Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube.

In today’s edition of The Daily Brief:

- Will we pay more for our cooking gas?

- What’s happening with Indian Auto Giants?

Will we pay more for our cooking gas?

A recent CareEdge report made a simple but telling observation: LPG Under-recoveries of OMCs Expected to Reduce by ~45% Y-o-Y in FY26. That’s the kind of line you’d typically skim past, unless you happen to be one of those people who care deeply about LPG. If that’s the case, it’s a little sad.

But let’s say you’re not one of those people. What exactly is an under-recovery? Why does it matter? And does this all mean that we will pay more for our cooking gas?

Let’s start with the gas itself. LPG, or liquefied petroleum gas, is a mix of propane and butane—byproducts of oil refining and natural gas processing. It’s compressed into a liquid so it can be stored in pressurized steel cylinders and shipped just about anywhere. When released, it vaporizes, burns with a clean blue flame, and makes tea.

If you still don’t know what I’m talking about, it’s that red color LPG cylinder in your kitchen.

But what’s interesting is how India went from LPG being a luxury for the urban elite to something that fuels nearly every household kitchen in the country. In the 1960s, when Indian Oil launched its Indane brand, the idea of having a gas connection at home was novel. By the 1990s, it was slowly reaching middle-class homes in small towns. But for much of rural India, cooking meant firewood, cow dung, or coal.

Not only were these fuels inefficient and polluting, but they were a public health hazard. Women and children inhaled smoke every day while cooking.

That’s where the government stepped in.

For decades, the government provided LPG at a subsidized price. Initially, the subsidy was built directly into the cylinder price. But this led to leakages, diversion, and misuse. So in 2013, the government rolled out PAHAL—short for Pratyaksh Hanstantarit Labh—one of the world’s largest direct benefit transfer (DBT) schemes. Instead of selling subsidized cylinders, oil companies sold them at market price and the government deposited the subsidy directly into the customer’s bank account. The scale was enormous—over 200 million households linked their Aadhaar and bank accounts to their gas connections.

Then came the GiveItUp campaign. Launched in 2015, it asked well-off households to voluntarily surrender their LPG subsidy. Reportedly, millions of consumers responded, freeing up subsidy for needy households. This was the warm-up act for what came next: the Pradhan Mantri Ujjwala Yojana (PMUY).

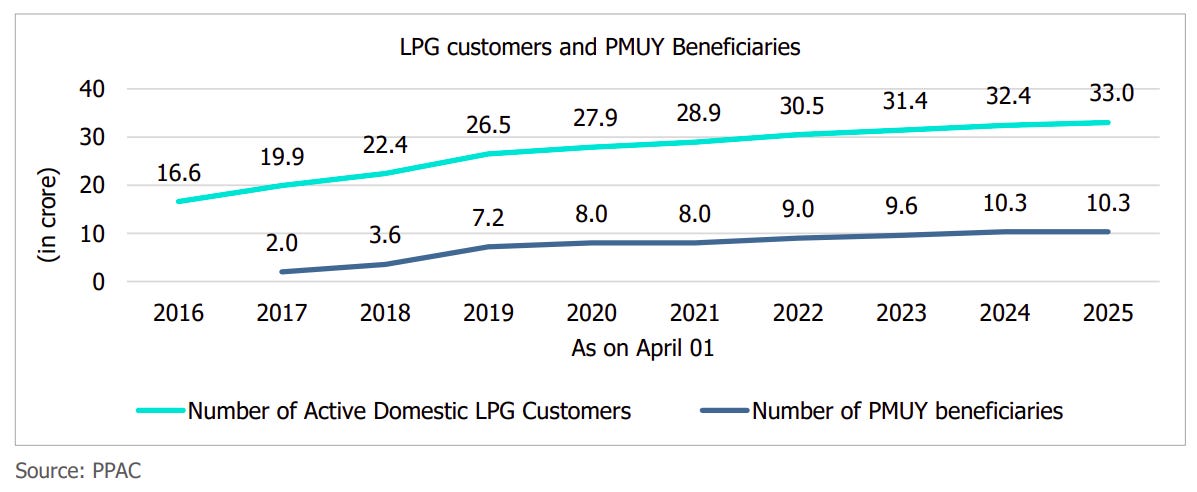

Ujjwala was launched in 2016 as a flagship welfare scheme aimed at energy access and women’s empowerment. It gave free LPG connections—including the cylinder, regulator, and hose—to women from below-poverty-line households. It was marketed not just as a convenience, but as a health intervention: clean kitchens, fewer respiratory issues, more dignity. And it worked. In just a few years, over 10 crore women received connections under the scheme. LPG coverage, which was at 62% in 2016, crossed 100% by 2024.

