Hello and welcome to the Weekly Market Metrics! I’m Sandeep Rao, and we are now in Week 24 of 2026.

On the Iran front — I really thought it was resolved after close to three months of uncertainty. On Thursday, Trump claimed a breakthrough in talks; Iran declined. On Friday, Iran confirmed the deal — including the reopening of the strait. And within a few hours, Iran rejected Trump’s deal again. I know I shouldn’t be saying this, but Covid times seem better compared to this. This is madness of a different order.

Closer to home, after one of the worst summers on record, the monsoon isn’t cooperating either. IMD expects below-average rainfall over the next two weeks — the first ten days of June were already 26.5% below normal. The first below-normal monsoon season in three years. Even the rain gods don’t seem to be happy in 2026.

Two Stories Worth Your Time

Nifty and Gold moving in sync. We’ve been pointing this out for a while — same direction, same timeframes. Gold is no longer acting as a hedge, at least not in the near term. A few possible reasons: we’re experiencing high inflation, which lifts corporate revenues and pushes stocks up while eroding cash, driving investors into gold. The old 60/40 portfolio has broken down again due to inflation — bonds are no longer acting as a hedge, so money rotates into gold. And the Iran war pushed oil past $100, forcing energy-importing countries to sell gold reserves for dollars to buy oil — the very event that should have sent gold soaring actually suppressed it. It could be a combination of these reasons playing out.

The SpaceX IPO and index fund dynamics. On 12 June, the world’s largest IPO went live — SpaceX listed on Nasdaq at a valuation of $1.75 trillion, nearly 42% of India’s entire GDP. But the real story is what happens to index funds. Nasdaq cut its waiting period from three months to just 15 trading days to accommodate SpaceX. FTSE Russell went to five. Index funds are projected to absorb $22 to $27 billion in SpaceX shares — funded by sales of Apple, Microsoft, and Nvidia. That’s how index rebalancing works.

But SpaceX as a company lost $4.9 billion in 2025 and another $4.3 billion in just the first quarter of 2026. It is valued at 94 times its revenue. Among all index providers, the S&P 500 held the line — saying profitability is required, and no entry before mid-2027. Three index providers bent their rules for one company. One didn’t. Anthropic IPOs later this year — it will be worth watching what happens next. An interesting dynamic playing out in the US.

A quick note: there’s an upcoming Varsity Live Session on Commodities Basics — this time in Hindi, co-presented with Prateek Sharma from Varsity. The session is on 20 and 21 June, completely free, and available only in live format with no recording. Register here

