Triple your Investments!!!

Don’t get too excited, I am not talking about some Ponzi Schemes to double your money overnight. I am talking about genuine schemes that are legal as well as are running from past few decades. But let me tell you first, there is no sure shot way of doubling money quickly. It requires immense knowledge of capital market like Rakesh JhunJhunwala or patience for long term. Here I am going to elaborate long-term money doubling schemes. Before we proceed you should first learn about the Thumb Rule 72.

What is Thumb Rule 72?

Rule 72 or Thumb Rule of 72 gives you estimation of two things:

The time period to double your money at given rate of return.

The rate of return at which your money will be double at given time-period.

Suppose you wish to invest in Bank Fixed Deposit at interest rate of 8% p.a. than according to Rule 72 your invested money will be doubled in 72/8 = 9 years. This means if you invest Rs.1 lakh in Bank Fixed today than you will get Rs.2 lakhs if you stay invested for 9 years.

Similar, if you wish to double your money say in 5 years than you will have to invest money at the rate of 72/5 = 14.40% p.a. to achieve your target. This means if you have Rs.1 lakh and you would need Rs.2 lakhs in 5 years than you will have to invest it in the financial products which gives you return at 14.40% per annum to achieve your target.

Though Rule 72 gives you rough estimates but it becomes very handy at the time when you have no access to calculator or do not know much about compounding or discounting. time when you have no access to calculator or do not know much about compounding or discounting.

10 Best Money Doubling Schemes in India

Tax-Free Bonds

Tax-Free Bonds are not issued every year. But fortunately this year Government has granted permission to seven state run entities to issue tax-free bonds amount to Rs.40,000 crore. We have already witnessed high demand of tax-free bonds issued by PFC and NTPC and there are plenty more in the pipeline.

Coupon Rate offered by tax-free bonds for 2015 series is around 8.20% to 8.50% per annum (Tax-Adjusted Return) depending on the tenure. So if you invest in one of these tax-free bonds you can double your money in approx. 8 to 9 years.

Corporate Deposits/Non-Convertible Debentures (NCD)

In the current scenario of rate cuts by RBI, many investors are looking for better investment avenues and whose risk appetite is bigger invests in Corporate Deposits. Since Corporates and NBFCs do not enjoy RBI backing like banks, the interest rates offered by them are quite high as compared to bank fixed deposits. Point to note is that NCDs are issued both by Companies including NBFCs while corporate deposits are only issued by Companies.

NCDs and Corporate Deposits give rate of return of around 9% to 10% per annum depending on the tenure and their CRISIL or ICRA ratings. Thus investing in these would get your money doubled in approx. 8 years.

National Savings Certificates

National Savings Certificates are issued by Postal Department of India and are considered one of the safest investment avenues. NSCs come with a fixed interest rate and fixed tenure i.e. for 5 years and 10 years. No TDS would be deducted on the maturity amount and also you would get tax-deduction up to Rs.1.50 lakhs u/s 80C. In addition, NSCs could be used as a collateral security to get loan from banks.

The interest rates offered by 5 years NSCs is 8.50% p.a. while 8.80% p.a. for 10 years NSC. Since both rate of return and time period is fixed under NSCs there is no need to use rule 72 and the returns would be Rs.1,516.2 for Rs.1,000 invested in 5 years NSC and Rs.2,366 for Rs.1,000 invested in 10 years NSC.

Kisan Vikas Patra (KVP)

Kisan Vikas Patra was abolished in 2012 but reintroduced in the current financial year. The reason for discontinuance of KVP was no check on the source of income for buying KVP. People used to buy KVP in cash (black money) and after the maturity the black money turns into white money. There was no requirement of the PAN and anyone with cash could buy KVP from Post-Office. Thus KVP was mainly used to turn black money into white.

This loophole has been done away with while reintroducing KVP, now every investor buying KVP in cash of Rs.50,000 or more has to mandatorily furnish his/her PAN number. Currently KVP is offering interest rate of 8.70% p.a. which results in money doubling in 100 months i.e. 8 years and 4 months.

Public Provident Fund (PPF)

Public Provident Fund is the second most popular scheme of Government after Employee Provident Fund Scheme. PPF enables every class of earner i.e. self-employed, salaried or even government employee to save and invest as low as Rs.500 per annum. PPF is one of the safest and most trusted scheme having minimum contribution of Rs.500 per year and a lock-in period of 15 years.

Rate of Return are fixed each year by Government and remain effective for that fiscal year. For the financial year 2015-16, applicable rate of return is 8.75% p.a. which translates into money doubling in 8 years 3 months. Since the lock-in period of PPF is 15 years your money gets multiple folds at the time of maturity.