This 100% is possible because the coverage figure compares total active LPG connections to estimated households based on older census projections. With population growth, multiple connections in joint families, and households owning more than one cylinder (like double-bottle connections), the number of connections can exceed the estimated number of households, pushing coverage beyond 100%.

That kind of saturation, in a country as vast and diverse as India, is a logistical marvel.

But there was a problem. Many of those connections sat unused after the first refill. Poor households couldn’t always afford the next cylinder. So the government kept stepping in. During COVID, Ujjwala users got up to three free refills. Later, as global LPG prices rose, the government introduced targeted subsidies—₹200 per cylinder, then ₹300. In 2023 and 2024, general price cuts were rolled out for everyone: ₹200 in August, ₹100 in March. These were often timed around festivals or elections, but they helped.

And usage began to rise. By 2024, the average Ujjwala user was consuming 4.4 cylinders a year, up from 2–3 earlier. Total LPG consumption in the country grew 7% in 2024 after years of stagnation.

This, in a market with over 33 crore active connections and a delivery network moving 4–5 million cylinders a day, was a big deal.

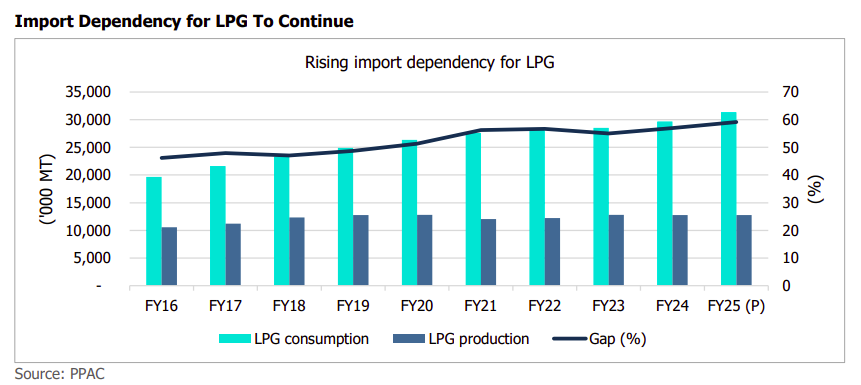

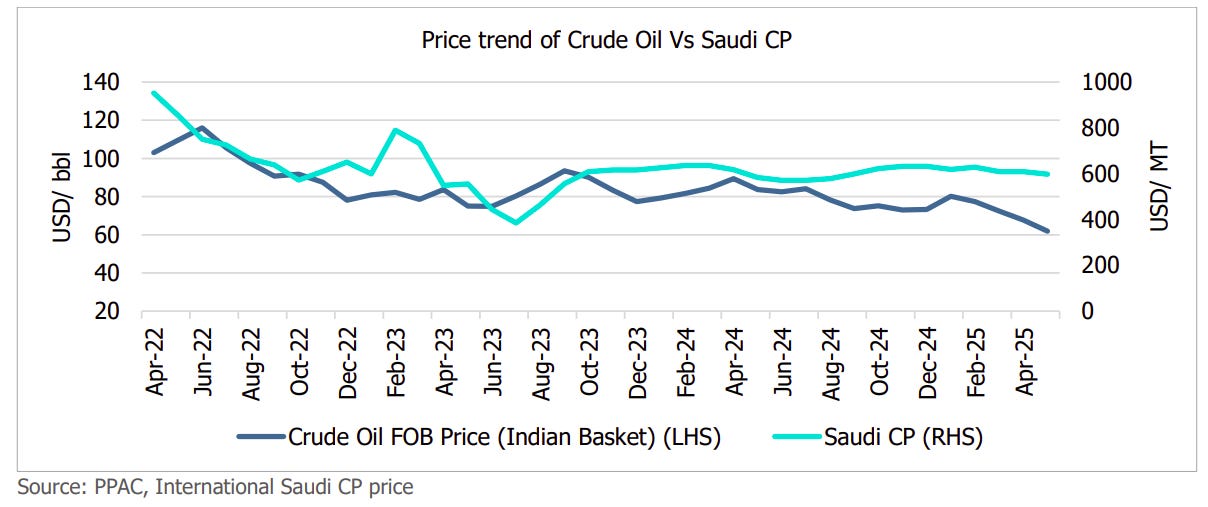

But all of this costs money. A lot of it. India imports nearly 60% of its LPG needs, mostly from the Middle East, and the prices are benchmarked to the Saudi Aramco Contract Price.

