The eye of the tiger meets the eye of the storm

Tiger Global LLC is one of the biggest names in Hedge-fund Crossover investing. Hedge-fund crossover investing is a way of investing where public market investors enter the private markets by funding startups at a later stage.

Crossover financings were initially developed to provide private companies more time and capital prior to an IPO. This type of financing also gave traditional mutual and hedge funds an opportunity to potentially increase their return by investing in a private company at a perceived discount to an upcoming IPO.

The tiger way

Take a look at Tiger’s approach. It isn’t limited to a typical VC that funds startups. Founded by Chase Coleman III, one of the prodigies of Julian Robertson, the ideology of Tiger Global is like the Tiger it is named after, Tiger Management.

I’d suggest reading the paper on the history, or rather, the legend of Tiger. You will have had a better context for this piece. ![]()

To sum it up, here are a few tricks from Tiger’s playbook which broke out of the taboo:

-

Rapid capital deployment and accepting a lower return profile.

-

Delegating due diligence to consultants like Bain.

-

Hands-off partner, which means that it does not interfere with founders.

The success of this ideology won Tiger quite a few accolades. Tiger eventually became the most attractive private market investor in 2021, cracking over 300 deals, more than it did in the previous five years combined.

The storm hits

Although the overall market sentiment has been weak in 2022 for obvious reasons, given the massive wealth erosion in tech stocks, Tiger Global, which has heavy bets placed on the sector, seems to be faring even worse.

As a result of the downturn in tech stocks, Tiger Global has racked in losses to the tune of $17 billion. As this Financial Times article put it:

“The run of poor performance means the firm — one of the world’s biggest hedge funds and a big investor in high-growth, speculative companies whose shares have tumbled since their pandemic peaks — has in four months erased about two-thirds of its gains since its launch in 2001.”

Because of these heavy losses, Tiger has cut its stake down in Netflix and Rivian. Tiger Global’s public stock positions fell from $46bn at the end of last year to just over $26bn at the end of the first quarter of FY22. Subsequently, Tiger has sold its entire stake in Bumble, Airbnb, and Didi.

It has further dumped about 80% of its stake in Robinhood.

Tiger has always been aggressive in its approach to funding startups. With no light visible from the end of the tunnel even in large economies like India, where Tiger has invested in companies like Flipkart, Ola, Myntra, Quikr, etc., this seems like a tough pill to swallow.

This has to be quite a lot to take for a hedge fund, especially one that has been highly unorthodox in funding. It won’t be long before Chase Coleman and the other tiger cubs sit at the table to mark down the valuations of the tech stocks they’ve invested in.

Tiger Global is not alone. SoftBank, another firm that has bet heavily on the tech sector, has reported $26 billion in losses for the fiscal year ending March 31, 2022. It is now cutting its investments in start-ups by up to 75%.

As aptly put in this article which talks more about the recent turn in fortunes of Tiger Global and SoftBank:

“With many of the most speculative pieces of the technology sector in retreat, it’s only fitting that the investors who bet the farm on high-growth tech stocks are suffering disproportionately.

In the bull market, SoftBank and Tiger Global became infamous for driving up valuations. Now they’re reaping what they sowed.”

Your take?

When you think about the unorthodox funding in situations like these, it makes you feel like Tiger was just a trust-fund baby who loved to splurge money. On the other hand, the aggression has helped Tiger win at least until now. They’ve had their method always work in their favor, given the numbers so far until 2021 Q3.

Do you think the tiger will ride the storm? Or do you think Tiger is just the first domino in VCs’ face, and HFCs are starting to mark down valuations and cut their long gracious funding arms to finger sprinklers?

SPACs Are Sputtering

“It’s different this time.”

SPACs have been around for decades, while these aren’t a phenomenon in India, they have grown wildly popular in recent years in the US. In 2020, 247 SPACs were created with $80 billion invested, and in 2021, there were a record 613 SPAC IPOs. And you ask what’s the narrative this time?

Bankers, lawyers, and sponsors, all said, “It’s different this time.” But it wasn’t.

A special purpose acquisition company (SPAC) is a company that has no commercial operations and is formed strictly to raise capital through an initial public offering (IPO) for the purpose of acquiring or merging with an existing company.

