Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- India’s food regulator just changed how it works

- The world’s most common metal is in short supply

India’s food regulator just changed how it works

If you’ve ever run any kind of food business in India — be it a restaurant chain or even a small sweets shop, or packaged food — you know what it takes to get a licence from FSSAI.

Every few years, you’d gather documents, pay fees, fill forms, wait for inspections, and hope nothing fell through the cracks. And it doesn’t get easier with each renewal — you have to go through this trial by fire every single time. But if you miss the renewal window, you’re basically operating illegally.

But maybe, this grind won’t have to go on much longer.

Recently, on March 10th, the government notified new amendments to FSSAI’s licensing regulations, which came into force the very next day. The change is monumental: from now on, food licences and registrations have perpetual validity. Once you have a licence, you keep it unless you violate the rules.

These changes are part of a broader government push away from compliance and paperwork-heavy regulation towards better oversight that concentrates on businesses that pose the most actual danger. Inspections will now be prioritised based on the type of food product, past compliance record, and performance in third-party audits.

However, while it might speed things up, whether it actually makes India’s food safer is a different question.

What FSSAI is and why it exists

Let’s roll the time machine 2 decades back.

Before 2006, food safety in India was governed by at least eight different laws spread across multiple ministries with no coordination. Spices fell under one law, meat under another, and packaged food under a third. There was no single standard and no single authority that could be held accountable.

So, the Food Safety and Standards Act of 2006 created a body called FSSAI to fix this. One body that abides by one framework and issues one 14-digit number that every food business must display.

However, FSSAI began functioning in 2011 — five years of the old fragmented system continued mostly unchanged. It basically inherited a heavy burden. After all, it had to now bring crores of food businesses — manufacturers, restaurants, caterers, cloud kitchens, etc — under a single umbrella for the first time.

