Recently I came across:

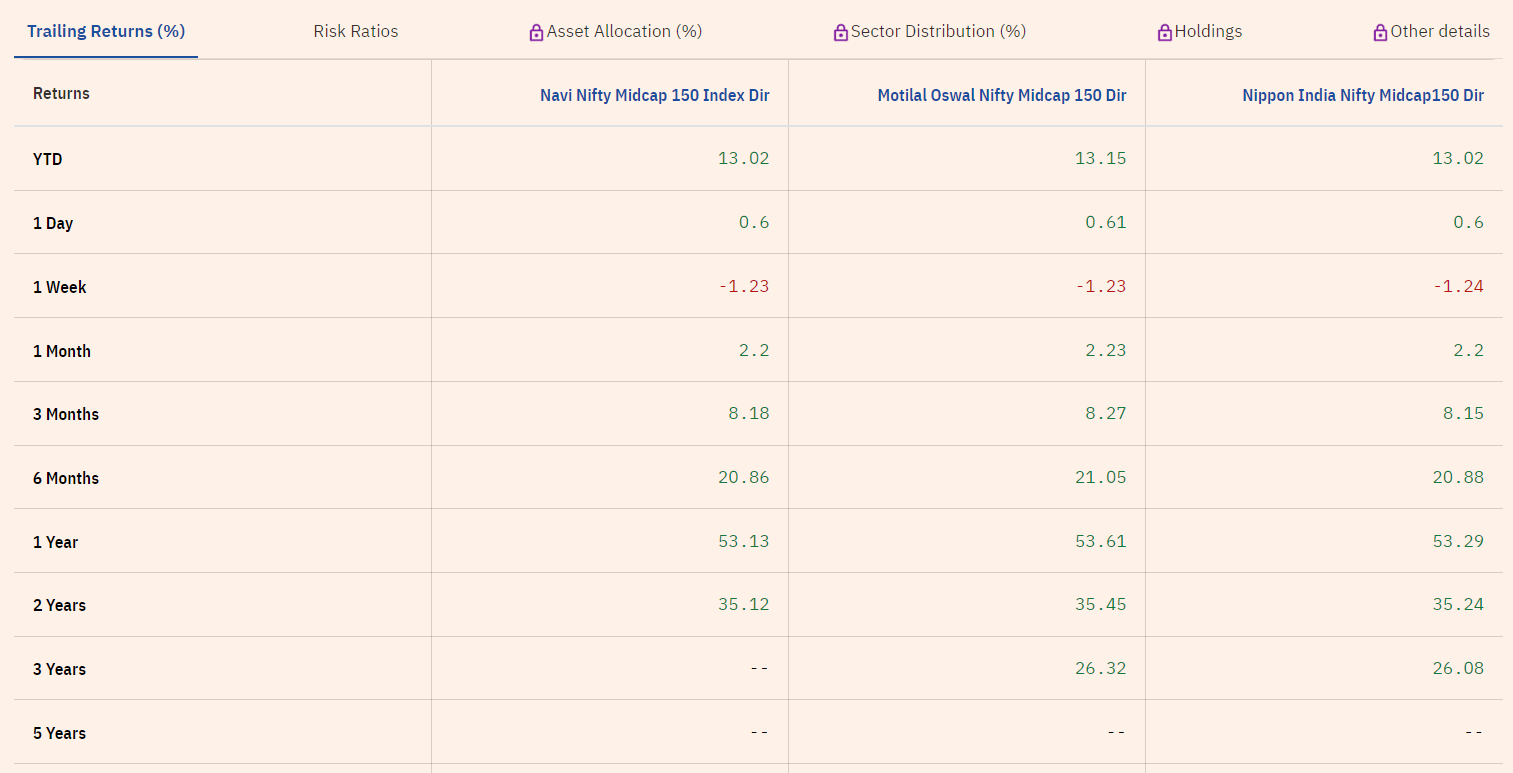

Navi MidCap 150 Index Fund

- Expense Ratio: 0.1% (Other’s is 0.3%)

- AUM: 138Cr

- Age: 2yrs

- Tracking error is not much as compared to High AUM index funds (around 1500Cr).

Therefore overall it looks fine…

So my question is what will happen if NAVI gets shut down?

What are additional risks if we go with NAVI?

PS: Zerodha AMC is even younger.

Thank you very much Neha.

Is there a chance of my investment getting stuck for years if mutual fund house does something fishy?

Therefore should I divide my investments across multiple mutual funds of same type? For example 4 NIFTY index funds instead of 1 NIFTY index fund?

In the article you shared, it’s written than the mutual funds gets transferred to a different fund house or the money is given back to investors. But how much time these processes take? Generally in India things take years to move. So is there a chance my investment will get stuck for years?

I would not worry too much if the AMC is well known. I have personally opted for SBI as an AMC for my investment in Nifty 50 ETF and Nifty next 50 ETF. The exception is motilal nasdaq 100 ETF. This is because SBi or UTI do not have such ETF.

As you are interested in Nifty 50 Index fund which is passive in nature, why would you go for lesser known AMC when you have SBI or UTI issuing the same Index funds.

Same rules apply for Term Insurance as well. It will always be LIC for me.

1 Like

Chances are always there. Very minute chance, but risk is always there

Something like that happened during COVID where 6 debt funds of franklin Tempelton were closed for redemption as they were unable to liquidate the bonds they were holding.

Finally that money was paid back over a couple of years, but I think at least for a year or two investors could not access their money.

So there is a small chance. I feel for largecap funds (nifty 50, next 50) risk is very low and can be ignored, but as you move away from large caps, you need to account for such risks.

1 Like

So it’s better to have at least 3-4 mutual funds of the same category to prepare for such a risk.

Complexity to Avoid Risk of whole capital getting locked for years.

4 MFs for Nifty (high allocation)

3 MFs for Next50

2 MFs for Mid150 (low allocation)

4 MFs for debt

The biggest problem in India is that the govt. is generally very very slow in providing solutions. And the common man is left hoping for a quick solution.

That’s why I fear. @Akash_Shah you gave a good example.