A thread for discussing all your trades, strategies, ideas, news, stories, etc.

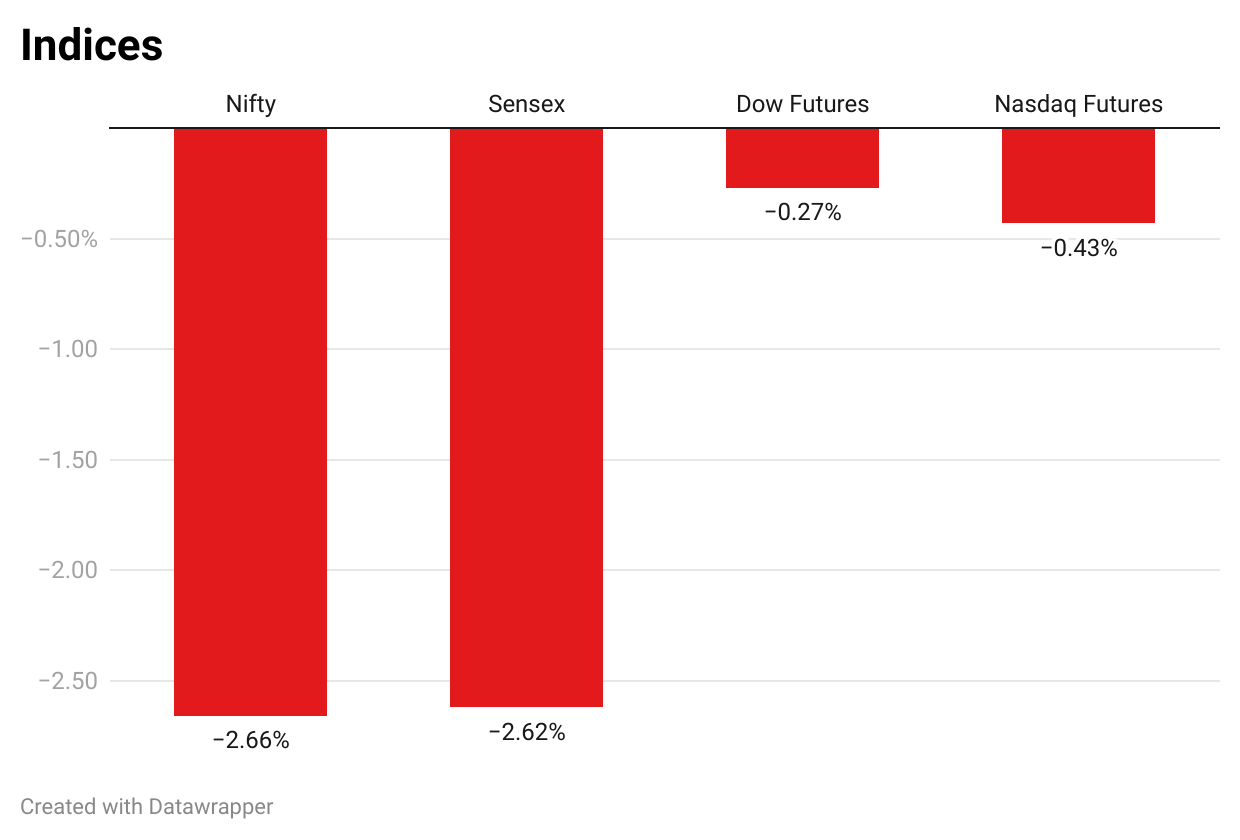

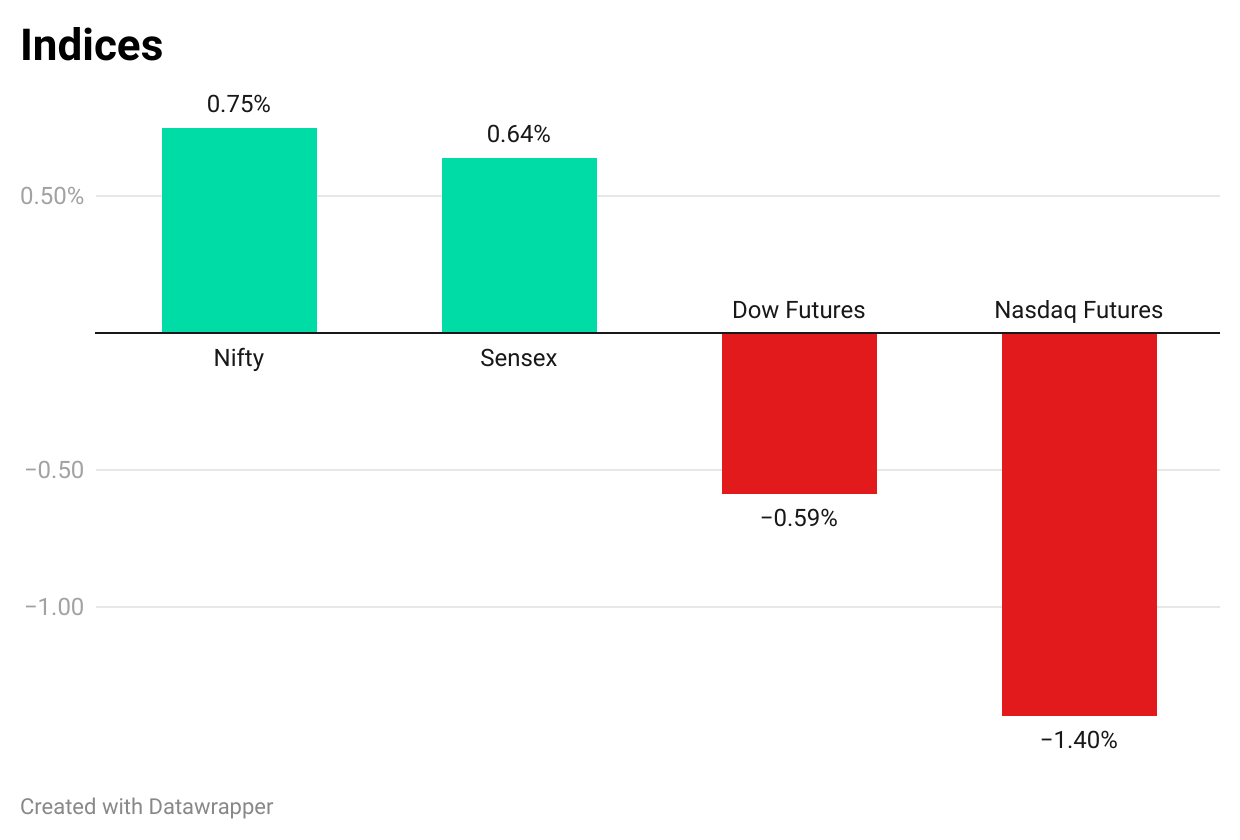

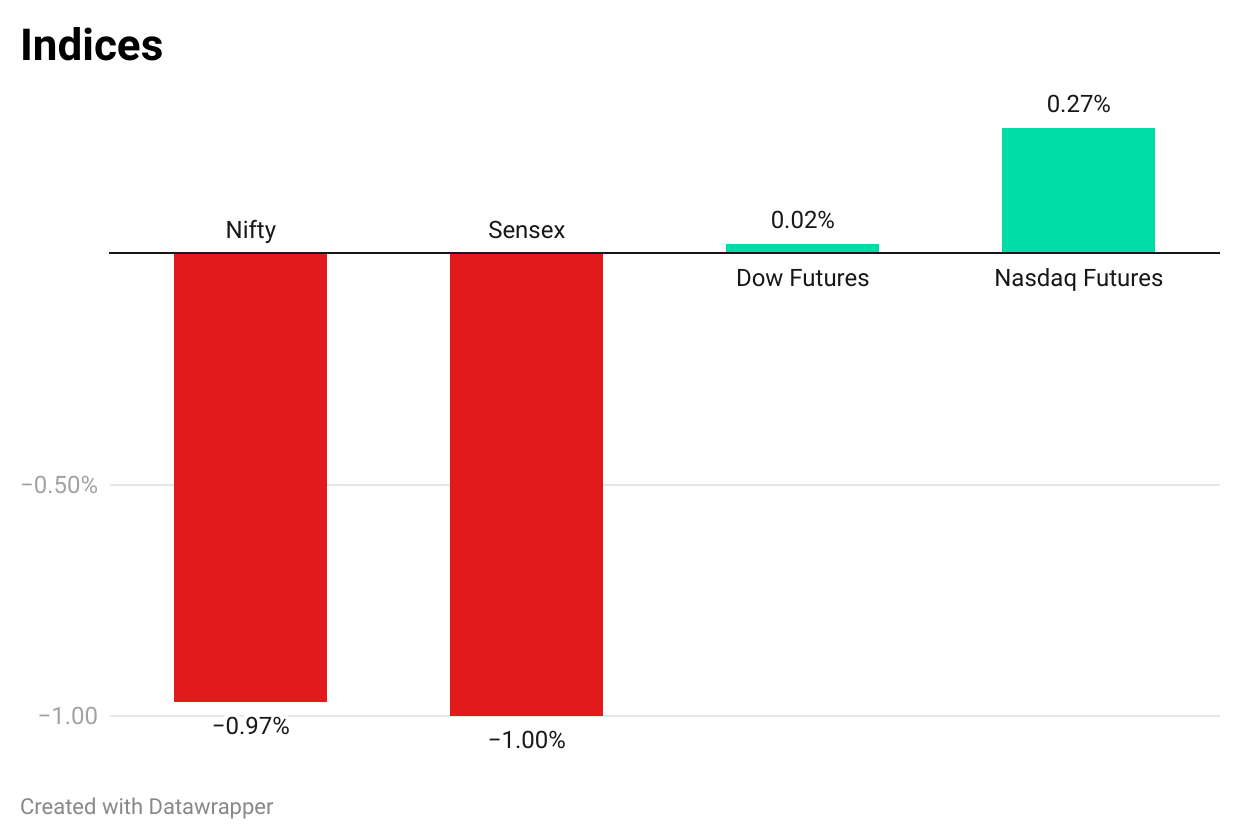

