Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how, too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Indian Banks Aren’t Failing, But They’re Not Winning Either

- Making money, battery-storage style?

Indian Banks Aren’t Failing, But They’re Not Winning Either

We’ve written about the banking sector quite a few times here at The Daily Brief . But with the Q1FY26 results now out, we figured it’s time to check in again. What’s really going on?

Now, one quarter doesn’t really materially change outcomes. And this quarter was no exception. Nothing blew us away. No surprises. No drama. But here’s the thing: if you zoom out just a bit, the bigger picture starts to look… well, a little bleak.

Over the last few quarters, the sector has been quietly sliding. Not falling off a cliff, but steadily losing its shine. Today, the banking sector looks like it’s walking on thin ice. And it’s easy to be caught off-guard by these results if you haven’t been paying attention.

This piece has a lot of interesting charts, so let’s dig in.

Credit Growth Has Been….Wobbly

If you’re betting on a bank, you’re basically betting that it’ll keep giving out more loans — and making money on them. That’s the simplest way to gauge whether a bank is growing: check how much new credit it’s disbursing.

Now, yes — loans only help if they’re actually paid back (defaults are a whole other story). But for now, let’s stick with the headline number of growth in banks’ loan books.

And that number is not great.

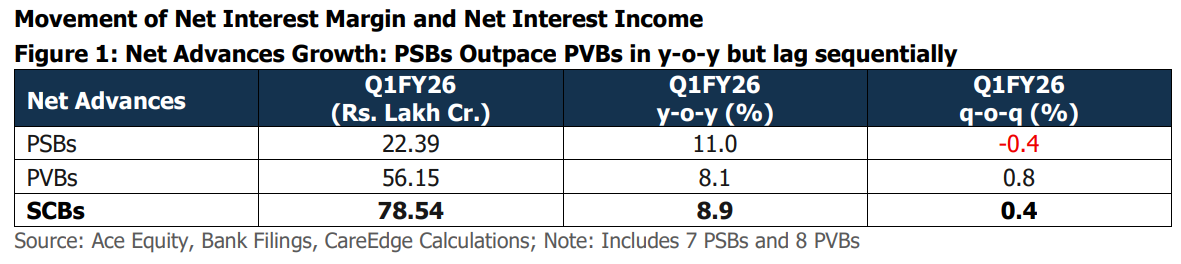

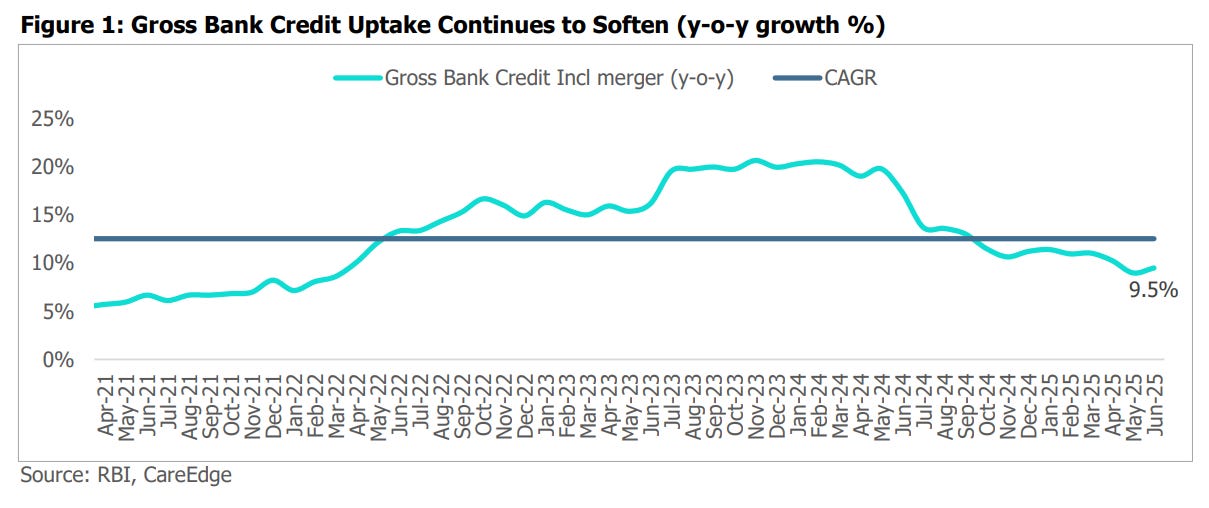

Credit growth across the entire banking system has been steadily slowing for several quarters now. In Q1FY26, overall loan growth came in at just 8.9% YoY. Private sector banks grew slow at 8.1%, while public sector banks were surprisingly stronger at 11%.

Why the divergence?

Well, public banks went all-in on priority sector lending — MSMEs, agriculture, rural loans — sectors that often find it hard to get credit in recession-like situations. These are sectors the government often nudges PSBs to support. Private banks, on the other hand, stayed cautious on these sectors — something we’ve covered in our last “Who Said What” episode. They focused on protecting margins rather than chasing loan volume.

So PSBs played the volume game, while PVBs played the margin game.

So what’s dragging growth?

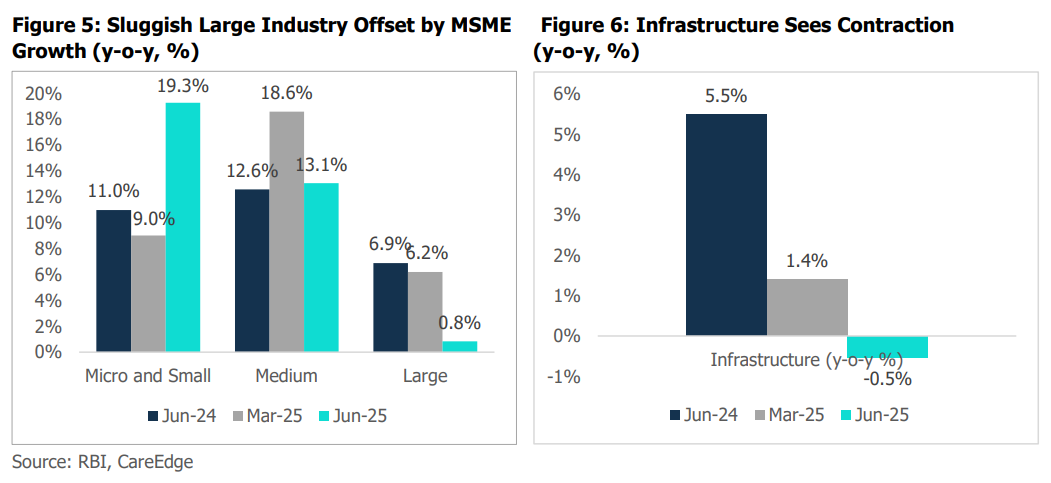

A big part of the slowdown is because large industries aren’t borrowing. India’s private sector has not been spending a lot on capital expenditure. Lending for large infrastructure projects has been cooling, too. Big companies are either flush with cash or hitting the bond market directly, but not investing in new capacity.

