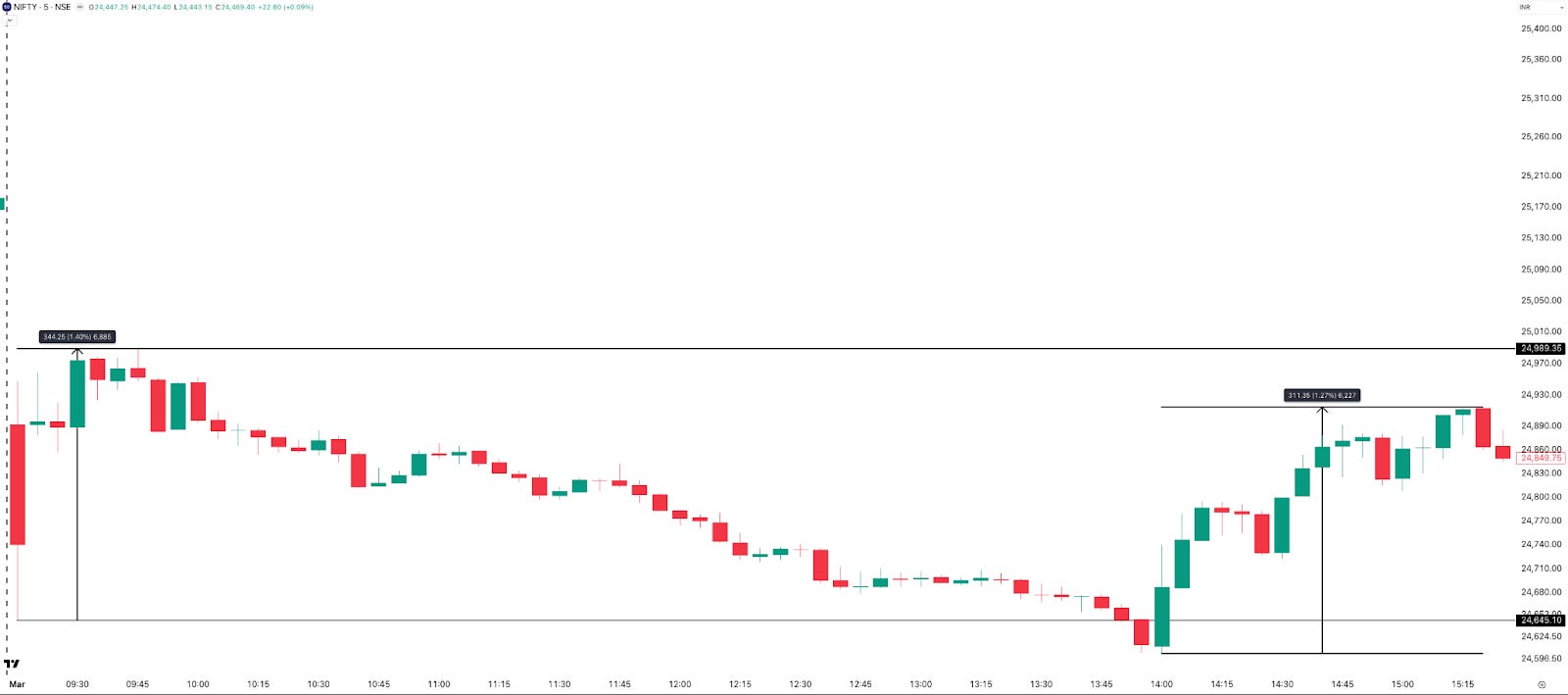

NIFTY First Weekly Expiry of March (2-Mar, Monday)

After a 313-point (1.25%) gap-down open, NIFTY made a 345-point range in the first 15 minutes and held within that range until 2 PM. Post 2 PM, it rallied 311 points (1.27%). The ATM straddle opened at 243 and dropped to 185 within the first 15 minutes — a 58-point crush in a quarter-hour. A strong day for option writers who could manage the volatility; whether option buyers profited would have depended entirely on catching the post-2 PM direction.

