Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how, too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Trying to understand the tariffs

- Fast food, faster business

Trying to understand the tariffs

We sort of overdosed on the Trump stories towards the beginning of the year. Ever since, we’ve been trying really hard to ignore the noise coming out of the United States. But here we go again. Practically out of nowhere , India’s biggest trading partner has slapped us with a 50% tariff.

That’s a 25% “base tariff‘, with an additional 25% slapped on supposedly because we buy Russian oil. That “punishment” is something that we at Markets , at least, don’t get the logic of. We covered that one on a recent Who Said What , though, so we won’t repeat ourselves here.

The first 25% of those are already in force. Another 25% will kick in from August 27. Or they may not. Who knows.

Those tariffs, if they stick around, could practically close the world’s biggest consumer market to our exports. Enough has been written about what that means (here’s the latest we’ve seen), so we won’t repeat things. We’ll leave you with a couple of good charts from Bloomberg.

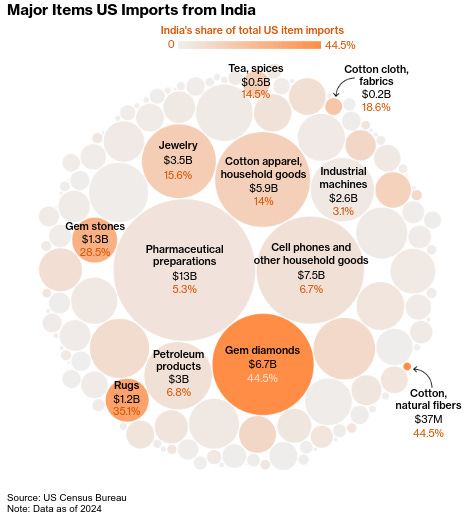

Here are our biggest exports to the US:

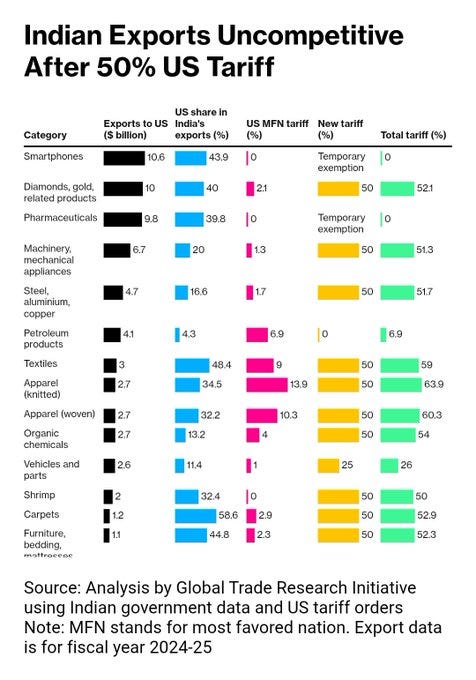

And if they’re tariffed, here’s what American importers will have to pay if they want to buy our goods:

From what we can tell, there’ll be some pockets of our economy — from shrimp exporters to carpet-weavers, who will see a short period of extreme pain.

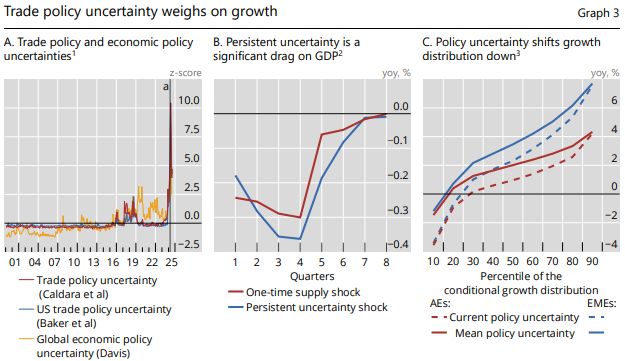

But to tell you the truth, this is a terribly confusing situation. It’s too extreme , and too sudden, for anyone to accurately tell you what might happen. We aren’t quite sure of how to even think of them. Thankfully, though, we’re starting to see rigorous research around what these tariffs are doing. Today, we’re going to look at two such pieces — a comprehensive bulletin by the Bank for International Settlements, as well as a paper by Ignatenko, Lashkaripour and others. It corroborates a lot of what we’ve said for a while.