SPACs had always been one of the dark sides of finance and this route is used by second-tier private equity companies to dump their dodgy holdings into the market by offering IPO investors. If you check out the numbers then more than 300 companies that have gone public via SPAC mergers since 2018 have averaged a loss of about 33% from the IPO price of the SPAC, whereas it’s 2 percent for the 1,000 other companies that chose to go public through a traditional IPO as of mid-April, according to Renaissance Capital, which tracks IPOs. On the other hand, the S&P 500 index gained more than 50%.

All these warnings went for a toss when the new crop of SPACs were sponsored by top-notch Wall Street players like hedge funds and venture capital and private equity mavens. The list of brand names is practically endless, including people like former Goldman Sachs CEO Gary Cohen and former Citigroup banker Michael Klein; tech superstars Reid Hoffman and Chamath Palihapitiya.

Big banks like Citigroup, Credit Suisse, and Goldman Sachs were suddenly topping the SPAC underwriting league tables, while multibillion-dollar hedge funds Millennium Management, Magnetar, and Citadel became some of the biggest investors in SPAC IPOs.

Today the SPAC market is in disarray due to redemptions and regulations. In 2022 there have been only 67 SPAC IPOs, raising some $11.6 billion, compared with 613 raising $162.5 billion last year. As of late April, SPAC sponsors were canceling their planned IPOs at a furious rate, with Bloomberg reporting that some 62 SPACs that were slated to raise more than $17 billion have nixed those plans. Since its peak in June 2021, the deSPAC Index was down more than 70% as of May 10.

Here’s the detailed research article by law professors Michael Ohlrogge and Michael Klausner:

Consistency is Key.

Consistency is the key to long-term investing success, you’ve probably read and heard this a gazillion times ever since you’ve started investing. Here’s one such article which shares a story about how being consistent means you have a high percentage of success not only while trading but also when buying businesses, based on Warren Buffet’s biggest purchase made in the ‘70s this company produced multiple new streams of cash for Berkshire Hathaway’s investments.

Warren Buffet’s Berkshire Hathaway owns dozens of companies ranging from insurance to banking to energy. But his favorite investment of all time seems to be a small candy chain See’s Candy that he initially hesitated to invest in, this company represents less than 0.1% of Berkshire Hathaway’s holdings.

In an era of fast-paced investments, the story of this chocolate shop reminds us that a company’s true value can’t always be quantified on its profits or ability to generate high income and should depend on branding and quality.

Focusing on high-quality products rather than producing high quantities of the product was both Buffet’s and See’s investment philosophy. When you have strong customer loyalty and provide premium quality products customers would not hesitate even if the costs go up. Slow growth doesn’t always mean it’s a bad thing, as long as that growth is steady and reliable.

Buffet purchased this company based on its intangible values like brand and customer loyalty rather than the numbers on its balance sheet, See’s, later on turned out to provide steady returns which it later used to buy into other attractive businesses like Coca-Cola shares.

A stock is not an Index

We are all attracted to discounts. And being swayed by falling stocks is just one of those attractions. The temptation to invest after a big fall in stock prices, thinking we are getting a good deal is unreal. But one has to keep in mind that what fallen 50% can fall another 50%. There’s no guarantee that the prices will rise.

There are plenty of examples of this, some of the most famous ones being Yes Bank, DHFL, Reliance Infra, etc. All of these were once investors’ favorites. Things went south and so did the stock prices and people invested in these stocks in hope of change in fortunes only to see their hard-earned money getting wiped off.