SENSEX Weekly Expiry (5-Mar, Thursday)

This expiry was derailed by a media incident. After opening with a 0.5% gap-up and holding within a contained range through early afternoon, false reports began circulating about Iran agreeing to a conditional ceasefire offer. In reality, it was an old statement being recirculated as breaking news. SENSEX rallied 1,100+ points in under 30 minutes, then crashed 500+ points when media houses ran corrections.

Many traders would have been caught in that whipsaw. Losses are an inherent part of trading, but it’s deeply frustrating when they stem from irresponsible reporting — and this is far from the first time this has happened. Self-regulation by media houses clearly isn’t working; stricter accountability frameworks are overdue.

INDIAVIX

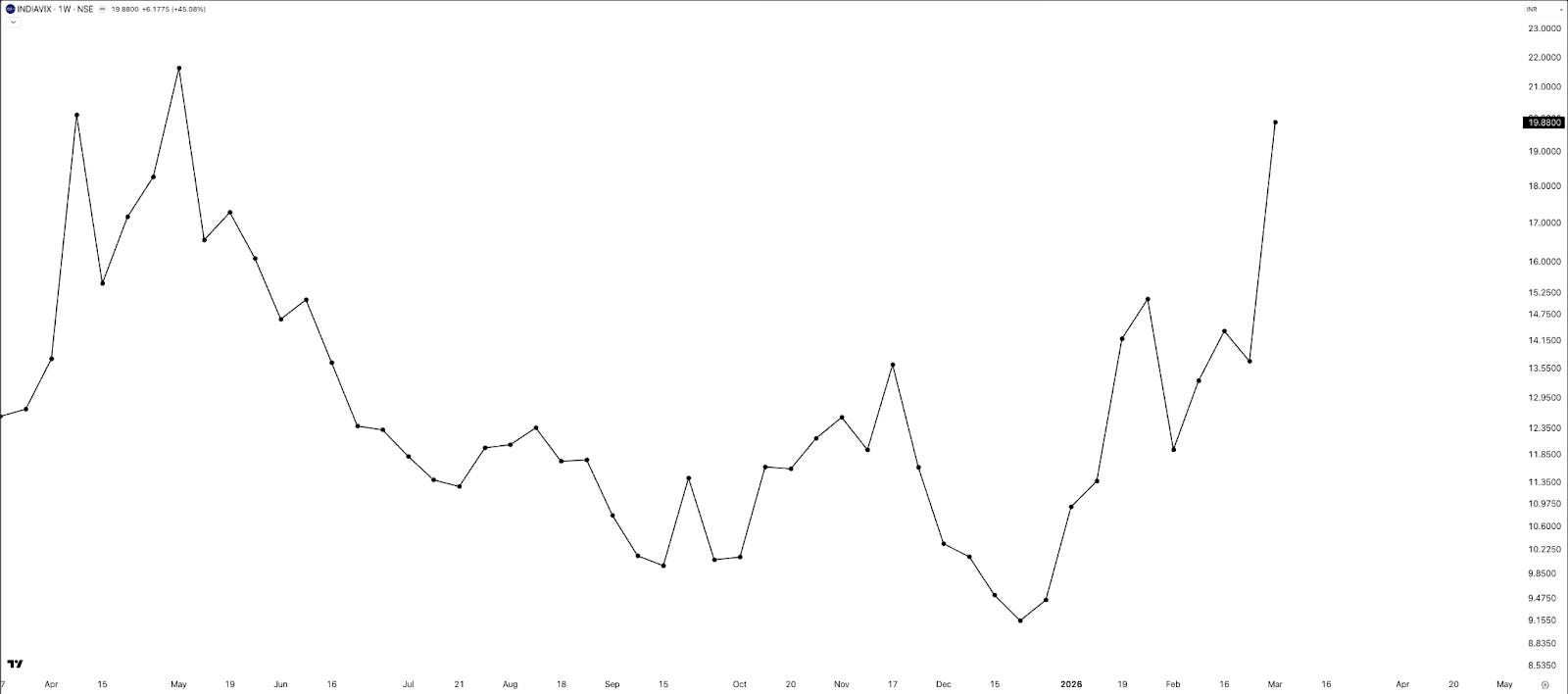

INDIAVIX surged 45% this week to close at 19.88 , briefly crossing 21 intraday. The rise is consistent with heightened geopolitical uncertainty. Elevated VIX means more volatile price action ahead and inflated premiums across near and far-term options.