Section 1 — What Happened Last Week

Rate of Change (ROC) Across Indices

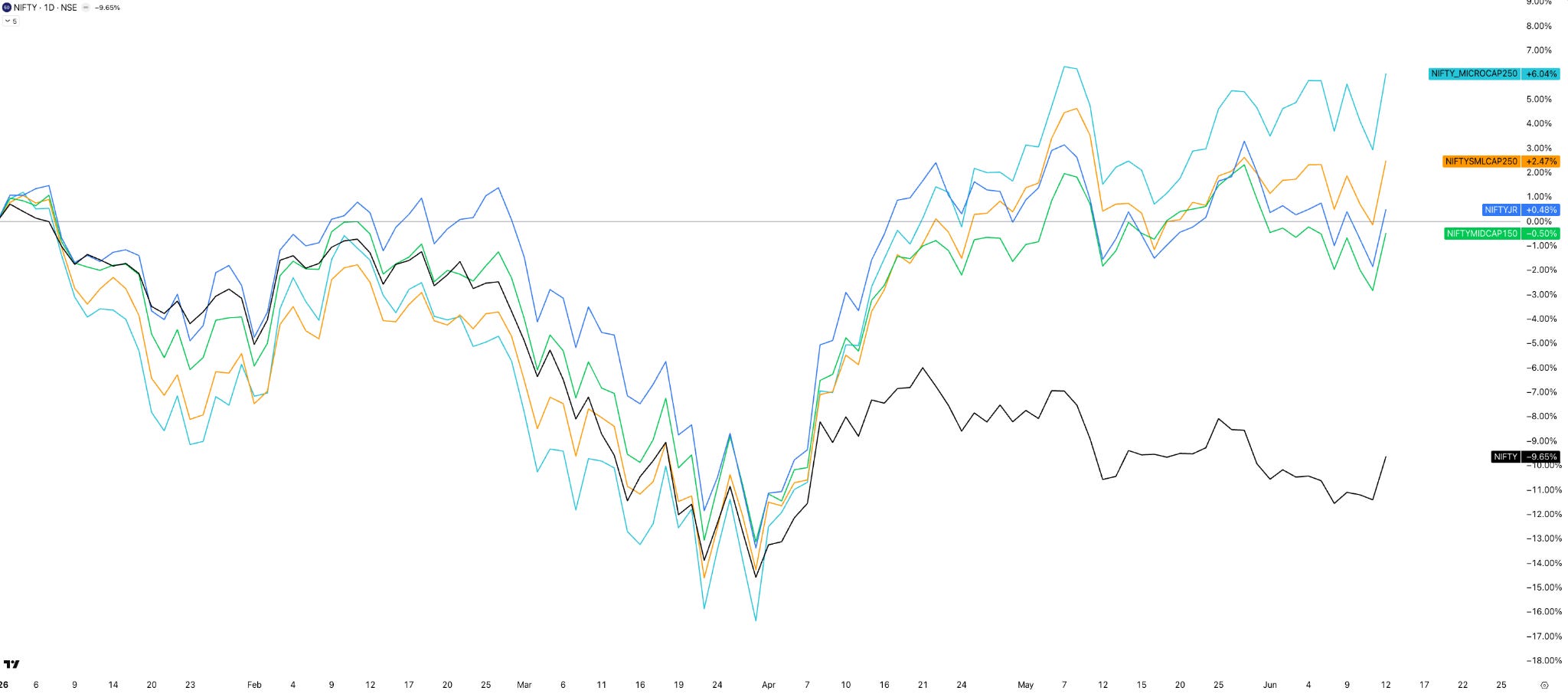

Not much happened this week — the one exception being Nifty 50, which gained 1.1%, largely thanks to Friday’s move. The other four — Next 50, Midcap 150, Smallcap 250, and Microcap 250 — all ended the week flatish.

On 3-month returns, Microcap 250 leads the pack at 21.6%, while Nifty 50 is the lowest at just 2.1%.

On YTD numbers, Microcap 250 again leads at +6%, while Nifty 50 is the clear laggard at -9.65%. Smallcap 250 is at +2.5%, and Midcap 150 and Next 50 are both almost flat.

Nifty Bank stands out again this week — up 4.25% for the week and 13% over the last three months. Midcap Select is the only index still in the green for 2026.

NIFTY

Weekly

This week, Nifty gained 256 points, or 1.1%, to close at 23,623 — and it still continues to trade below all its key weekly moving averages.

As mentioned last week, Nifty was in a range between 24,600 and 23,150. This week, it broke below the lower end of that range, making a new low around 23,070 — but held above the 23,000 level. Then came Friday’s move, which pushed the index well above that support. Going into Week 25, the 23,070 to 23,000 zone now works as a strong support.

The weekly range remained almost identical to last week — 575 points this week versus 582 points last week. On the daily timeframe, Friday saw the widest range at 331 points, while Tuesday — the weekly expiry day — came in as the narrowest at just 175 points.

Daily

If you look closely at the daily chart, the first four days of the week were like four days of eating salad — and then biryani on Friday. The market moved in a combined 350-point range across those four days, and then Friday just printed a massive 2% green candle.

In Week 24, Nifty has finally climbed back above the 21 EMA — but continues to trade below the 50 and 100-day EMAs, as well as the 200-day SMA. Encouraging to see, but it’s one step at a time.

Hourly

On the hourly chart, Nifty stayed below the 50 EMA until Wednesday, then chopped through Thursday. Friday’s gap-up opening and follow-through post 1:30 PM kept it well above the 50 EMA to close the week.

Hoping for a clean uptrending move from here — but in 2026, hardly any weekend has gone by without some notable event affecting how the market behaves on Monday. Let’s see if this weekend is any different.