The picture they paint is more complex than most people realize.

How economic pain spreads

How exactly do tariffs mess with an economy?

Obviously, they make imports more expensive. But that’s just the beginning: it’s the first stone cast into a calm pond. Once that is done, though, the waves that ripple outward.

For one, they create what economists call the “direct trade impact ”. When a country slaps tariffs on its imports, it chokes supply. People in that country see prices of imported goods shoot up, almost as if there was a sudden shortage of those things. That guts their “real wages” — that is, although their paycheck might stay the same, it buys fewer things.

How, precisely, this plays out can vary — depending on the margins businesses had, and how much more people are willing to pay. But this is bad timing. See, inflation is often a matter of what people believe . If people believe prices will go up further, they hoard on supplies, sending prices up. Meanwhile, businesses find people more tolerant of higher rates. As people lose sight of what prices “should” be — as these expectations become “unanchored” — this vicious cycle becomes increasingly hard to fight.

Many Americans never recovered from the post-pandemic surge in inflation. Their expectations weren’t anchored to begin with. When you add staggering tariffs, like the 54% on Chinese goods, that could derail those expectations severely.

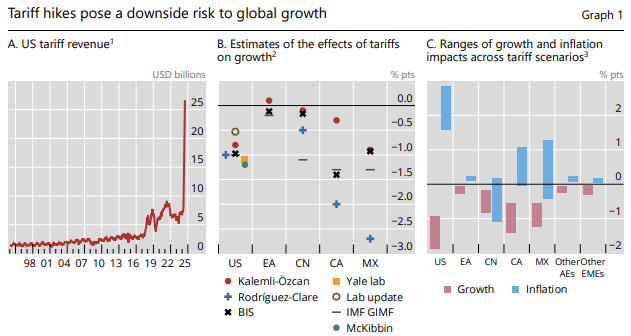

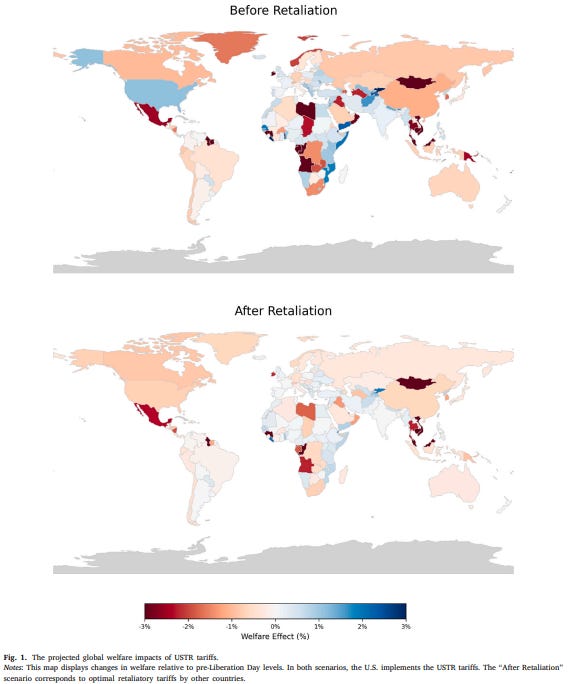

In the aggregate, the research points to one thing: the US, despite being the one imposing the tariffs, suffers the most . Although America’s tariff revenues quadrupled in July, that came at a cost: the country is modelled to take a growth hit of ~1% of GDP growth.

But things get more complicated from here. Once this plays out, three “indirect channels ” take over.

-

First , your supply chains break. Imagine you’re a car parts manufacturer — and the steel you need suddenly costs 25% more. Switching suppliers takes time. In the meanwhile, you might reduce production — but that creates bottlenecks for everyone that depends on you. These problems cascade through entire industries, creating shortages and price spikes.

