Research by DOLAT Analysis - Key highlights

-

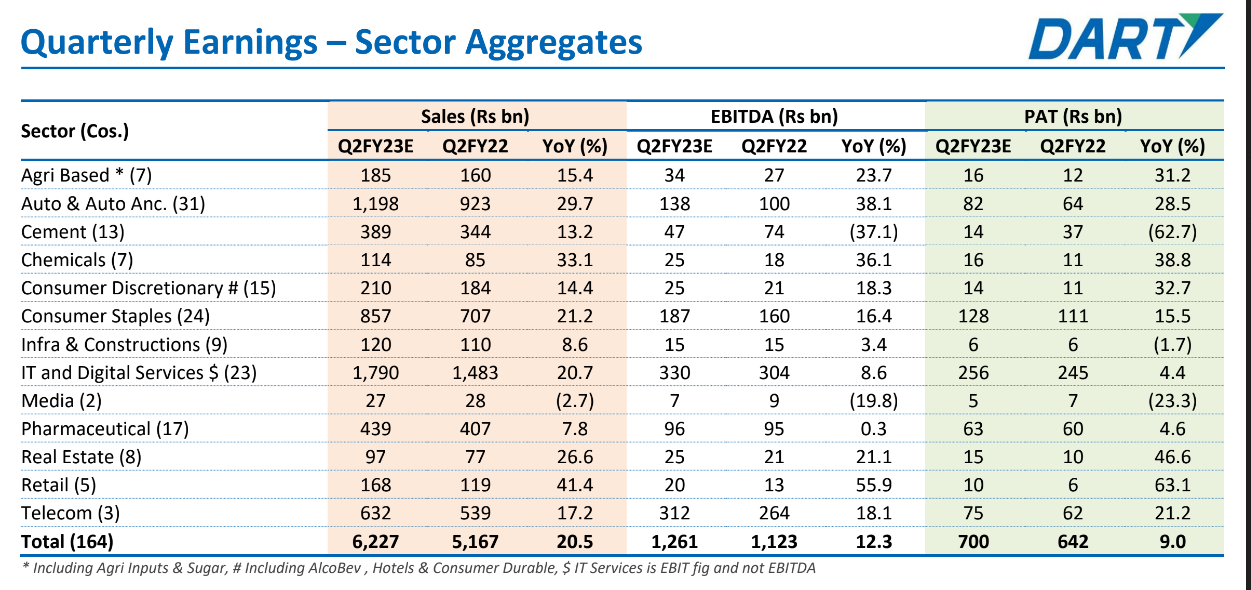

Our coverage universe (164 cos) is projected to show revenue growth of 20.5% yoy for Q2, while operating profits are projected to grow 12.3% yoy.

-

The Q2 net earnings growth estimates, as per DART projections, stand at 9% (ex-banks). However adjusting for the impact of the sharp decline in cement earnings and below average IT Services, the adjusted growth stands at a healthy 19%. Retail and Autos will be the highest ranked on revenue and earnings growth from our coverage. Real Estate shall also be another stand out quarter as per our channel checks although q2 is the weakest seasonally.

-

The large cap universe (40 cos, Mcap USD 908 bn, ex banks) is projected to report top line growth at 21% and 14% operating profit. Net earnings for the segment are estimated for grow at 9%. The divergence on revenue and net earnings is yet again due to the decline in cement earnings as well as muted show from the IT universe.

