NSE market watch shows most SGBs trading near 9000 or less. But, the ibjarates for 999 purity to which SGBs are linked shows it’s intrinsic value as 9300+ today. Given the pending interest, shouldn’t it trade higher?

Unlikely. Liquidity issues were always there. In spite of that, It used to trade above ibja rates by 10-20%. See

Maybe bond market doesn’t believe the government to pay up or expect customs to reduce more or just expect Gold to fall? Something doesn’t add up here.

Pending interest is on issue price not current price, so it’s not as big as it seems

More likely that they expect it to fall before maturity. Plus SGBs always play catch up (in movement), it is not instant due to low liquidity. The prices you see are sometimes yesterday’s or way older since no trades took place for that SGB since then

And they are not trading that low as per my calculations. 2% premium is normal. I’ve been monitoring since months and all long term SGBs were at 1-2% premium. Same today.

Near maturity SGBs always trade at high XIRRs due to being only a few days away from maturity, which inflates XIRR

Disc: Calculations are done programmatically by me and could be wrong. XIRR is calculated inclusive of interest

1 Like

No SGB is trading at premium. Which SGB is trading at 2% premium? They’re at minimum at 6% discount.

I’m talking about yield. You’re talking about price discount with gold. The site you linked is showing many SGBs at 2-3% yield.

Lol, I feel the same. Maybe some new taxation news on cg on the horizon ![]()

1 Like

Ok. Why are they trading at a discount in their price then, when they used to trade at a premium?

Well, I kind of see the possible reason - but I am not completely sure about it. On July 23, 2024 the budget presented slashed customs duty on gold and silver from 15% to 6%. That is 9% hit. That implies that the secondary market for SGBs were always pricing in this 15% on top of gold price till July 23, 2024.

And if this is true, SGBs are still pricing in additional 6%. And there was chatter that it can be further cut by 3%.

We already know that government is struggling to pay the bills on this one. Its a bond so government has to stick to its promise to pay interest and gold price on redemption but perhaps they will find a way to reduce their burden. And I guess that is what secondary market (being smart enough) is pricing in the discount of SGBs.

