Global food crisis!

One of the most horrible problems we have faced since the dawn of time is the food crisis. No doubt the war situation between Russia and Ukraine has escalated the issues but is it the only cause for the current global food crisis? I doubt that!

“Russia’s invasion of Ukraine seals a fate that was already inked by the woefully inadequate economic and political responses to COVID-19. The rise in prices and hunger triggered by the war will cause a wave of rebellions, just as food price spikes have in the past: as with the 2010 demonstrations that inaugurated the Arab Spring, the 2007–8 wave of food protests from Haiti to Italy, and the 1980s and ’90s International Monetary Fund (IMF) riots. The only difference is that this time, it will be worse.”

Among the endless list of reasons for this crisis, here are a few major ones;

-

Colonial legacies - encouraging not to grow food, nor to waste resources on grain storage for local emergencies, but to concentrate on tropical export products

-

Climate change - extreme weather conditions affecting agriculture and its yields

-

Covid - majorly supply chain disruptions

-

Capitalism - corporates trading commodities

As per stats, in 2014, 606.9 million people (around 8.3% of the global population) were undernourished. In 2020, the COVID-19 pandemic added 118–161 million more people to the list. In 2021, as per USDA projections roughly there is a 7% increase. The war in Ukraine has piled an additional 8–13 million people onto that. In 2022, we are looking at 830 million people being deprived of 2,100 calories a day.

What can we really do about it?

Raj Patel has presented his views in the form of 5 D’s (Depots, Diversify, Debt reparation, Decouple, Decolonize) in the following article suggesting a few solutions for the food crisis.

Gender Lens Equity Funds

Probably the most fascinating piece I’ve read this week, it talks about how climate crises affect women and girls across all demographics.

Roles such as primary caregivers and providers of food and fuel make them more vulnerable when flooding and drought occur.

The 2015 Paris Agreement has made specific provisions for the empowerment of women, recognizing that they are disproportionately impacted.

Coming to the monetary aspect of this effect, this piece talks about the ongoing worldwide gender gaps, and climate events taking a toll on women’s job security and education.

Enter, Gender Lens Equity Funds

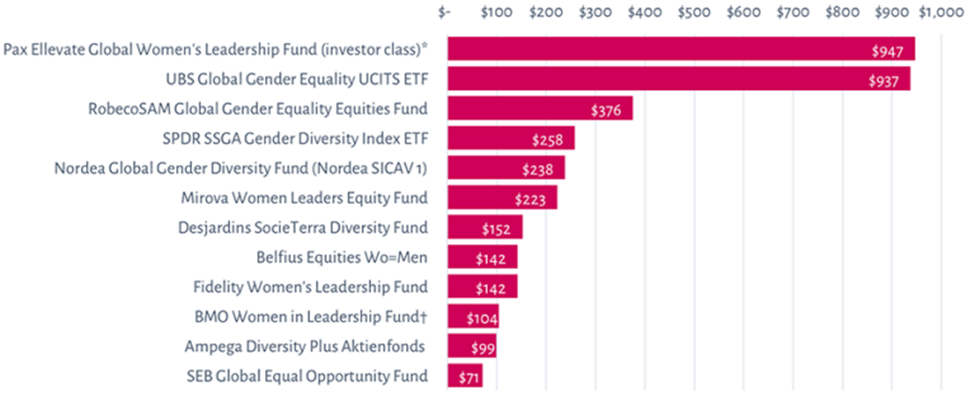

Gender lens investing puts resources into women-based initiatives, women-owned businesses, and firms that demonstrate a commitment to gender and broad-based equality internally and through their external relationships, products, and services. Here’s an interesting graph bit.

The 12 Largest Gender Lens Equity Funds, in US Millions, as of 31 March 2022

It discusses the relationship between climate funds and the inclusion of the Gender Lens fabric in it, the way forward, and how equality criteria can be included.