But while large borrowers are pulling back, MSMEs seem to be stepping up.

There’s a visible shift toward lending to small and medium enterprises — thanks to government push, formalisation efforts, and credit guarantee schemes like ECLGS and CGTMSE. It’s still a smaller piece of the pie, but it’s growing. However, as we highlighted in our last “Who Said What” episode, this is a nuance in this trend: lending to MSMEs may have increased in value, but decreased in volume. That is, only the bigger MSMEs may be getting large-ticket loans, while smaller SMEs are starved for credit. That trend might be at play in this shift.

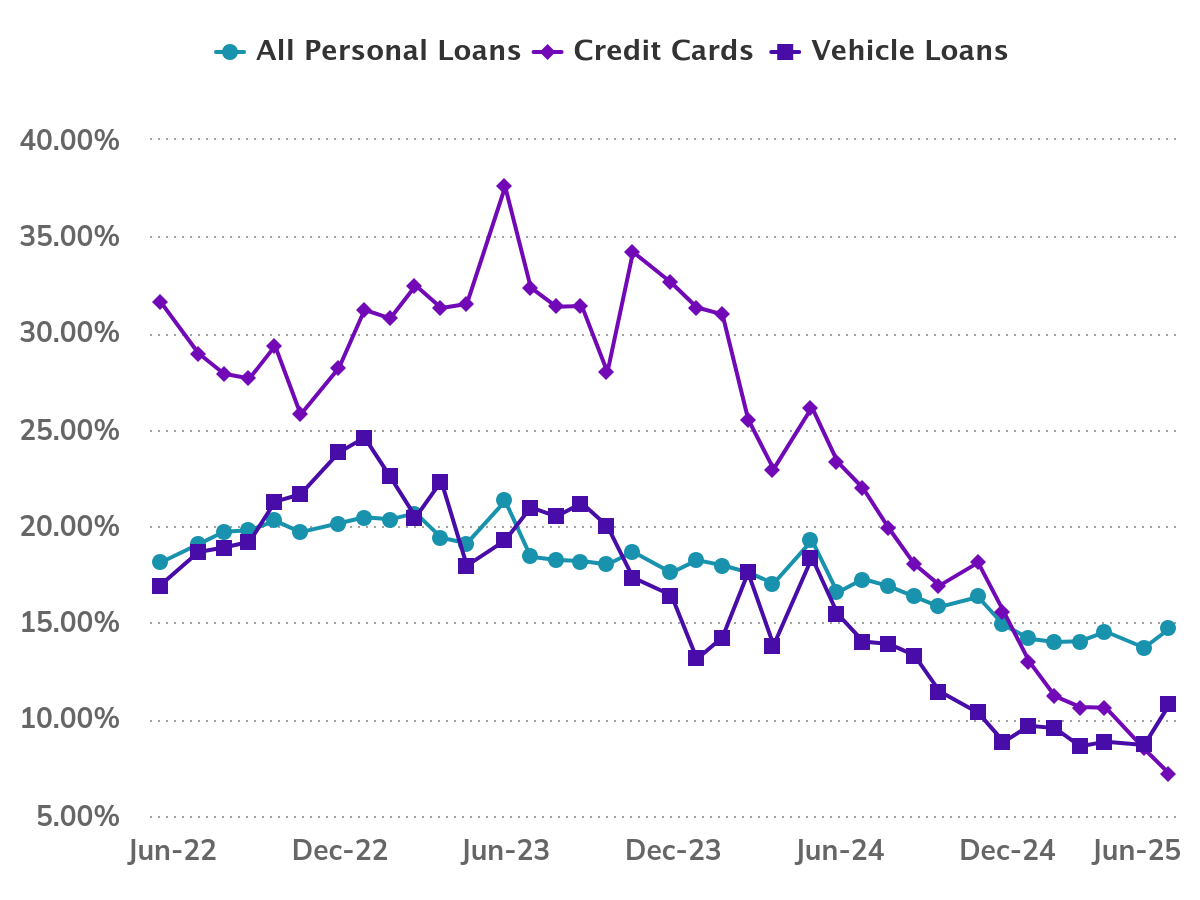

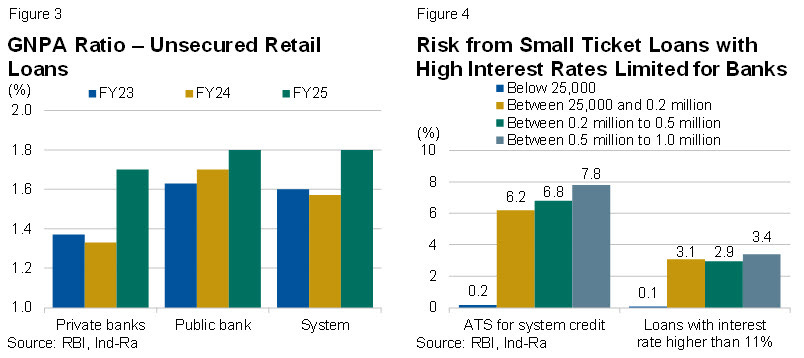

Another drag on banks’ growth has been unsecured personal loans — loans offered without taking any collateral.

Credit cards, personal loans, vehicle loans — all are showing signs of a cool-off. That doesn’t always mean that consumers aren’t willing to borrow. It’s more about banks pulling back, especially after a rise in loan stress and customers being close to defaulting on their loans.

Let’s talk about specific banks.