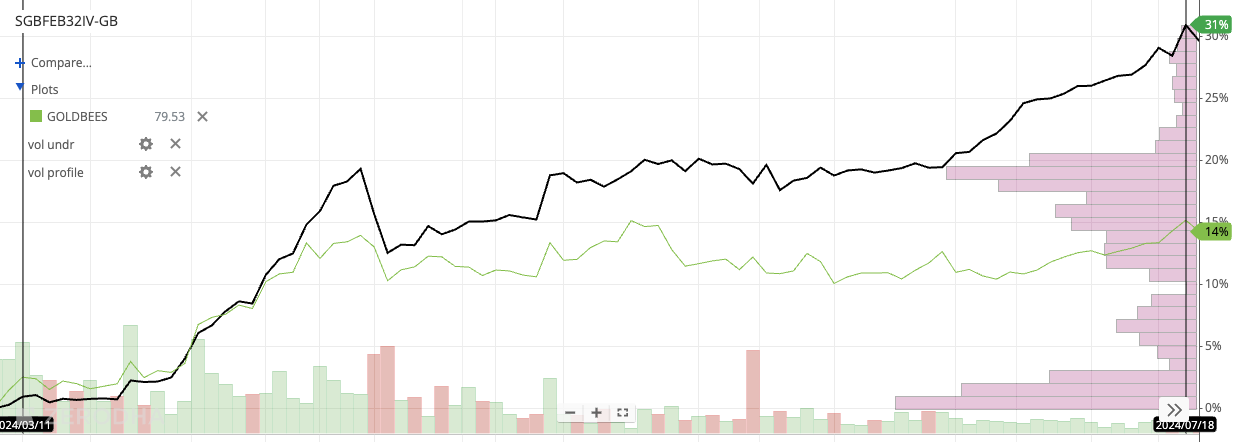

SGB Premium - Till July 23, 2024 - 32% Latest SGB Vs 19% GOLDBEES

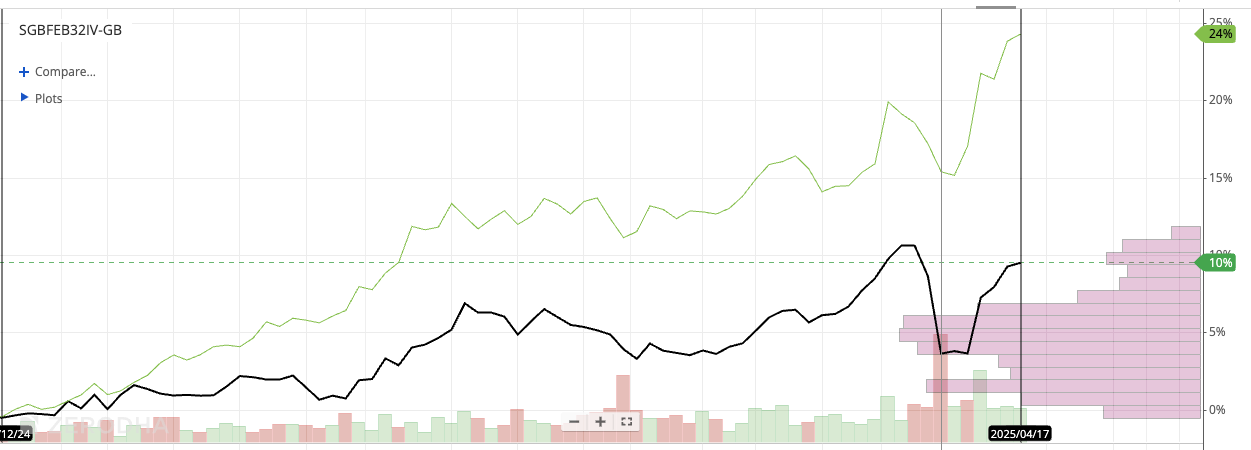

SGB Discount - From July 23, 2024 - 15% Latest SGB Vs 31% GOLDBEES

P.S. This is really sad for SGB holders. I am also struggling to find an alternative of SGBs that can give true gold returns and can be collateralised as cash component of the margin made available.

P.S. This is only one possible reason. But it still doesn’t explain the huge divergence. Though it started from Jan 2025 when this money control report of further cut came in. But still, there has to be something in the way bonds are being treated and I would love someone knowledgeable to give a cogent explanation.

1 Like

Import duties were on top of price of gold. It’s not specific to SGB.

IBJA rates and market rates of gold also fell when import duty was slashed?

True that. It should have affected all Indian rupee denominated products uniformly - and not just on that day but there on as well.

But then something changed in the sentiment for SGBs on 23-Jul-2024 and 01-Jan-2025 which is around news of import duty slashing or rumours of further slashing. And from that point on they (SGB) had clear divergence in their pricing compared to GOLDBEES. When both should have uniform effect of IBJA prices.

SGB Premium - From Listing To 23-Jul-2024

SGB In Tandem - From 23-Jul-2024 To 01-Jan-2025

SGB Discount - From 01-Jan-2025 Till Date

As I said, this is conjecture and one possible explanation. I am not sure about it. And I would love to hear alternate explanation for these divergence periods.

For whatever reason, SGBs are closing/closed their intrinsic discount very fast the last few sessions. It’s trading near their intrinsic value. It’s possible we might have a premium soon. Something to watch for.

Yeah. I think it has some kind of yearly cycle of in-sync, divergence and convergence when compared to GOLDBEES. We considered all the news, IBJA prices, import export slashing hike, exchange prices, dollar denomination, etc. but seems the premature window of RBI has a big role to play giving downward pressure on SGBs. It just starts diverging (in SGBs favor) after the window closes i.e. exactly around April/May.

Anyhow, I ain’t complaining anymore … ![]()

2 Likes

SGB back in discount territory.

Btw, what software is shown in your screenshot?