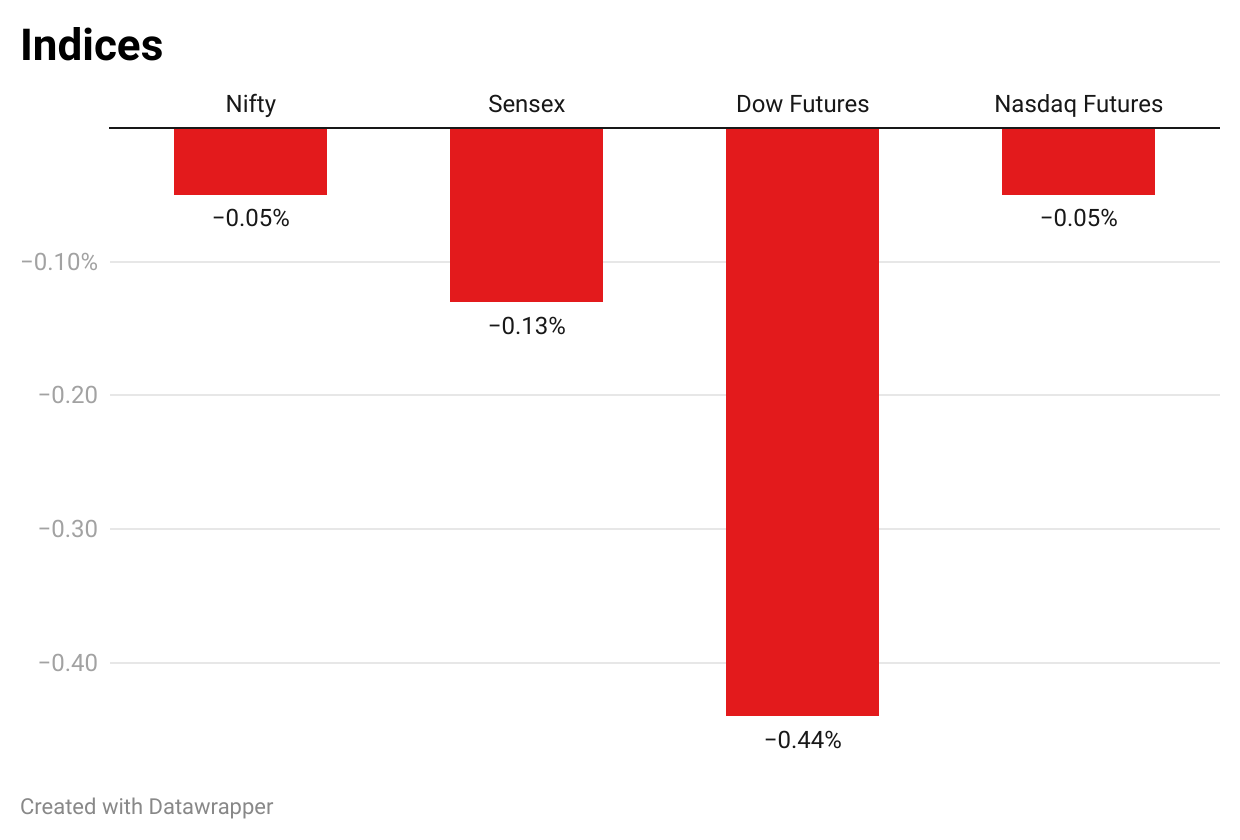

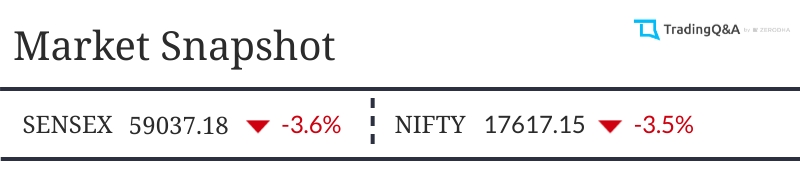

It was a bad week for equity markets around the world. Sensex shed 2185 points to end the week