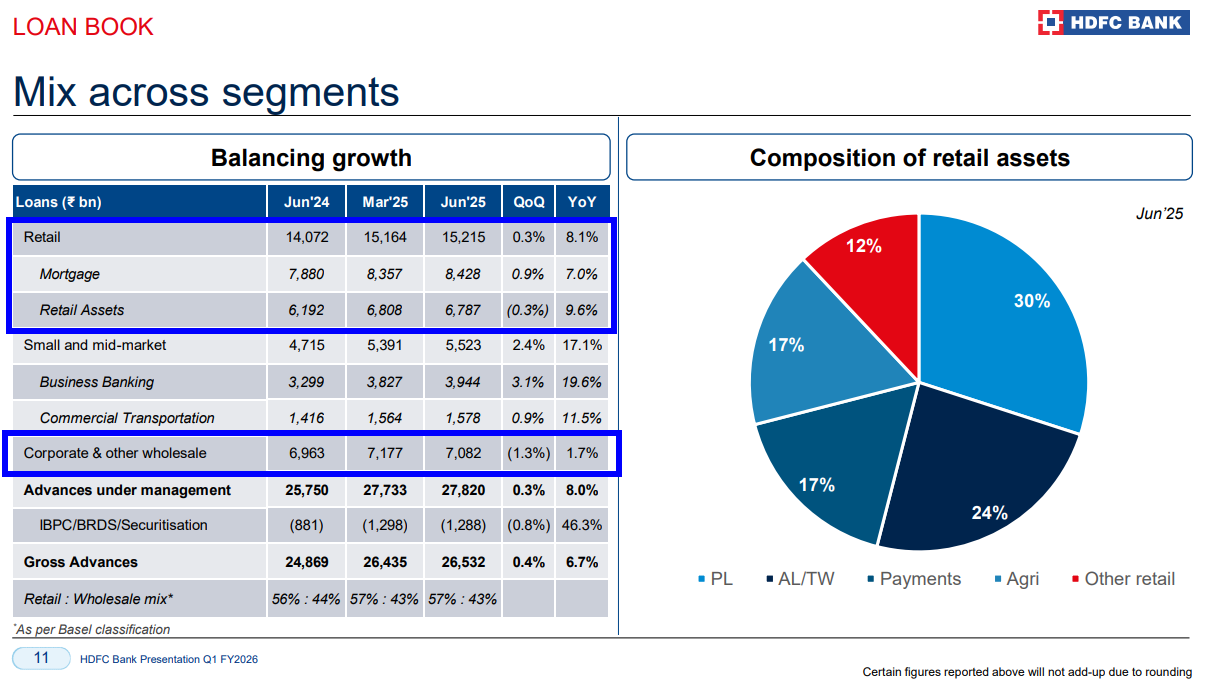

First, HDFC Bank: Corporate loans have remained flat, and retail loans recorded just a single-digit growth of 8%. The only real, double-digit growth came from small and medium businesses — which, to be fair, is still a small part of the book.

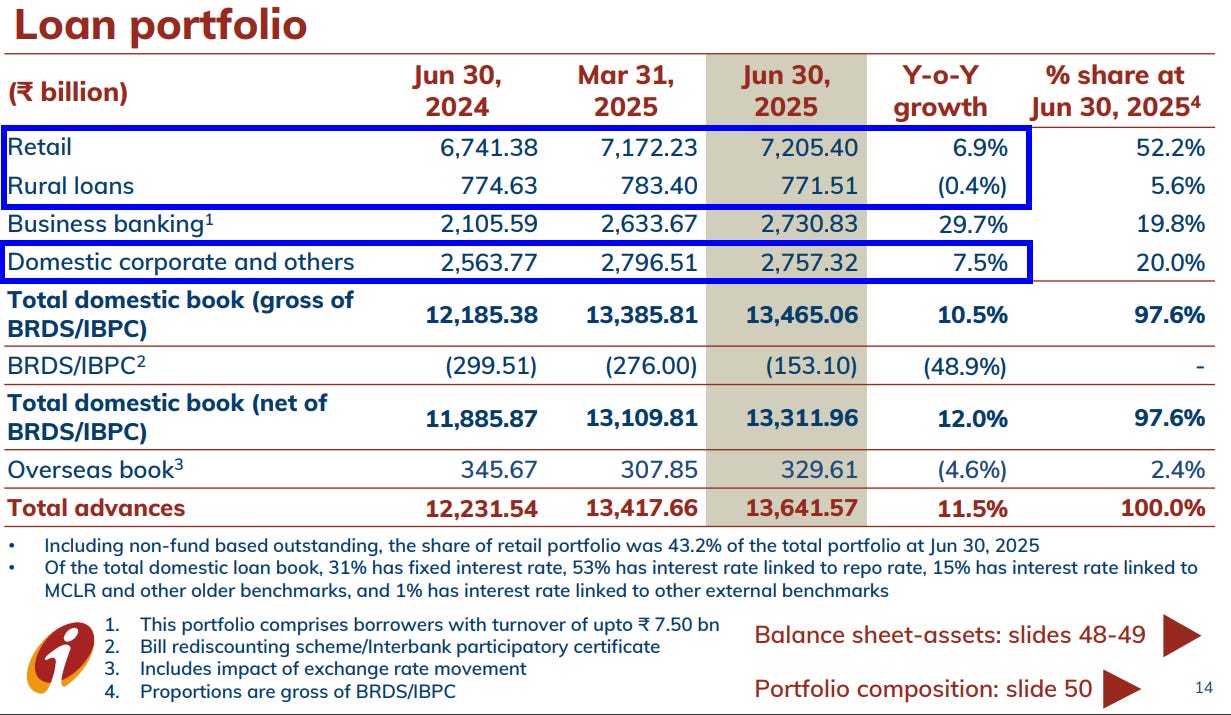

Second, ICICI Bank: The story doesn’t change much for ICICI. Corporate and retail growth was tepid, but SME-focused “business banking” grew 30% YoY.

