Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- What’s the point of a Whoop?

- The unglamorous reforms that actually work

What’s the point of a Whoop?

Last week, Whoop raised $575 million, at a 10 billion dollar valuation.

We generally don’t like talking about valuations here. But we’ll make an exception, because it’s something we’re personally interested in. One of our writers, Krishna, has been using an Apple Watch for about a year, works out regularly, and has been reading about health wearables for a while. For months, he has been on the fence about getting a Whoop. Not that he doubts that it tracks things; he just keeps asking himself if there’s a point to having all that data.

That, it turns out, is perhaps the most fundamental question you can ask about this industry right now. More, perhaps, than we realised at first.

Here’s what Krishna found, digging through this rabbithole.

The band that started it all

Our story starts with Fitbit .

Fitbit launched their first device in 2009. This was a small clip you could wear on your waistband. It would count the steps you took, and tracked your sleep.

It was a hit. There were pedometers before this, but nobody had done like this before — not well anyway. Revenue grew from about $5 million, in 2010, to $745 million by 2014. By the time they went public in June 2015, they held over a quarter of the entire global wearables market, shipping 21 million devices that year. For a company that essentially made a glorified pedometer, that was a remarkable position.

Then, two things hit them simultaneously.

One, Apple launched the Watch . Here was a device that did everything Fitbit did, but also handled your calls, messages and payments. And it kept getting better with every software update. Xiaomi entered from the other direction, with the Mi Band, doing the same basic fitness tracking for under $15. Fitbit was crushed in the middle. According to IDC’s Worldwide Wearable Device Tracker, by 2017, Xiaomi and Apple had entirely supplanted Fitbit from the top of the market. Fitbit’s SEC filing for FY2017 shows its revenue falling from $2.17 billion to $1.61 billion in a single year. The units it sold, too, dropped from 22.3 million to 15.3 million.

But the intense competition was only part of the story. There was also a deeper failure.

Over those years, Fitbit had accumulated health data from tens of millions of people. By 2016, with the Charge 2 , they could even measure heart rate variability: the millisecond variation between heartbeats that tells you how much your body has really recovered from stressful activity. But they never built the layer that turned any of that data into something personalised and meaningful. They showed you a nightly number. They could tell you how many hours you slept, for instance, but not what it meant for your body, specifically, or what to do about it.

As a Harvard Business School analysis put it, Fitbit never built an ecosystem around itself, and once cheaper devices could do the same counting, there was no reason for anyone to stay. All that data simply sat there for years, unused. Google bought the company in 2021 for $2.1 billion — less than a quarter of its peak — and has been winding it down ever since.

The Fitbit saga left one question open: did any of this actually matter, or was it just collecting vanity metrics? That is the question Apple Watch answered first.

The Swiss knife on your wrist

The Apple Watch is a fitness wearable, but it isn’t just that. It is the Swiss knife of wearable technology — calls, messages, payments, navigation, and fitness tracking, all in one device. You couldn’t beat it if all you offered was fitness tracking.

But what Apple Watch did for this story is bigger than the competition. In September 2018, they launched the Series 4. This came with something that had never existed in a consumer product before: FDA clearance for ECG recording and atrial fibrillation detection . Atrial fibrillation is a heart rhythm disorder which significantly raises stroke risk. A large number of people carry it without any symptoms at all. The Apple Heart Study, run with Stanford Medicine and published in the New England Journal of Medicine, enrolled over 400,000 participants and proved that a device on your wrist could detect it before you felt anything.

That settled the question: a consumer wearable could do something genuinely medical. The ambition of preventive health monitoring was no longer theoretical.

But the Apple Watch was still a generalist device. Health was one feature, among dozens. This opened the room for specialists. If a company could offer specialised health intelligence as the whole product, it could open a new niche. This is what Whoop and Oura brought to the picture.

The subscription body

Whoop was founded in 2012, in Boston, by Will Ahmed — a Harvard squash captain obsessed with one question: why do equally trained athletes recover at such different rates ? He spent years with the medical literature, and finally landed on heart rate variability as the answer. You couldn’t get this from a single reading; you needed to study patterns over months — your personal baseline, what normal looks like for your body specifically, and how your body behaves when something is starting to shift, often days before you actually feel it.

