Hello and welcome to the Weekly Market Metrics! I’m Sandeep Rao, and we’re in Week 26 of 2026.

The Strait of Hormuz has opened, and oil wasted no time in taking the elevator down. As of now, Brent crude is at its lowest since before the Iran war — around $73 a barrel, nearly 39% off from the $120 peak. For India, the key thing is the Rupee. We import close to 85% of our crude, so when oil drops this hard, the current account improves, and the Rupee gets stronger. The Dollar-Rupee is around 94 right now.

But the monsoon is a separate concern. The deficit has widened to 43% nationally, the advance has stalled near Mumbai, and both IMD and the US National Oceanic and Atmospheric Administration are flagging a moderate to strong El Niño this year. Central India is at a 63% deficit. If July and August don’t deliver, kharif crops — summer-sown staples like rice, pulses, oilseeds — will feel it, and food inflation could concern the RBI.

And if you follow the startup ecosystem, you could not have missed Kunal Shah being named global head of WhatsApp. Founders stepping out to run someone else’s company is rare — but with Kunal, the predictable move was never on the table. There’s a short Rainmatter conversation with him and Dinesh Pai that just dropped, possibly his last on record as CRED’s founder and CEO.

Markets did reflect the general positive backdrop — Nifty is up roughly 0.2% on the week, trading around 24,050 as of Thursday’s close. This was a short week on the eve of Muharram.

Section 1 — What Happened Last Week

Rate of Change (ROC) Across Indices

Not much changed this week, which is exactly what you’d expect after last week’s rally. Nifty 50 ended almost flat, up just 0.2%, while Nifty Bank continued to inch higher with a gain of 0.9%.

The one exception was Nifty Mid Select, which corrected 1.3% after being one of the strongest performers over the last few weeks. Even then, it remains up nearly 19% over the last three months and close to 5% for the year.

The broader takeaway hasn’t changed. Nifty Bank continues to be one of the strongest large-cap indices, while Nifty 50 still remains down almost 8% for the year. One quiet week doesn’t change the trend.

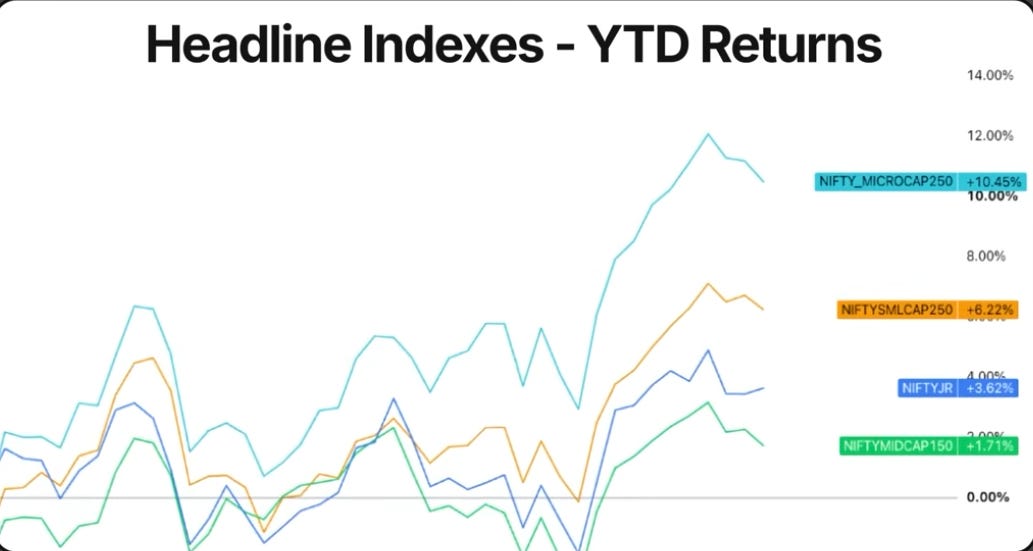

On YTD numbers, Microcap 250 continues to lead at 10.5%, followed by Smallcap 250 at 6.2%. Next 50 is up 3.6%, while Midcap 150 has eased to 1.7%. Nifty 50 remains the clear laggard at -8%. The past week hasn’t changed the broader picture — 2026 continues to reward investors willing to move beyond the headline index.