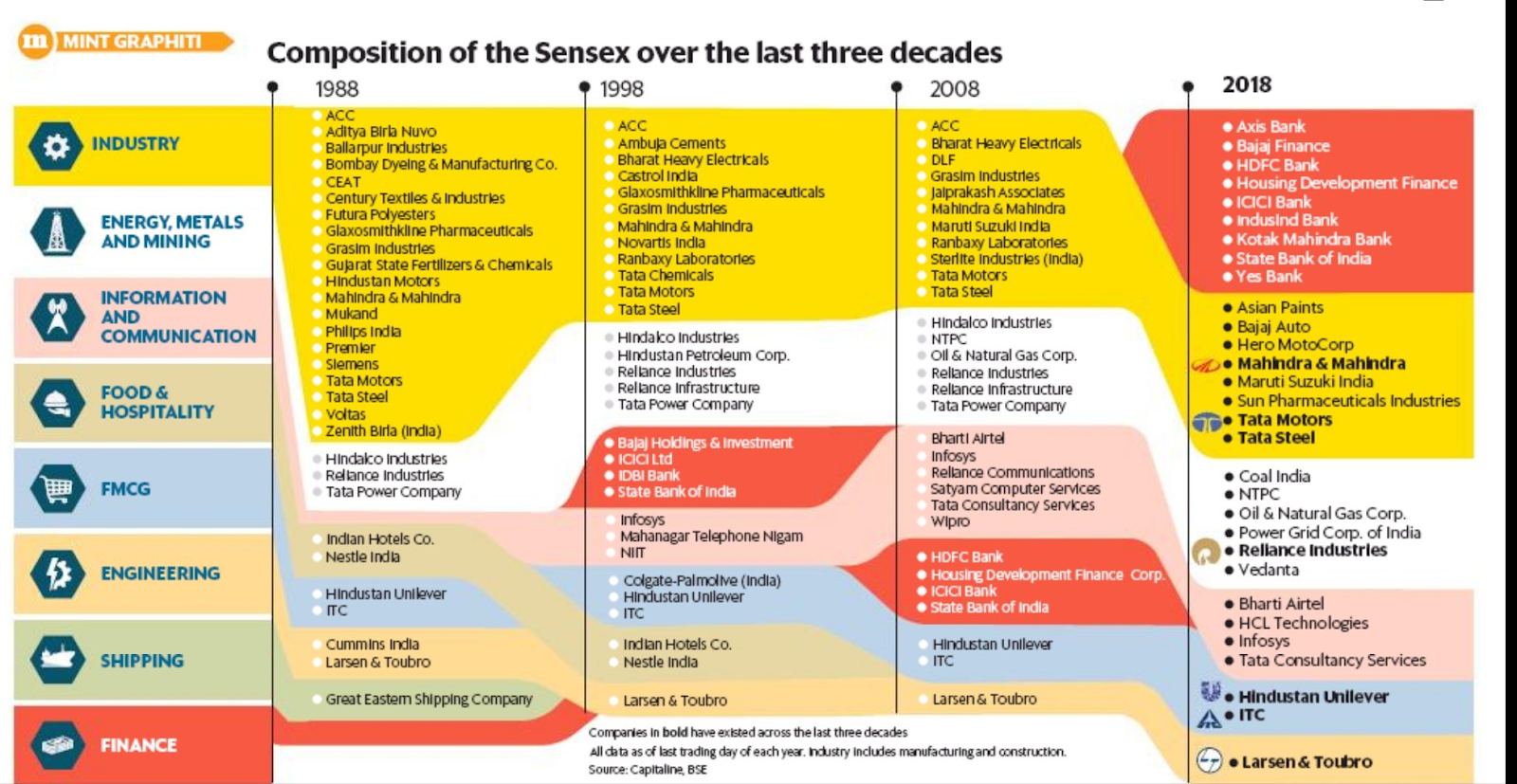

There’s a difference between buying a declining stock and a declining index. The key being, that there is no guarantee that the individual company will recover, there are a lot of things that need to fall in place. Index on the other hand will, as it is diversified and comprised of stocks from different sectors, which keep on changing over time. Though there are exceptions to this, ie. Japan ![]() but you get the point.

but you get the point.

Source: Mint

Although this graphic is from 2019, but this is how Sensex has changed over the decades.

This is not to say that investing in individual stocks isn’t good. Just that, investing simply based on price ignoring the underlying causes for the drop in prices is a bad idea.

Trying too hard

“I’ve tried so hard and got so far, But in the end, it doesn’t even matter”

Linkin Park lovers would know exactly what this means. ![]()

But more than them, A trader who has tried way too hard dabbling complex stuff may relate to the above song more.

In my trading journey, I have tried many methods and finally realized that too much of anything (simplicity and complexity) is injurious both to health and wealth. The “truth” may “lie” in between the both.

