Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- When you should increase the price of medicine

- Indian hotels find comfort at home

When you should increase the price of medicine

The government just did something that, at first glance, would seem inhumane: it agreed to let the prices of two cancer drugs rise by as much as 50%.

The drugs are cisplatin and carboplatin. Both are made from platinum-based raw material. They are first-line chemotherapy drugs, used to treat ovarian, cervical, lung, breast, head-and-neck and testicular cancers. They are also cheap — a 10 mg vial of carboplatin is capped at ₹61.10.

In the last few months, though, they started disappearing from hospitals, including AIIMS Delhi and the Tata Memorial Centre. This is why the government invoked an emergency clause to let its manufacturers charge more. It was better to let a drug cost slightly more than to not have it on pharmacy shelves at all.

This tells you why a price cap can be a trade-off. On one hand, the cap did exactly what it was designed to do: it held the price flat. Only, that itself became the problem.

To be perfectly honest with you, some of this is speculation. It isn’t fully clear how much of this shortage is caused by the price cap itself. There are other things happening at the same time: platinum has become scarce globally, the rupee is weak, import permits are slow, and these drugs are hard to make and produced by only a few companies. Manufacturers claim production has become unviable at capped prices, but it isn’t entirely clear to us exactly where the chain breaks down.

With that caveat aside, however, the episode is a demonstration of how India’s drug-pricing system works, where it breaks, and the two very different problems it is trying to solve with one tool.

How India decides what your medicine costs

There’s a body called the National Pharmaceutical Pricing Authority, or NPPA, which was set up in 1997. It is usually described as the agency that caps drug prices. That is only half its job. Its mandate is to keep “essential medicines” both affordable and available . Its price regulation, as the government itself notes, should not make drugs disappear.

Those two goals, however, are in constant tension. That’s where our story starts.

How much can a medicine cost?

A drug’s price is determined by a rulebook: the Drugs (Prices Control) Order, 2013. This order puts every medicine into one of two buckets. One, there are “scheduled” drugs, which include 900 formulations on the National List of Essential Medicines, such as key antibiotics, insulins, heart drugs and cancer drugs. These all have a fixed ceiling price. Everything else is “non-scheduled.” These are left to the market, but with a limit: a company cannot raise their price by more than 10% a year.