The best opportunities in options markets typically come after this phase — when VIX cools and implied volatility compresses. But first, the priority is to survive the current rising-vol regime, which is often the most punishing stretch for options strategies.

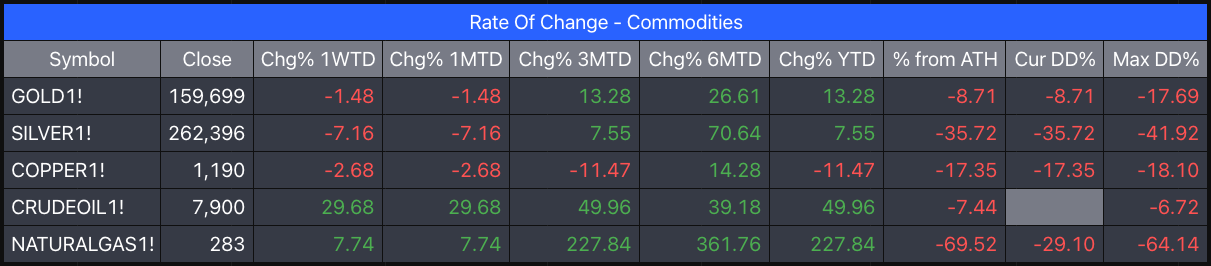

Commodities

This was one of those unusual weeks where both equities and precious metals fell simultaneously — even as the rupee weakened against the dollar.

- Crude Oil: +29.68%

- Natural Gas: +7.74%

- Silver: –7.16%

- Copper: –2.68%

- Gold: –1.48%

The energy spike deserves attention: India imports close to 50% of its crude from the Middle East. A sustained move higher in oil translates into a larger import bill, further rupee weakness, and rising inflation. In a connected world, no one is fully insulated from geopolitical risk.

On a related but different note, I will be conducting a Zerodha Varsity Live course on Commodity Trading on the 14th and 15th of March, which is the coming weekend.

Just in case you are interested, do have a look - as with all varsity live courses, this too is free.

Summary

Week 10 was sharply negative for equities, with all major indices ending deep in the red. BANKNIFTY — which had been holding up relatively well — turned into the biggest weekly loser, marking a notable shift in character.

Volatility expanded significantly, with multiple 1%+ daily moves, wider weekly ranges, and INDIAVIX rising 45%. Price action remained clearly bearish, with rallies getting sold into and markets trading well below key moving averages.

Sectorally, NIFTY CPSE was the lone performer; most other sectors ended negatively, reflecting broad-based weakness. In commodities, precious metals corrected while energy markets surged on geopolitical concerns.

The overall structure remains bearish to sideways — rising volatility, weak breadth, and a market that continues to sell strength.

What Caught Our Attention This Week

1. State of the Markets — Prabhakar Kuduva A current market read from a fund manager and analyst worth following — covering where markets stand, sectors to focus on, and the outlook ahead. Recommended reading in the context of long-term investing. Read here →

2. The Acquired Podcast — Formula 1 Whether you follow F1 or are simply curious about how complex businesses are built, this episode is worth your time. It covers the technology and business model behind Formula 1 in the depth Acquired is known for. Listen here →

What to Expect Next Week

Next week is a full five-day trading week with no major scheduled events on the calendar. Geopolitical uncertainty remains elevated, and the trend continues to point lower.

We are living through times where black swans are beginning to feel almost routine. All one can do is hunker down and let the storm pass. But markets at correction levels also create opportunity — the last 10%+ correction from ATH came in April 2025, and we’re currently at about 7% off the top. Keep your SIPs and long-term investments going. Let the market do its job.

If you find this series useful, don’t forget to subscribe to the newsletter.

Until then — stay curious, stay steady, and enjoy your weekend.