How the old licensing worked

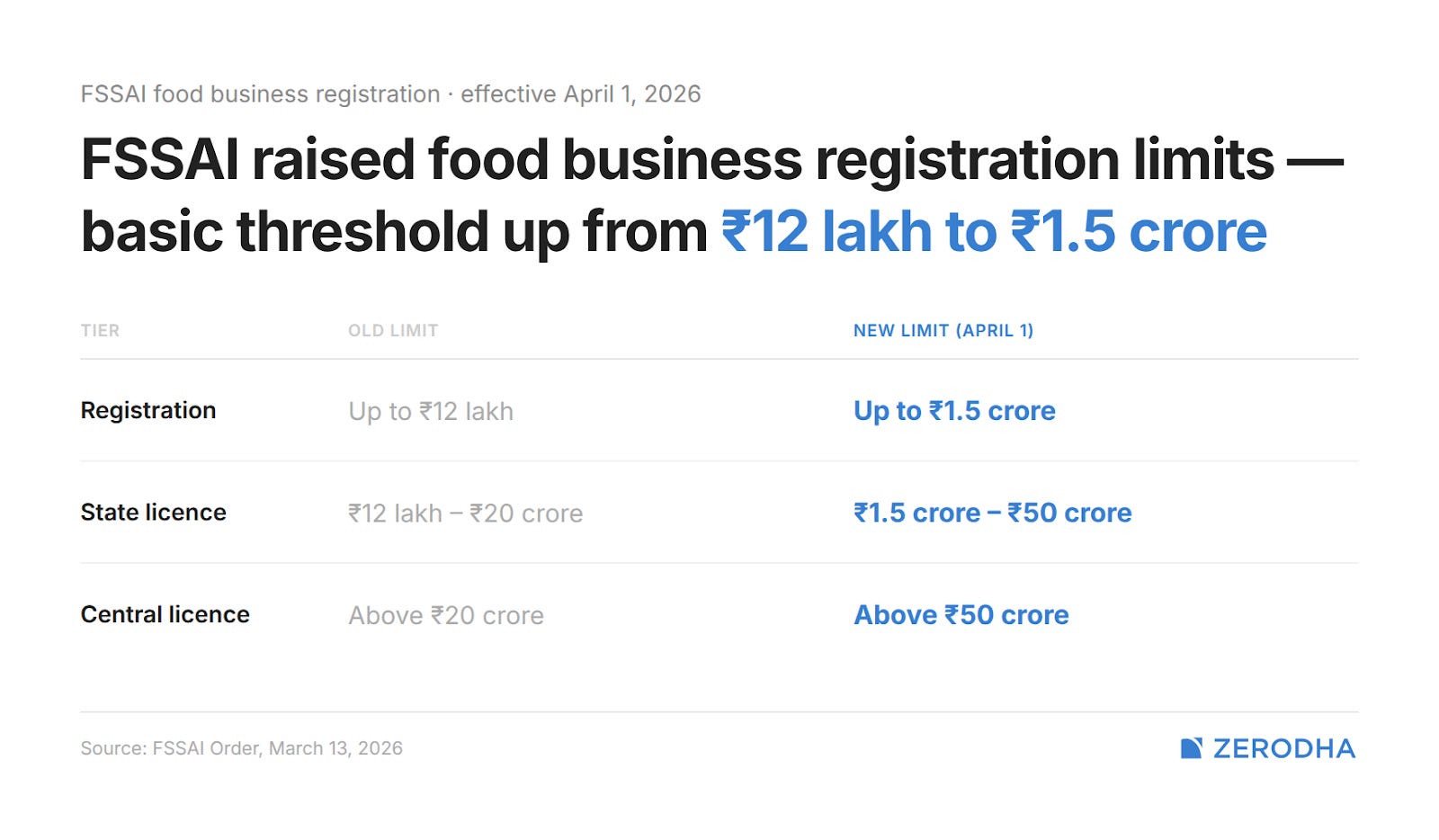

Every food business in India needs either a registration or a licence from FSSAI depending on its size, and the system works in three tiers.

The smallest operators, like your neighborhood golgappa stall, juice cart, or a sweet shop, need basic registration, which, until now, applied to firms with annual turnover up to ₹12 lakh.

The process was entirely online. You fill a form, submit basic documents like identity proof and address proof, pay ₹100 per year, and get your 14-digit ID — normally without having your establishment inspected. FSSAI can order one at its discretion, but most small operators get their registration without anyone visiting their premises. The new reform removes pre-inspection requirements for micro and small businesses entirely.

But whether that’s necessarily a welcome move was up for debate.

See, the thought behind this rule might have made intuitive sense. A small local operator has limited reach, while a large manufacturer distributing nationally poses the bigger public health risk. However, it’s these very small informal food operations that are far more likely to use unhealthy, adulterated practices — like using loose oil, unpackaged ingredients, and open preparation.

Then, we move to medium-sized businesses, which need a state licence. That comes with a mandatory inspection. Manufacturers holding state or central licences must also test their products at an NABL-accredited laboratory every six months and upload results to FSSAI’s portal.

Lastly, you have the largest operators, like multi-state businesses, importers, and large dairy units, get the most scrutiny, being subject to detailed documentation, periodic testing, and FSSAI’s targeted national surveillance campaigns. Under the new reform, this tier of businesses can be ordered at any time at any time to get externally audited by a third-party at their own cost.

Even here, being large and licensed is not a guarantee of safety.

For instance, in 2024, Hong Kong and Singapore banned spice products from MDH and Everest after detecting ethylene oxide, a carcinogen, in their products. FSSAI’s own domestic tests found no traces, but an investigation by Scroll found that Indian food safety norms don’t even require ethylene oxide testing in spice mixes. It took foreign regulators testing export products to flag something being sold to Indian consumers for years. This test was never even part of what FSSAI considered a necessary health standard.

What the reforms actually change

Three things changed with the recent notification.

The first, most important is perpetual validity itself. The licenses remain valid indefinitely unless the Authority suspends or cancels them for a violation. This removes the renewal deadline that both food businesses and inspectors navigated.

What that also means is that now, inspectors have much less leverage to demand illegal payments from food businesses to fast-track inspections. Many reports document the existence of bribes demanded by local food inspectors which determined whether you got inspected at all. In 2024, the CBI caught an FSSAI assistant director taking a bribe red-handed. The raids uncovered assets worth ₹1.8 crore that his salary could never explain.