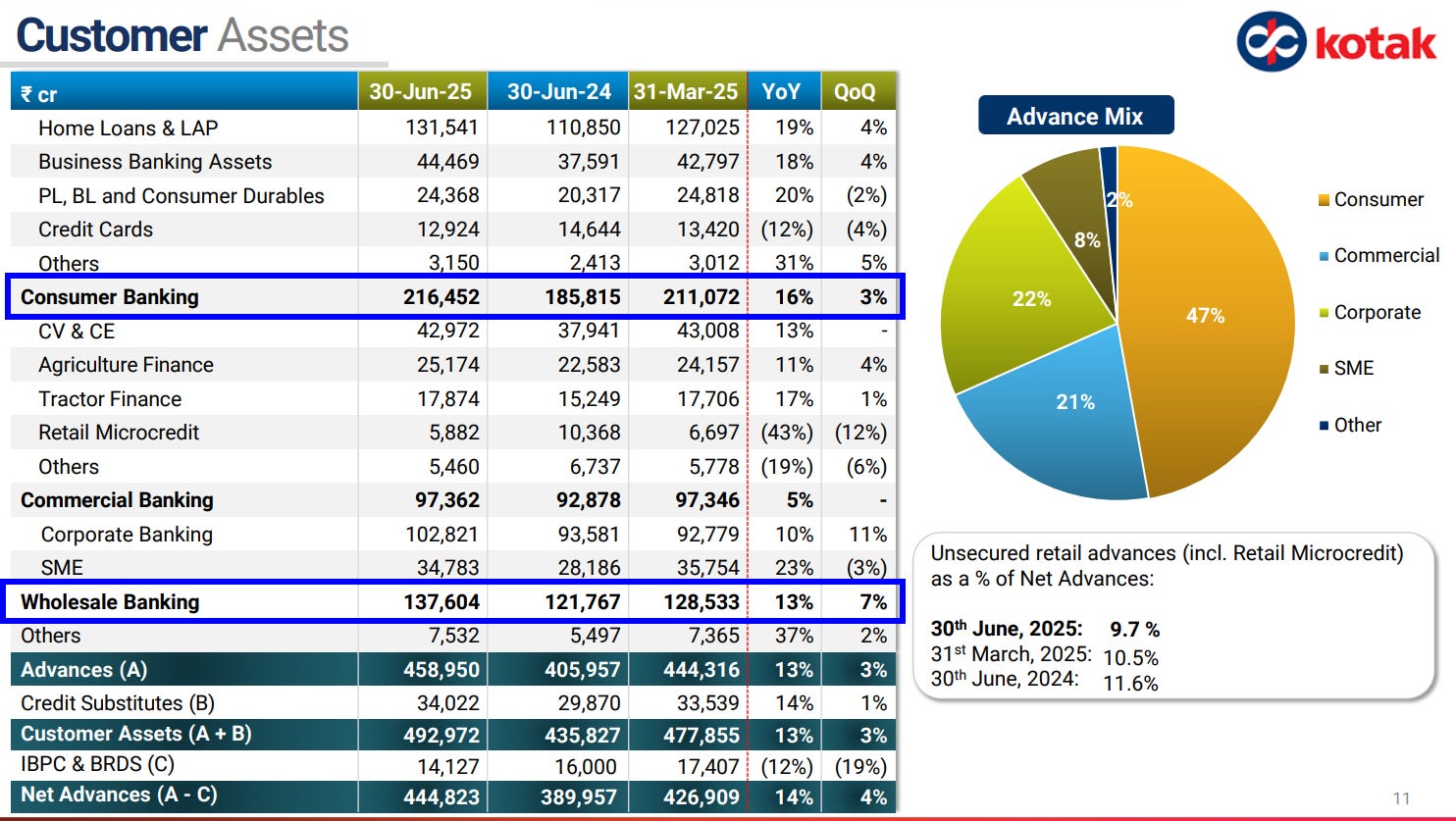

Third, Kotak Mahindra Bank: Now, Kotak is a bit of an outlier. Its consumer banking book grew 16%, and total advances rose 14% — much faster than the industry average. In fact, this might mean that Kotak has actually gained market share while others were being cautious.

Margins Are Getting Squeezed

If slowing credit growth wasn’t enough, banks are now hurting with shrinking margins.

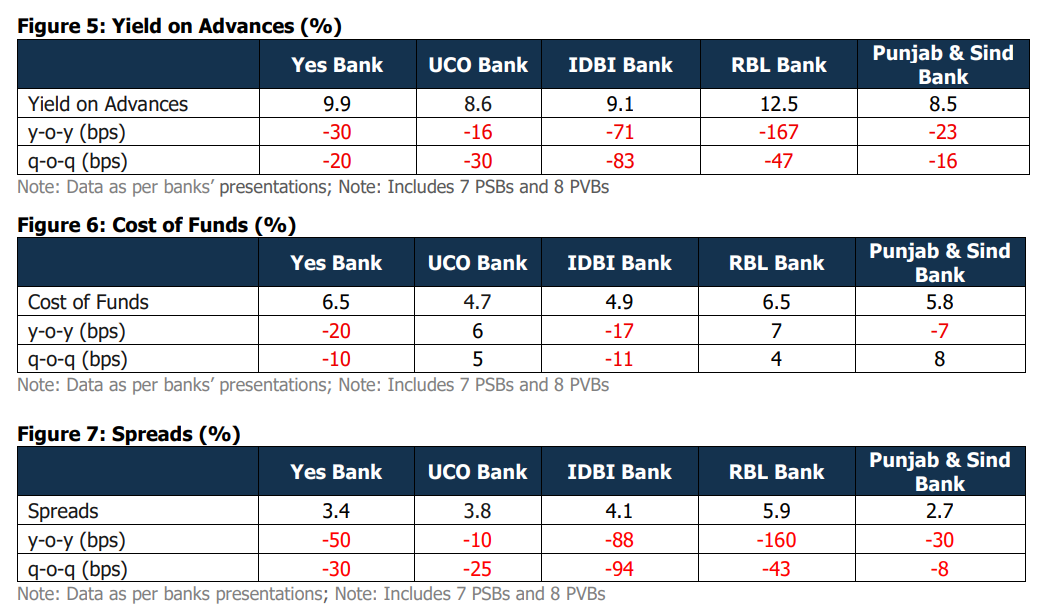

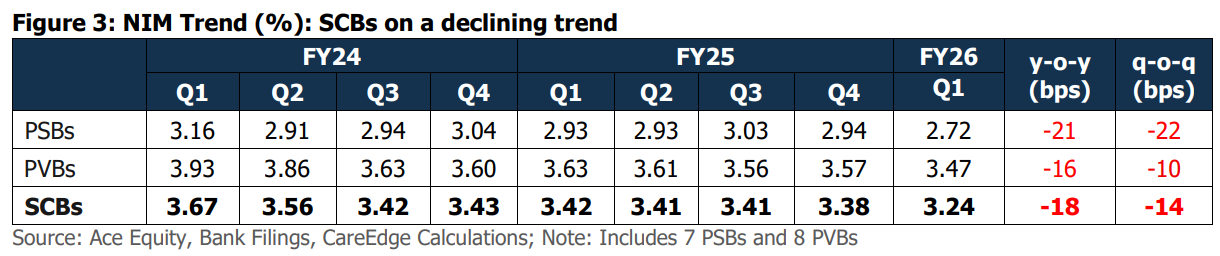

One of the most-watched metrics here is the Net Interest Margin (NIM). Think of it as what banks get to keep after paying for the money they lend out. In Q1FY26, NIM for the entire system dropped to 3.24% — the lowest in at least two to three years.

Why are margins falling? Turns out, the answer is pretty intuitive.

Earlier this year, the RBI cut repo rates by a full 1% . Most loans today are linked to external benchmarks (like the repo). That means banks were forced to lower lending rates almost immediately. This is called yields on advances .

But here’s the catch: the rates on bank deposits didn’t fall as fast. So the cost of funds for the banks (interest they have to pay on those deposits) remained more or less the same. This meant that banks were still paying depositors almost the same high rate, while earning a lot less from borrowers. A perfect recipe for margin compression.