-

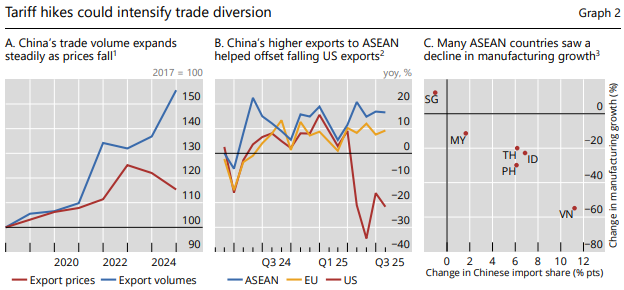

Second , the trade heading your way starts going elsewhere. This is already happening: Chinese exports to Europe and Southeast Asia have surged, while exports to the US have collapsed. This flood of diverted goods can depress prices in their new markets, hurting their manufacturers. Some ASEAN countries are already seeing their manufacturing struggle in the face of Chinese goods.

Source

- Third , there’s uncertainty, which is the one thing businesses hate more than high costs. When trade policies keep changing, when deals get made and unmade, companies freeze — unable to judge what risks are worth taking. They stop investing, delay hiring, and cancel expansion plans. This can damage growth as much as the tariffs themselves.

A tale of two economic worlds

This tariff story looks very different depending on where you live.

For advanced economies like those in Europe or Japan, things are probably more muted. They have diversified trading relationships, sophisticated markets, and the policy tools to respond. Coincidentally, these are also the very markets that have struck “deals” for lower tariffs.

But there’s a twist: Trump’s tariffs could actually be deflationary for these countries. Their economies will have to accommodate the produce of their own manufacturers, who will see lower export demand, as well as goods from other countries that are looking for a rich market. All of this could push prices lower.

Emerging markets face a much more complex picture.

On one hand, some will definitely look for opportunities in the debris of 50+% tariffs on countries like India and China. But they’ll also run massive risks.

So far, in a weird way, the trade tensions have actually been good for emerging markets. They pushed down the value of the dollar against other currencies. That was excellent news for many businesses in emerging markets, who had borrowed in dollars. As long as the dollar’s value stayed in check, this debt load was comfortable. But this isn’t a patch of good luck that you can trust. With so much chaos, you could easily see an abrupt reversal — pushing up the Dollar’s value, and putting massive pressure on those same borrowers.

If the tensions push an emerging market into a crisis, they could well be stranded. As the research shows, emerging markets often have less fiscal and monetary firepower to respond to shocks. If growth slows, they can’t cut interest rates or boost government spending the way advanced economies can.

Two countries, though, deserve special mention: Canada and Mexico .

These two countries face what economists call “stagflationary effects” that might be second, in scale, only to the United States. They were integrated deeply with the US economy for decades . Even as the tariffs have hit, diversifying away from American markets hasn’t been easy.

The global growth slowdown

Unlike a conventional war, which often has a victor, nobody wins a trade war. That’s what the research expects to happen this time around as well.

Even though some countries have reached bilateral trade deals, average US tariffs are likely to settle at levels unprecedented in the modern era. At the end of 2024, America’s average tariff rate was at 2.4%. The best deal it has now offered — to the United Kingdom — puts these at 10%. The rate on everyone else is even higher. At these levels, you should expect a meaningful drag on the global economy. If things escalate any further, some economies could be thrown into a full-blown recession.

We’re already seeing early warning signs. Recent US data indicates that people are spending less even as costs rise, and the economy is struggling to create jobs. Outside the US, meanwhile, consumer confidence has fallen in economies all across the world. Corporate earnings too are feeling the pinch.

This would have been a bad sign in the best of times. But even before this latest round of tariff escalation, global growth was already slowing. These latest tariffs have added an extra layer of disruption to an already fragile economic environment. are at

We haven’t seen the real damage yet. So far, the global economy has been remarkably resilient. As soon as the announcements were made, American companies frontloaded their purchases, rushing to stock up their inventories before tariffs hit. This resulted in a temporary boost to trade, masking the weakness beneath. That bump in trade may even have distorted near-term GDP figures.

But that exercise is already over. A lot of the “resilience” we’re seeing was on borrowed time. That time might be running out.

In its place will come a persistent “uncertainty tax” — where businesses stop making long-term decisions. In the past, the research suggests, this level of uncertainty shifted growth distributions downward by up to two percentage points. For many countries, that’s the difference between healthy growth and stagnation.