This became the basis for his first commercial product, launched in 2016 at $500. But in 2018, Whoop made a decision that changed the business: they stopped selling the device. Instead, they gave it away for free, with a $30-a-month membership. The device, after all, was just a sensor. What made it valuable was their health intelligence , which only gained value as you spent time with the band. Within six months, the platform learns your baseline. After a year, it knows exactly how your body responds to poor sleep or overtraining. Walk away, and you lose all of that. According to disclosures, Whoop has now accumulated over 24 billion hours of physiological data from its members.

Oura worked on the same logic, but built into a ring. The Finnish company was founded in 2013, and launched via Kickstarter in 2015. It got an early credibility boost when Stanford Research Institute independently validated its sleep tracking accuracy — without any tie-up with Oura. Then, during COVID, the NBA used Oura rings in their bubble to monitor player health. A UCSF study showed the ring could detect infection before symptoms appeared. That was when it went beyond a sleep tracker. Today, Oura has sold 5.5 million rings, and has raised $900 million at an $11 billion valuation.

Amazon entered this market in 2020 with the Halo band. It came in with unlimited capital, global distribution, and Alexa built in. It shut the project down in 2023. After all, building a sensor isn’t hard; building models trained for years on millions of people’s physiological data is.

That accumulated data also started attracting a very different kind of attention.

When wellness meets medicine

These devices are legally classified as wellness products, not medical devices. That isn’t a trivial difference; under US law, a product that encourages healthy behaviour but steps clear of clinical claims can largely avoid FDA oversight. The moment you claim your device can diagnose or prevent a disease, however, you become a regulated medical device. That obliges you to run clinical trials, seek premarket approval, and wade through years of process .

And so, the entire industry has been trying to get as close to that line as possible without crossing it.

This came to a head in a clash between Whoop and the FDA, last year. In April 2025, Whoop received FDA clearance for its ECG feature. But in July 2025, the FDA sent Whoop a warning letter. Its may have approved Whoop’s ECG tracker, but its blood pressure monitor still made it a medical device that lacked FDA clearance. It went so far as to call the product both “adulterated” and “misbranded.” Whoop’s founder Will Ahmed went on CNBC and publicly refused to remove it — arguing it was a wellness feature, not a medical device. The standoff lasted until January 2026, when the FDA updated its own guidelines, effectively moving the line in Whoop’s direction.

Whatever this regulatory back-and-forth might indicate, the company sure draws a lot of medical investors .

Whoop’s recent round includes Abbott Laboratories — the company that makes the FreeStyle Libre, the continuous glucose monitor prescribed to diabetics worldwide — and Mayo Clinic, one of the most respected hospital systems in the world. Dexcom, which makes the other dominant glucose monitor, participated in Oura’s 2024 fundraise, and announced a product integration through which both devices share data. These are not fitness investors. They are medical device companies and hospital systems. And they’re betting on a specific future: that continuous health monitoring becomes the standard front door to preventive healthcare, and that they’re inside the platforms that get there first.

The fundamental question

Which brings us back to where we started. Is there a point to this?

For one specific thing, definitely . The Apple Heart Study proved, across 400,000 participants, that a consumer wearable could catch atrial fibrillation before it caused serious harm. A separate study in the American Heart Association’s journal Circulation confirmed similar results. That evidence is real and peer-reviewed.

Beyond that, things are complicated. An independent study that tested Apple Watch, Whoop, Oura, Garmin, and Polar simultaneously against clinical-grade sleep monitoring equipment found that even the best consumer device correctly classified sleep stages around 65% of the time. Now, classifying sleep stages from a wrist sensor is genuinely hard, and they only claim to give estimates . But it’s important to remember that there’s a major difference between an estimate and a clinical measurement.

But the question we began with isn’t whether these wearables measure things; it is whether there’s a point to measuring things. Do they actually change behaviour ?

It isn’t clear that they do. A systematic review of clinical trials found no evidence of continued behaviour change beyond the original study period. Research by Endeavour Partners found that more than half of people who bought a modern activity tracker eventually stopped using it. Knowing your recovery score is red only matters if you actually do something about it. Most people, it appears, don’t — at least not consistently over the long term.

Keeping a tab

In the first generation of wearables, companies sold sensors . The industry matured from there; companies like Whoop and Oura started selling intelligence instead — they learnt how your body worked, over time, and fed insights that get more accurate with time. We know for a fact that these can catch some major risks.