Meanwhile, manufacturers with state or central licences still have to file annual returns by May 31st each year and pay their annual fee. The licence is automatically suspended on missing these requirements.

The second change is related to the revenue thresholds. Basic registration now covers businesses with annual turnover up to ₹1.5 crore at the same ₹100 annual fee — a 12-fold jump from the previous ₹12 lakh limit. State licences now apply up to ₹50 crore, and only businesses above that need a central licence. For manufacturers previously holding central licences who fall below the new threshold, this means dealing with the state authority rather than FSSAI’s Delhi headquarters — simpler oversight, less paperwork.

Third, street food vendors registered with municipal corporations or town vending committees will now be treated as automatically registered with FSSAI. This would benefit over ten lakh vendors who previously had to maintain two parallel registrations for the same business.

However, this rule is dependent on having a Town Vending Committee, or an able municipal corporation to begin with.

What do we mean by this? See, the new reform only helps vendors already registered with their municipal body. But municipal bodies have always had incentives to keep vendors unregistered — they were easier to evict and extort illegal payments from. So those who weren’t registered, like your coconut water vendor or tapri wala , remain as invisible to the regulatory system as before.

Similarly, since 2014, city governments were required to set up Town Vending Committees — bodies that survey vendors, issue vending certificates, and designate vending zones. A Parliamentary Standing Committee found that only 31% of eligible towns had actually done this. Without this committee, vendor registration itself becomes difficult.

The part that’s harder to answer

What this reform mostly proves is that compliance and food safety are not the same thing.

See, compliance measures whether a business has interacted correctly with the regulatory system. It says nothing about what is actually in the food. A business can be fully compliant and still be selling adulterated food.

The only mechanism that answers that question is testing. It is where India’s food safety system has its deepest structural problems. None of that changes with perpetual validity or a revised revenue threshold, even with beloved household brands like MDH and Everest.