-

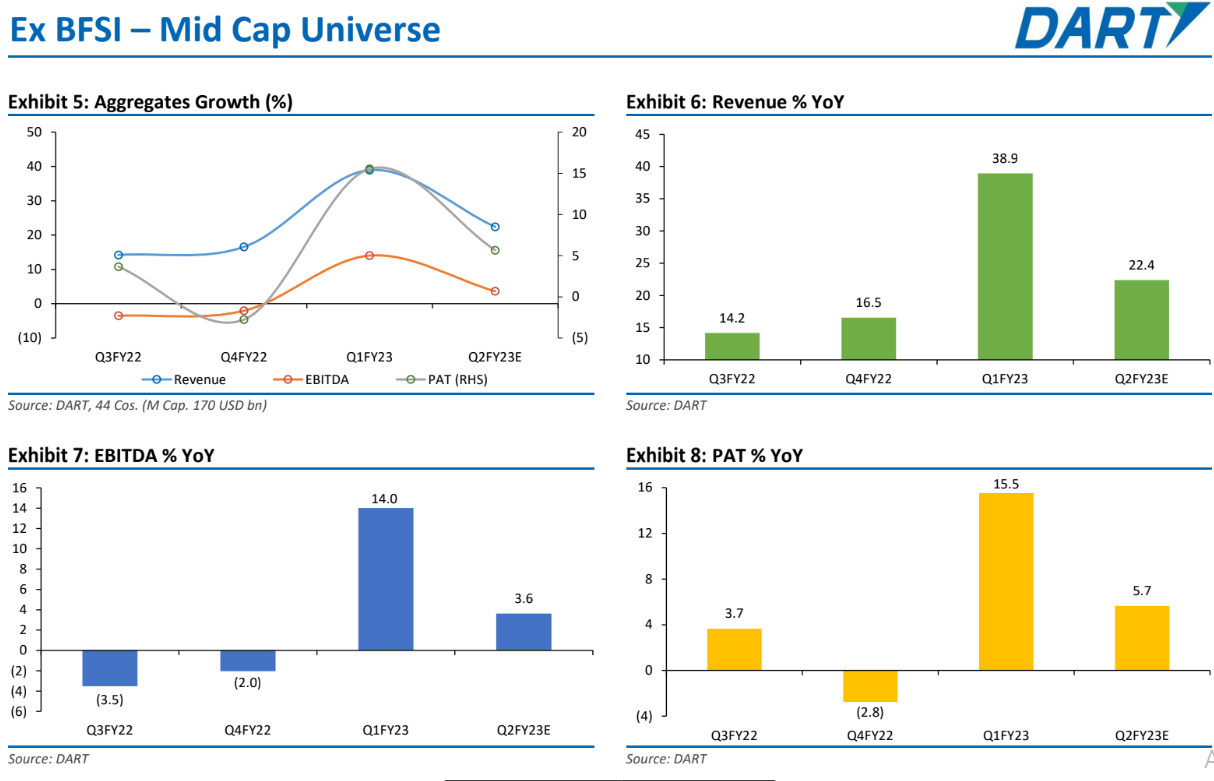

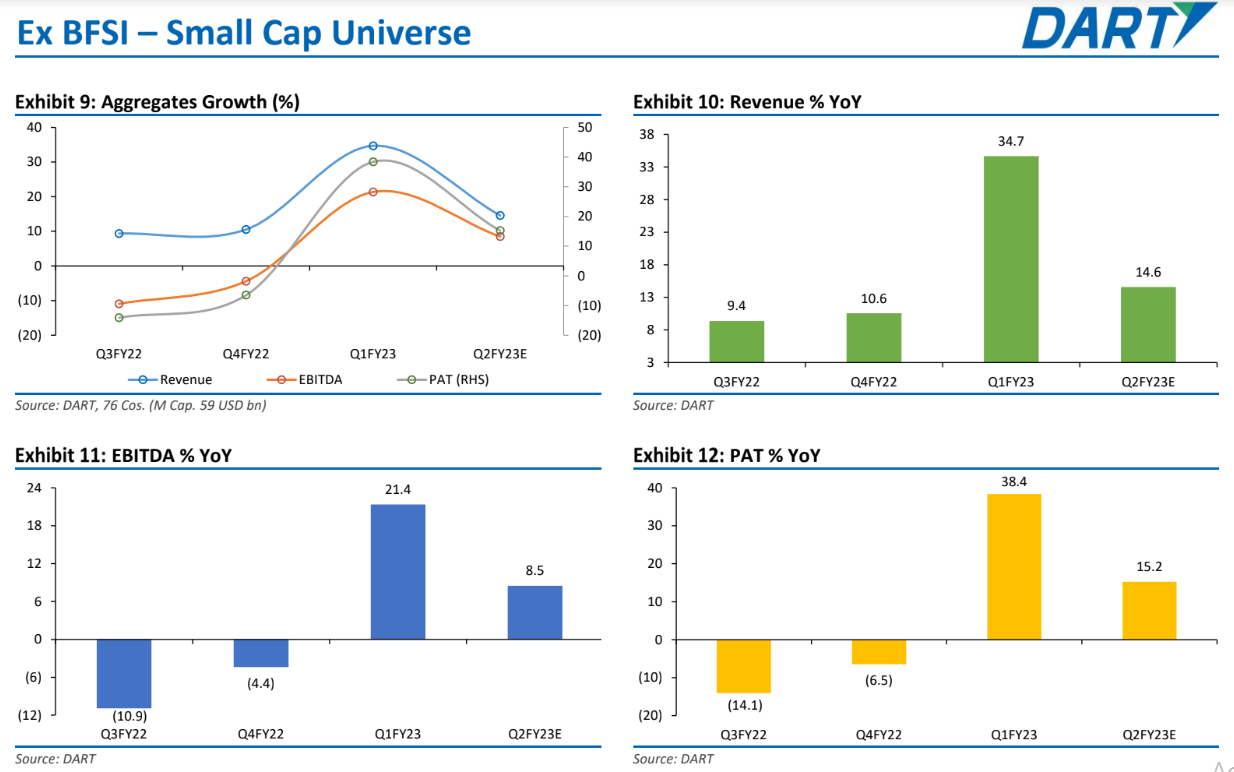

The mid (41 cos, USD 156 bn mkt cap) and small cap universe (68 cos, USD 50 bn) will see revenue growth of 22% and 15% respectively, while their net earnings growth is projected at 6% and 15%. Here again the cement and IT services lead to a swing on the operating and net earnings.

-

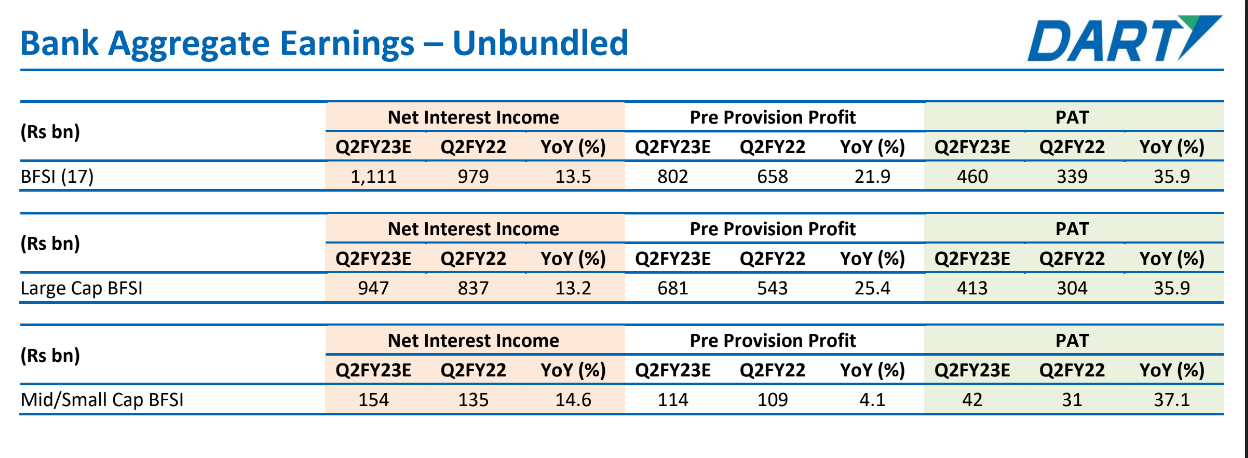

Banks as a universe will probably be at the strongest trajectory of growth for years - NII projected to grow 13% yoy and pre-provision profit growth estimated at 22% and net earnings to leap up by 36%. The growth is also well spread uniformly between large cap banks as well mid / small cap banks – this gives us greater confidence in the credit uptick sustaining going ahead and the quality.

Sector-wise growth expectation

Midcaps (Excluding BFSI)

Smallcaps (Excluding BFSI)

Let us use this thread to share both expectations from street and actual earnings of various sectors and companies and share various research reports.