While all banks felt the pinch, public sector banks saw bigger margin drops compared to private banks. Why?

For the same reason we discussed earlier — they are the ones dishing out loans to lower-yielding priority sectors — like agri, rural lending, and MSMEs. That helped them grow loan books, sure, but it came at the cost of profitability. Although, one may argue that it is actually the job of PSBs (or the government) to lend to these areas during phases of low growth. As a result, they do not have as much pressure to earn profit as private banks which stayed picky in contrast — lending less, but keeping spreads tighter.

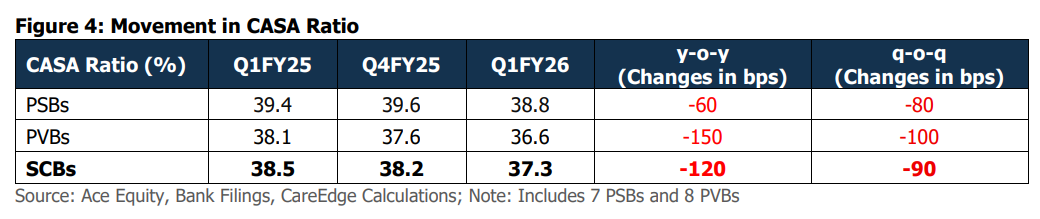

There’s another reason margins are under pressure: CASA (Current Account Savings Account) ratios are falling.

CASA deposits are a super-cheap source of funding for banks. But over the last few quarters, people have been moving money out of savings accounts and into higher-return options like term deposits or mutual funds. That means banks are now relying more on expensive sources of funds — which pushes up their overall cost of borrowing, and pushes down margins even further.

So here’s the situation:

- Banks are lending at lower rates (thanks to loans linked to the repo rate),

- But paying almost the same (or more) to raise funds,

- While also losing access to cheap deposits (CASA).

The result is obvious: squeezed margins, slower income growth, and even more pressure on already-cautious banks.

Treasury Gains: A One-Time Lifesaver?

Now, after all that bad news on credit growth and margins, you might wonder — banks would have reported depressing profit growth rates.

Honestly, the results would have been even worse, had it not been for treasury gains. Let us explain.

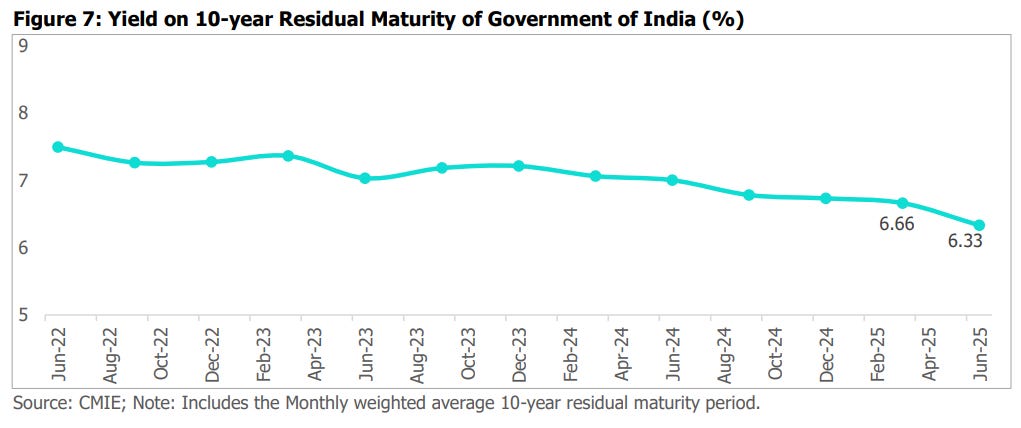

Banks don’t just earn money by lending to you and me. They also park a chunk of their money in government bonds. When interest rates fall, bond prices go up. And when that happens, banks can sell these bonds and make a neat profit — that’s what’s called a treasury gain.

In Q1FY26, treasury income acted like a floatie keeping the banks above water. On average, treasury income made up 0.40% of total assets, up from just 0.16% a year ago. For public sector banks, treasury income more than doubled this quarter. For private banks, it nearly tripled compared to last year.

This windfall came because bond yields dropped sharply — the 10-year yield fell 0.33% in the June quarter. That’s a big move in the land of bonds.

But here’s the thing, this kind of income isn’t sustainable. Why?

Because this treasury boost was driven by falling interest rates — partly owing to the earlier cut in repo rate. If the RBI doesn’t issue a fresh rate cut in the next quarter, banks would have to say a painful goodbye to gains.

Even the RBI has now moved from “cutting” mode to “liquidity absorption” mode — which means they’re trying to mop up excess liquidity, not add more. Translation: bond yields may not fall further, and could even go up slightly.

So… Should You Still Bet on Banks?

Look, banks didn’t report a disaster this quarter. On paper, the numbers weren’t horrifying. But that’s exactly why this quarter is so important — it looks fine on the surface, but under the hood, there may be serious cracks.

Credit growth is slowing. Margins are getting squeezed. The cost of funds is going up. And the cheap deposit engine — CASA — is stalling. On top of that, loan growth is being driven by smaller segments like MSMEs, while big industry and corporate credit have hit pause.

But banks did still manage to put out decent profits because of treasury gains.

So if you’re an investor asking “Can I still bank on banks?” — you may want to sit with that question a little longer. Because this is the kind of quarter that keeps you guessing.

Making money, battery-storage style?

As a team, we keep wading through all sorts of fascinating reports and research papers that people rarely talk about. Sometimes, we dig into these because they offer glimpses of the future, ideas that feel slightly mad, but also just plausible enough to wonder: what if ?

Some of these ideas we’ve even covered before for The Daily Brief. The report we’re talking about today is an analysis from energy think tank Ember, about batteries and India’s electricity markets.

How traders make win-win-win situations

But before we dive into what Ember is saying, let us tell you a fictional story about tomatoes.

Every morning, wholesale tomato prices at a sabji mandi start high. Restaurants need them for lunch prep, and households are shopping for dinner. By afternoon, as the day’s supply piles up and buyers thin out, prices crash. Tomato farmers become unable to find good rates.

That’s where middlemen traders come in. They buy in the afternoon slump, promising good prices to farmers while taking the risk of storing and protecting those tomatoes, and sell the next morning to you and me when prices recover. A win-win-win for the trader, the farmer, and the consumer.

Now, imagine if electricity worked the same way.

For most of India’s history, sadly, it hasn’t. This was true for when fossil fuel plants were the sole source of power. And now, as India tries to explore into a new energy frontier in solar, this problem continues to remain unsolved.