Financial markets: A double-edged buffer

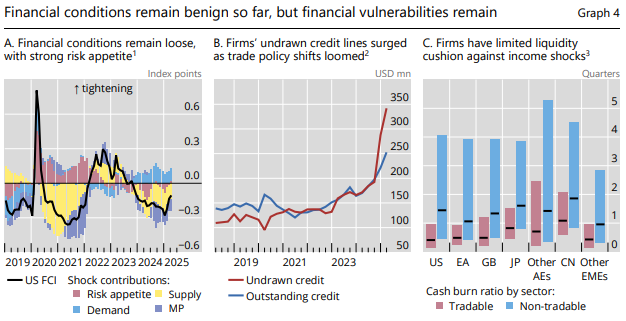

Through all this chaos, so far, financial markets have played the role of an economic shock absorber.

Financial conditions have remained remarkably accommodative throughout this trade tension. After the rout that followed April 2, Trump’s infamous “Liberation Day”, markets rebounded. The panic was short-lived. As trade tensions weakened the Dollar — even more money flowed into American markets.

This wasn’t dumb luck. All over the world, central banks were willing to keep financial conditions loose, in face of all the uncertainty. That created a large spout of money that could flow anywhere.

Many companies, too, reacted smartly to the chaos. Anticipating tariff impacts, many firms rushed to secure credit lines in late 2024. This gave them a “war chest” of liquidity that has helped them weather the initial storm.

But financial markets can be a double-edged sword.

For one, those liquidity buffers aren’t infinite. According toare at are at the research, firms in tradable sectors — that is, those that sell their goods or services across borders — could struggle to sustain operations for more than a quarter without new cash flows coming in. In many markets, firms in sectors exposed to trade are already stretched thin.

As balance sheets come under the risk of getting stretched, valuations remain high. A correction, now, could create serious problems — especially if banks decide to pull back on lending at the same time. Those stresses, in a worst case scenario, could ripple through the system. An acute shortage of money at one node of a supply chain could create cascading problems for anyone that does business with it.

The absolute worst case , however, will arrive if the world loses confidence in the dollar’s role as a global safe haven. That would create cracks in the entire edifice of dollar-based global finance. We won’t even pretend to know what might happen then.

Where does this leave us?

All the research we’ve looked at paints a picture of a global economy under pressure from many directions. India’s 50% tariffs aren’t coming in isolation — they’re part of a much larger, tangled web of trade disruptions, supply chain breakdowns, and financial vulnerabilities. The universe we’re heading into could be one where global employment contracts by 0.58%, hitting workers everywhere. In practical terms, that’s something like 21 million people that might soon be out of a job.

So far, circumstances have ensured that the blow is limited. Companies have been smart in planning their way through these tariffs — both in managing their inventories, and in ensuring enough liquidity. Financial markets have ridden through the chaos stoically. Phenomena like front-loading and dollar weakness have given them some breathing space.

But that resilience could easily flip. The resilience we’ve seen so far has been on borrowed time. The harsh truth is that trade wars don’t create winners. They only shift losses around. unless policy pivots toward stability rather than escalation, the global economy may soon discover just how difficult things can get.

Fast food, faster business

Remember that late-night Domino’s order when nothing else was open? Or that McDonald’s breakfast you had after partying all night long? Or the Burger King meal that somehow tasted better than you remembered? These brands are so embedded in our daily lives that we barely think about the companies running them, but maybe we should.

The businesses behind these familiar brands run extremely tight operations to ensure that every next meal you order from them feels just as delightful as the last. In their first-quarter results, we found a fun story about the economics and logistics of how these Quick Service Restaurants (QSRs) businesses fulfill the cravings of millions of Indians every day.

We’ll be specifically looking into the results of three such Indian companies: Jubilant FoodWorks which runs Domino’s, Westlife Foodworld which runs McDonald’s, and Restaurant Brands Asia (RBA) which runs Burger King and Tim Hortons.

Let’s dig in.

How do QSRs work?

On the surface, QSRs just seem to make food fast, serve customers quickly, and collect money.

But we know to never judge a book by its cover. Underlying this simple operation is a unique business model (called the master franchisee model*)* , and a mastery of supply chains and technology.