Nifty Weekly Expiry — Tuesday, 9 June

It had the lowest daily range of the week at just 175 points, with an opening ATM straddle premium of just 129 points. It was a fairly decent expiry for non-directional traders — mainly options sellers. A 175-point range, in an environment where we routinely see 250 to 300-point daily ranges, felt noticeably calm. The post-2 PM shenanigans were there — but overall, it was an easy 0DTE for short vol traders. Let me know in the comments how your expiry went.

Section 2 — What to Expect in the Coming Week

NIFTY

The 23,070 to 23,000 zone is now a strong support — Nifty tested it multiple times and couldn’t break below it. On the upside, 24,000 to 24,100 is the first resistance, followed by 24,600 and then 25,000.

After many weeks, the overall bias for Nifty has finally shifted — from bearish-sideways to bullish-sideways .

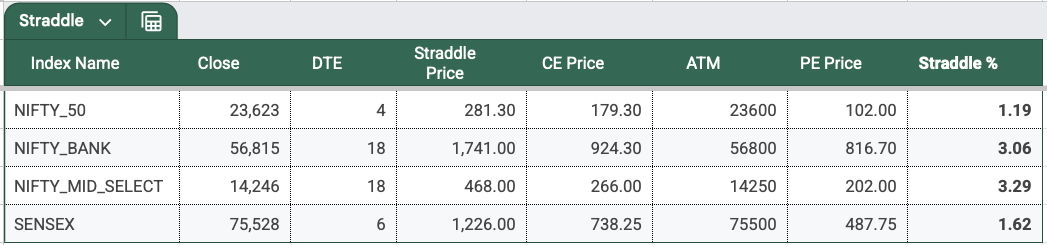

The Nifty ATM straddle closed at 281 points, up from 267 points last week, implying an expected move of roughly 1.19% on either side. That gives an expected range of 23,904 on the upside and 23,342 on the downside for the upcoming weekly expiry on Tuesday, 16 June .

Looking back at last week’s straddle pricing — the expected range was 23,634 to 23,100, and Nifty closed at 23,242 on weekly expiry, well within that range. However, the actual range it made over those two days was 297 points — including the gap down on Monday — against a straddle premium of 267. Realised volatility was still higher than implied volatility.