During sunny afternoons, India’s growing solar capacity floods the electricity grid with power. Think massive solar farms in Rajasthan pumping out thousands of megawatts when the sun is blazing hot. But here’s the thing: at 2 PM on a weekday, most offices have their ACs running efficiently, factories are in steady-state operation, and residential demand is low because people are at work. There’s more power than anyone needs.

So electricity prices on the wholesale market crash. With solar, though, the crash is far more pronounced — in Europe, for example, they’ve often turned negative!

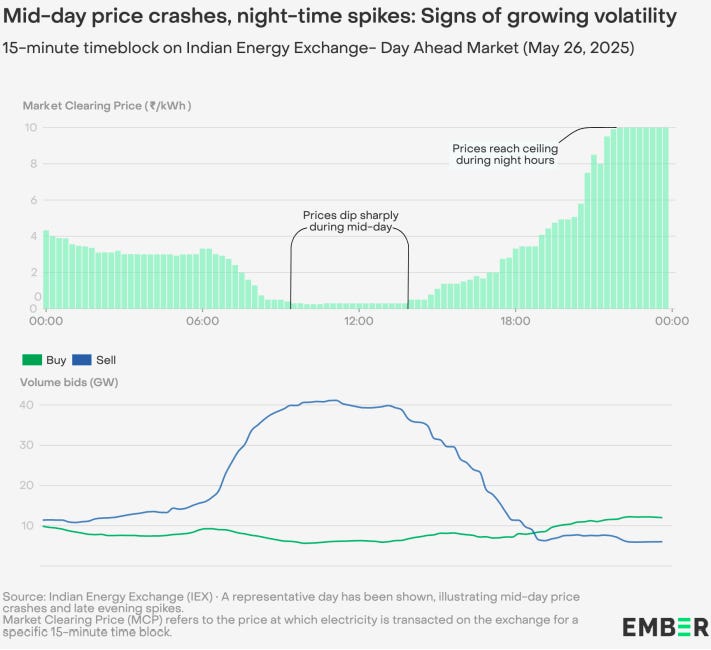

Then evening comes. The sun sets, solar generation drops to nothing, and suddenly people start coming home, switching on lights, TVs, and ACs. Demand rockets up just as solar supply vanishes. Power plants burning expensive gas or diesel rush to fill the gap. Wholesale electricity prices can jump tenfold in a matter of hours. There is immense volatility in prices during the day, with less win-win situations between power generators and consumers.

But what if, just like those tomato traders, someone could buy electricity in the afternoon when it’s dirt cheap, build an innovative form of storage, and sell it back to the grid in the evening when prices spike?

This is where batteries enter the picture. That’s exactly what Ember’s report is exploring.

Batteries, the savior of electricity markets

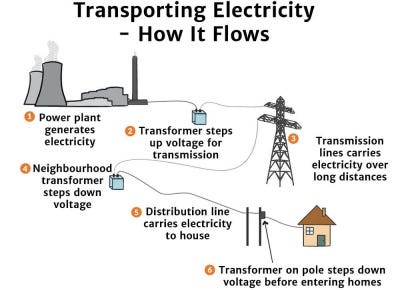

To understand why this matters, you need to know how electricity is bought and sold in India. Most people think power just flows from power plants to their homes through government wires. That’s partly true, but there’s a whole hidden market in between.

Think of it like this: Power plants are like factories making a product (electricity). Your local electricity distribution company (like BEST in Mumbai) is like a retailer who sells you that product. But between the factory and retailer, there’s a wholesale market —the Indian Energy Exchange (IEX).

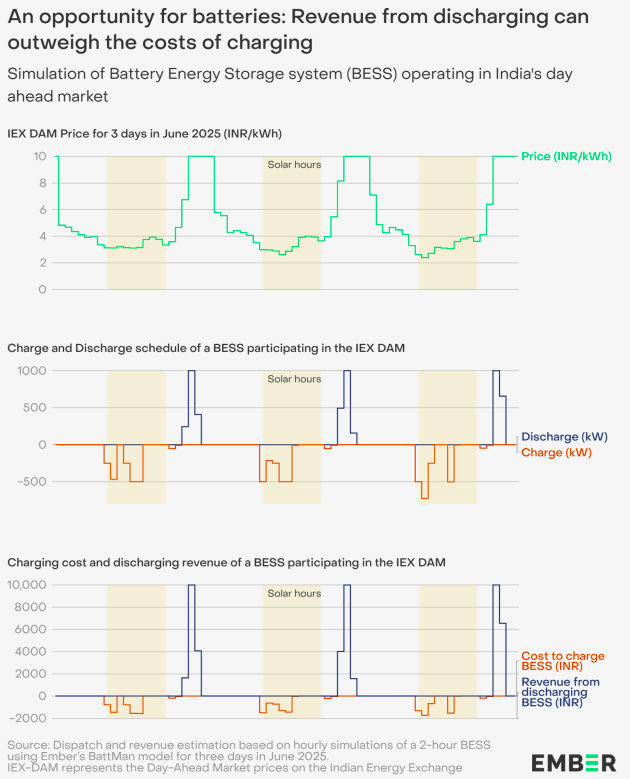

Every day, power plants and electricity distribution companies come to this market. In the morning, a distribution company might realize, "Oh no, we need extra power for the evening peak. " They place buy orders. A gas power plant might say, "We can supply that, but gas is expensive, so we need 8 rupees per unit. " If no cheaper option exists, the deal happens at that price.

But at noon, when solar plants are producing like crazy, they come to the market saying, "We have too much power, please someone buy it for just 1 rupee per unit, or even less! " The same electricity that costs 8 rupees in the evening is available for 1 rupee at noon.

Until recently, this price gap was just an unfortunate reality. Nobody could do anything about it because it was always hard to build storage facilities for power generated through coal. For one, it was far cheaper to keep the coal un-burnt rather than build new storage for it. But moreover, shutting down and starting up coal power plants is itself an extremely expensive affair.

But solar power — and batteries — change everything. There are minimal costs to shutting down and starting up a solar panel. Every bit of power generated (through the Sun) is essentially free because it’s unlimited.

How to build a battery storage business

Here’s how the business works, step by step.

Imagine you’re an entrepreneur who decides to set up a battery storage facility. Firstly, you need serious money . This isn’t a Duracell in your flashlight — we’re talking hundreds of crores for an industrial-scale battery system. Picture a warehouse filled with thousands of lithium-ion cells, similar to what goes into electric cars but packaged for the grid.

You connect this battery facility to the electricity grid and register as a trader on the IEX. Now you’re ready to play the game.

