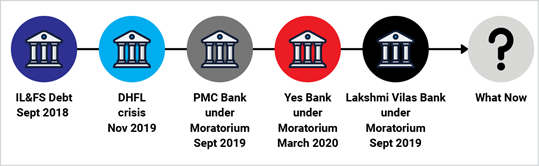

Starting with IL&FS, DHFL, PMC Bank, Yes Bank, and now Lakshmi Vilas Bank is the fifth financial firm to fail in a span of less than three years. The financial regulator- Reserve Bank of India (RBI) had to step in to impose swift controls due to financial irregularities of such firms

Many investors have either lost their hard-earned money or have limited access to their savings until the moratorium is lifted or per the prevailing RBI/Firm norms.

Case Analysis: Lakshmi Vilas Bank Crisis

Lakshmi Vilas Bank was a legacy 93-year-old financial institution and was offering attractive interest rates for deposits. However, this is in retrospect was also a sign that the bank was too eager for deposits. Weakening financials was another clear indicator that the bank was struggling. Gross NPA (Non-Performing Assets) of the bank has been consistently increasing for the past three years. LVB’s net non-performing assets stood at 7.01 percent on September 30, 2020. A non-performing asset is a loan or an advance where recovery of interest and / or principal has become uncertain.

Though Rs. 5 lakh depositors coverage is offered to customers by the Deposit Insurance and Credit Guarantee Corporation (DICGC), any savings exceeding this amount could face a possible loss.

So what should you do?

You can begin by considering these questions carefully.

Are you concentrating all your investments?

Have you done due diligence of the firm/bank you are investing with?

Can you consider alternative investment option such as Mutual Funds to park your hard-earned money?

Are you performing a periodic review of your investments?

Concentrating all your investments is definitely not a risk-worth taking.

We all know that mutual funds are subject to market risks. However, you can choose to diversify your investment options and start your investment in a multi-asset allocation fund that spreads your investment risk across asset classes.

Multi Asset Allocation Funds are hybrid funds that typically have a combination of equity, debt and gold or real estate, etc.

The thing to remember is that ideal asset allocation is not static. Asset allocation needs to change depending on an asset class’s relative performance vis-à-vis other asset class. Multi asset allocation performs regular portfolio rebalancing depending on the market movements

Here’s why your money in Multi Asset Mutual Funds is a smart choice:

Risk adjusted returns

Risk adjusted returns

Potential to generate risk adjusted returns over the long term

Impact of inflation

Impact of inflation

You are better positioned to cope with the effects of inflation due to the equity component that offers market linked returns over the long term

Transparency

Transparency

Regulated by SEBI, bringing transparency / disclosure norms by identifying and disclosing the risk factors in the scheme information document

Diversification

Diversification

Diversifies the risk across asset classes such as equity, debt & gold to mitigate the downside risk of investing in a single asset class

Liquidity

Liquidity

Offers liquidity, where mutual fund units can be redeemed at any time online or offline and the money will be deposited to the designated bank account generally within two-three business days

Note: Investments in mutual funds should not be construed as a promise, guarantee or a forecast of any minimum returns. Unlike Fixed Deposit with banks / money in the bank accounts, there is no capital protection guarantee or assurance of any return in mutual funds investment. Investments in Mutual Funds as compared to Fixed Deposits with banks / money in the bank accounts carry moderately high risk, follow different tax treatment and are subject to market risk. Please consult your Tax Consultant or Financial Advisor before taking any investment related decision.

Disclaimer: The views expressed here in this Article / Video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The Article / Video has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of the Article / Video should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. None of the Quantum Advisors, Quantum AMC, Quantum Trustee or Quantum Mutual Fund, their Affiliates or Representative shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary losses or damages including lost profits arising in any way on account of any action taken basis the data / information / views provided in the Article / video.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.