Bull Market Rhymes

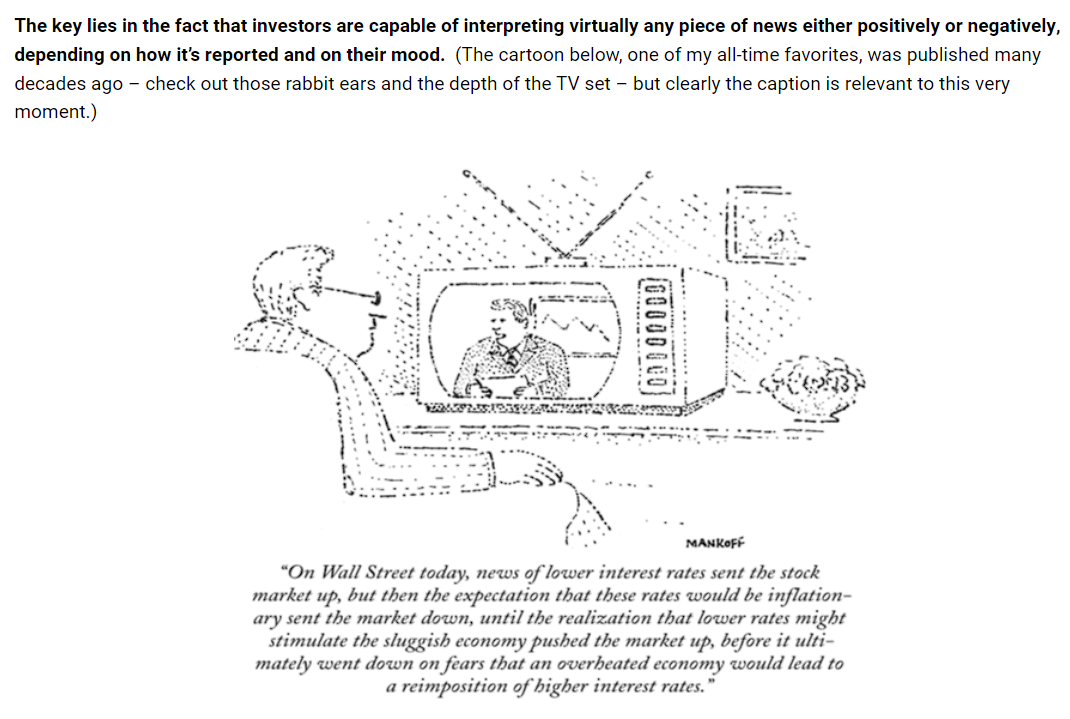

Howard Mark’s recent memo is an insightful read. In his latest memo, Mark’s writes about the recurring investment themes, things that drive the bull and bear markets. The role played by financial innovations like SPACs and cryptocurrencies. And why he believes that markets are driven primarily by psychology, not fundamentals.

There are quite a lot of interesting takeaways, one that I liked the most:

https://www.oaktreecapital.com/insights/memo/bull-market-rhymes

### Anti-financial advice that we all need.

“You need to save more” that’s what my mother always tells me and it’s probably something you’ve also heard or said at some point in time. So imagine my joy when I came across this little piece that talks the opposite.

It explains how to give yourself the freedom to spend cash without feeling guilty because, in the end, the sole purpose of earning money is to spend it but spend it once you’ve covered the basics; an emergency fund & retirement savings. The general rule of thumb is to save at least 10% of your income, and once you’ve saved enough you can spend that money on experiences that add value to your life.

Don’t deprive your current life of experiences that you would enjoy to give your future self money that they don’t need.

Make enough money to cover your expenses and investments while still having some cash leftover which you can spend however you’d like. Instead of cutting costs focus on expanding your income side. Expand your income, increase your dispensable cash, and do whatever you want.

Default Alive or Default Dead

This is a nice essay from Paul Graham. Although old, from 2015, I think it is quite apparent in today’s time of uncertainty. The basic idea is that there are two stages to a company, default alive or default dead.

And it’s not just about the companies, these principles can be applied to our personal finances as well. To simply put, if we are in the default alive stage, have our finances in order, we can look forward to achieving better things. If we are in default dead stage, we need to get things in order.

It’s important to know where we stand, and more importantly to know it early.

“It’s hard to say precisely when the question switches polarity. But it’s probably not that dangerous to start worrying too early that you’re default dead, whereas it’s very dangerous to start worrying too late.”

http://www.paulgraham.com/aord.html

Twenty Lessons Learned

Nothing lasts forever. Survival is the most important thing. Memes are not fundamentals. Nobody knows what will happen next. Past performance is not indicative of future performance. Past behavior is. Investing is hard.

A nice list of lessons that we can learn from bad market cycles.