Every morning, your team (or your algorithms) studies the market. You can see that yesterday at 2 PM, electricity was trading at ₹2 per unit. By 8 PM, it hit ₹9. You predict today will be similar, it’s another sunny day, and evening demand patterns don’t change much. So you decide to buy low and sell high the next day accordingly.

But here’s a crucial detail—batteries aren’t perfectly efficient. When you charge a battery with 100 units of electricity, you can only get back about 85 units — like a few tomatoes that spoil overnight. So your real cost is higher—around ₹2.35 per unit stored.

Even after accounting for losses, though, you’re selling at ₹9 what you bought at ₹2.35. That’s a hefty profit margin .

Do this every day, and you have a business with a win-win-win proposition. Your entire ecosystem wins with stable electricity supply.

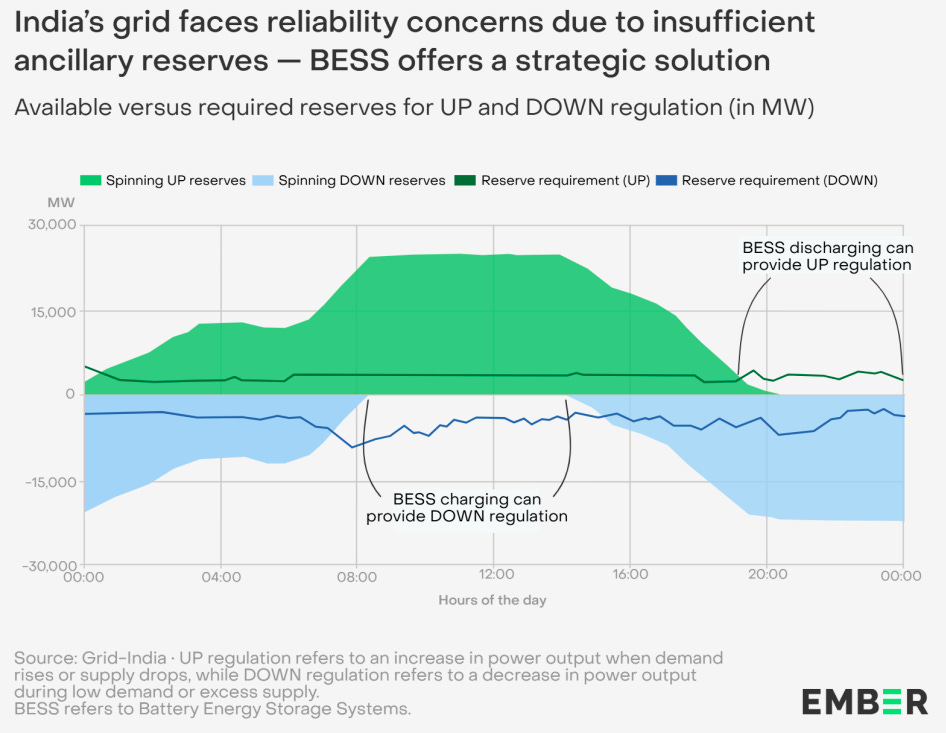

But it gets better. The grid operator—the government agency managing electricity flows—has another problem. The frequency of alternating current (AC) electricity needs to stay exactly at 50 Hz. Too much power, it goes up. Too little, it goes down. Even small deviations can damage equipment and cause blackouts.

Batteries are perfect for fixing this. They can absorb excess power or inject needed power in milliseconds. So the grid operator offers extra payments for batteries that provide this “frequency regulation” service.

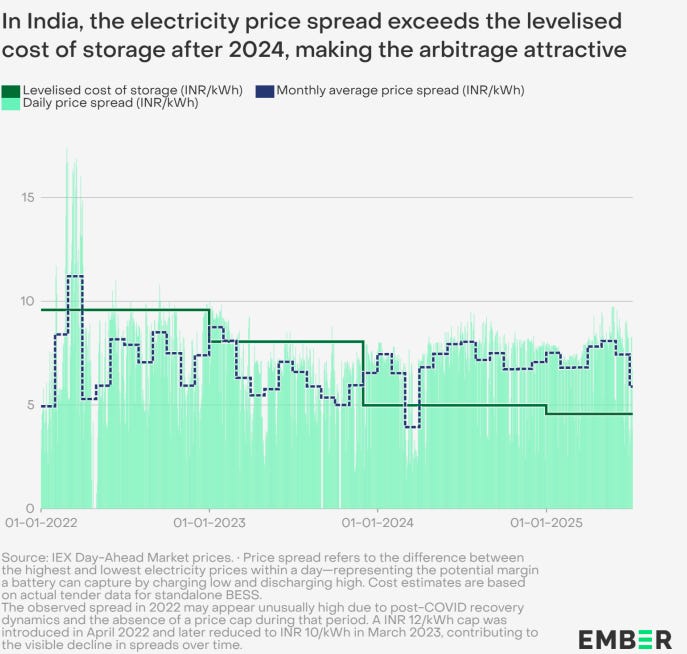

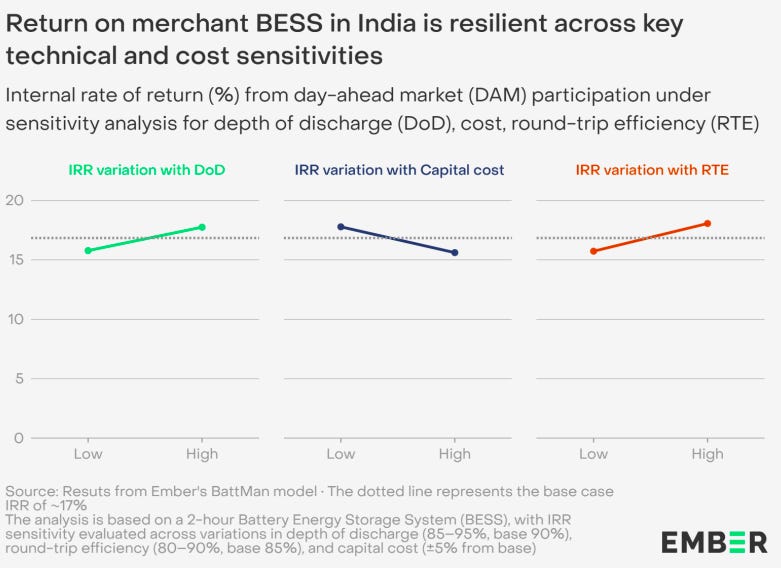

Ember’s report crunches the numbers and finds something remarkable about solar storage that was not true for coal: For the first time in India, such a business can generate an impressive 17% IRR.

This is a profound shift. For decades, anyone building power infrastructure in India wanted long-term contracts. If you built a solar plant, you’d sign a 25-year deal with a state government to sell power at a fixed price. Banks loved this because returns were guaranteed.