What we haven’t seen yet, however, is the other side of the equation: where ordinary people change how they live, at scale.

In India, at least, that won’t change anytime soon. We need such services; according to the Indian Council of Medical Research, non-communicable diseases now account for 61.8% of all deaths in our country — led by cardiovascular disease. But most Indians are simply nowhere near the price points these devices come at.

But what about a single Indian — Krishna? Well, he still doesn’t know if he’s getting a Whoop.

The unglamorous reforms that actually work

Until recently, if you had unclaimed shares or dividends sitting with a company, getting them back was a nightmare.

The Investor Education and Protection Fund Authority (IEPFA) was set up in 2016 precisely for this — to hold unclaimed corporate shares and dividends, and return them to their rightful owners. Simple enough in theory, but in practice, the process involved 25 steps spread across three separate web portals. One portal handled the application and approval. A second, run by the depositories, handled the actual share transfer. A third handled dividend payments.

The three portals didn’t talk to each other. Information had to be manually re-entered at every stage and cross-checked multiple times. A single data-entry mistake at any point could send the claimant back to square one. Resultantly, by March 2025, the IEPFA had accumulated a backlog of ~51,000 applications and the claimants were waiting close to three years to recover what was rightfully theirs. Many gave up while others paid commissions to intermediaries just to navigate the system.

When the Economic Advisory Council to the PM (EAC-PM) started researching this in early 2025, they mapped out the actual process and found that the biggest problem was also the most obvious one: the three portals operated in silos. Each segment was digitised on its own, but the absence of integration defeated the very purpose of going digital.

The fix was straightforward — integrate the portals. Eliminate the redundant data entry and make share transfers and dividend payments happen in parallel instead of sequentially.

The results have been dramatic. Between April and September 2025, IEPFA was approving about 850 applications a month. After the new integrated system went live, that number jumped to over 9,100 a month — the monthly rate now matches what used to be the annual rate. What earlier took up to two years after approval now gets done in days. At this pace, the entire accumulated backlog will be cleared within months.

This isn’t a new law or institution. Unlike broad-based policies designed from the top-down, the appreciation of the IEPFA story comes from what a simple fix it really is. It’s what Sanjeev Sanyal, an EAC-PM member, calls a “process reform”, which fixes something that existed.

Better plumbing.

Think about what actually fixed the IEPFA. Nobody passed a new law or created a new regulator. Someone mapped how the system actually worked, asked why three portals didn’t talk to each other, and integrated them. With one coordination fix, a three-year wait turned into a three-day one.

When we think about economic reforms, we tend to think big — the 1991 liberalisation, GST, the Insolvency and Bankruptcy Code, and so on. These are structural reforms that reshape the architecture of an economy.

Process reforms, though, are different. They’re the small, targeted fixes to how the government actually operates on the ground. They’re simple corrections to existing architectures. And unlike big-bang reforms, they’re far cheaper to execute. India’s headline structural reforms are mostly done or already underway. But what could unlock the next leg of growth is fixing hundreds of broken processes across the government.