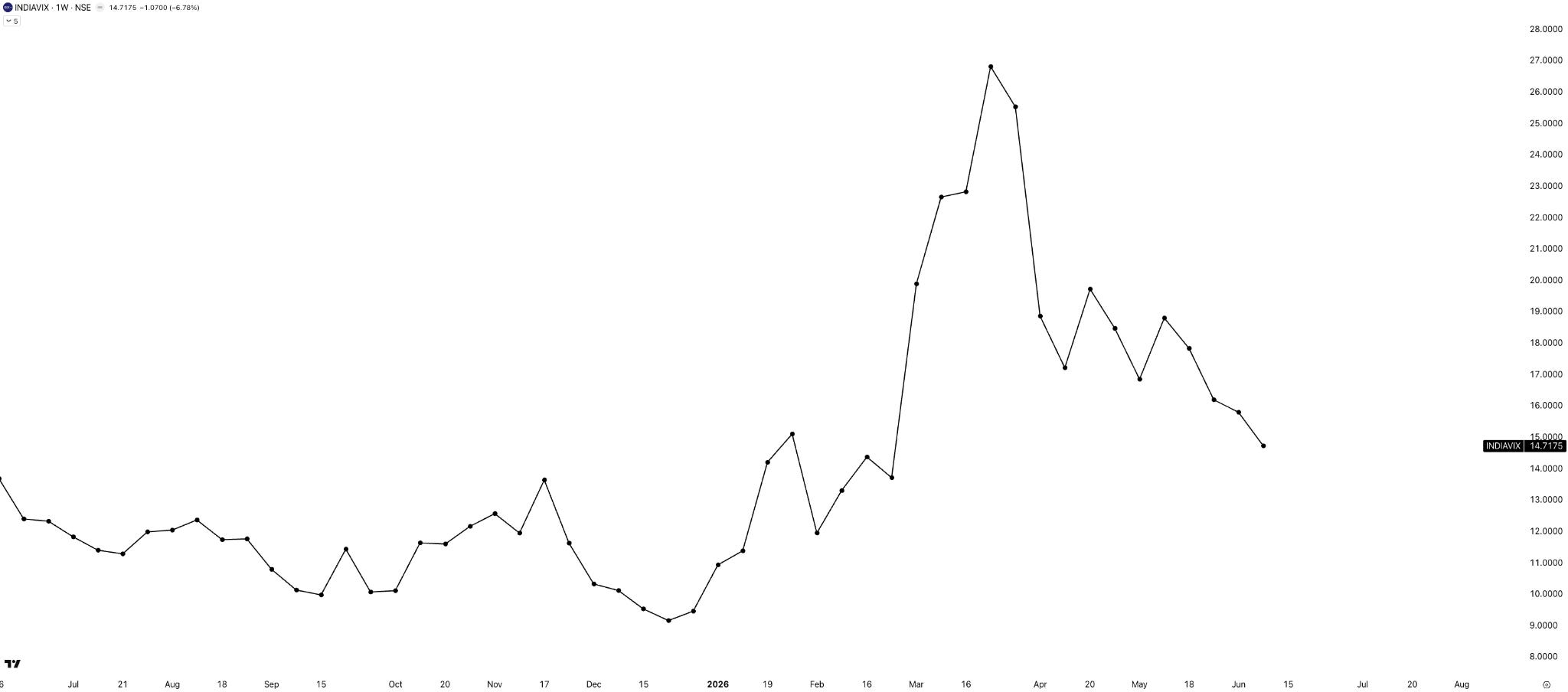

India VIX

India VIX fell 6.8% this week, closing below 15 for the first time in a while, at 14.72. Is this the beginning of acchhe din for the markets? I really hope so.

Sectoral Performance

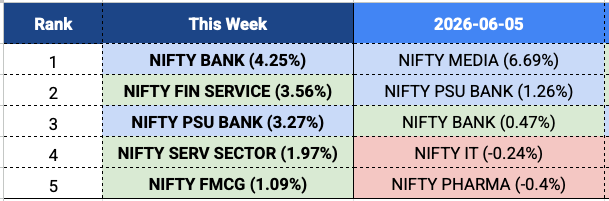

Nifty sector view: Nifty Bank tops the list this week with a 4.25% gain — notably, it was sitting at just 0.47% last week in third place. A significant jump. Nifty Fin Service comes in second at 3.56%, and PSU Bank holds on at third with 3.27% — that’s two weeks running for PSU Bank, which as always, is a signal worth watching. The financial space is dominating the top three spots this week. Nifty Serv Sector and FMCG round out the top five with gains of 2% and 1.1% respectively.

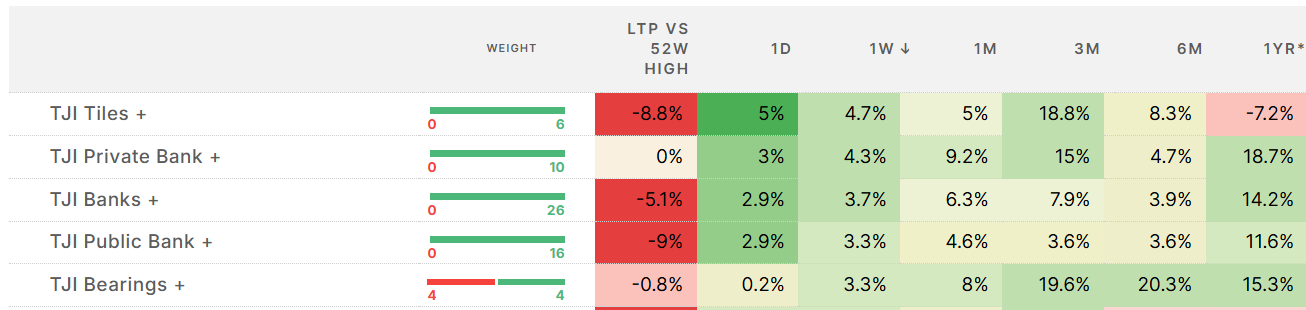

Tijori index view: TJI Tiles at the top, which has been holding up well for three months, followed by Private Bank and Banks, then Public Bank, and Bearings. No overlaps with last week’s sectors. This was a week about banks and banking across the board. Worth watching to see if this holds.

