Can Google own the internet?

If there is one product that everyone uses daily and is a synonym for search, that’s Google. Even if you want to know about Google then 90% chances are that you will have to “Google” it to know. Such is the monopoly of this internet behemoth search engine. But it has always found itself in the crosshairs of lawmakers’ policies citing antitrust and unfair manipulation of the market to its own advantage.

This article shares a few insights on a Big Tech antitrust bill against Google and other huge tech companies like Apple, Amazon, Microsoft, and Meta that have similar market share and power.

“There are two bipartisan antitrust bills that are very close to becoming law, likely by the end of the summer. Both of them would forbid Google from giving its own products preference on the platforms it owns and operates: The Open App Markets Act would force the Google Play app store to follow certain rules, while the American Innovation and Choice Online Act bans self-preferencing on platforms that Big Tech companies own and operate. Google wouldn’t be allowed to give its own products prominent placement in Google search results, for instance, unless those products organically earned that spot.”

Listing a few instances explained in the article of how this monopoly can affect everyone in the ecosystem;

Google hurting its competition:

-

By putting its own reviews at the top of its own search engine results.

-

By making “exclusionary agreements” with other companies to keep its search engine dominant. Google isn’t just the default search engine on Chrome; it’s also the default on Apple’s Safari and Mozilla’s Firefox.

-

Higher commissions for app downloads on the Google app store.

Google hurting consumers:

-

A consumer spending on apps through Google’s Play Store, and is required to use Google’s in-app payment system ends up paying Google a commission. Companies have to make that up somehow and that cost comes on to the consumer itself.

-

Advertising costs are being built into the price of the product and the consumers bear the brunt without even being aware that the product shown in the result is actually a quality product and whether it meets the consumer’s requirement or not, because if the costs aren’t compensated then the quality is compromised.

Do make sure to check out more on this in the below article by Sara Morrison.

The Rise and Fall of Wall Street’s Most Controversial Investor

Cathie Wood is an unusual creature in the realm of Wall Street. An outlier in her nearly boundless optimism about the riskiest investments on the market. Her willingness to make bold calls, and being out of step with Wall Street’s old guard earned her a rockstar reputation amongst new-age investors.

“She told risk-drunk investors exactly what they wanted to hear. In her view, it seemed, tech stocks only went up and to the right.”

Her fund Ark Innovation, popularly known as ARKK was riding high atop the Fed-driven bull market. The fund returned 157% during that first year of the pandemic, compared to just 18% by the S&P 500. A performance that drew accolades from various market watchers.

But things don’t go up forever, as the euphoria around new-age stocks died down, so did the fund’s performance. The fund is now where it was in March 2020 with investors in the fund since then having round-tripped all the way up and all the way back down. While the investors who bought at the peak are now down over 75%. Making many question Wood’s approach, who continued betting heavily on falling knives.

“Wood’s undoing in the midst of a market meltdown was seen as inevitable by those who resisted the bullish frenzy. “From our side of the table, none of this is shocking about Cathie Wood. I’ve seen this movie before,” says Carson Block “It’s not that you were really that brilliant, you were just long.”

An interesting read on the rise and fall of Cathie Wood and ARKK.

Related Reads;

https://twitter.com/michaelxpettis/status/1532669485618167813?s=20&t=0bwSGDQnOQqBHWOnkrRAAg