down by -3.6%, while Nifty gave up 638 points, down by 3.5% for the week, ending a four-week gaining streak.

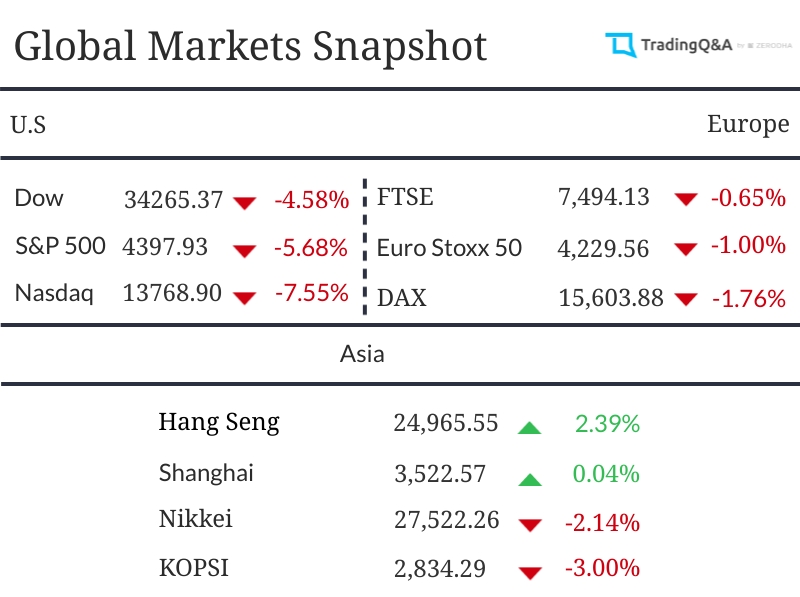

Globally, amongst the major markets, only Hang Seng and Shanghai Composite Index managed to end the week on a positive note. US markets, S&P and Nasdaq suffered their worst week since the pandemic began, tumbling -5.7% and -7.55%.

