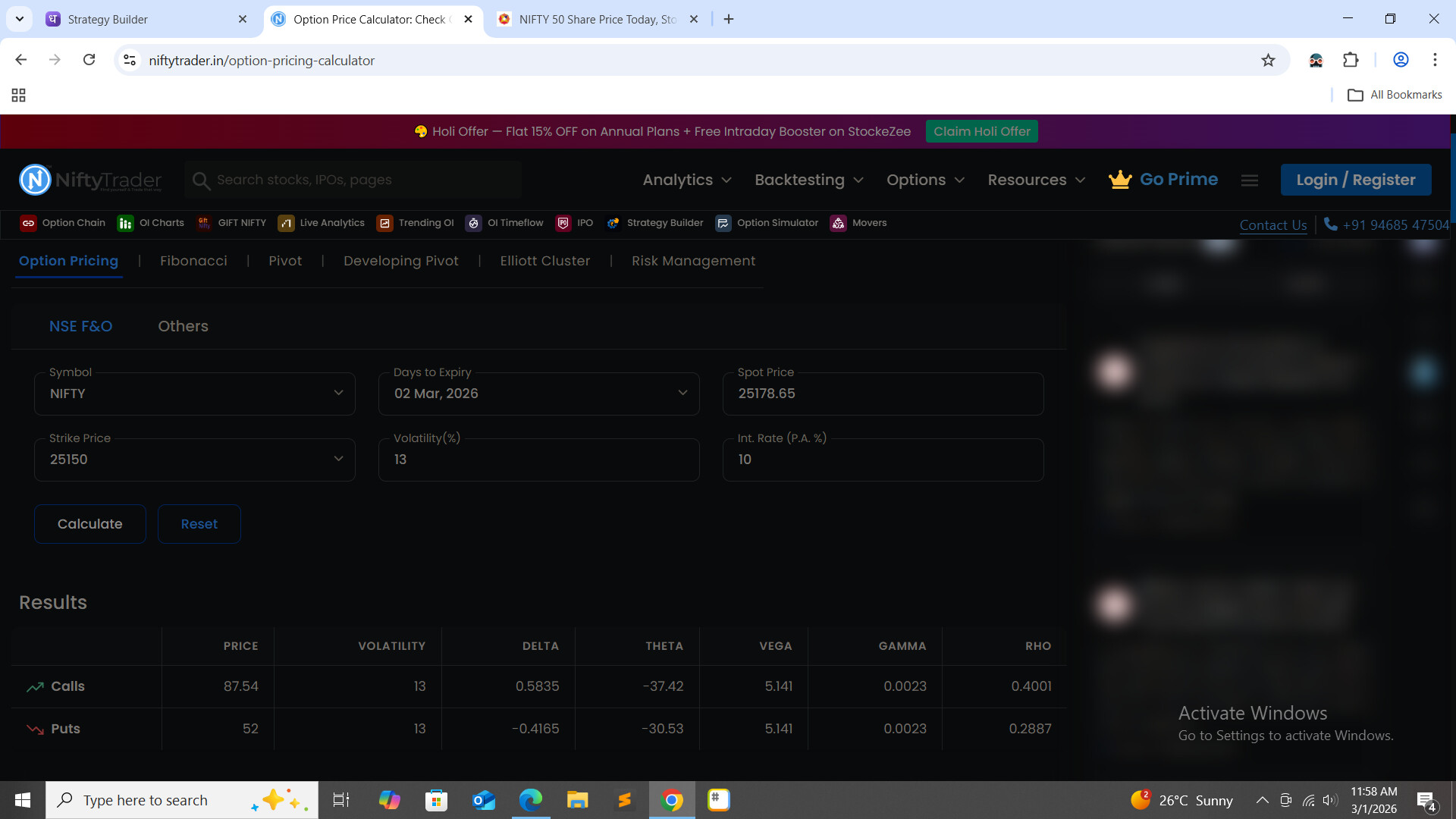

Since IV is obtained by reversing the Black–Scholes formula from the market price, I expected that using IV = 13% in the Bs model would reproduce the same option price.

However, the price I calculate using Black–Scholes is different from the NSE LTP.

Why does this mismatch occur? Does NSE use different assumptions for another method to compute IV? @BB789@niftymonk@nithin_kumrr