The master franchisee model

QSRs operate as master franchisees of the big brands you love. To use the famous names of brands like Domino’s and McDonald’s, these QSRs pay those brands an initial fee, and 5-6% of everything they make. In exchange, they get the exclusive right (or a master franchise) to operate these brands in India, along with all the recipes and global marketing power that comes with them.

Except for changing the logo or brand name, these QSRs have nearly full authority to grow these brand names in India however they choose — be it changing menus altogether to suit Indian tastes, or opening new outlets anywhere. But this great power doesn’t come without risks. If you win, the upside is yours. If you lose, though, you’ll have to bear the losses. And one of the biggest risks is that of location.

Imagine you’re a QSR that’s trying to expand your brand to new, tier-2 towns in India. Now, these locations are untested ground — you don’t know whether your outlet will succeed here or not. If it runs into losses, you want to be able to exit the location as quickly as possible and open somewhere else. In order to do that, you might want to rent your property instead of buying it straight up.

Property rent is a major cost item in the finances of QSRs, and can be the difference between success and failure. Pick the right location and you’re printing money, but pick wrong and you’re stuck paying rent on a dud for months. Here’s RBA outlining how important rent optimization is for them:

Farm-to-fork, at all costs

The promise of Indian QSRs lies in satisfying their customers as quickly as possible. And robust supply chains are a key part of ensuring that.

Every Maharaja Mac has to taste the same, whether you’re in Delhi or Chennai, and that requires serious logistics. For example, the vendor you source your expensive olive oil from has to be suitable for your menu, you should have enough cold storage facilities to ensure your vegetables are preserved well. And all this must be done profitably.

It isn’t always easy to do both, especially if both goals have tensions between each other. For instance, when tomato prices double during monsoons, these companies can’t just switch to something cheaper, or even pass on the higher prices to customers like us. They have to absorb the cost or risk disappointing customers.

How do QSRs resolve this? They try to use one stone to knock down two birds: lower costs, and have every item taste similar everywhere. The QSRs get a part of the cooking done beforehand by a central hub called a commissary kitchen . Here, the raw materials (like cheese and tomato) are converted into more complex ingredients for the outlets. The outlets mostly have to spend time assembling and putting the pizza into the oven, or deep-frying the chicken. This makes their cooking not just standardized across India, but also more efficient.

In the last decade, technology has helped streamline these supply chains a lot more. For instance, QSRs have automated large chunks of how customers order food now. Take McDonald’s, which has large self-serving kiosks at many Indian outlets. Or Domino’s which has its own mobile app and delivery tracking.

But this is just what you, the customer, get to see. In the back-end, QSRs rely on analytics to track not just where and what, but also when and how often customers order, and which customers need discounts . They also use data extensively to ensure their inventories never have shortages or excess supply, and plug other gaps in the supply chain.

Rent and supply chain investments aren’t the only heavy costs. Restaurants require a lot of manpower, which means spending a lot on salaries. Additionally, they have to face a lot of competition — the barriers to opening a restaurant are fairly low. As a result, profits are really hard to come by in the restaurant business. Even if a restaurant is profitable, the profits aren’t huge. The net margin of Jubilant, for instance, was 5.2% this quarter, while for Westlife it barely exists at 0.2%.

So, QSR businesses focus more on what they can control — their day-to-day operations. And that is usually represented by gross margins and EBITDA. But as we shall see, those metrics were a little out of control this quarter as well. The Q1 FY26 results of these companies show how even similar business models can produce very different outcomes.