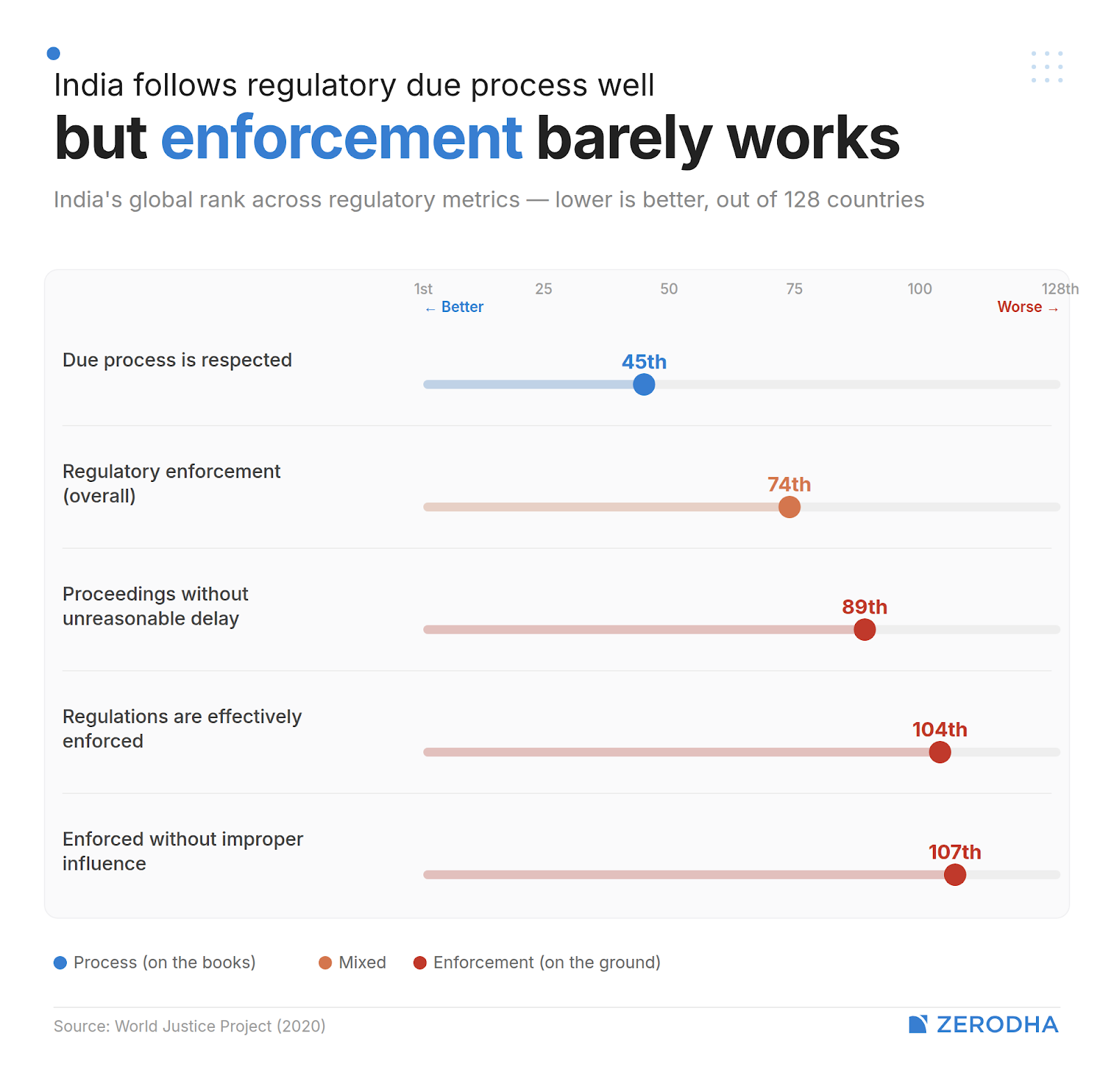

The Economic Survey 2020-21 explains why there are so many broken processes to fix. Cross-country comparisons show that India actually does well at having rules and regulatory standards, and following due process. Where India falls behind, dramatically, is in whether those regulations actually produce results.

And more rules don’t help. It’s really difficult to write rules that anticipate every possible future scenario. Any such attempt adds complexity, and complexity only creates ambiguity. Every ambiguity, in turn, becomes a judgment call, which only leads to more discretion. That creates huge, uneven variance in outcomes that are related to a single rule set. It becomes nearly impossible to enact these rules uniformly.

