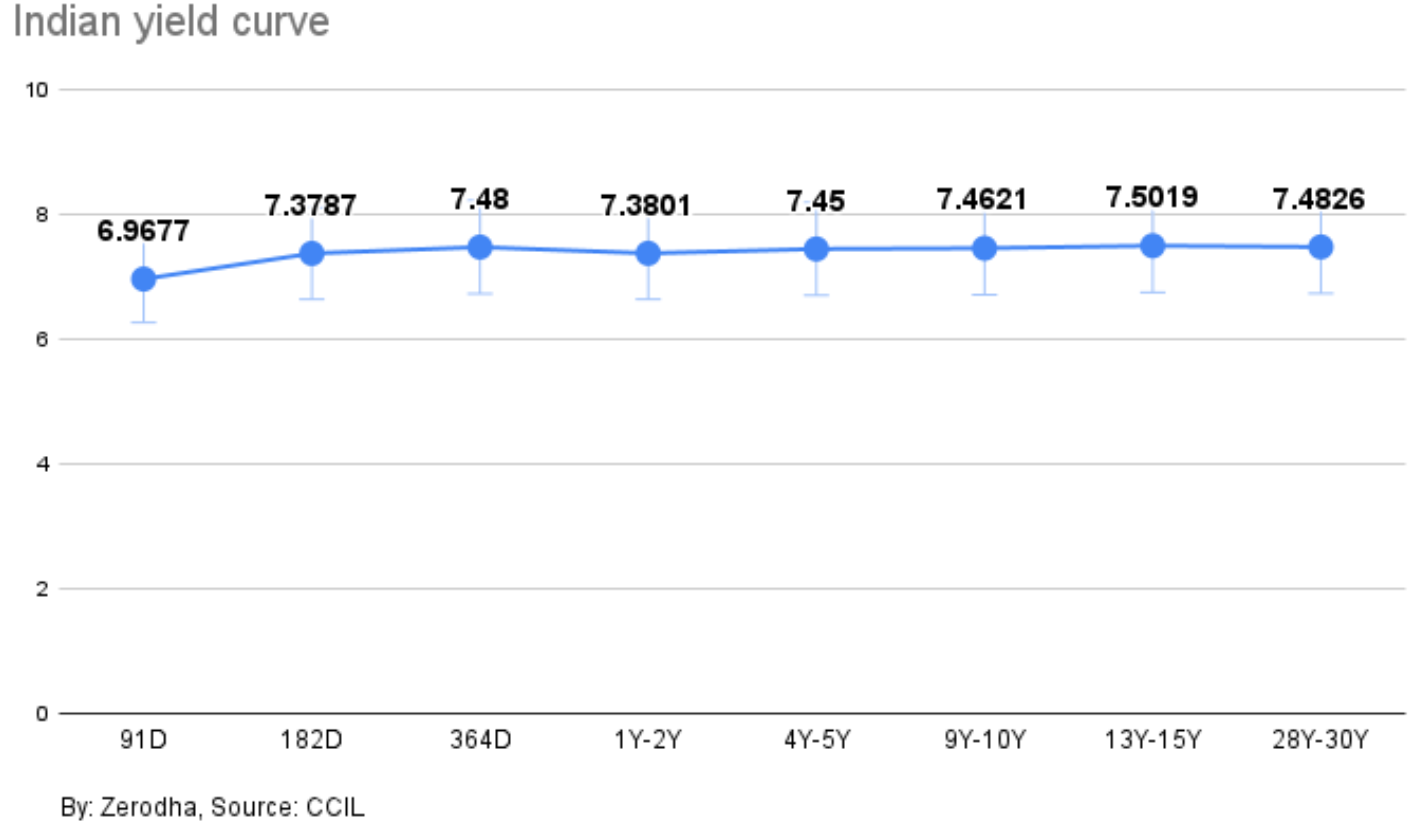

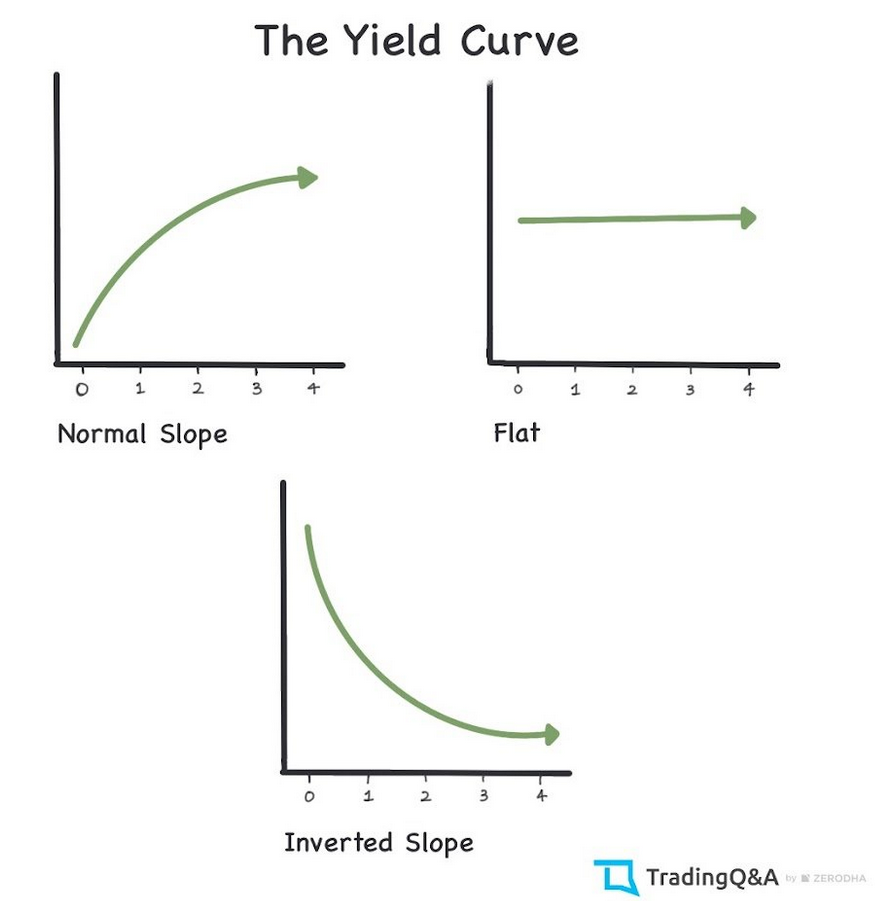

The Indian government bond yield curve is currently inverted. In normal times, a yield curve is upward-sloping. The shorter maturity bonds will yield less compared to the longer maturity bonds.

When a yield curve inverts, short-term bond yields are higher than long-term bonds.

Why does this matter?

In the US, inverted yield curves have predicted almost all recessions since 1955 (shaded regions) with a lag of 16–20 months.

At present, the entire US yield curve is inverted. People assume that it might happen in India too.

So will there be a recession in India?