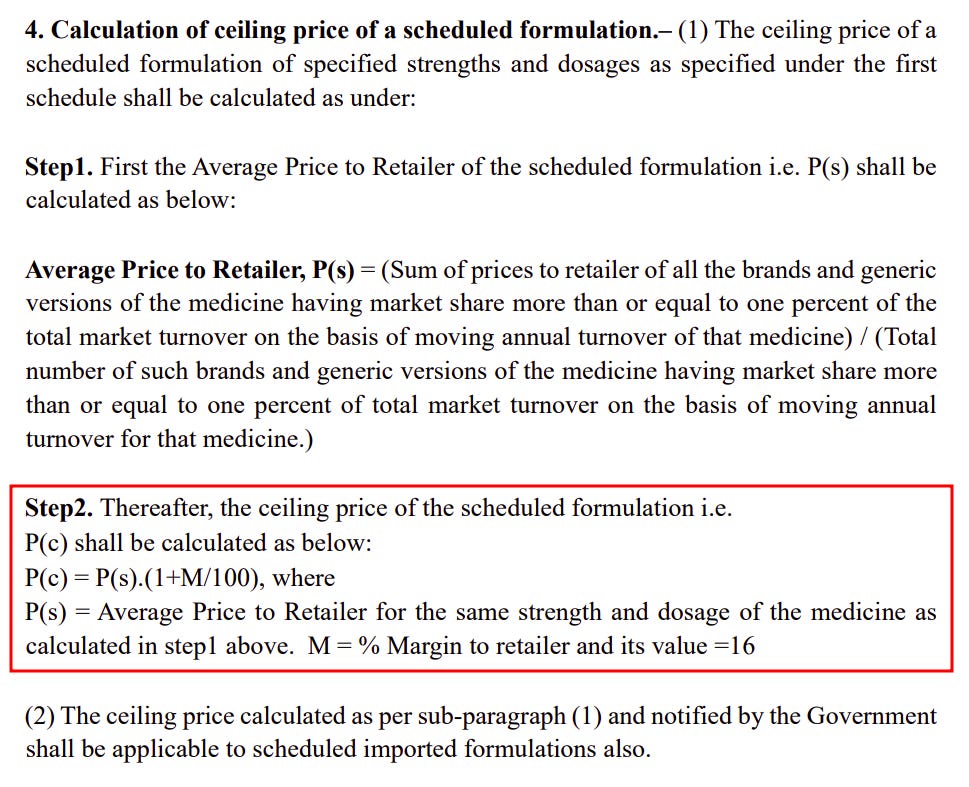

How do we decide the price ceiling for scheduled drugs? Since 2013, India has used a market-based formula. The NPPA takes every brand of a medicine with at least 1% market share, averages the prices at which they are made available to the retailer, and then adds a 16% retail margin. That average becomes the cap. Anyone priced above that must cut down within 45 days. Those already below the cap, however, cannot jump up; they keep their lower price.

There’s a strong case for this system.

Indians still pay a large share of their health costs out of pocket. The picture is changing; out-of-pocket spending has fallen from over 64% of all health spending in 2013-14 to roughly 43% in 2022-23, but it remains high. In a confusing market, where distressed and sick patients must choose between dozens of brand names with very different prices, completely free prices can hurt patients.

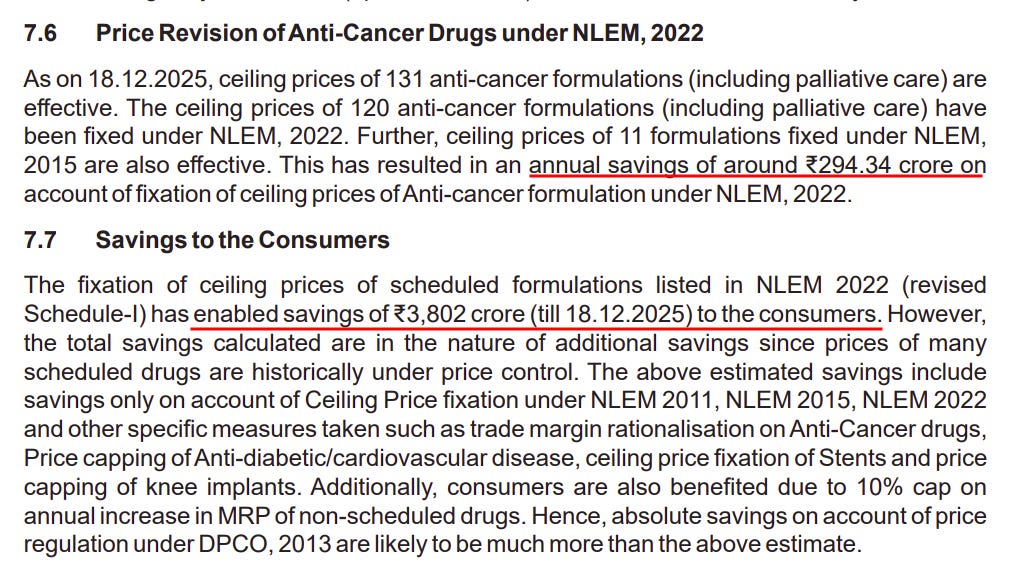

A cap brings genuine savings with it. The government claims its essential-medicine ceilings saved consumers about ₹3,802 crore by late 2025. Anti-cancer drugs alone account for about ₹294 crore a year. A clear example of these savings came in 2017, when NPPA put price caps on stents, the small mesh tubes used to open blocked arteries. Before that, hospitals were marking them up by as much as 654%. Once the cap kicked in, prices fell by up to 85%.

Department of Pharmaceuticals Annual Report 2025-26

Prices aren’t static

With time, however, prices change. And with that, the ceiling moves as well. It is revised once a year, in April, in line with the Wholesale Price Index. That’s where the problem arises.

The WPI measures how fast prices are rising across the whole economy, from steel to soap. It does not track the cost of any single drug. In some years, there’s a genuine increase. In some, there isn’t. In 2024, overall, prices increased by about 0.0055%, which is to say they basically stayed flat. With that, the ceiling price of drugs stayed still as well, even while the actual cost of making it climbed much faster.

But there can come a point where the gap becomes too wide, and the drug is no longer worth manufacturing. Then, the system can reach for a backup. This back-up is Paragraph 19, which lets the government override the formula and reset any drug’s price, up or down, in “extraordinary circumstances”.

