Here’s what you should be reading:

1. The Nothingness of Money

Money has an outsized importance in our lives. The pursuit of money consumes most of us and over a period it becomes way more important than it should. We lead our entire lives worrying day and night about money, about meeting arbitrary targets-not that aren’t important. But all of us philosophically know that we don’t take the money to our graves.

Ironically, money becomes less important as we get older and at that point the other things, the experiences become important. So what if realize that nothingness of money early in our lives? This is a brilliant piece on our never-ending pursuit of money.

The only way to resolve this tension is to remind yourself that you are already aware of the inevitable futility of a money-centered pursuit. That what you will see as ridiculous later can actually be perceived as ridiculous now.

Money is the great everything and also the great nothing.

“Wisdom is the co-existence of contradictory truths, and money is the clearest example of this. We must internalize its importance while also recognizing its pointlessness. We must operate within the story of money while also understanding that it’s a fairy tale.”

2. How do fund flows impact stock prices?

When investors are looking at stocks, they mostly don’t think about the impact of fund flows on the prices. The common assumption is that the markets are efficient enough to digest the impact of large flows on stocks and the prices will revert to their fair price. But we live in the world of passive investing where there are continuous flows into large portions of the market. Some people have called it the “permanent bid”. So this leads to the question: Can stocks remain disconnected from their fundamentals for a long time?

Drew Dickson is this brilliant post looks at the research and teases out the various perspective on this. This is really fascinating

So yes, flows may matter in the short, and maybe even the intermediate term. As Graham said, the market is a voting machine. But it eventually weighs.

Accordingly, flows just aren’t the primary motivator of long-term stock returns. They may accompany them on the journey, but they aren’t sitting in the driver’s seat.

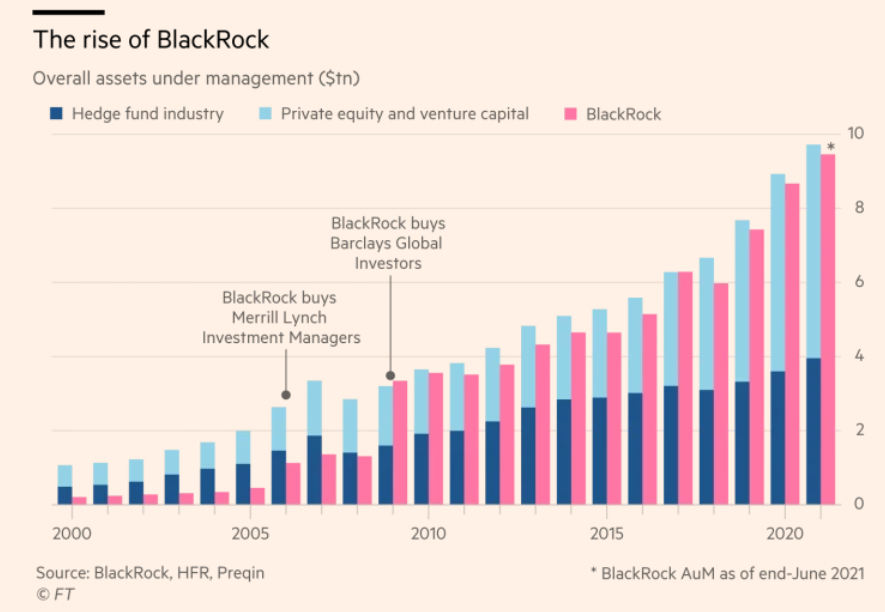

3. The ten trillion dollar man

Exchange Traded Funds (ETFs) are eating the world. It nearly took a decade for US ETFs to hit the $100 billion mark, today, the ETF AUM is $7 trillion, the growth has been stunning.

And no single firm has been responsible for the growth of ETFs than Blackrock, which is the 80,000-pound gorilla in the ETF space. Larry Fink, the founder of Blackrock has turned the firm into a global asset management giant through some shrewd and deft maneuvers with $10 trillion in AUM. For context, the Indian mutual fund AUM for context is just around ~$500 billion.

The story of how Blackrock became the giant that it is today is just like a suspense thriller. Here’s a brilliant FT long read.

Today, BlackRock has overall assets under management of almost $10 trillion crores, which is roughly equivalent to the entire global hedge fund, private equity, and venture capital industries combined.

4. 3 Levels of FOMO

Warren Buffett once said the reason bubbles exist is because people see neighbors dumber than they are getting rich.

And there’s a lot of dumb stuff that is making people rich these days as the fear of missing out, or what we call FOMO has to be at all-time highs.

5. It’s all in the earnings

Share prices deviate from fair value all the time and the volatility in markets is much higher than what is justified by the fundamentals. But what drives investors to move share prices away from fair value? The first thing that comes to our mind when presented with this question are things like sentiment or expectations about future earnings. But it is much harder to try to quantify the impact of these factors.

Joachim Klement summarizes a research paper published by Andrei Shleifer and his colleagues on what actually makes prices deviate from fair value.

6. The same stories, again and again

This one from Morgan Housel is a brilliant read; Every culture and era share universal characteristics that repeat again and again. The same attitudes, the same flaws, the same stories that show up all over the place. They’re reflections of how people’s heads work no matter where they live or when they were born.

Those common behaviours are what I find the most interesting from history because they’re not just trivia – you can be nearly assured that they’ll eventually impact your own life.

In the news:

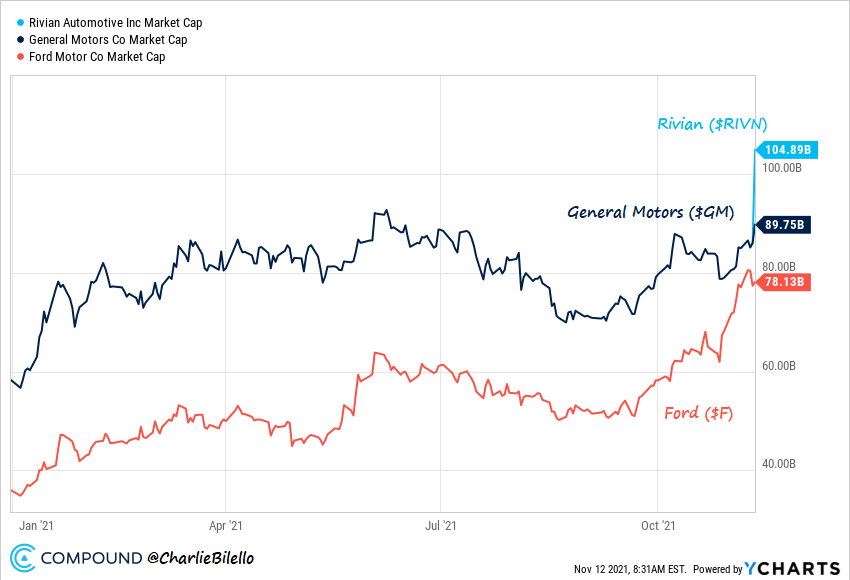

$100 billion in valuation, no real revenue:

If there is something that can summarize irrationality or sky-high levels of optimism in the markets, I think the IPO of Rivian might just be it. The EV startup made its stock market debut recently in 2021’s biggest IPO. Soon after the listing, the company hit a valuation of $100 billion, which is more than that of century-old Ford and General Motors. Interesting thing to note in all this is, the company is yet to make any real revenue as of now.

https://twitter.com/charliebilello/status/1459153703320043523

Here’s what you should listen to;

So what have you been reading, listening, watching to? Share below ![]()