NIFTY

Weekly

A truncated week with just 4 trading days. Nifty gained just 43 points, or 0.2%, to close at 24,056. It continues to trade above both the 10-week and 20-week SMAs, holding on to last week’s breakout.

Nifty is currently hovering around the 24,000 mark. Last week’s breakout has held, but there still isn’t enough evidence to say the index has decisively moved higher. For now, 24,000 remains the level to watch, while 24,600 continues to be the next major resistance.

W26

W25

Even in a relatively low VIX environment, Nifty’s average daily range rose to 242 points this week from 149 points last week — a reminder that low VIX doesn’t always mean small intraday ranges. Monday was the quietest session at just 95 points. Tuesday and Wednesday recorded the widest ranges at 351 and 301 points respectively, while Thursday was still fairly active with a 223-point range.

Daily

On the daily chart, Nifty had a volatile but largely directionless week. After a quiet Monday, Tuesday saw a sharp sell-off, while Wednesday and Thursday recovered most of those losses. The recovery, however, stalled near 24,200, with Nifty unable to close above it. The index ended the week almost flat but, more importantly, continued to hold above 24,000.

Nifty continues to hold above both the 21 EMA and the 50 EMA. It briefly touched the 100-day EMA this week but couldn’t close above it. The 200-day SMA at around 24,900 remains the next major hurdle overhead.

Hourly

Nifty largely stayed above the 50 EMA this week. Tuesday’s sell-off briefly broke that structure, but Wednesday’s recovery quickly reversed it. Thursday saw a move to fresh weekly highs before some profit-booking into the close brought the price closer to the EMA. Overall, the hourly trend continues to remain positive.

Nifty Weekly Expiry — Tuesday, 23 June

The ATM straddle opened at around 90 points and steadily decayed to nearly 57 points by around 11:30 AM. But the sharp afternoon sell-off, which pushed Nifty into a 351-point daily range, saw the straddle briefly spike back to around 108 points before theta took over again into the close. Realised volatility ended up much higher than what the opening straddle had implied, making it a much harder expiry for non-directional sellers. Buyers, on the other hand, must have had a good day. Let me know in the comments how your expiry went.

Section 2 — What to Expect in the Coming Week

NIFTY

The 24,000 level continues to be the key support. Just below that, the 23,800–23,650 gap zone remains an important support area if the market sees a deeper pullback. On the upside, 24,200 has once again proved to be a hurdle — a decisive close above it could open the door for a move towards 24,600, which continues to be the next major resistance.

The overall bias remains bullish-sideways . As long as Nifty holds above 24,000, the benefit of the doubt stays with the bulls.

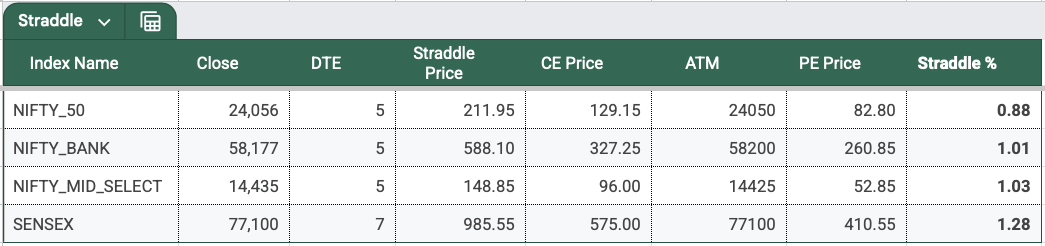

The Nifty ATM straddle closed at 212 points, up slightly from 192 points last week, implying an expected move of roughly 0.88% on either side. That gives an expected range of 24,262 on the upside and 23,838 on the downside for the upcoming monthly expiry on Tuesday, 30 June .

Despite India VIX remaining below 13, the options market is pricing in a slightly wider move than last week, likely reflecting the monthly expiry.