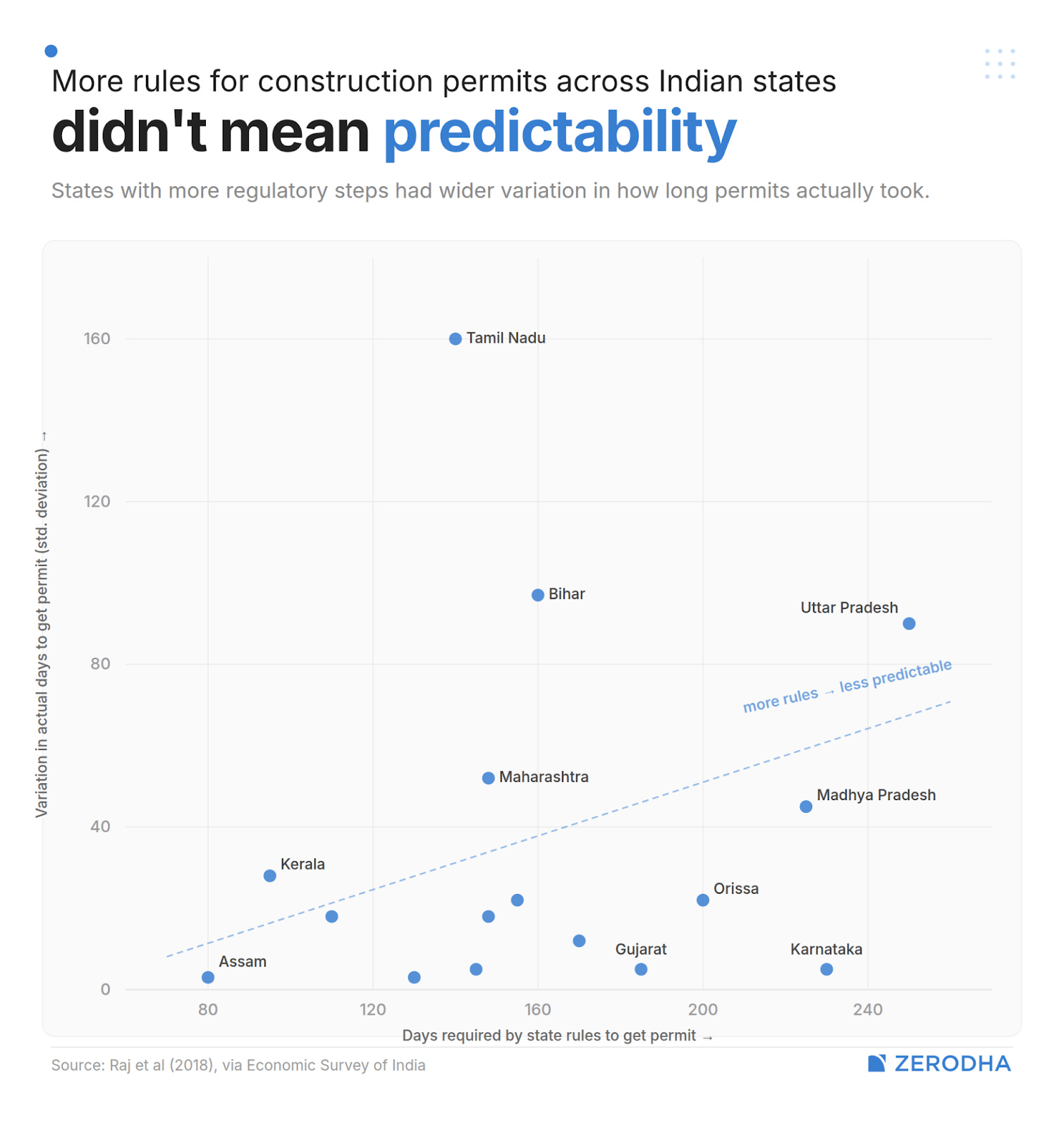

The Economic Survey found exactly this when, for instance, it looked at construction permits across Indian states. States with more elaborate regulatory requirements for granting permits didn’t have more, but rather less predictable timelines. The more boxes an applicant had to tick, the more divergence existed in the experiences of each firm in getting a permit. In many ways, the rules made it feel like a lottery.

But the solution, Sanyal argues, isn’t deregulation or removing the government from things it shouldn’t be doing. It’s process reform, which is getting the government to do things it should be doing, but better. And the case studies from India show just how powerful this can be.