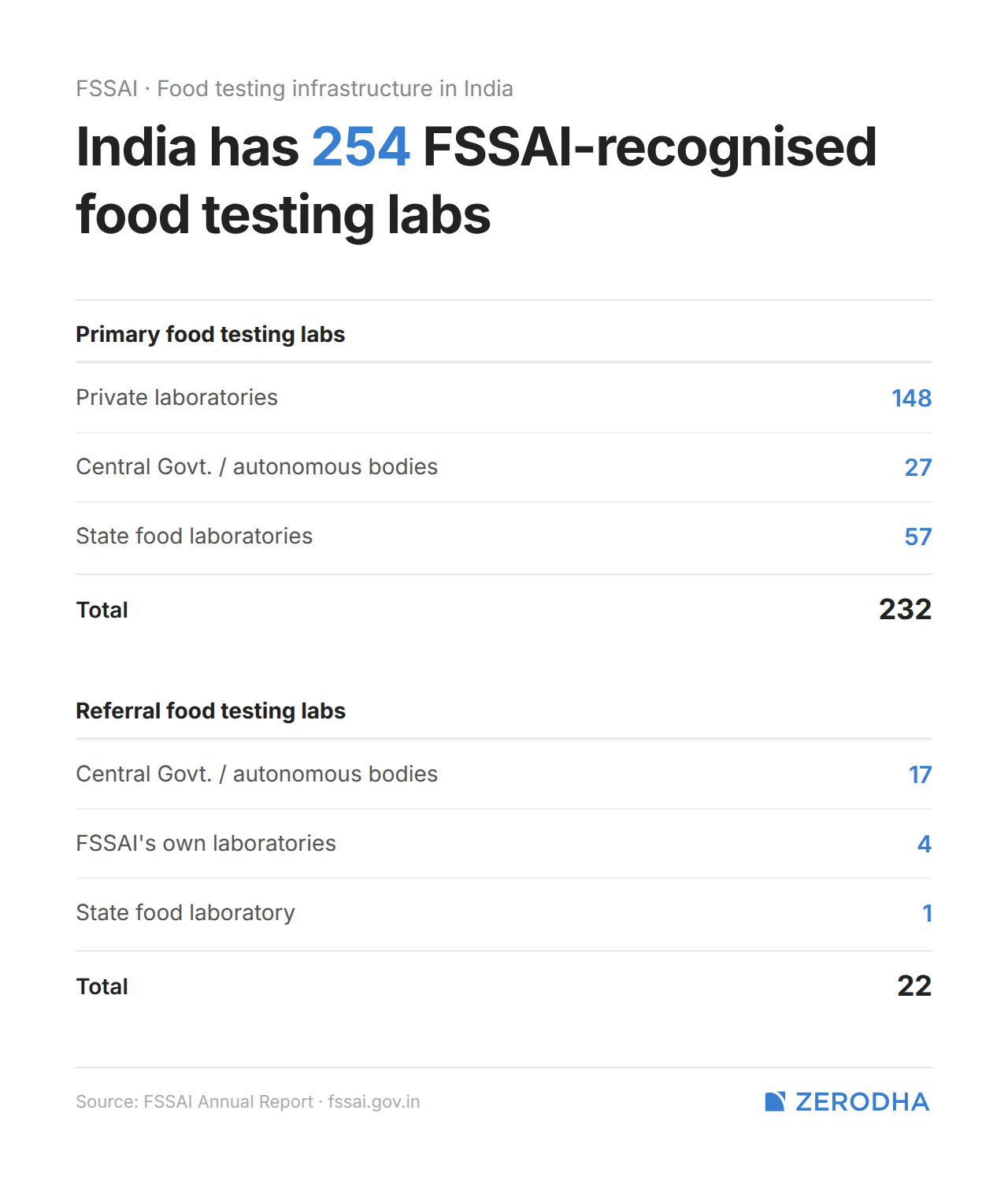

And the testing infrastructure is genuinely thin. State food laboratories lack equipment for heavy metals, pesticide residues, and microbiological parameters — precisely the tests that catch the most dangerous adulteration. FSSAI’s total lab network for the entire country is 232, while the other 22 are referral food testing labs. Testing backlogs mean samples often sit for weeks after the food has already been eaten.

A dire inspector shortage only worsens this. As of 2021, there were only 2,531 Food Safety Officers across the country for roughly one crore food businesses, against the government’s own guideline of one FSO per 1,000 businesses. Vacancy rates ran between 33% and 90% across states. The reform shifts to risk-based inspection, but risk classification happens inside the same understaffed state departments.

Meanwhile, between 2018 and 2022, FSSAI revoked just 1,225 licences across the entire country. That’s a fraction of 1 crore. In a weird reversal of the famous Dettol statistic, 99.96% of businesses, including many caught violating standards, faced no permanent consequence.

Conclusion

In 2021, FSSAI announced perpetual licences for restaurants and food manufacturers conditional on annual returns — it didn’t scale. The 2026 reform has the weight of a government committee behind it, but the enforcement infrastructure is essentially unchanged.

The reform’s logic is sound in the places it applies. Freeing FSSAI from renewal administration is valuable if that bandwidth moves toward enforcement. Simplifying compliance for small operators who were never really being supervised anyway acknowledges ground reality. Eliminating duplicate registration for ten lakh street vendors removes bureaucratic overlap.

But India’s poor testing infrastructure could potentially bottleneck the otherwise-welcome shift to risk-based inspection. Filling inspector vacancies, building lab capacity, setting standards that actually catch what’s dangerous, and revoking licences on time — all of this has been pending for fifteen years, and might only last longer.