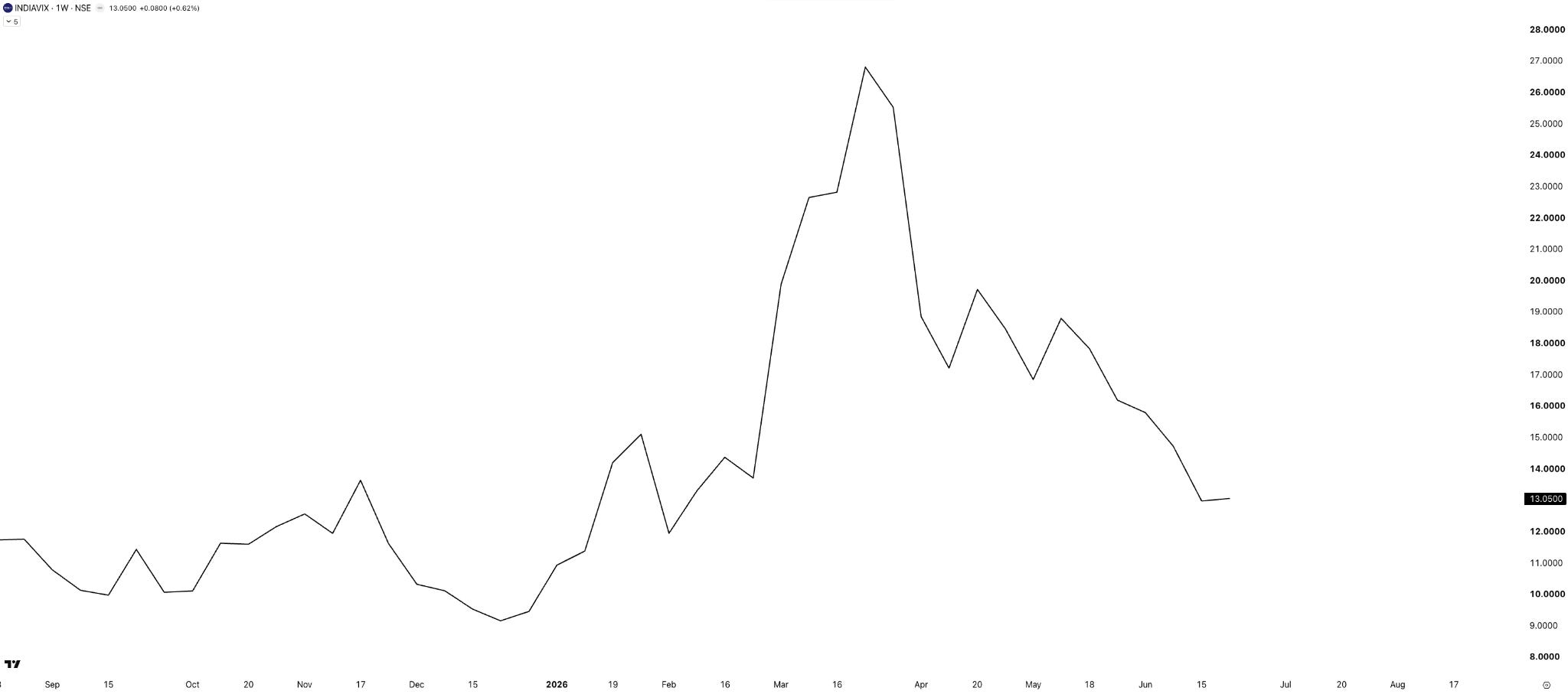

India VIX

India VIX was almost unchanged this week, closing at 13.05 after briefly dipping below 13 last week. This week’s price action was a reminder that low VIX doesn’t necessarily mean low intraday volatility — Nifty’s daily ranges expanded sharply despite VIX staying around 13.

Sectoral Performance

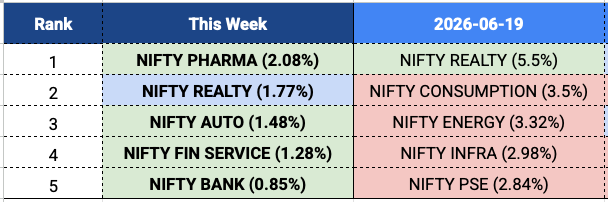

Nifty sector view: Leadership narrowed quite a bit this week. Nifty Pharma took the top spot with a 2.1% gain, followed by Realty at 1.8% and Auto at 1.5%. Financials also made a comeback, with Fin Service and Bank rounding out the top five. Unlike last week, when leadership was broad-based, this week saw more modest gains with no sector returning more than 2.1%. Worth watching whether Pharma can sustain this momentum.

