…and its highest on expiry day

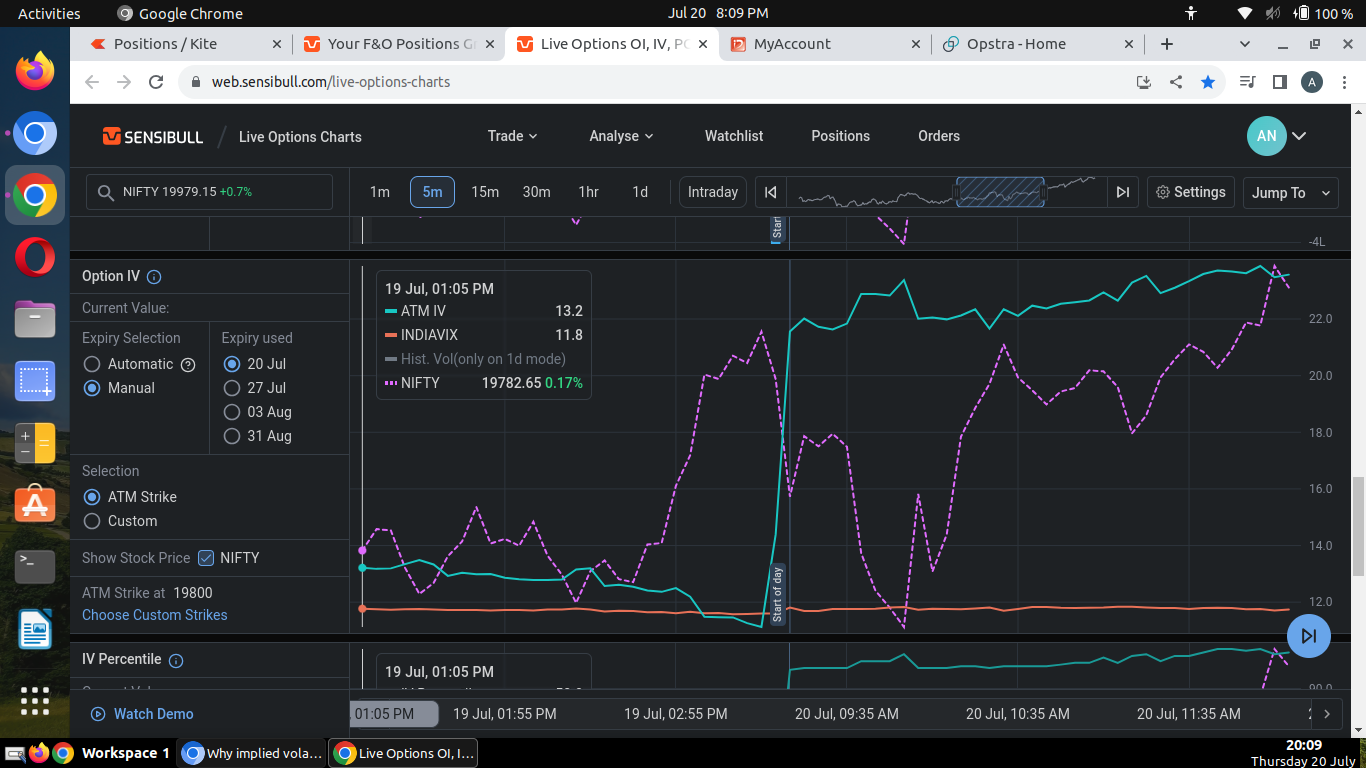

iv is calculated based on the current option prices & their bid-ask. iv doesn’t always increase as time passes, this is only happening in recent expiries. Reason:

recent expiries have consistently opened with very low option prices (participants expect low volatility). This is being proved wrong even before the first hour of trading. So, iv rises. If markets continue to behave more volatile than expected, iv will keep rising. Again, this is only the behaviour of recent expiries (& some other past periods of low iv)

what software/website are you using to calculate the IV - sensibull ?

IV is not the highest on the expiry day & it does not increase with the passage of time - well, for the days you measured it would have. But its not a recurring pattern.

my mistake …i misinterpreted it… figured it out .![]()

price is made up of intrinsic value + extrinsic value .>> & extrinsic value is made up of time value + implied volatility>>>> but implied value is derived from price of option …

its actually time value callapsing & only impled value left in price of option at start of expiry day ![]()