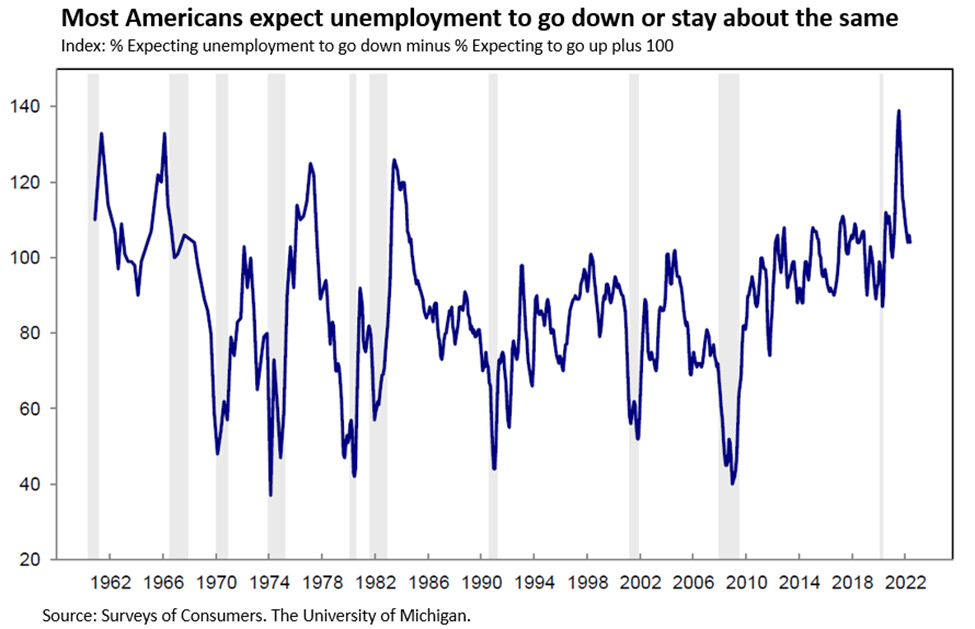

We’re not in recession… yet.

This paper authored by Claudia Sahm is a fine piece. Claudia used statistical findings to break the notion that we’re already in recession. This is a brave write-up scribed to make it clear that we’re yet to ride the storm. Of course, this is based on the US, so it does not entirely paint a global picture. However, since we depend on the US economy relatively more significantly, this stays relatable.

-

Businesses added almost 400,000 jobs last month in the US.

-

The unemployment rate held at 3.6% for the third month.

Interesting chart depicting a survey of what Americans think about the current scenario.

She argues that these are definitely not recession-causing numbers. She goes on to explain how we actually know if a recession is brewing. A couple of facts concerning here are:

- Inflation is too high.

- Big names in finance like Jamie Dimon are hinting at a recession’s onset.

Claudia moves on to explain the steps that can be taken to try and curb inflation. She talks about labour shortage and the reasons behind it, how the US labour market is improving and where workers are placed in this whole post-pandemic job market.

My take:

Surprisingly, I felt that Claudia could’ve, or rather, should’ve spoken about the Great Resignation. Although she has vaguely mentioned it in the paper, a deeper reference to this subject would’ve leaned the paper more toward how the labour market would move on to sustain if the great resignation continued.

The war in Ukraine and its adverse effects on energy and food prices are an additional hardship for many families and a further risk to many flourishing and established economies around the globe.

Poor financial health can have physical consequences.

Debt is not a bad thing as long as it’s used cautiously, in fact, it can build up wealth over time, that’s where “Good” debt and “Bad” debt come into the picture. Money owed for things that can help build wealth or increase income over time, such as student loans, mortgages or business loans is considered good. Whereas things like credit cards or other consumer debt that do little to improve your financial outcome are bad and need to be avoided as much as possible. But in all cases, no debt is the best debt because based on one’s financial situation it can turn out to be detrimental to your wellbeing.

In fact this whole report is based on how elderly adults carrying large amounts of unsecured debt have significantly worse health outcomes.

Researchers at the Urban Institute analyzed broad national data over 20 years, and have reported that indebted older adults have significantly multiple diagnosed illnesses like depression, hypertension, diabetes, cancer, heart & lung disease, heart attacks and strokes, which also hinders their ability to work and handle everyday activities.

Older adults close to retirement should be at the peak of their wealth accumulation and typically should carry less debt than younger ones because they tend to pay off their debts as they approach retirement age. But in recent decades, each group of seniors have been more indebted than the previous one.

Seniors with any kind of debt were more likely to encounter health problems, but the kind of debt also mattered: Secured Debt appeared less detrimental to health than Unsecured Debt.

But what are Secured and Unsecured debt?

Secured debt is a planned debt, for example buying a house. It’s an investment, and often a well-thought-out decision.

Unsecured debt often comes as a surprise, you could lose a job and might have to live off a credit card. You might fall ill and face a huge hospital bills, such as credit card balances, unplanned loans and overdue medical payments, which usually charge higher interest rates and this stress might lead to deteriorating health.

Why would unsecured debt have such an impact? This remains unclear even to them, although Dr. Mudrazija in this article adds that this works in the other direction as well; people with poorer health might need to borrow more, especially as health care costs tend to also increase due to inflation.

What could help seniors avoid these credit traps, apart from higher incomes and more comprehensive health insurance?