W26

W25

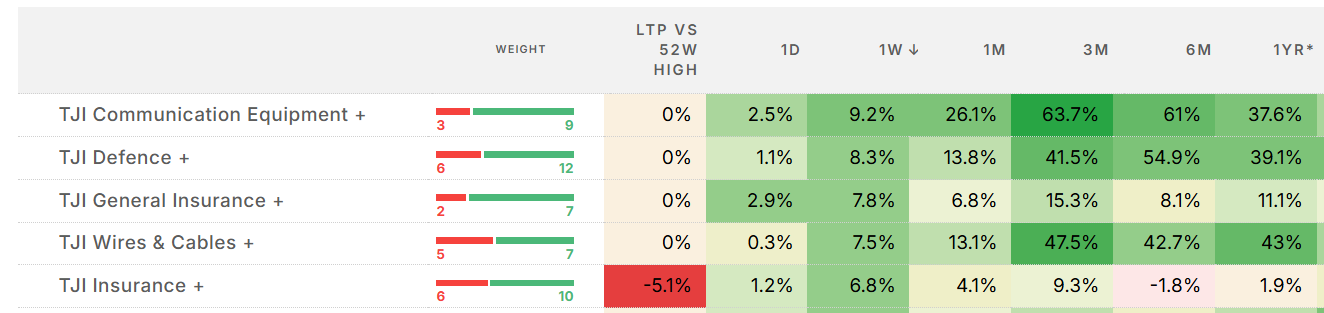

Tijori index view: QSR is at the top, up about 4.7%. The sector has had a difficult year — weak demand, rising input costs, pressure on earnings — so this week’s move looks more like a relief rally than a sign that the fundamentals have completely turned. Hospitality is a similar story. General Insurance is up as well, but that looks more like a continuation of the NSE IPO-related re-rating discussed last week rather than fresh news.

What caught attention this week was Transformers and Refractories appearing together . Transformers — the industrial kind — are a critical part of India’s power infrastructure. Every time the grid expands or renewable capacity is added, more transformers are needed. At the heart of most transformer cores is a material called Cold Rolled Grain Oriented electrical steel, or CRGO, much of which India imports. Refractories, on the other hand, are the heat-resistant materials used to line steel furnaces — an essential consumable in steel manufacturing.

The link between the two came on 23 June, when the Directorate General of Trade Remedies initiated an anti-dumping investigation into imports of CRGO electrical steel and amorphous metal from China, Japan, Korea, and Russia, following a complaint by JSW JFE Electrical Steel. If the investigation eventually results in anti-dumping duties, it could encourage greater domestic production of transformer-grade electrical steel, which may also benefit upstream industries such as refractories. Whether this week’s move in these two Tijori indexes was driven entirely by this news is difficult to say — markets rarely move for a single reason. But the timing is certainly interesting, and it’s one development worth keeping an eye on. Business Standard — Anti-dumping probe into electrical steel