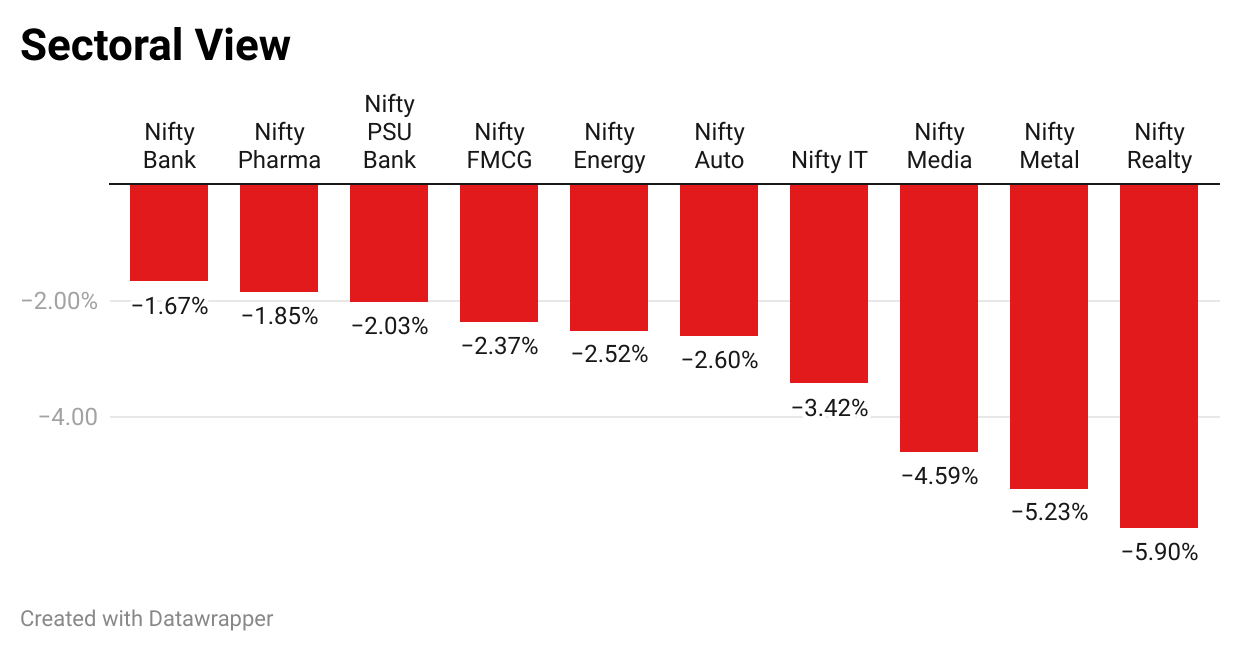

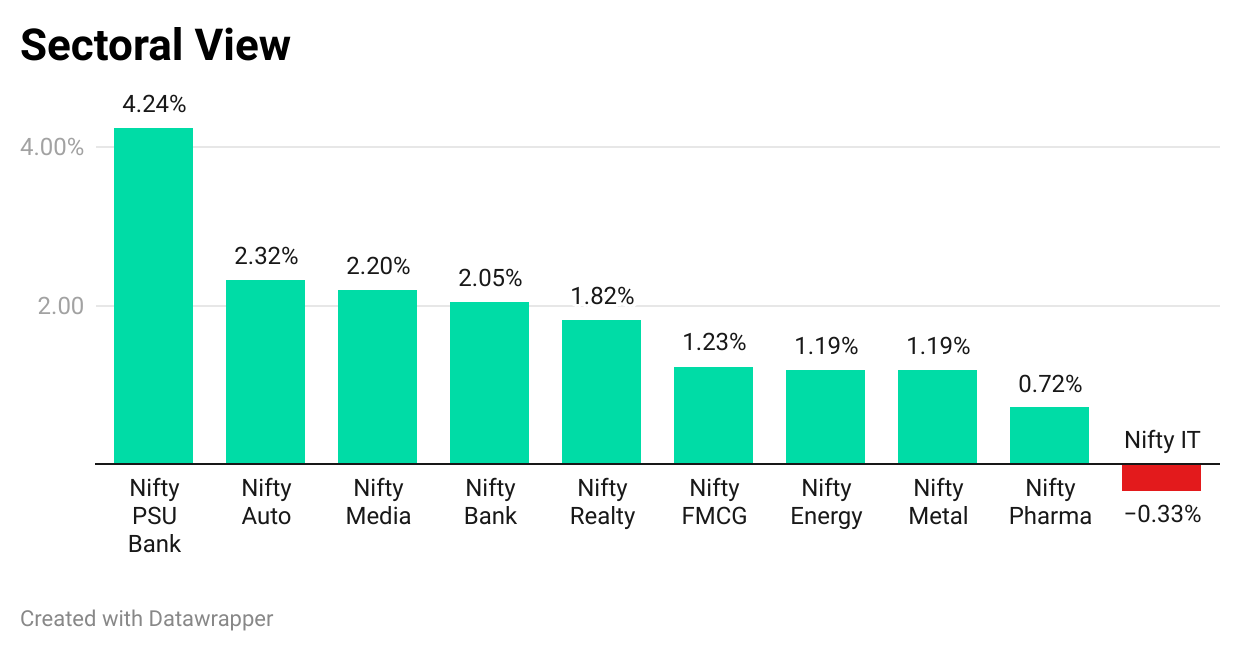

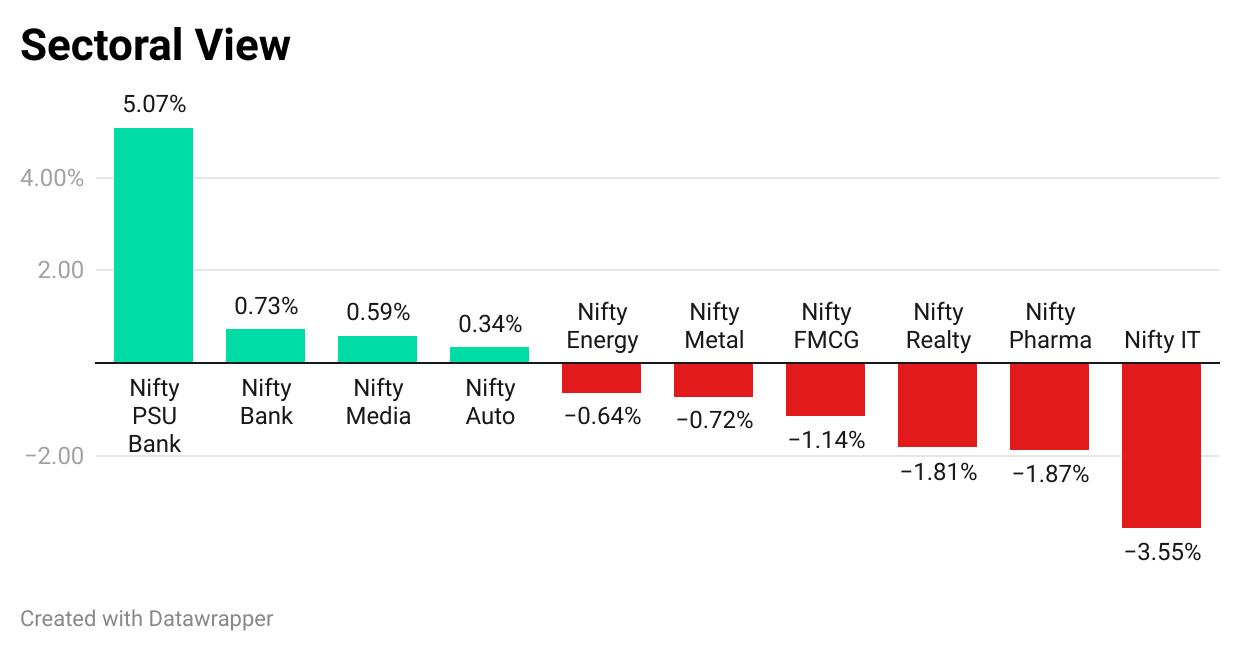

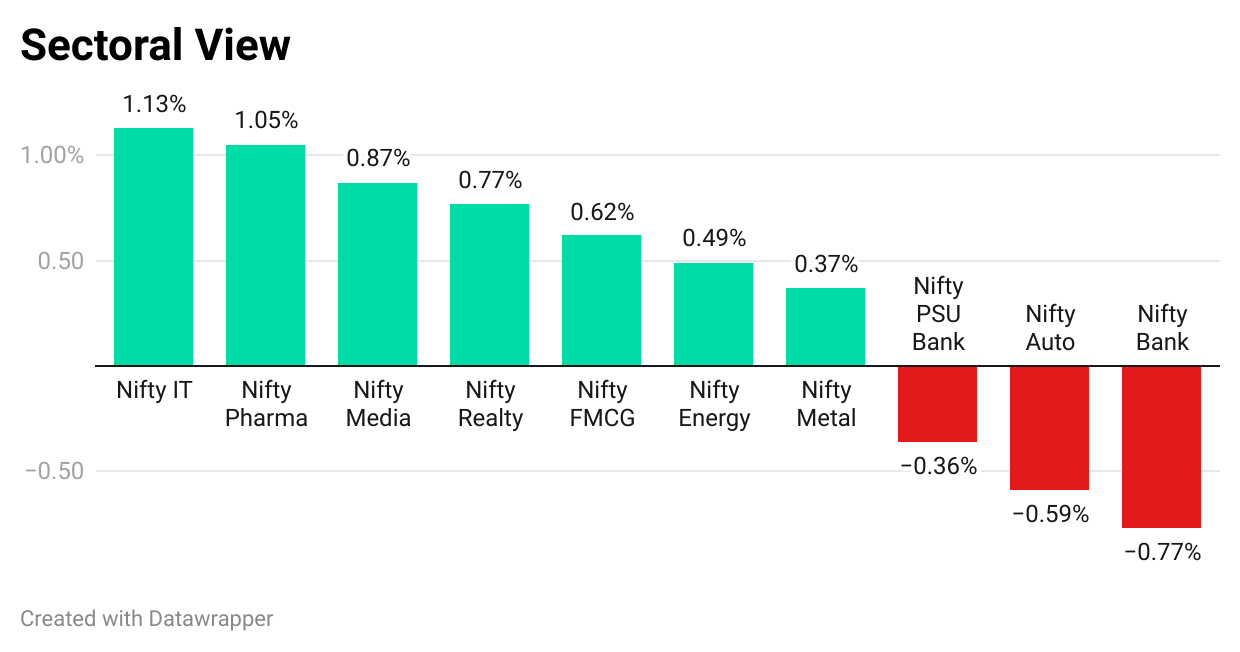

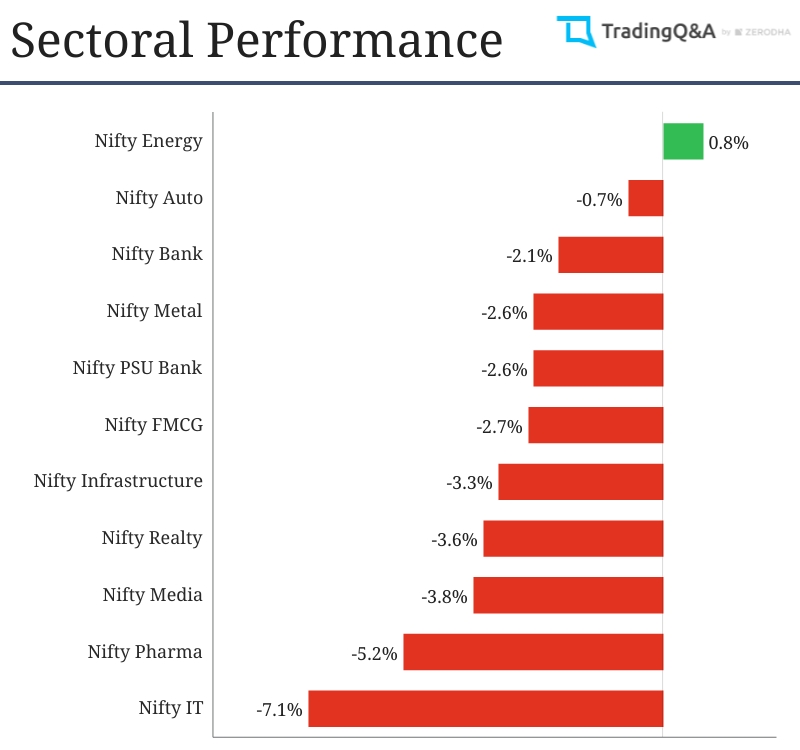

Nifty Energy was the only sector that managed to post-minimal gains for the week, while all other sectors ended up in red. Pharma -7.1% and Pharma 5.2% were the top draggers.

Things to watch out for in the week:

IPOs

Adani Wilmar’s Rs. 3,600 crore IPO will option for subscription on 27th January, with a price band set between Rs. 218 - 230. The IPO will close on 31st January. More details on the Adani Wilmar IPO here: Everything You Need to Know About the Adani Wilmar IPO