Dr Lusardi advocates financial literacy training in workplaces, emphasizing more retirement savings than debt management, providing clearer consumer information and helping borrowers grasp fundamentals such as the way interest compounds can help all of us enjoy our golden years later on, hopefully, debt-free.

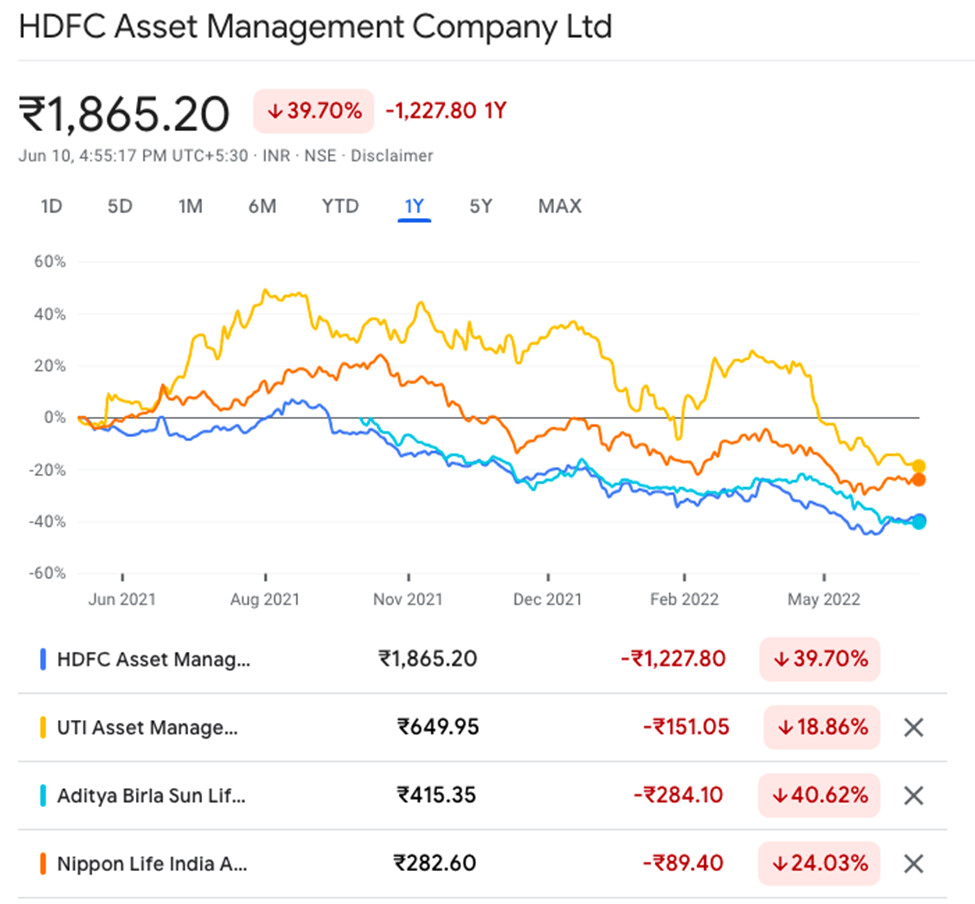

Why are mutual fund AMC stocks falling?

If you are like me and have been investing in mutual funds for a long time, and believe that people will continue to invest in mutual funds and that the industry will continue to grow. You may have bought a few AMC stocks, and given the size of the Indian population, everyone speculated that the country would see a massive surge of new investors.

The AMC industry operates in a highly regulated framework. SEBI has set plenty of guidelines and rules to keep the market safe and regulated. Despite the continuous Mutual fund ads running all over, the industry seems to be having a rough time. AMC stocks have taken a hit in the last year.

Here’s the performance of AMC stocks over the last year.

Here’s a good read from Capital Mind on why AMC stock is falling:

The Market Has No Memory. Should We?

“According to efficient market theory, the market has no memory. People, on the other hand, tend to remember their wins and losses vividly. They keep score, collect trophies, and accumulate scar tissue. But their memories can quickly get in the way.

But there is a danger of getting stuck in this failure-driven learning loop of contemplation that can leave us with self-doubt and hesitation. And the more emphasis we put on memory and lessons from specific situations, the more we may close ourselves off to situations that share similarities but should be viewed with fresh eyes.

We learn by studying history and our own mistakes and actions. But if we hold on to our memories too tightly, we close ourselves off from the present. We view new situations through an aging and outdated prism. In your quest for knowledge and better understanding, don’t be afraid to forget.”