This requires paperwork. There’s an online system where companies file everything from applications for new-drug prices, to annual revisions, to quarterly production data. If a firm wants to stop making a scheduled drug, it must give six months’ notice, and if needed, the government can ask it to keep production up for a year. If a company thinks NPPA set a price wrong, it can file a formal review with the Department of Pharmaceuticals.

This is what happened with cisplatin and carboplatin. The medicines became too expensive to sell. One maker, Naprod Life Sciences, told Business Standard that platinum had roughly doubled in cost in a year, from about ₹2,000 to nearly ₹5,000 a gram, and can only be imported with a special permit, which takes months. This is what made the drugs “unviable” to produce.

The NPPA received requests from the industry to raise prices on 82 formulations because of raw-material costs and currency swings. The committee approved only four: cisplatin, carboplatin and two anti-tetanus injections.

The system isn’t perfect

This illustrates a problem that most price caps come with: they can distort the market. If something becomes too expensive or inconvenient to sell, and you can’t pass any of it to customers, you might just check out of the market, or try clawing profits out in other ways.

The NPPA caps the price of finished medicine. It has no control over the prices of inputs in making it, however: the active ingredient, the solvents, the packaging, the import duty, the exchange rate. The price ceiling can sometimes fall below the real cost of production, and then, it makes no sense to keep making the drug at a loss. So companies can make less, or stop altogether.

This isn’t just a matter of these cancer medicines; the same thing repeats itself. In 2025, for instance, small manufacturers told the NITI Aayog that “unsustainable” ceilings had pushed quality drugs out of the market. They pointed to co-trimoxazole, a basic antibiotic, as becoming uneconomic to produce.

A year later, a Himachal industry body representing more than 500 units said raw-material, solvent and packaging costs had jumped 200-300%.

Or consider the price cap on stents. Foreign manufacturers claimed the capped price was below their cost of production. Some tried to pull their newest stents out from the market. Meanwhile, there were clinical distortions. Hospitals, seeing their margins squeezed, ramped up non-transparent charges, like consumables or room charges. On the other hand, with stents now cheaper, they began pushing everyone to stent-based procedures, whether or not other options — like a bypass — would have been better.

To be fair, it isn’t that price caps always cause shortages. A 2024 government-commissioned study of stents and knee implants, for instance, found that supply and demand actually rose after the caps.