But it’s okay to get minor bruises but just make sure that your back isn’t broken. I have luckily followed the above principle.

This piece by Morgan Housel talks about the various nuances associated with being a novice and the process of being an expert and the journey.

Bear Market Playbook

While we are not there yet but it sure feels like we are.

“The most important thing right now is not to panic and to stick to your plan, assuming you had one. But every market environment presents an opportunity to do something to improve your portfolio or your total financial picture. These actions can help scratch the urge to DO SOMETHING to ease the pain of seeing red on your statements. It is in our human nature to react to fear, and with careful planning and deliberation, perhaps we can harness that energy into something productive rather than destructive.”

While most of the points are from U.S. perspective but a good read nevertheless.

Intangible assets and the relationship with rate hikes

Companies have an increasing amount of capitalized goodwill and other intangibles on their books. But what do the intangible assets account for?

Intangible assets increase the book value but aren’t a form of productive capital. These assets cannot be converted into dividends, buybacks, or revenues for shareholders. How healthy is it for companies to have a higher intangible asset ratio in the long run?

This piece by Joachim Klement talks about the effect of rate hikes by the fed on companies with a higher intangible asset ratio.

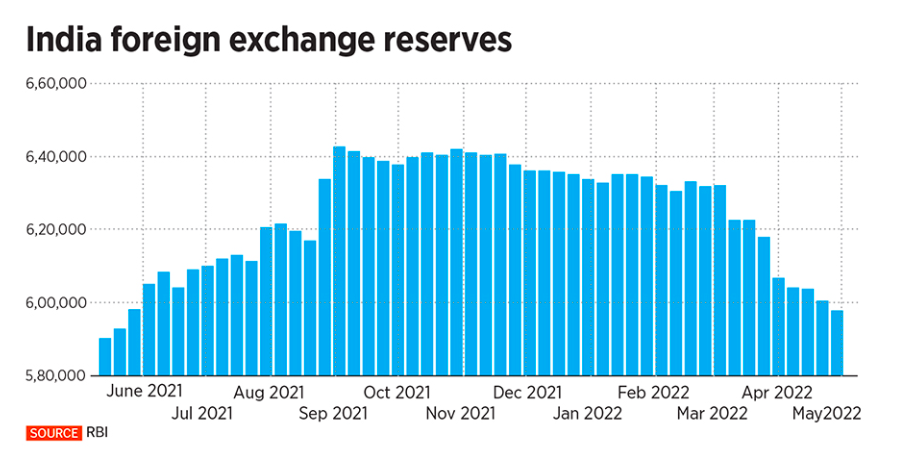

Rupee depreciating!

The rupee falling to an all-time low is the one thing that is headlining the most this week. The USD INR spot rate is at 77.552 as of the 20th of May. It has weakened as a result of the global slowdown, the Ukraine-Russia crisis, and the Fed raising interest rates.

A few factors to know while we understand this:

India’s foreign exchange reserves have dropped below 600 billion dollars since March.