The world’s most common metal is in short supply

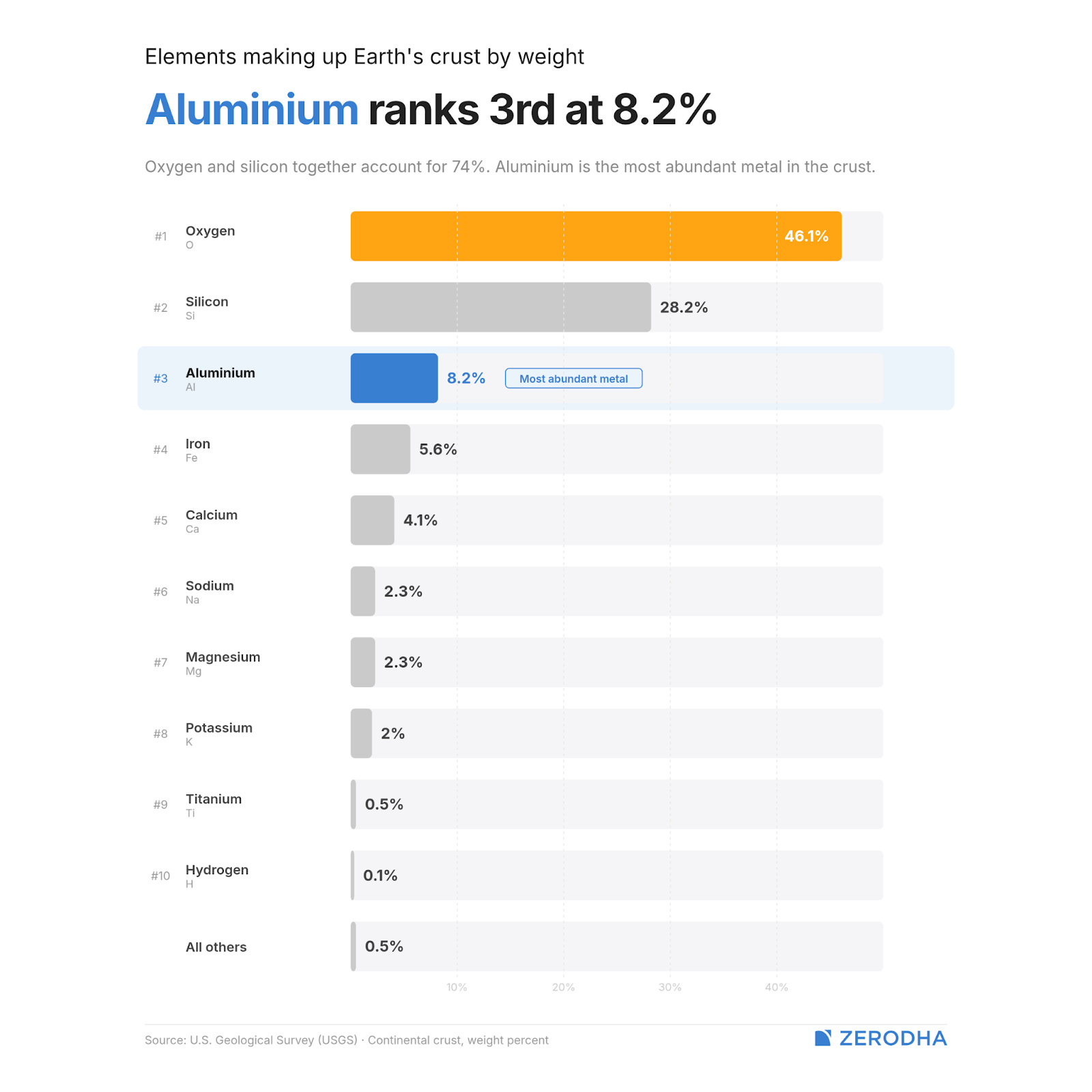

Aluminum is the most abundant metal in the Earth’s crust. It makes up 8% of the weight of the rocky surface of our planet; more than any other metal. It is found as part of a rock called bauxite, and global bauxite reserves stand at around 29 billion tonnes — enough to sustain current production for centuries.

And yet, in early 2026, Aluminum prices have been skyrocketing, and the problem is not enough supply .

You see, the global aluminum market has a peculiar shape. China sits at the centre of it — producing about 45 million of the world’s 72 million tonnes, while consuming roughly 60% of global supply. It’s both the world’s aluminium factory and its aluminium sink. China doesn’t export much primary aluminum — it uses most of what it makes. It does, however, export semi-finished products — sheets, extrusions, foils — in record quantities, to factories across Asia, Europe, and Africa.

Everyone else arranges themselves around China. Canada supplies the US (which imports about two-thirds of its aluminum), mostly from across the border). Russia’s metal historically flowed to Europe, until sanctions began redirecting it to Asia. The Middle East — Qatar, Bahrain, UAE — built smelters on cheap gas and sell to both Europe and Asia. India produces more than it consumes and exports the surplus.