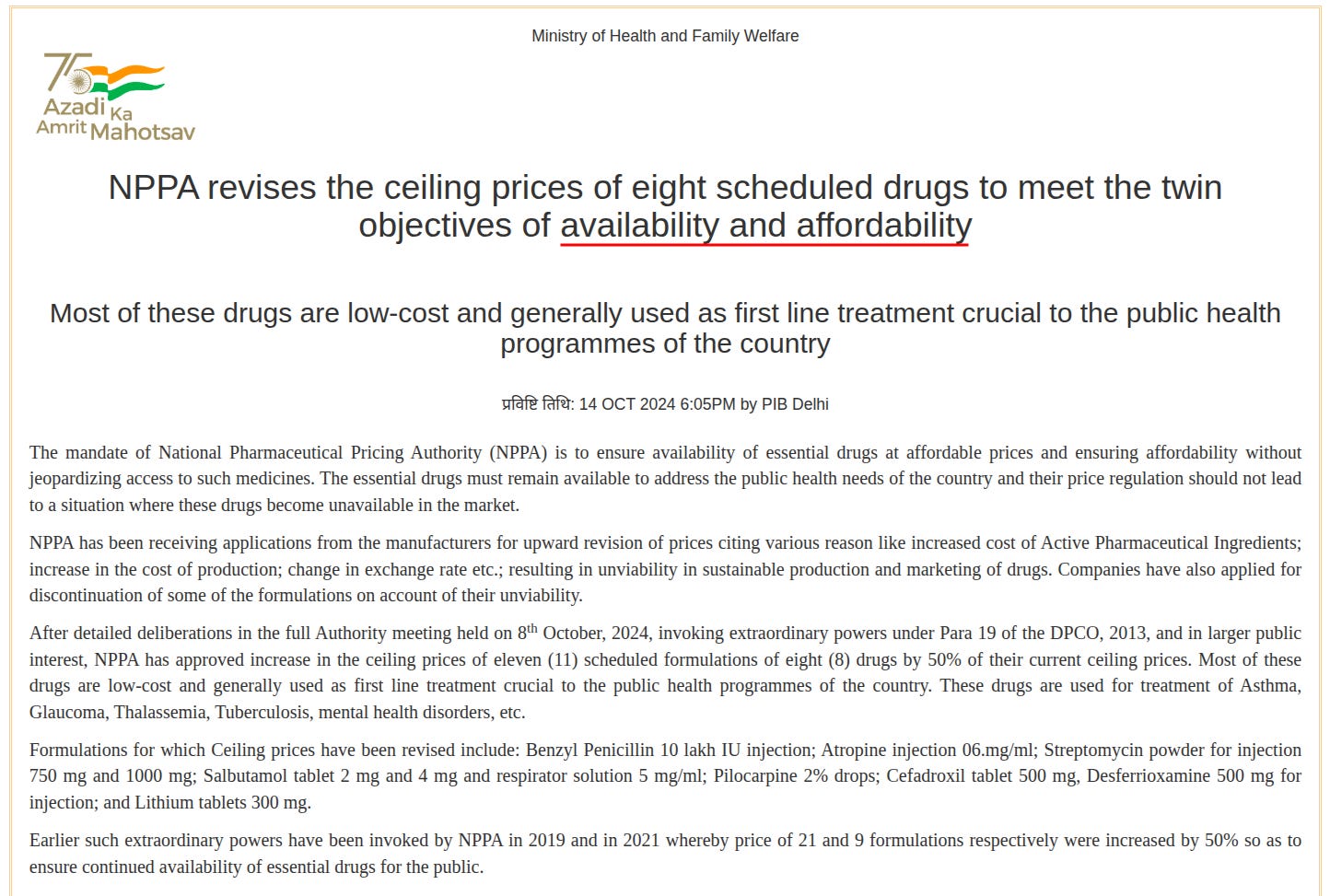

But the pattern shows up consistently enough. The government routinely finds itself reaching for emergency procedures to increase rates. In October 2024, for instance, NPPA used the same Paragraph 19 to raise prices by 50% on drugs for asthma, tuberculosis, glaucoma and thalassemia. It had done something similar for smaller sets of drugs in 2019 and 2021. Each time, the goal was to stop manufacturers from leaving.

If a system keeps needing emergency exceptions, what does that say about its normal rules?

Beyond the obvious

Do price controls achieve their original goal of actually improving access, however?

The research is mixed. Cheaper medicines aren’t always more available medicines. Price caps can reduce prices, but access isn’t a matter of price alone; it is also a matter of availability, prescribing behaviour, and insurance and procurement coverage. These things don’t always work in a straightforward way.

And on the way, they cause all sorts of other issues.

The more of a company’s sales sit inside the essential-medicines list, the more it lives on volume rather than margin — growing by selling more units, not by charging more.

Many companies try to get around this through cross-subsidisation. A large, diversified firm can sell a capped essential drug at a thin margin, or even at a loss, and cover it with profits from exports, specialty and patented products, and chronic-disease brands that face no cap. A small or mid-sized maker with a narrow portfolio has nothing to cross-subsidise from. So when prices rise, big firms absorb the hit, while small ones pull out completely.

A Center for Global Development study found, for instance, that while price caps lowered prices, that came at a terrible cost: it wiped out many small local generic makers. Those firms were often the only suppliers to rural pharmacies. So the savings for city buyers showed up as stockouts for the rural poor.

At the same time, larger companies actually start gaming the formula. Because the ceiling is an average of prices before control kicks in , researchers studying the metformin market found firms raising prices just before NPPA took its snapshot, pushing the average up.

Often, price caps don’t even increase access to the very medicines that are capped. Some studies on anti-cancer drugs, in fact, found a drop in use of the controlled drugs in some cases.

Why is that? As another paper found, when their margins were squeezed, companies pulled their sales reps off the cheap, regulated drugs, deploying them to push costlier but unregulated substitutes instead. That shift hit prescriptions from less-educated doctors treating poorer patients the hardest, hurting the very people the policy was meant to protect.