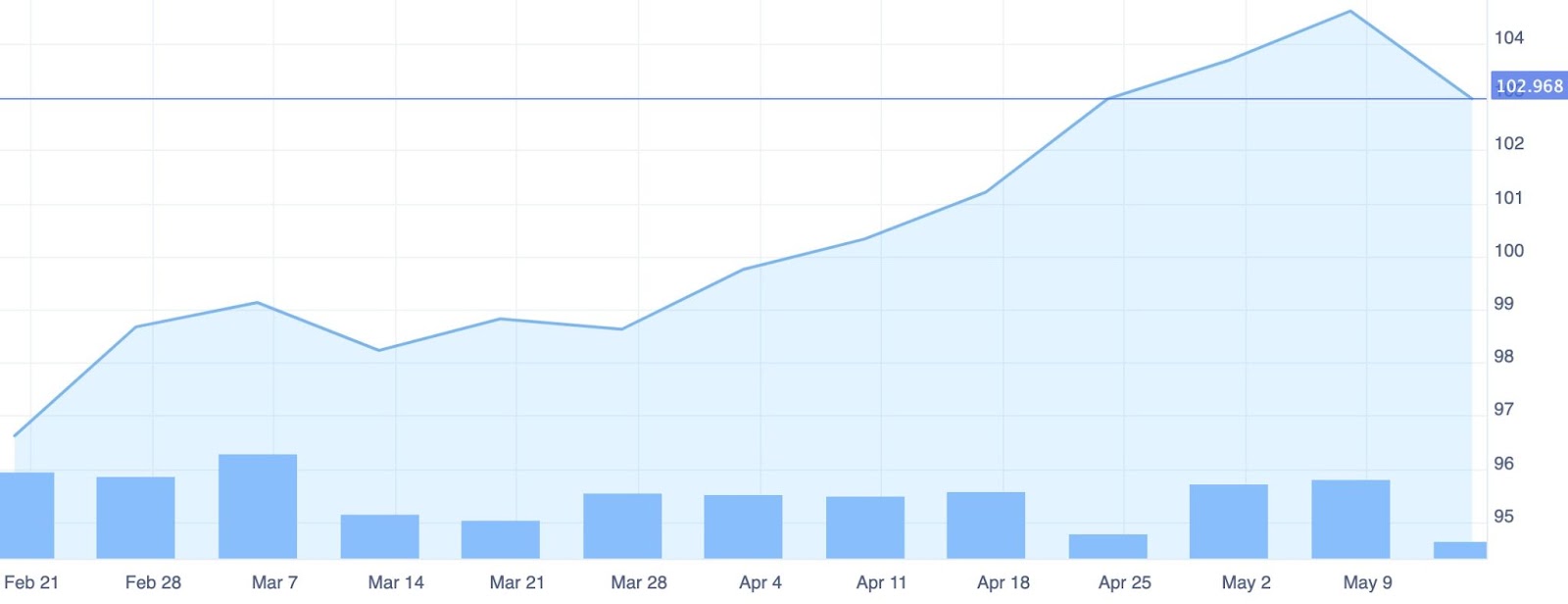

If you look at the dollar index, which covers the currency of key indexes, it’s up more than 8% in the previous three months.

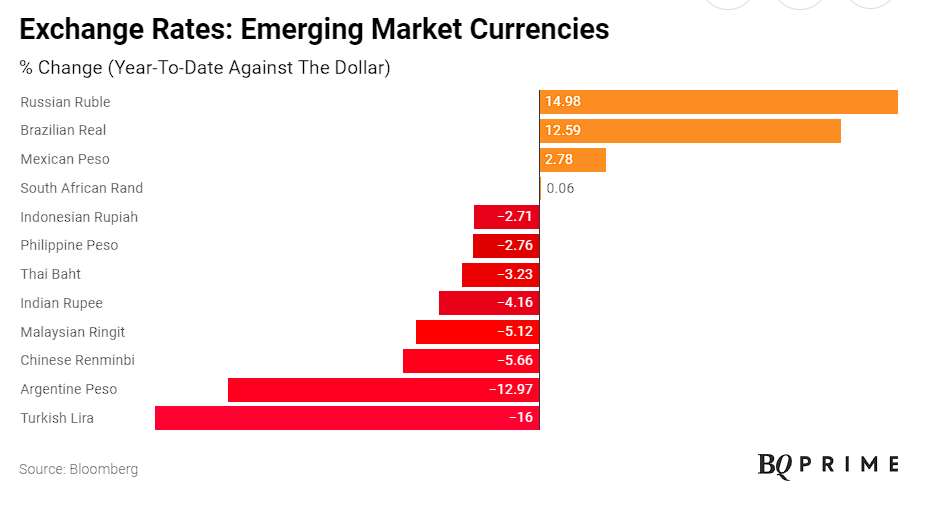

Also, it’s not just the Indian rupee that has suffered, many other currencies have also suffered. This is how the emerging market currencies have fared against US Dollar year-to-date.

To put it simply, you should not be shocked if commodities prices skyrocket and become more expensive than ever before. To state the obvious, India imports over 80% of its crude oil, which is the biggest import, followed by edible oil. Exports will rise when the dollar strengthens, causing exporters to suffer a loss and export at a lower cost.

Here’s a quick read from Tickertape and a podcast from Finshots daily on the rupee’s all-time low.