But in 2026, while demand was growing steadily, Aluminium prices were running haywire. In early January, the London Metal Exchange benchmark crossed $3,000 per tonne for the first time since 2022. By the end of the month, it was already circling the $3,300 mark. It dipped briefly afterwards, as traders took profits, but by March, prices started soaring again as prices shot past $3,500. Citi has warned they could hit $4,000 if disruptions persist.

But why is this happening?

Aluminium follows electricity

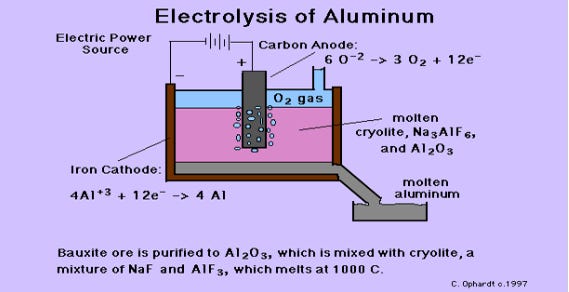

In nature, aluminum is always stuck to oxygen, bonded extremely tightly. The only way to pull them apart is with electricity. You melt the oxygen-laden metal in a special chemical bath at about 960°C and then force a massive electric current through it. The current rips the oxygen away. Pure molten aluminum, heavier than the liquid sinks to the bottom and gets siphoned off.

This is called the Hall-Héroult process. The process, invented in 1886, is still the only way we can make aluminum. From Jharsuguda to Iceland, every tonne of aluminum in the world comes from the same process.

Source- EduMission

There’s one problem with this centuries-old process: it uses an immense amount of electricity.

Every tonne of aluminum takes roughly 14 megawatt-hours of electricity to make. That is, roughly, the amount of electricity 12 Indian households use through a year. To someone in the business of making the metal, this shows up as massive power bills: as much as 30-40% of their total cost.

And a smelter cannot be turned off. If you ever cut the power, that 960°C bath starts to solidify, creating a frozen lump of rock that can destroy the entire pot. Restarting, then, takes months — if it’s at all possible.

So smelters aren’t built where aluminum is needed, but where electricity is cheap, abundant, and uninterrupted. That’s why Iceland, despite zero bauxite reserves, is one of the world’s top aluminium producers. It has mighty waterfalls which produce a continuous stream of cheap electricity, some of which is used to make aluminium. You see something similar in other parts of the world with abundant hydroelectric power — like Quebec, Norway, and Russia.

On the other hand, China and India use coal plants for their smelters. We’ll come back to this later.

So why are prices soaring?

Prices are always a question of demand and supply. For aluminium, the demand side of the equation is sedate: growing at a steady-but-not-incredible 2-3% a year. But the supply, after twenty years of reliability, has seized up — sending prices roaring.

China hit the ceiling.

For decades, when aluminum prices rose, China would build more smelters. This would place a ceiling on how far prices could rise.

An employee working in an aluminium factory in Zouping, Shandong province, China.

But in 2017, Beijing put a stop to this, capping annual capacity at 45 million tonnes. In just the preceding fifteen years, Chinese output had grown ten-fold, from 4 million tonnes in 2002 to over 40 million by 2017. Increasingly, this industry was eating up an unsustainable amount of its coal-fired electricity. Meanwhile, its cheap aluminium output had put it at odds with the US and Europe, who alleged that it was dumping its excess aluminium on the rest of the world for cents on the dollar. It would reaffirm this decision in its 2025-2027 Action Plan.

In early 2026, China has come within touching distance of that 45 million tonne cap. Goldman Sachs notes that although the plant managers can squeeze out a little above the cap, we’re past the era where China would always scale up to meet global demand. New smelters can only be approved, now, if old ones are decommissioned first.

Chinese companies are still trying to find work-arounds. For instance, Chalco, one of the world’s largest aluminium producers, is trying to build an aluminium smelter in Indonesia. But the project is riven with higher costs and local barriers. They’re nowhere close to China’s efficiency.