Commodities

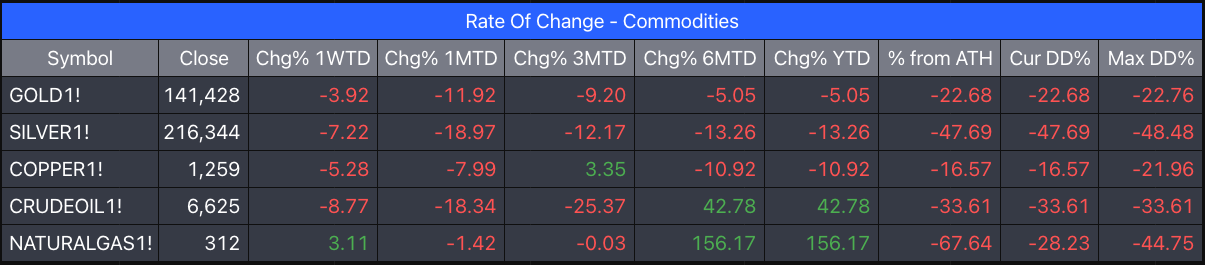

On the daily timeframe, both Gold and Silver continue to remain under pressure. Gold futures are trading around ₹1,39,700, well below the 50 EMA at ₹1,52,700. After last week’s weakness, prices extended their decline further before seeing a small bounce on Thursday. Silver tells a very similar story — currently trading around ₹2,23,200, significantly below its 50 EMA at ₹2,59,700. Like Gold, it has seen a small rebound after a sharp fall, but remains well below its moving average. Both precious metals continue to trade below their 50 EMAs, and until they reclaim those levels, the broader trend remains weak.

On a weekly basis, it was another weak week for most commodities. Crude Oil led the losses, falling 8.8%, followed by Silver at -7.2%, Copper at -5.3%, and Gold at -3.9%. The only commodity that ended in the green was Natural Gas, gaining 3.1%.

Despite the recent correction, Natural Gas remains the standout performer of 2026 with gains of over 156%, while Crude Oil is still up nearly 43% for the year.

Summary

Markets took a breather after last week’s rally, with Nifty ending almost unchanged but comfortably holding above the 24,000 mark. India VIX remained anchored near 13, although the sharp swings on Tuesday and Wednesday were a reminder that low VIX doesn’t always mean low intraday volatility.

The broader market story remains intact. Microcap 250 continues to lead the pack in 2026, while Nifty 50 is still the clear laggard, down around 8% for the year. Nifty Bank continues to quietly outperform among the large-cap indices.

On the sectoral front, leadership narrowed this week, with Pharma, Realty, and Auto leading the gains. Among the Tijori indexes, the anti-dumping probe into transformer-grade electrical steel made Transformers and Refractories two interesting sectors to keep an eye on.

Commodities remained under pressure. Crude Oil, Gold, Silver, and Copper all declined, while Natural Gas was the lone bright spot and continues to be the best-performing commodity of 2026.

The bottom line: the market continues to consolidate above 24,000. The broader trend remains bullish-sideways , but a decisive move above 24,200 is still needed to signal the next leg higher.

What Caught My Attention This Week

Given there’s a long weekend coming up, here are two long-form listens worth saving for it.

Watch: Emily Chang’s extended interview with Anthropic CEO Dario Amodei on The Circuit at Bloomberg Originals. It covers a lot — his San Francisco roots, leaving OpenAI, the Pentagon standoff — but the part worth sitting with is the Mythos section. Mythos is Anthropic’s most advanced model, one they deliberately held back from public release because it could autonomously navigate cyber kill chains — meaning it can independently plan and execute a cyberattack from start to finish. They took the commercial hit to patch vulnerabilities first. There’s also a section on civilisational collapse risk — Amodei puts it at 10 to 25% — which sounds alarming, but as with any predictions about the future, it’s always better to take it with a spoonful of salt. Worth the full hour.

Listen: The latest Acquired podcast episode — on The Walt Disney Company. Ben and David go deep on Walt’s era: the story of how the man who went bankrupt twice and lost his first hit character to a distributor ended up building an empire by turning Mickey Mouse into an unstoppable money-making machine. If you’ve ever wondered how Disney became Disney, this is the one. Long, as Acquired always is — but worth every minute.

Events to Factor In

Back to a full 5-day trading week next week. Tuesday, 30 June, marks the NSE monthly expiry for Nifty, Bank Nifty, Midcap Nifty, and the other NSE index derivatives — after which we roll into the July series.

No major known macro events on the calendar as of now, unless something unexpected pops up.

One interesting thing worth noting: there isn’t a single market holiday in July or August, apart from the regular weekends. Let me know in the comments which you prefer — a long weekend or an uninterrupted five-day trading week. Zerodha Holiday Calendar

If you find this series useful, don’t forget to subscribe to the channel — and do share it with your friends.

Until then — stay curious, stay steady, and enjoy your long weekend.