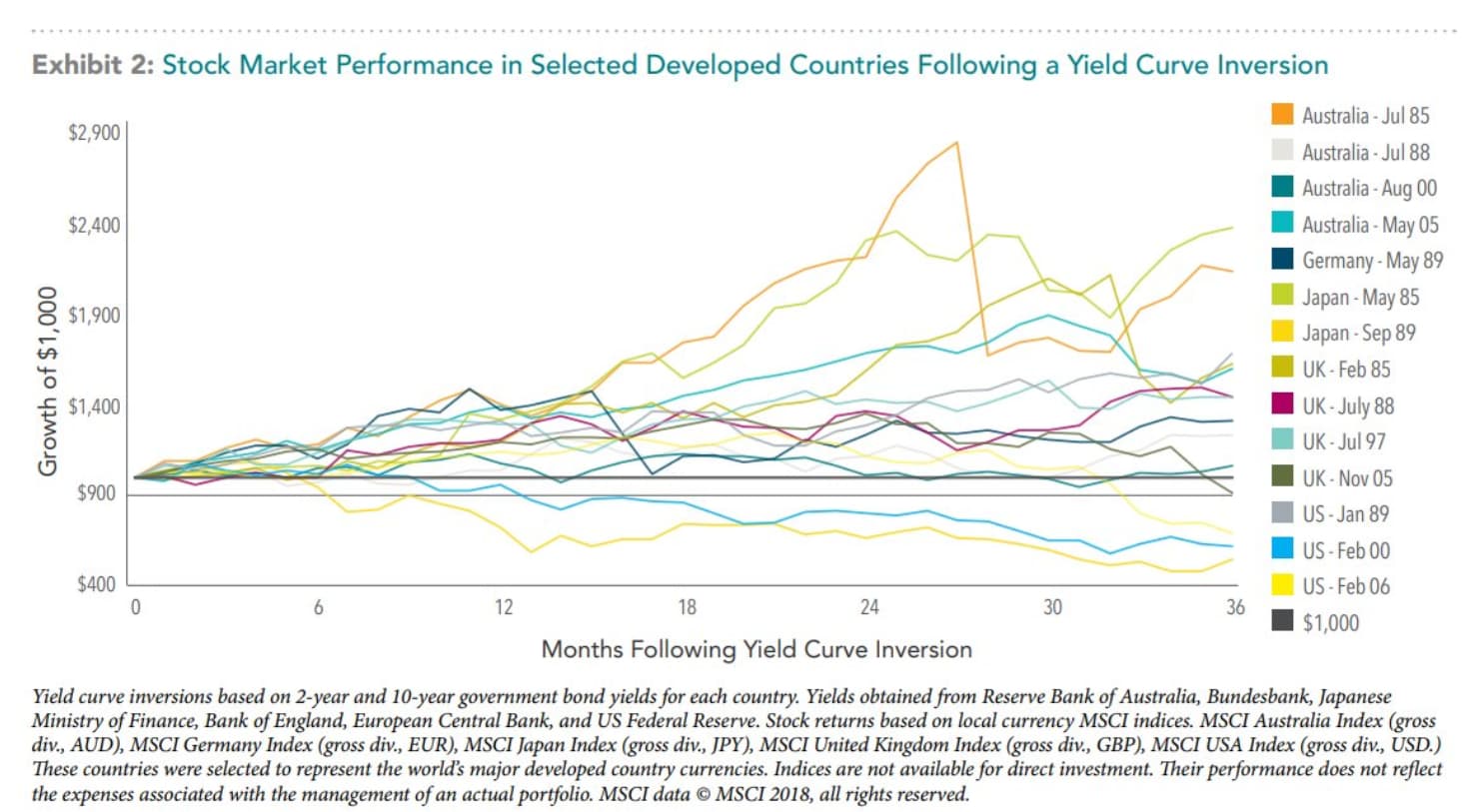

The evidence of inverted yield curves in predicting recessions outside the United States is mixed. Dimension Funds looked at five developed markets outside the US since 1985. As you can see, the evidence is mixed at best.

Another study of the US and 11 other developed markets by Eugene Fama and Ken French found the same.

"We find no evidence that yield curve inversions can help investors avoid poor stock returns. "

So, are yield curves useless?

No. Yield curves shouldn’t be seen as “yes” or “no” indicators of recessions.

The long-term yield is a combination of short-term interest rate, the expected future short-term interest rate, and the term premium.

So, the shape of a yield curve reflects the future economic prospects and inflation expectations. An upward-sloping curve implies strong economic growth and hence higher inflation. So, investors demand a higher yield.

Conversely, a flat or inverted yield curve signals future economic growth prospects are weak, and by extension, lower inflation and interest rates.

Yield curves shouldn’t be seen in isolation and must be considered with other data points to get a sense of growth expectations.

Most importantly, yield curves are lagging indicators. They cannot and should not be used to time investments if you are a long term investor.

You are better off ignoring the noise and investing.

Additional reading

https://www.rbi.org.in/Scripts/BS_ViewBulletin.aspx?Id=21066