A cascade of fixes

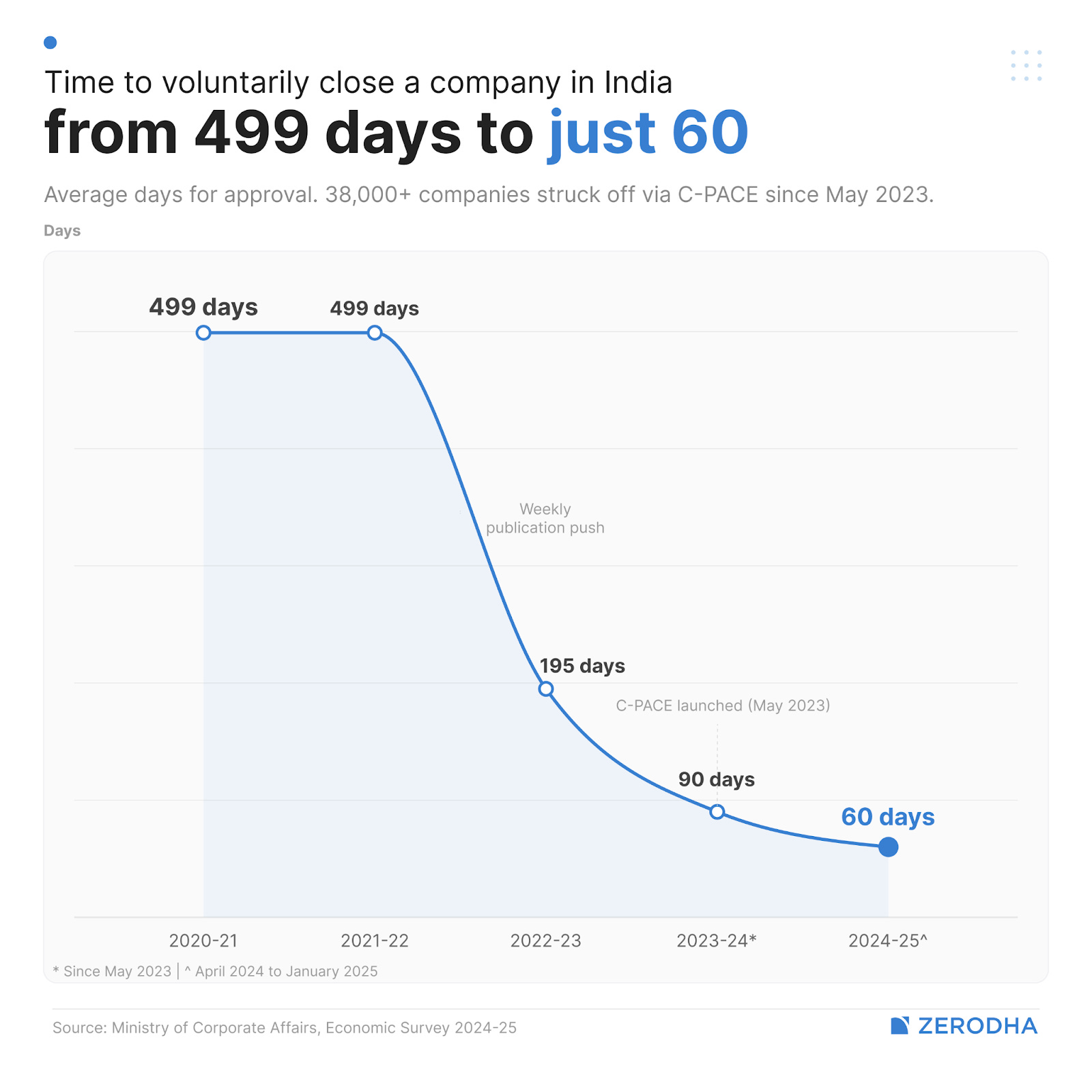

Closing a company: 1,570 days → 60 days

The first case relates to how a corporation is closed in India.

Before 2024, it used to take 1,570 days to voluntarily close a company in India, even when there was no dispute, no litigation, and all paperwork was in order. For comparison, Singapore does it in about 12 months, while Germany took 12-24 months, and the UK did it in 15.

When the EAC-PM mapped the actual process, they found the delays weren’t caused by some deep structural flaw. Over 2/3rd of the days were eaten up waiting for clearances from Income Tax, Provident Fund, and GST departments. But even before that, there was a more mundane bottleneck: the Registrar of Companies had to publish closure notices in newspapers, and because publication was expensive, RoCs would wait until they had enough cases to batch-publish in one go. There were also no fixed timelines and no cap on how many times they could demand document resubmissions.

The fix arrived in stages. First came an administrative push to publish notices weekly or fortnightly instead of waiting; this alone cut average processing time from 499 days to 195 days.

Then, in 2023, the Ministry of Corporate Affairs set up C-PACE — a centralised, faceless, one-window portal. That set fixed timelines for every step with nodal officers identified in each department and resubmission requests capped at two. As a result, average processing time dropped to 60 days by 2024-25. Over 38,000 companies have been struck off through C-PACE since May 2023.

Patent pendency: 6 years → 4 months

The second case study relates to India’s patents.

