Hi.

I’ve an account with Interactive brokers and was looking to invest in US stocks. Which bank gives best conversion rates for Inward and Outward Remittance?

Hi.

I’ve an account with Interactive brokers and was looking to invest in US stocks. Which bank gives best conversion rates for Inward and Outward Remittance?

Check out Indus Forex - Indus Ind Bank, they offer the best rate for outward remittances. However, do talk to your main bank where you maintain your account and negotiate a rate from their treasury. Use the Indus Forex rates online as benchmark. You can also use XE app, which will let you know more or less the international rate in the market, but do not expect anyone to give you this as there are additional cost a bank will need to bear including their profit margin.

Disclaimer: These are my personal view, please do your own research on this.

PSU Banks give much better forex rates for inward and outward remittances. Take a look at the rate cards of different banks that is updated on every working day. Look under the TT BUY and TT SELL COLUMN. Out of all the banks in India and exchange providers like bookmyforex, Indian Overseas bank provides the best forex rates. Canara Bank is a close second.

Just type on google X Bank Forex card rates and look for the updated rate.

Some banks also charge some fees for receiving or sending funds which you can find on their terms and conditions page in the forex section.

https://instantforex.icicibank.com/instantforex/forms/MicroCardRateView.aspx

https://www.kotak.com/en/rates/forex-rates.html

https://www.idfcfirstbank.com/forex-rate

For TT BUY, a higher rate is better

For TT SELL, a lower rate is better.

One more thing, if your are an NRI Customer, then preferential rates may be available to you which will be slightly better. If you are transfering a large amount - More than USD 10,000 or equivalent, then most banks will offer a better rate than their default card rate if you talk to your RM.

The default forex card rates for IDFC First Bank, ICICI Bank and Axis Bank are amongst the worst forex rates one can get. The card rates are attached in my above post. Can you elaborate why you feel these banks are preferable?

Canara Bank rates with regard to USD is seriously fine. Did not know PSU were offering such fine rates when compared to private banks.

Thanks for the info.

The rs 85.15 rate that you have referred to is for purchasing/selling cash or if you use your debit card in an international currency. For remittances, one has to look at the Telegraphic transfer (TT column). Now, today the USDINR is about 83.32.

Lets compare the best rate (IOB with idfc)

IOB TT SELL rate is 83.65 and IDFC TT SELL rate is 84.83.

Using IOB, one will lose 0.4% and using IDFC, one wil lose 2.2%.

When remitting the funds back you will lose about the same.

So, using IDFC sending and receiving one will lose approx 4% whereas using IOB one will lose approx 0.8%.

An FD gives 8% for a full year and here one is losing 2.2% at one go.

My point is that even though the absolute amount seems small to you, the percentage is what one should pay attention to and it is quite high.

Another example: If one invests in an average equity mutual fund in india the MER is about 0.8 to 1%.

So, taking this into perspective, losing 4% for a round trip transaction is quite large and a sunk cost.

So, when you start an investment in Vested, your return is already at a Negative 4%.

Mam, can you guide me in what are the additional charges bank will charge when i deposit usd to interactive brokers from my IndusInd bank account. Also how much to negotiate and wirh whom?