Down to the numbers

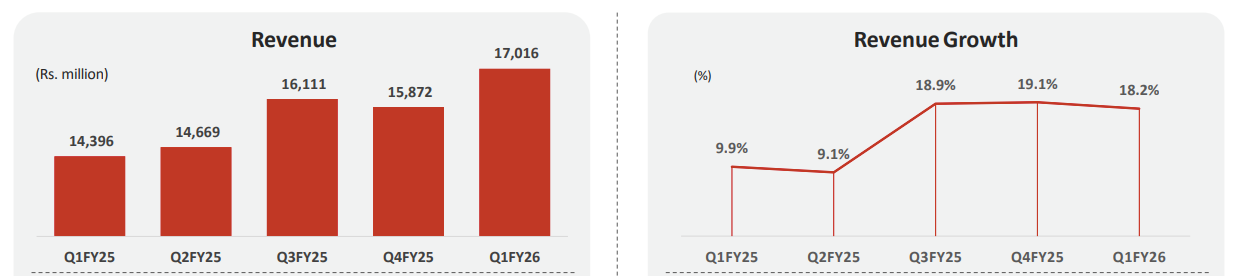

By far the largest of the three businesses, Jubilant FoodWorks ’ revenue grew a whopping 18% to ₹1,701.6 crores. People are ordering more, as volumes jumped over 17% from last year. Every day this year, the average sales across all their outlets was ₹85,396. They also opened 71 net new stores during the quarter.

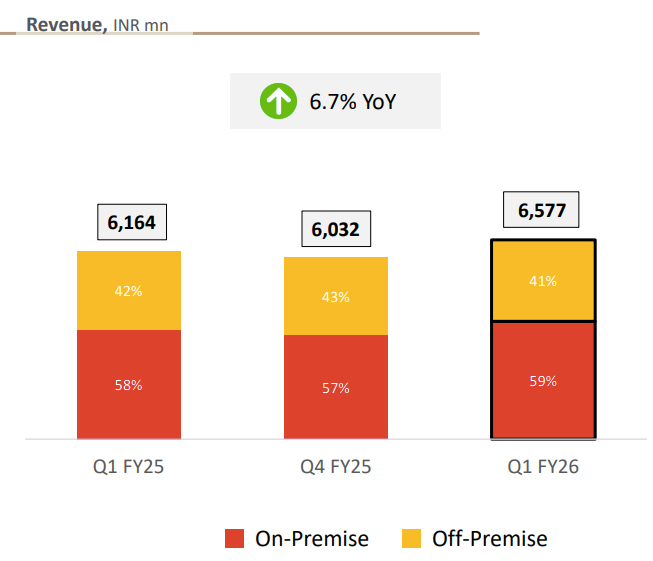

What’s really interesting for Jubilant is that most of their sales don’t come from in-store dining, but delivery — a whopping 73% of sales.

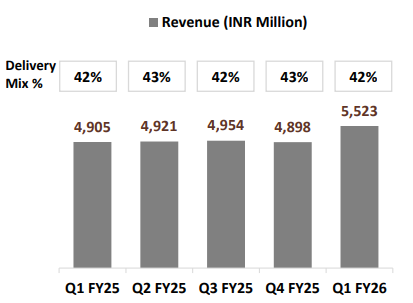

Westlife grew revenue about 7% to ₹657 crores by taking a more measured approach to expansion. They added 9 new McDonald’s restaurants but also closed 3 that weren’t performing well. Their dine-in and takeaway business grew 8% and now makes up about 60% of sales. The other 40% is food delivery — much lower than Jubilant.

RBA’s Indian operations are growing healthily with revenue up 13% to ₹552.3 crores. On average, each Burger King store generates a whopping ₹120,000 per day — higher than most QSR chains. They added 6 net new Burger King stores.

However, this expansion is proving very costly to them — in contrast to Jubilant and Westlife, they have been recording net losses for the last few years, losing ₹42 crores this quarter alone. The reason boils down to stiff competition — to gain market share in such a crowded market, Burger King India is selling their low-ticket, value-conscious meals a lot more than their premium items. This shows up in sales being higher, but margins being far tighter; even negative.

The slow growth of RBA’s more recently-started Indonesian business has also worsened their profitability. Revenue actually fell 6.9% from the last year. The average daily sales of Burger King Indonesia has been improving for nine straight months, but at a snail’s pace.

Raw revenue growth only tells part of the story. The real test of these businesses is whether their older, same-store sales — and not their new, less-mature stores — are actually better.

Same-Store Sales

Jubilant’s same-store numbers this quarter were the best among the three, recording 11.6% growth. Within that, however, their delivery business grew over 20%. Their core business model of getting pizza to your door got even stronger this quarter.

Westlife ’s same-store sales barely grew at 0.5%, but it’s their third straight quarter moving in the right direction. They launched a Korean-themed menu in March, expecting it to meaningfully impact next quarter’s results. McDonald’s affordable McSaver line is driving a major chunk of their dine-in.