Bank Fixed Deposits

No matter where market goes or how much RBI cut rate, Bank Fixed Deposit always remains the first choice of every Indian investor. There are many cons and pros of investing in fixed deposit. Such as fixed deposit up to Rs.1 lakh is insured by RBI while the returns after tax may not beat inflation. But still for short term period bank fixed deposits are preferred over other investment options.

After the recent rate cut of 50 bps (0.50%) by RBI, almost all banks have reduced the interest rate on FD either by 0.25% or 0.50% p.a. Currently FD interest rates varies between 8% to 9% p.a. So to double money by investing in bank fixed deposit would take 8 years to 9 years.

Mutual Funds

Investor who is willing to take little risk may choose mutual funds to earn better returns. There are varied types of mutual funds namely equity oriented, debt oriented, ELSS, Balanced or Hybrid Mutual Funds etc. Each type of fund has its own pros and cons and may not be suitable for every investor. Such as if you are investing for your child education and have enough time of 15 to 18 years than you can go with equity oriented funds but if you are looking for short term financial goal like accumulating money for down payment of your dream house than you should go with debt oriented fund. Likewise if you are a new investor and want to dip your fingers into stock market than it would be wise to start with balanced funds as it would give you experience of both debt and equity instruments.

Returns of mutual funds varied from fund to fund and the tenure you choose to invest. But if we go by the normal perception, in long term mutual funds tends to give return of 12% to 15% p.a. Thus you can double your money by choosing mutual fund route in approx. 5 years to 6 years.

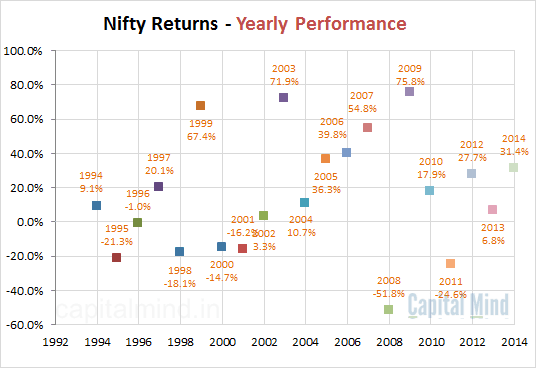

Stock Market

“High Risk High Reward”, those who believe on this statement is definitely indulged in stock market. There is no certainty of return in stock market. You can earn as much as multifold returns in a years’ time or can run out of money in months’ time. Investing or trading in stock market needs both technical as well as fundamental knowledge.

Gold/Gold ETFs

Love for the Gold is irresistible for Indian. Not only women are attracted towards its glitter but men also inclined towards it. In India, Gold is not only considered as an investment avenue but it is also given as a gift at the time of wedding. Gold is symbol of wealth and we Indian tend to collect it throughout our life.

Though the returns of gold are highly volatile but still it manages to give CAGR of 22% over past 5 years. This translates the doubling of invested money in 3 years to 4 years.

Real Estate

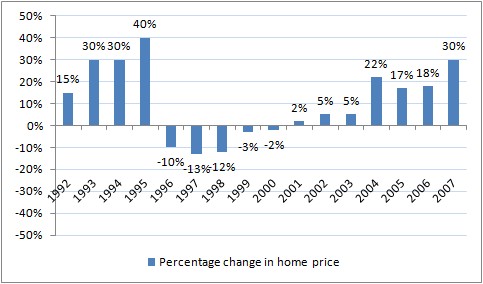

Real Estate

Real Estate investment is not everyone’s cup of tea. It requires huge capital to invest to generate a considerable return. Since tracking average return of real estate is not possible I have considered example of Gurgaon which has become the hub of industries from a small village. If you have invested in Rs.2 lakh in Gurgaon in 1980, it would have resulted in Rs.2 crore now i.e. CAGR of 15% over 34 years. Though investment in real estate looks too alluring but it requires pretty long time period for a hefty returns.

Taking a return of 15% p.a. we can calculate that money gets doubled in just 5 years but it may not be correct because the returns are totally depend on demand and supply. Place like Bangalore has become the hub while on the other side Mysore and other cities close to Mumbai has nowhere near.

The Bottom Line

Invest 75 % of the capital into Fixed Income schemes via FD's , PPF's , POMIS , KVP's , NSC which are guaranteed to double your investment in 10 years and 25 % of the capital into stock markets via mutual funds,Gold ETF's, picking a combination of Large cap, Mid cap and Small cap stocks where "High Risk High Reward" is in action which can triple your investments.

Happy Investing....;-)

Credit - simple interest.in