India’s patent office used to be one of the slowest in the world. Average pendency was around five years — the highest among major economies. The problem wasn’t the patent law itself but capacity. India had roughly 900 staff processing patent applications while China had 13,700 and The US had 8,100.

A few years ago, examiners were added at the junior level. But that just shifted the bottleneck as applications cleared the first examination faster, only to pile up at the senior controller level, waiting for final disposal. The real fix required tripling overall capacity, adding senior staff, cutting fees by 80% for startups and MSMEs, and mandating e-filing. The outcome was a 17-fold surge in patent grants from ~6,000 in FY15 to over 100,000 in FY24.

Welfare delivery: ₹3.65 spent to transfer ₹1

The last case study is about India’s welfare distribution.

India’s welfare system had a delivery problem. For every ₹1 of income transfer to the poor, the government spent ₹3.65. That meant one rupee of budgeted subsidy was worth only 27 paise to the actual beneficiary. About 58% of subsidised food grains under the public distribution system were lost to identification errors, duplicate beneficiaries, and middlemen, never reaching the intended recipient families.

To fix this, the government triangulated three things that mostly already existed: Aadhaar (unique ID), Jan Dhan (no-frills bank accounts), and mobile linking. Benefits were routed directly to Aadhaar-linked bank accounts, cutting out intermediaries entirely. The Direct Benefit Transfer system has since saved an estimated ₹3.48 lakh crore, weeded out 42 million fake ration cards, and expanded coverage 16-fold.

Similar patterns show up wherever you look. The Government e-Marketplace (GeM) brought transparency to public procurement, cutting average prices by 15-20% and making them comparable to Amazon and Flipkart. Telecom regulations for the IT-BPO sector were slashed from 40 pages to 5, scrapping registration requirements and allowing work-from-home. In fact, 92% of companies surveyed by NASSCOM said compliance burden dropped due to this.

The unfinished business

There is a recognizable pattern in how these bottlenecks are recognized and fixed. But the scale of remaining friction in India’s system is enormous.

For instance, India’s courts have 55.8 million pending cases. The judge-to-population ratio is 21 per million; in comparison, the US has 150 per million. The government itself is the biggest litigant, responsible for roughly half of pending cases. And the Income Tax department loses 73% of its own cases at the Supreme Court and 87% at High Courts. Yet, it continues to file appeals as a matter of routine, just because no official wants to exercise the discretion to not appeal.

Tax litigation alone has over 5.4 lakh appeals pending before Commissioners of Income Tax, with disputed demands exceeding ₹16.75 lakh crore locked up in procedural limbo. India’s compliance ecosystem remains extraordinarily dense: a 2025 study found that manufacturing MSMEs face 1,450+ regulatory obligations annually, maintain 48 different registers, and spend ₹13-17 lakh per year on compliance. And land — where over 60% of all Indian litigation originates — still runs on a deed registration system inherited from the Registration Act of 1908, where buying property doesn’t actually guarantee you own it.

Each of these could be a process reform waiting to happen. The question is whether the approach that turned shortened year-long waits into days can be institutionalised and scaled across various arms of the government.

Tidbits

- Google’s $15 billion data centre in Andhra Pradesh Google is set to break ground on April 28 on what would be the single largest foreign direct investment in Indian history — a $15 billion, 1-gigawatt data centre hub spanning three campuses across 600+ acres near Visakhapatnam, targeted for completion by July 2028.

Source: The Hindu BusinessLine - Biocon’s insulin and GLP-1 strategy Biocon Biologics, already a leading global supplier of biosimilar insulins, is now pushing into the fast-growing GLP-1 market — drugs like Ozempic and Mounjaro — arguing that its existing insulin R&D, manufacturing, and prescriber relationships give it a foundation similar to the one Novo Nordisk and Eli Lilly built before dominating that space.

Source: Business Standard - Saudi Arabia raises oil prices to Asia at record premium Saudi Aramco has set Arab Light crude prices for May sales to Asian refiners at a record premium of $19.50 per barrel over regional benchmarks, as Iran’s near-closure of the Strait of Hormuz disrupts Gulf oil flows — though the figure came in well below the $40 premium many traders had anticipated.

Source: The Print

- This edition of the newsletter was written by Krishna and Kashish

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Subtext by Zerodha

Subtext by ZerodhaWe’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()