This also pushes the capital for drug development away from regulated medicines, starving research budgets for the very medicines price controls protect. Companies instead move money and attention toward biosimilars, specialty drugs and export markets, where prices are set by the market rather than by the government. Multinationals, meanwhile, have pushed to exempt patented drugs from price control. This divergence has caused a split within the pharmaceutical industry: hospitals and contract manufacturers are pulling ahead while plain generics struggle.

Is ₹61 too much?

There are many reasons to protect customers from a large, confusing industry, which they only see when their health, or even their lives, are in danger. Few of those, however, apply to a ₹61 vial, whose problem is not greed, but the cost of a metal. Cisplatin and carboplatin are decades-old generics. If even these are becoming unviable, there’s a genuine problem in our system.

The price hike on cisplatin and carboplatin, now, buys time. But that time will be wasted unless we can build a system that can discover problems before the shelves are already empty.

Indian hotels find comfort at home

The crisis at the Strait of Hormuz has undoubtedly been bad for most businesses with international exposure. Airlines rerouted. Large corporate events like meetings, incentives, conferences and exhibitions (collectively called MICE), were cancelled as the region became inaccessible. IHCL, which runs the Taj Hotel, estimated the conflict cost it ₹40-45 crore in lost revenue in the quarter.

And yet, IHCL called this its sixteenth consecutive quarter of record performance, with revenue, profit and EBITDA all up roughly 14-15% from a year ago.

So what led to this outperformance? The short answer is that even as international markets fell away, domestic demand held its ground. It didn’t replace everything that was lost, but it was large enough to hold the sector up.

To get into the long answer, let’s first understand how hotels make money, and then see what happened to the industry that surrounds them.

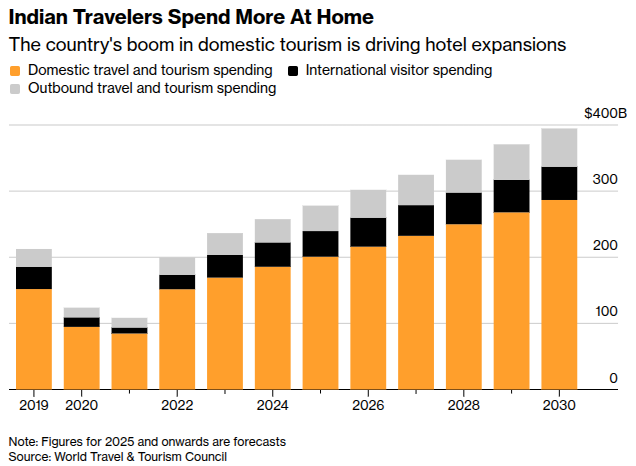

The domestic travel boom

A hotel earns in two ways, that is by filling the available rooms and charging more for them. The number that combines both is revenue per available room , which clearly depicts whether a hotel is actually doing well, because it captures both how full the hotel is and what guests are paying.

In this quarter, due to foreign cancellations, occupancy at hotels dependent on international guests took a hit. But the premium hotels didn’t need to discount because domestic demand was strong.

For premium hotels, Indian travellers stepped in where foreign guests had left. However, mid-market hotels, that depend more heavily on corporate bookings, had a harder time, as we will see later.

The first half of the quarter ran on business: think foreign government delegations, corporate conferences, a packed events calendar. Weddings were also a significant driver. And by March, when the conflict hit hardest and international bookings dried up, it was leisure travellers who kept hotels busy, basically Indians driving to hill stations, booking beach resorts, and visiting religious destinations.

The domestic travel trend didn’t start in March, though. It had been growing for years before the conflict gave it an extra push.

MakeMyTrip, India’s largest online travel platform, reported FY26 gross bookings of $10.4 billion (roughly ₹97,800 crore at $1 = ₹94), up 10.4% in constant currency. Meanwhile, Yatra’s hotel room nights booked grew over 36% in the quarter compared to a year ago. On the hotel side, IHCL’s standalone RevPAR grew 12% in the quarter across hotels already in operation before the conflict.

This is part of a much broader shift in how Indians travel. A survey by Allianz Partners and Ipsos found 60% of Indian travellers planned to holiday within India in the summer of 2026. More branded hotels have also opened in smaller, tier-2 markets in recent years, like the Lemon Tree chain in Aurangabad, Jammu and Dehradun, and IHCL’s budget brand Ginger. That ensures good options while travelling across India.