However, even with positive same-store growth, each McDonald’s location is actually generating less money per year than before — down 3% to about ₹6.2 crores. Their stores in smaller cities or different formats aren’t as profitable as their established big-city locations. Moreover, locations in southern states are underperforming more than others.

RBA’s same-store performance grew merely 3%. Almost all of that growth came from dine-in rather than delivery. Much like Westlife, they are doubling down on Korean-themed menu items which are already showing results for them.

The real question, however, is how does growth in same-store sales translate to actual profits?

Profits hide, restaurants seek — harder

Jubilant, like other companies, faced the brutal reality of cost inflation. Raw material costs exploded 28% year-over-year — everything from cheese to flour to chicken got significantly more expensive. And instead of passing these costs entirely to customers, they chose to absorb much of the impact.

This put pressure on their margins, with their EBITDA margin compressing to 19.0% from 19.3%. They hope that by not raising prices, they gain more market share. Plus, Jubilant has been cleaning up their portfolio by removing loss-making lines like their Russian operations.

Westlife , on the other hand, didn’t hurt from cost inflation as much. If anything, they actually made more money while everything around them got more expensive. They managed to cut their food costs from 30% down to about 28% of sales. How?

Well, the biggest reason their management states is that their supply chain — including how they procure raw materials for burgers — became more efficient in the long-term, but they don’t fully elaborate how . The margins were also propped up by a small price raise in March, but the increase wasn’t too big to deter repeat orders from customers. Their EBITDA margins remained relatively more stable at 13%.

RBA’s Indian arm saw their EBITDA margin go up to 4.1% from 3.6% — already a measly range compared to its peers. They added ₹10 crores in employee expenses during the quarter to train staff to help customers navigate self-ordering systems and manage more complex operations. They also absorbed ₹7 crores in one-time costs from closing 5 underperforming stores in India, while also investing in new stores as we mentioned earlier. And they’re hoping that these expenses pay off in the future.

Bottom line

Success in the restaurant business isn’t just about making good food anymore. It’s about making tough choices — where do you open? When do you shut a loss-making store? Do you expand aggressively or play it safe? Do you invest in fancy technology or focus on getting the basics right?

In an industry where one bad restaurant location can drag down results for years, and one viral menu item can boost sales for months, these strategic choices will likely determine who comes out ahead as India’s food delivery and dining market keeps evolving.

Tidbits

- Just two months after India’s solar surge pushed power prices near zero, a correction has arrived. The MNRE has confirmed curbs on solar output to stabilize the grid. Rajasthan, the top solar state, saw curtailments as high as 48% during peak hours , erasing nearly $26 million in developer revenues since April , according to NSEFI. Heavyweights like Adani, Tata, and AWS are directly hit.

Source: Reuters

- OpenAI has rolled out ChatGPT Go , an India-only subscription plan priced at ₹399/month ($4.57) — its cheapest offering yet. The move targets India’s nearly 1 billion internet users , making advanced AI more accessible in one of its fastest-growing markets.

Source: Reuters

- Reliance Consumer Products has acquired a majority stake in Naturedge Beverages, the firm behind the zero-sugar, herb-based Shunya brand. The strategic move strengthens Reliance’s health-focused beverage portfolio—already including Campa, Sosyo, Spinner, and RasKik—to tap growing demand for sugar-free drinks.

Source: Economic Times

- India’s state-run telecom company MTNL has defaulted on loan repayments of ₹86.6 billion—covering ₹77.9 billion in principal and ₹8.65 billion in overdue interest—to seven public sector banks. Total debt has now risen to ₹345.8 billion, highlighting mounting financial distress in the increasingly uncompetitive telecom firm.

Source: Reuters

- This edition of the newsletter was written by Pranav and Prerana

Join our book club

Join our book club

We’ve started a book club where we meet each week in JP Nagar, Bangalore to read and talk about books we find fascinating.

If you think you’d be serious about this and would like to join us, we’d love to have you along! Join in here.

Have you checked out The Chatter?

Have you checked out The Chatter?

Every week we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Go check out The Chatter here.

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()