Corporate earnings to watch for:

| 24th Jan | 25th Jan | 26th Jan | 27th Jan | 28th Jan | 29th Jan | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Axis Bank Limited | Maruti Suzuki | - | Bharat Heavy Electricals Limited | Atul Limited | IDFC First Bank | |||||

| Burger King India | Aditya Birla Sun Life AMC | Birla Soft | AU Small Finance Bank | IndusInd Bank | ||||||

| Craftsman Automation | Can Fin Homes | Canara Bank | Bharat Electronics | NTPC | ||||||

| Deepak Nitrite | Cipla | Colgate Palmolive | Britannia Industries | |||||||

| Indian Energy Exchange | Federal Bank | Fino Payments Bank | Central Bank of India | |||||||

| HDFC AMC | Indiabulls Real Estate | Indus Towers Limited | Dixon Technologies | |||||||

| SBI Cards and Payment Services | United Spirits | Laurus Labs | Dr. Reddy’s Laboratories | |||||||

| Shriram Transport Finance | Pidilite Industries | C.E. Info Systems | Happiest Minds Technologies | |||||||

| SRF Limited | Nippon Life India AMC | Kotak Mahindra Bank | ||||||||

| Star Cement | Punjab National Bank | Larsen & Toubro Limited | ||||||||

| Torrent Pharma | RBL Bank | Marico | ||||||||

| Max Financial Services | ||||||||||

| Info Edge | ||||||||||

| Strides Pharma | ||||||||||

| United Breweries | ||||||||||

| Vedanta | ||||||||||

Key economic events for the week:

| 24th Jan | 25th Jan | 26th Jan | 27th Jan | 28th Jan | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| USA | Manufacturing PMI (JAN) | USA | Consumer Confidence (JAN) | USA | Goods Trade Balance (DEC) | USA | Fed Interest Rate Decision | Japan | Core CPI | |||||

| Services PMI (JAN) | Home Sales (DEC) | FOMC Statement | Germany | GDP (Q4) | ||||||||||

| Japan | Services PMI (JAN) | Crude Oil Inventories | GDP (Q4) | |||||||||||

| Eurozone | Manufacturing PMI (JAN) | Jobless Claims | ||||||||||||

| Markit Composite PMI (JAN) | ||||||||||||||

| Services PMI (JAN) | ||||||||||||||

| Britain | Manufacturing PMI (JAN) | |||||||||||||

| Services PMI (JAN) | ||||||||||||||

| Composite PMI (JAN) | ||||||||||||||

What are you looking forward to the coming week? Share below ![]()