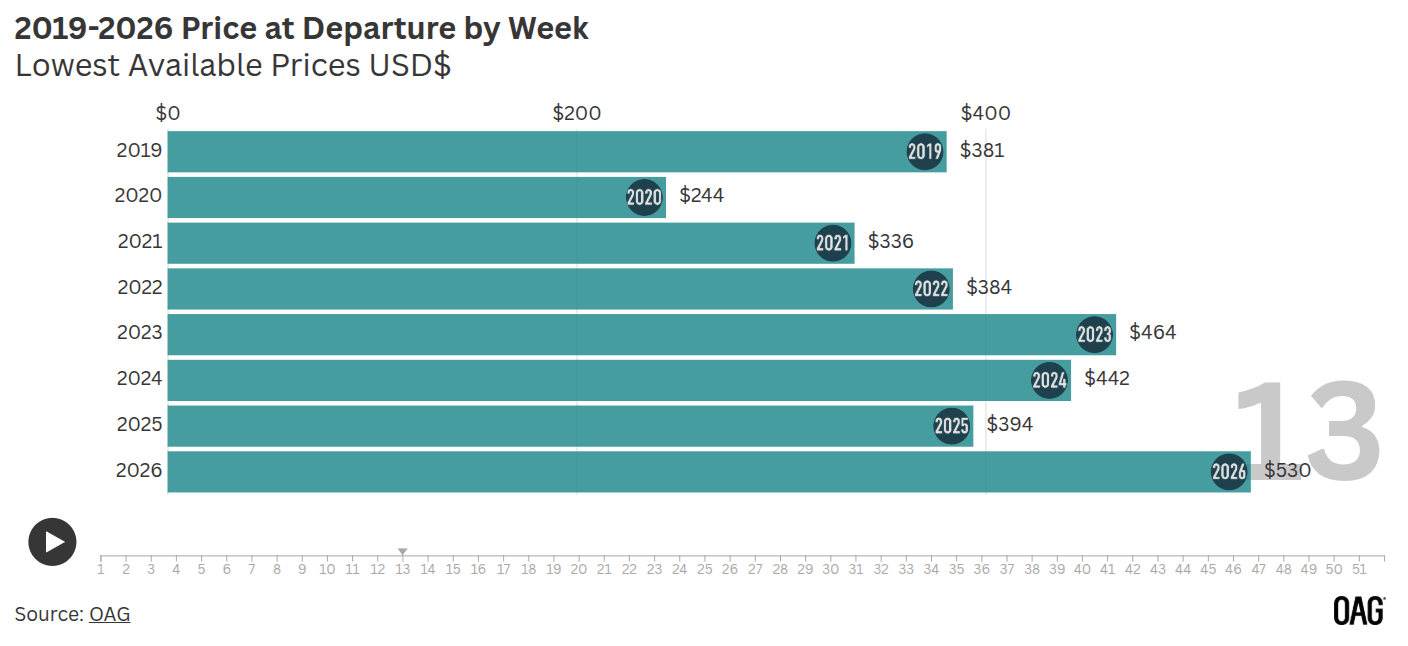

Part of the shift is also about cost. International airfares rose sharply as the conflict disrupted routes through West Asia, which handles a large share of India’s outbound flights. For many households, a trip within India simply became the cheaper, easier option.

Why companies are still building

If this demand trend were a single-quarter story, companies wouldn’t be spending the way they are. And India simply doesn’t have enough quality hotel rooms.

According to Hilton, the country has roughly one hotel room for every 3,000 people, compared to one for every 60 in the US. And, India’s hotel construction pipeline reached a record 906 projects representing around 118,000 additional rooms. This shortage of supply has so far created pricing power that benefited the revenues of hotel operators.

So hotel companies are building. IHCL ended the year with 630 hotels (64,000-plus keys) and a pipeline of nearly 31,000 keys, growing mostly by managing hotels for other owners rather than building everything itself. Lemon Tree signed 55 new hotels this year and is splitting into two companies to help manage this expansion better. One will own the hotel buildings, the other will run them. The management business earns fees without owning property, so it needs less capital to grow.

EIH is adding both hotels it will own outright and hotels it will manage for other owners, paying for the expansion from its own earnings rather than borrowing. Chalet, which owns and operates most of its hotels directly, crossed 5,000 total rooms that are fully built or are undergoing construction, and is spending roughly ₹3,000 crore on new properties over the next three years. Its diversification into office buildings helps it hedge against risks in travel.