Smelters shut down across the world

Meanwhile, many other things have gone wrong at the same time.

The first, as with so much we’re writing on these days, is the war in Iran. The Persian Gulf, apart from being a hub for energy products , is also lined with industries that need cheap energy — including aluminium. But as the war escalates, these industries have started feeling the pressure.

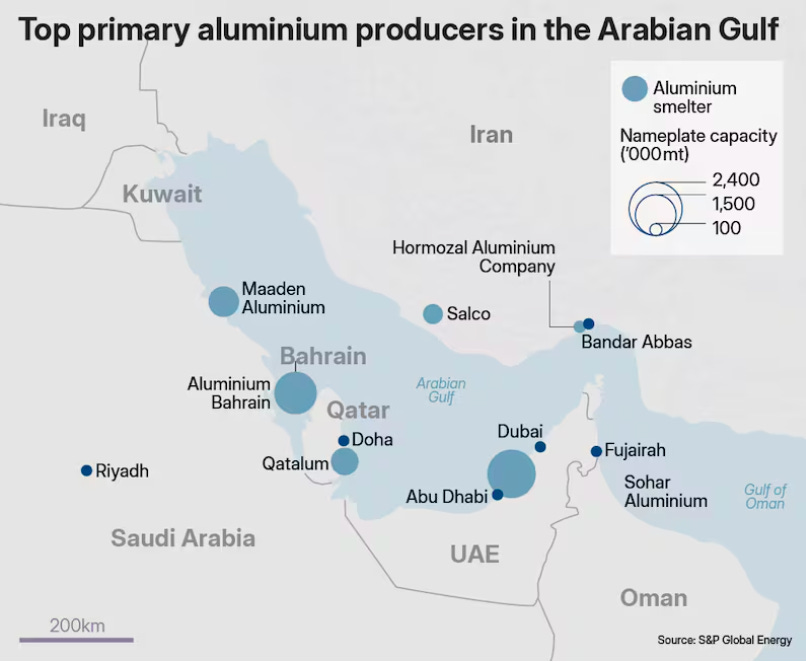

The Gulf, UAE, Bahrain, Saudi Arabia, Qatar, Oman, produced about 6.2 million tonnes in 2025, roughly 8-9% of global output. That sounds modest, but the Gulf punches above its weight because nearly all of that metal gets exported to Europe, Japan, Mexico, and across Asia. It’s one of the world’s most important sources of seaborne aluminum. And all of it flows through one narrow waterway, you guessed it, the Strait of Hormuz.

On March 2, Iranian drone attacks hit QatarEnergy’s facilities, forcing it to halt LNG production entirely. Qatalum, which runs on gas from the same system, began a controlled shutdown the next day. It has since stabilised at 60% capacity on reduced supply — but full restart timing is unknown. Aluminium Bahrain (Alba), the world’s largest single-site smelter at over 1.6 million tonnes a year, declared force majeure too — not because it stopped producing, but because with the Strait closed, it can neither export finished metal nor receive raw alumina.

The war added additional stress to a market that was already stretched. Even before the war, Europe had decided to cut itself entirely off Russian aluminium, as part of its 16th sanctions package. Meanwhile, major smelters across the world were shutting down for unrelated reasons. For example, one of Africa’s largest smelters, the Mozal smelter in Mozambique, was wound down because power prices made it unviable. Meanwhile, Iceland’s Grundartangi smelter cut output by two-thirds after a major equipment failure.

Then, there’s AI

Even where capacity does exist, making aluminium has recently become more expensive. And the culprit, strangely enough, is artificial intelligence.

Smelters are built where electricity is cheap. Until recently, if you were trying to set a smelter up, you’d try finding a deal to lock up electricity supply for the next couple of decades at $25-40 per MWh.

Only, those deals are becoming harder to find. A new type of customer is looking for the same cheap electricity, and their war-chests dwarf anything the aluminium industry can manage.

Microsoft, for instance, committed $80 billion to data centre buildout in fiscal 2025. Amazon, Google, and Meta are spending at comparable scale. Like smelters, these data centres need 24/7 uninterrupted baseload power, guaranteed for years. Only, they’re willing to pay thrice as much for it, at $80-115 per MWh.