Commodities

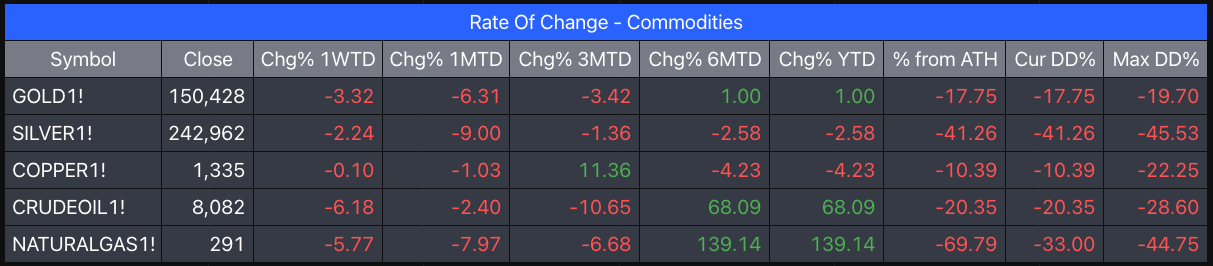

On the daily timeframe, Gold futures have clearly slipped below their 50 EMA — currently trading around ₹1,48,500, with the 50 EMA sitting up at ₹1,55,600. A sharp drop early in the week was followed by a mild bounce, but no real sign of strength yet. Silver is in a similar spot — trading around ₹2,47,600, well below its 50 EMA at ₹2,62,400. Some support near the lows and an attempted recovery, but like Gold, nothing convincing. Both metals are now trading below their 50 EMAs — wait-and-watch continues.

On a weekly basis, it was a red week across the board — no gainers. Crude Oil was the biggest loser, down 6.18% — quite a reversal from the 6.50% gain it posted just last week. Natural Gas wasn’t far behind, down 5.77%, and Gold slipped 3.32%. Silver was down 2.24%, while Copper barely moved, down just 0.10%.

Summary

Markets ended the second week of June on a positive note, with Nifty gaining 1.1% to close at 23,623 — though it was largely a Friday story. The Iran deal finally coming through was the big macro development, and after months of uncertainty, that’s one less thing hanging over the market.

The divergence across market caps remains the defining story of 2026 — Microcap and Smallcap continue to hold their ground, while Nifty 50 remains the clear laggard, still down nearly 10% for the year.

On the sectoral front, the financial space dominated this week — Nifty Bank, Fin Service, and PSU Bank swept the top three spots. PSU Bank, showing up for the second week running, is worth keeping an eye on.

Commodities had a tough week — red across the board. Crude gave back last week’s gains entirely, and Gold and Silver are both trading below their 50 EMAs with no clear direction.

The bottom line: after many weeks, the overall bias has finally shifted — from bearish-sideways to bullish-sideways . One step at a time.

What Caught My Attention This Week

Read: “Why China got rich, and India didn’t” — a Substack essay by David Oks, published this week. In 1950, China and India were equally poor. By 2022, China’s median income was two and a half times India’s — and the gap widened even after both countries fully liberalised. Oks’s argument is that the divergence happened around the 1950s. China, through brutal and often catastrophic means, spent three decades building human capital — literate, healthy, disciplined workers ready for industrial modernity. India’s traditional social order survived independence intact. When the economy opened in 1991, India simply wasn’t prepared the way China was. Fair argument and hard to dismiss. Read it here

Watch: David Perell sits down with Steven Pinker, the Harvard linguist, to talk about what makes writing good and what AI is doing to it. Pinker says something early on that stuck: great writing is about making ideas visual, not just clear. In a world where AI generates fluent text by the second, that distinction matters more than ever. About forty minutes. Absolutely worth it. Watch on YouTube

Events to Factor In

Next week is a 5-day trading week with no market holidays.

The Fed’s interest rate decision comes on Wednesday at 11:30 PM IST — watch out for some initial volatility on Thursday morning, which also happens to be the Sensex weekly expiry. Lately, these announcements have been well telegraphed and largely priced in by the market, so there hasn’t been much volatility around the actual decision. Will this time be any different? Let’s see.

If you find this series useful, don’t forget to subscribe to the channel — and do share it with your friends.

Until then — stay curious, stay steady, and enjoy your weekend.