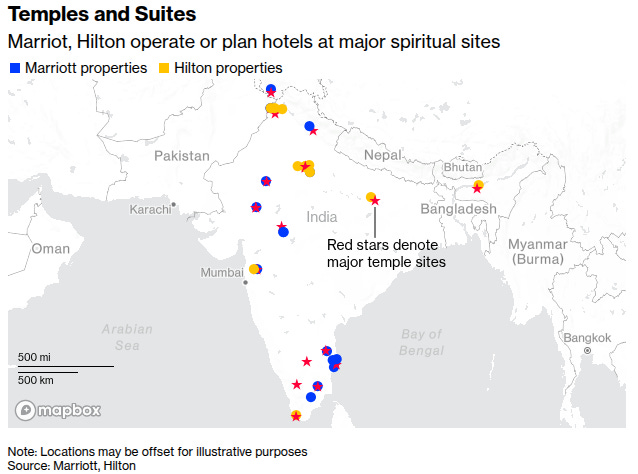

Even international brands like Marriott, Hilton, and InterContinental Hotels Group are all aggressively expanding in India, with a notable focus on religious and spiritual destinations. Marriott says about 11% of its roughly 220 hotels in India cater to temple visitors, and Hilton says around 15% of its India pipeline is near spiritual destinations.

As per JLL, hotel investment across India jumped 67% year-on-year to $567 million (₹5,330 crore considering $1 = ₹94) in 2025, up 67% from the year before.

The cracks

Not every company had a good quarter, though. Since various hotels operate in very different parts of the market, their problems were also different. IHCL runs premium and luxury properties under the Taj and Vivanta brands. EIH operates the ultra-luxury Oberoi and Trident hotels, catering heavily to high-spending foreign visitors. Chalet owns and operates upscale business hotels concentrated in Mumbai. Lemon Tree is mid-market, catering more to domestic corporate and leisure travellers across a wider spread of cities.

Among them, Chalet had the hardest quarter. A large share of its hotels are in Mumbai, and Mumbai had a weaker quarter than most other Indian cities. Occupancy across Chalet’s portfolio fell nearly eight percentage points, and the rate increase wasn’t enough to compensate, so overall earnings per available room dropped.

March was particularly damaging because Dubai and Abu Dhabi are major destinations for corporate reward trips and company conferences. The most popular window for these events is the few weeks after Ramadan ends, when companies fly employees out for annual incentive programmes. That window shrunk this year, right when the conflict made those trips impossible. The entire season was wiped out in one month.

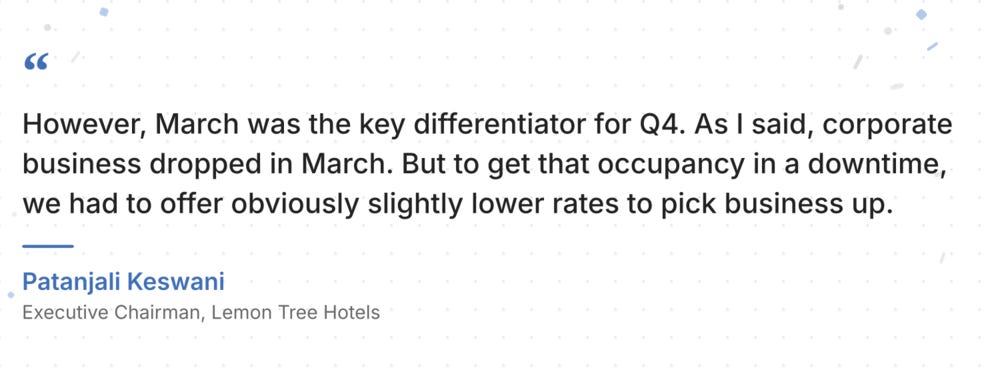

EIH had a weak January for different reasons. North India’s winter air quality, which regularly draws negative attention, kept some visitors away, and foreign tourist arrivals were also softer that month. On top of that, IndiGo’s grounding of all flights for a few days in December had already softened bookings in January — especially for Lemon Tree’s airport hotels. When corporate bookings dropped later, Lemon Tree had to lower retail prices to fill rooms.