Sometimes, this transition is direct. Last month, for instance, Century Aluminum sold its Hawesville smelter in Kentucky — the second-largest in the US — to TeraWulf, a digital infrastructure company. With energy costs rising, the plant was no longer viable. As a data centre, however, the site was more promising.

Expect this to continue. According to the IEA, global data centre electricity demand will more than double in the next five years, from 415 TWh in 2024 to 945 TWh by 2030. This build-out will be clustered in a few parts of the world. By 2030, the US will use more electricity processing data, alone, than manufacturing all energy-intensive goods combined .

What does this mean for India?

India is the world’s fourth-largest aluminum producer. We make about 4.1-4.2 million tonnes of it a year: led by companies like Vedanta, with an output of ~2.4 million, or Hindalco, with ~1.3 million.

Of that, just 2.3-2.4 million tonnes is consumed here itself. The rest is exported abroad. Right now, these rising global prices are a tailwind. For instance, NALCO’s profit surged 77% YoY in the first quarter of FY26. Hindalco, too, posted a 30% jump in consolidated net profit.

Over time, however, two forces may start working against India.

First, we have a coal problem. Nearly all Indian smelting runs on coal. A coal smelter produces 16-20 tonnes of CO₂ per tonne of aluminum; a hydro-powered one emits 4-5 tonnes.

Until recently, the world didn’t price that carbon, which is why the difference didn’t matter commercially. In January 2026, however, the EU fully implemented its Carbon Border Adjustment Mechanism (CBAM). Their aluminium imports from India, now, are taxed based on how much carbon went into making them. This is a penalty that aluminium smelted in Norway, for instance, doesn’t have.

Because of this penalty, we can’t capture the premium that the world’s most lucrative markets offer. The big four companies in this space, Vedanta, Hindalco, NALCO, and BALCO have committed $5 billion toward 20 GW of renewable energy by 2030. But that’s a long way to go.

The consumption gap. As India develops, our aluminium needs will only grow. At the moment, India uses just 2.5-3 kg of aluminum per person. Compare that to China, where the average person uses 12-14 kg, or the West, where consumption nears 25-30 kg per person. We will get there too; as India builds metros, airports, grids, housing, and EVs, the demand for aluminium will surge. According to estimates, our needs will grow 7-8% a year.

So will prices cool down?

The ~$3,500 mark, as far as we can tell, is unlikely to be a new floor. Some of what’s happening right now will reverse, while those prices will tempt others to ramp up supply.

But structurally , the market is hitting some hard constraints.

And the underlying demand is only growing. The International Aluminium Institute projects global demand will rise by an additional 33 million tonnes a year. The biggest pull comes from EVs and transport, followed by the electrical sector — solar, wind, grid upgrades.

But the current events upset the rhythm of the last 20 years. China, for instance, appears to have no intention of lifting its production cap. Data centres will keep outbidding smelters for electricity over the next few years. Carbon taxes will continue to penalise smelters run on fossil fuels.

Tidbits

- The Delhi High Court turned down SpiceJet’s offer to deposit immovable property worth ~₹148 crore as security in lieu of paying ₹144 crore owed to former promoter Kalanithi Maran. However, it granted a four-week extension to make the cash deposit — a limited reprieve for an airline that has openly acknowledged a liquidity crunch.

Source**: Economic Times** - Standard Chartered settles SEBI case over FPI lapses for ₹57.20 lakh. The bank, acting as a Designated Depository Participant, allegedly failed to report delays of over six months in beneficial ownership changes for certain FPIs and improperly granted disclosure exemptions.

Source: Economic Times - KKR commits $310 million to PMI Electro’s e-bus platform in its first India climate deal. The PE giant will take a majority stake in Allfleet — PMI Electro’s bus operating arm — and a minority stake in the manufacturer itself, backing a platform that has already deployed 3,000+ e-buses across 30 cities and is on course to hit 5,000 under state transport authority contracts.

Source: The Hindu BusinessLine

- This edition of the newsletter was written by Krishna and Aakanksha.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Subtext by Zerodha

Subtext by ZerodhaWe’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()