But merchant batteries don’t need contracts. They’re free agents, making money from short-term market volatility itself. It’s a different business model which doesn’t require you to build power plants.

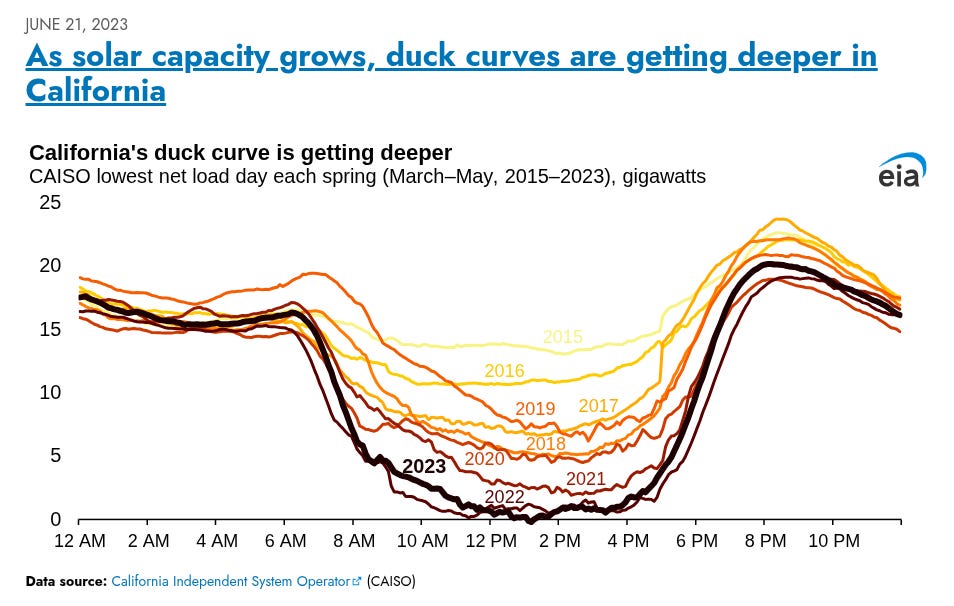

And we know this model works really well to reduce price unpredictability for consumers. In California, the evening price spikes have mellowed considerably. The "California duck curve "—the shape of daily power prices that created the battery opportunity—is flattening as more batteries enter the market. However, as a result of more battery players, the arbitrage opportunities also reduce.

So why isn’t everyone rushing to build batteries?

The answer lies in the gap between spreadsheet models and ground reality. When you actually try to build and operate a merchant battery in India, you run into a bunch of problems that reports often gloss over.

First, consider what you’re actually building . A grid-scale battery isn’t something you order online. You need land near electrical substations, permits from multiple authorities — pollution control, fire safety, electricity regulators, and specialized equipment — most of which is imported from China or Korea. In current global supply chains, the prices can swing wildly and delivery times can stretch.

Then there’s the grid connection itself. You can’t just plug a giant battery into any electrical socket. You need tools that help you transmit power —transformers, switchgear, safety systems. The local grid also needs to be able to handle your charging and discharging. In many parts of India, the grid is already congested. Too many solar plants in Rajasthan are trying to send power through the same transmission lines.

The technology risk is real too. Batteries need ideal temperatures. Too hot and they degrade faster or even catch fire, too cold and they won’t perform. Every charge-discharge cycle ages them slightly, slowing them down after 1000 cycles. Your business model assumes the battery lasts 10-15 years, but what if it degrades faster?

There’s also regulatory risk. Indian electricity markets are heavily regulated. The government caps maximum prices, sets trading rules, and can change market structures. What if regulators decide battery traders are making “too much” profit and impose new fees, or change market timing or settlement rules?

In the face of all this, how do you get a bank to finance this business model? Banks understand solar and wind — predictable technologies with long-term contracts. But do they understand batteries? It’s a business that requires complex technology and dealing with unknown regulatory risks. Banks may charge much higher interest rates.

Even day-to-day operations are challenging. Running a battery plant requires specialized skills. You need electrical engineers who understand grid operations, traders who can navigate power markets, safety experts who can prevent fires, and managers who can handle the regulatory maze.

So where does this leave us?

Ember’s report is right about the opportunity. The math does work—if you can execute perfectly, if regulations remain stable, if too many competitors don’t enter, if technology performs as expected, and if you can manage the operational complexities.

But that’s a lot of ifs and buts .

None of this means battery storage is a bad idea. In fact, it’s essential for India’s energy transition. As solar and wind capacity grows, we desperately need batteries to balance the grid. The question is whether the merchant model—with all its risks and complexities—is the right way to build this infrastructure.

Tidbits

- India’s rare earth crisis is now hitting where it hurts — Q2 EV deliveries.

Bajaj Auto has admitted it will only meet 50–60% of its electric two-wheeler and 70–80% of three-wheeler production targets, citing acute shortage of rare earth magnets. These components are crucial for motors and have been stuck in Chinese ports due to new export restrictions imposed in April. While Bajaj explores stopgap fixes — including switching to light rare earth-based motors — its CFO confirmed the company may only fully de-risk from China by March 2026.

Source: Reuters

- Amid the quick commerce battle, another quiet yet telling move is happening.

Alibaba’s Antfin is selling its entire 2.08% stake in Eternal for ₹53.75 billion (~$613 million) via a block deal. The sale is priced at ₹285 per share — about a 4.6% discount to Eternal’s last close. While a small stake, the move signals China’s strategic retreat from Indian tech — part of a larger trend since geopolitical tensions and FDI restrictions ramped up.

Source: Reuters

- The power sector seems to be in flux.

India’s Bharat Heavy Electricals (BHEL) reported that its first‑quarter net loss more than doubled—from ₹211 crore to ₹455 crore—driven by slowing power demand and rising operating expenses. Its share price also fell nearly 5% following the disappointing results.

Source: Reuters

- It isn’t always rosy in India’s liquor sector.

India’s leading winemaker Sula Vineyards saw its quarterly profit plunge by nearly 87%, falling to just ₹19.4 million, as urban consumers cut back on affordable wines amid wage stagnation and cost pressures. The strong performance in its wine tourism segment—up 22%—couldn’t offset the sharp decline in its core sales.

Source: Reuters

- This edition of the newsletter was written by Kashish and Krishna

Join our book club

Join our book club

We’ve started a book club where we meet each week in JP Nagar, Bangalore to read and talk about books we find fascinating.

If you think you’d be serious about this and would like to join us, we’d love to have you along! Join in here.

Have you checked out The Chatter?

Have you checked out The Chatter?

Every week we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Go check out The Chatter here.

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()