Thomas Cook’s CEO Mahesh Iyer noted that Indians travelling within India or on short trips abroad don’t fully replace the money lost from cancelled long-haul travel, because those are much more expensive trips. For hotels this matters less, since a domestic guest and an international guest often pay similar rates at the same property. Nonetheless, there is a gap.

Some disruptions were one-off. Wedding calendars shift year to year. January air quality is a recurring seasonal pattern in North India.

What to watch

The real question going forward is whether domestic travel is strong enough on its own to sustain the sector if international demand stays weak for longer.

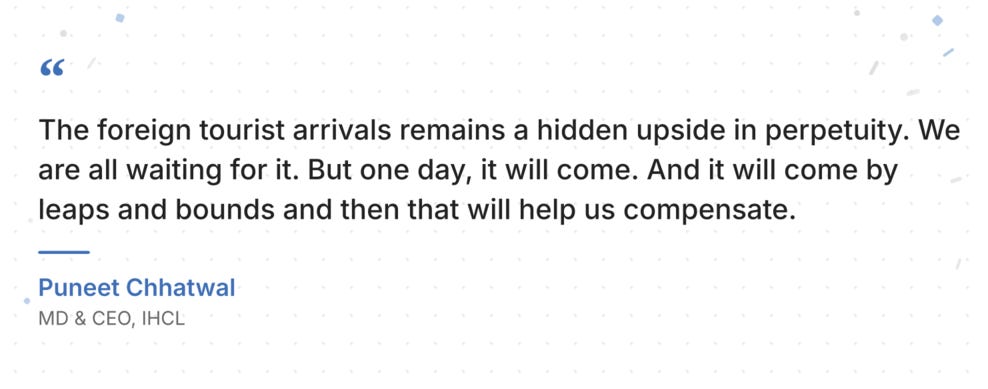

If things in West Asia settle and international flights recover, hotels which depend most on foreign visitors, will get a boost on top of what domestic demand already provides.

If it takes longer, the sector will depend on whether Indians keep travelling within the country at the current pace, and whether corporate travel recovers as uncertainty fades. An RBI consumer confidence survey from June showed that household spending sentiment weakened significantly in May. When people feel less wealthy, travel is usually one of the first things they cut back on.

Indian domestic travel may have become large enough to carry the hotel sector through a global disruption. The chains building aggressively right now are betting that is a permanent shift. The bet may be right, but only if domestic demand stays strong after foreign travel normalises and new supply starts arriving.

Tidbits

- JSW Makes E-Bus Market Debut with Aggressive Bids

JSW Eco Mobility bid across all five cities in the government’s 6,230 electric bus tender, undercutting Tata Motors, Olectra, JBM, and Ashok Leyland, finishing second or third-lowest in four cities despite winning no orders.

2.Source:* Mint

- Govt Caps Retail Diesel Sales at 200 Litres to Curb Hoarding

The government capped retail diesel purchases at 200 litres per vehicle daily and barred industrial and commercial users from buying fuel at retail pumps for 90 days, addressing bulk diversion driven by the ₹95.20 vs ₹134.50 retail-bulk price gap.

4.Source:* BS

- Sebi Proposes Uniform Price Bands for Thinly Traded Stocks

Sebi has proposed that exchanges with no trading activity in a stock adopt the closing price from the most active exchange, preventing price divergence in illiquid scrips; public comments are invited until July 2.

6.Source:* Mint

- This edition of the newsletter was written by Kashish and Vignesh.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Subtext by Zerodha

Subtext by ZerodhaDecoding Bain’s India Venture Capital report with the authors

Bain & Company’s annual India Venture Capital report is one of the most rigorous deep dives into the country’s opaque private markets, and this year’s edition is themed Warm Currents and Cold Seas . We sat down with co-authors Aditya Shukla and Aditya Muralidhar to look beyond the slides and unpack what is actually happening on the ground. Our conversation goes into how private market data is built without a Bloomberg equivalent, how the LP landscape and family offices have shifted over the last six years, why VC held steady while PE faced headwinds, the unexpected explosion of quick commerce, and the mounting pressure on SaaS companies to figure out AI. Read the key takeaways on Subtext:

Watch the full podcast episode below, where the authors of the Bain report discuss the nuances of India’s venture capital ecosystem and the future of startup funding

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()