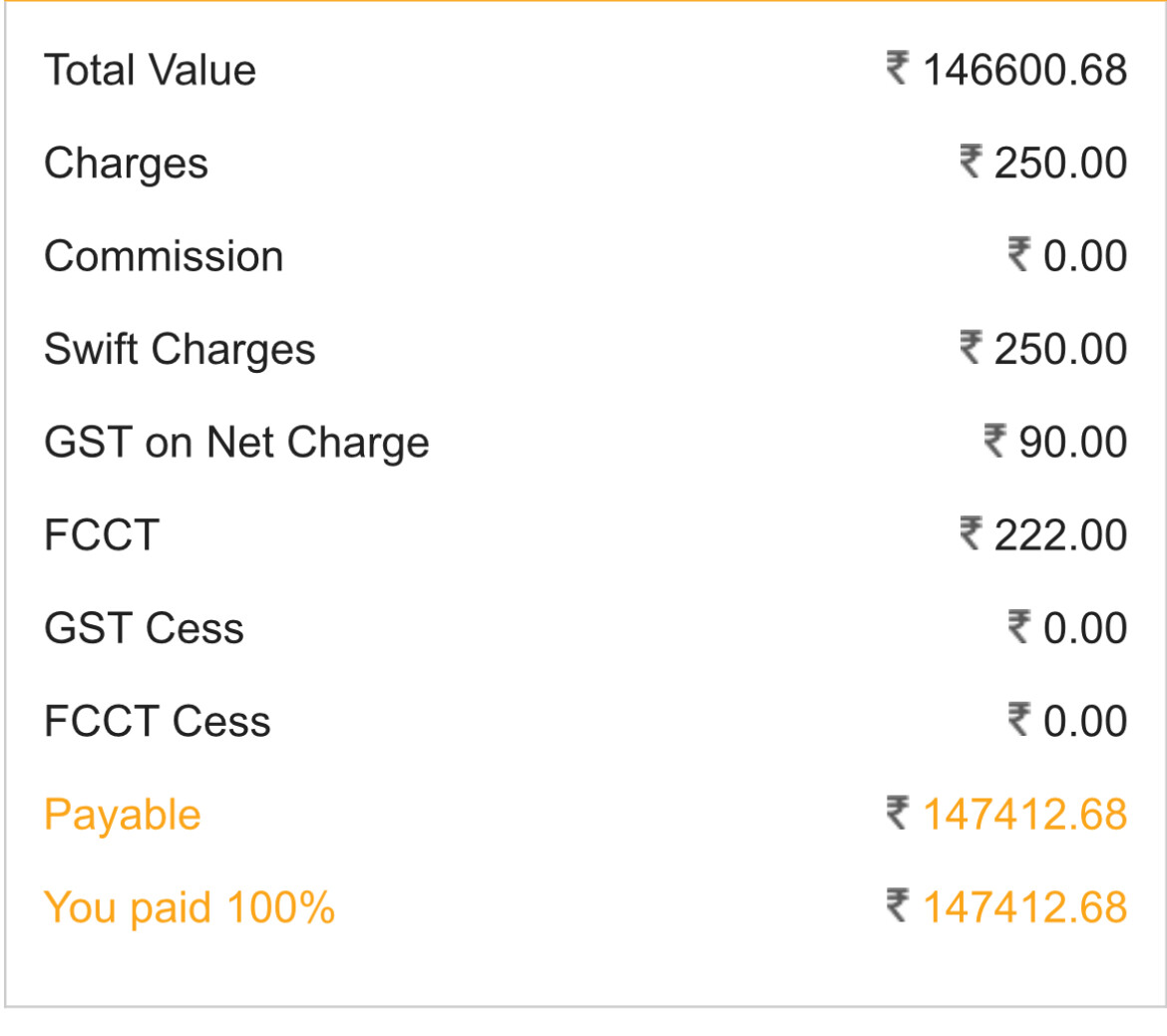

See these are the charges indus forex takes when remitting funds from nre inr to outside.

You will get an idea of the charges

When it comes to resident there could be tcs as well

Best option is to approach a branch and talk to them.

This info is from my friend. I could be wrong.

They get you on the conversion rate ![]()

Check the rate from XE application which should be your base and then shop around. Few banks take their own fees, so better to check before doing anything. Federal Bank has this extra charge, as if they are giving out a loan.

When you go to a branch and ask them for a fine rate, the amount of remittance should be on the high side. Amounts in the range of 1000 to 2000 usd they will not bother.

Banks are not too keen because money is going out and also due to the work involved in the background which is as follows

The above is the minimum work a RM has to do for outward remittance when customer wants the transaction to happen through branch. Online they dont care as there is no RM intervention.

Think of above transaction or just call customer “Good morning sir, open FD online” we give the best rate possible.

RM prefers the second option than the first hence FX is not encouraged until it is in min 10 lakh plus

PS: RM is She and Customer is HE - Just for clarity in the above case