The Reserve Bank of India (RBI) recently revised the Liquidity Coverage Ratio (LCR) to ensure banks have enough liquid assets to meet short-term obligations amid increasing digital transactions.

This was put in place looking at the increase in digital payments over the last few years. If a bank allows Internet & Mobile Banking to their customers, the bank has to provide 10% additional LCR where the deposits are stable and 15% additional LCR where the deposits are deemed unstable. The new norms will come into effect on 1st April 2025.

The ramifications for banks are essentially that they need to maintain more money in assets such as Gsecs and Tbills to provide the required liquidity. To understand this better, one may want to answer a few basic questions.

What is the LCR?

The LCR mandates banks to hold high-quality liquid assets to cover 30-day stress period liabilities, preventing bank runs and ensuring smooth financial operations.

Why does RBI feel digital payments can be a liquidity risk?

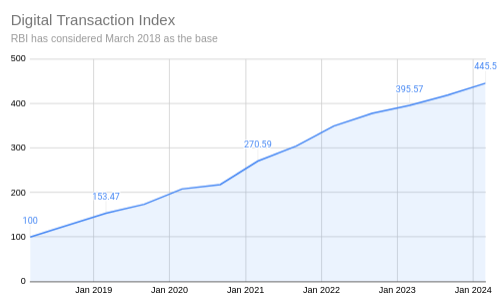

RBI maintains an index that tracks digital payment activity. The index has grown more than 4x since, from 100 in March 2018 to 445.5 in March 2024.

The RBI’s Digital Payments Index (DPI) measures the digitization of payments through:

Payment Enablers (25%): Internet and mobile penetration.

Payment Infrastructure – Demand-side factors (10%): Consumer access to digital payments.

Payment Infrastructure – Supply-side factors (15%): Availability of payment services.

Payment Performance (45%): Usage of digital transactions.

Consumer Centricity (5%): User experience and security.

Here is the announcement from RBI where they launched the DPI - Link.

True, I mentioned this comes into effect next year in April. In most likelihood, nothing will change. Since its a material change, its nice that RBI announced this through the draft really early.

The additional LCR used to be at 5% for stable deposits, which is now 10% for stable deposits with internet & mobile banking.

Most banks will already have the liquidity in place and not have given out loans to an extent where they maintain the minimum margin. This will be from the viewpoint of having enough liquidity for withdrawals even if the minimum to maintain is 5%. Now, the buffer maintained above the minimum number of 10% might not be too much.

Stable deposits are not necessarily fixed deposits (FDs). According to the Basel III Framework, stable deposits for the purpose of the Liquidity Coverage Ratio (LCR) are defined as:

Fully Insured Deposits: Deposits that are fully insured by an effective deposit insurance scheme.

Run-Off Rate: Deposits with a run-off probability of 5% or less in a 30-day period.

This means all deposits of less than ₹5 lakhs that appear to stay in the bank for at least 30 days without significant withdrawals will be classified under the stable retail bucket. This classification can include both FDs and funds parked in demand deposits, such as savings and current accounts, provided they meet the insurance and stability criteria.