When global oil and gas prices rise, so does the cost of LPG. But domestic cylinder prices don’t always keep up, especially because of the political sensitivity. So oil marketing companies—IOC, BPCL, HPCL—sell at a loss.

That’s the under-recovery.

In April 2025, the government allowed a ₹50 price hike. The cost of a 14.2 kg LPG cylinder in Delhi rose from ₹803 to ₹853. This was a rare moment of price discipline. And it applied to everyone—even Ujjwala beneficiaries. They still got ₹300 back in their accounts, but now had to pay ₹553 upfront instead of ₹503.

BPCL’s Director of Finance, V.R.K. Gupta, didn’t sugarcoat the impact.

He added:

This cost of about ₹700 crore per month rounds off to over ₹8,000 crore annually for just one company. Add HPCL to the mix, and the scale becomes even more staggering.

HPCL’s Director of Finance, Rajneesh Narang, said:

To ease the pain further, BPCL and others are also looking at cheaper sources. Gupta said:

But there’s a technical hitch here—U.S. LPG tends to be richer in propane, while India’s domestic distribution network and appliances are calibrated for a specific propane-butane mix. Using propane-heavy LPG could impact pressure regulation and burner performance, which means OMCs need to either blend the imported fuel or upgrade infrastructure to accommodate it. So while American LPG may be cheaper on paper, its usability hinges on logistical and safety adjustments.

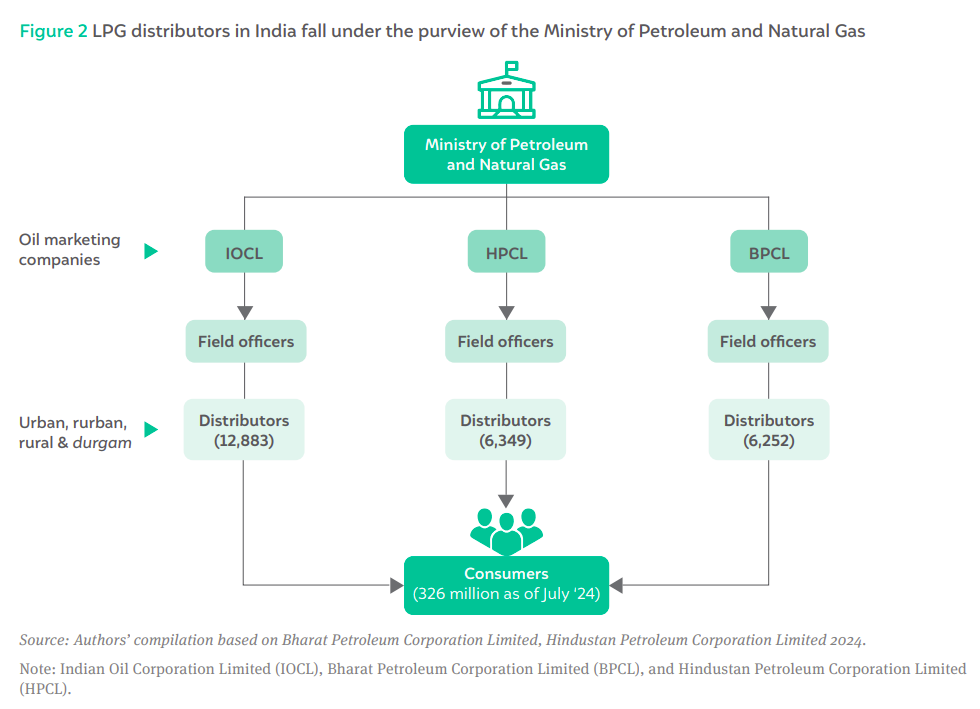

The LPG distribution network in India is one of the most extensive in the world. Over 200 bottling plants, more than 24,000 distributors, and delivery mechanisms that reach every district—urban or rural. Innovations like composite cylinders (lighter, translucent) and 2 kg mini-cylinders called “Munna cylinders” have also made LPG more accessible to students, migrants, and informal workers.

Today, India has nearly 33 crore active LPG connections.

Indane, BharatGas, and HP Gas—run by IOC, BPCL, and HPCL respectively—dominate the household market. Private players like Reliance and TotalEnergies serve industrial and commercial users but haven’t made a dent in the retail segment, mostly due to the subsidy structure that keeps pricing skewed.

So yes, LPG in India is a mature market. But it’s not a simple one. It’s propped up by direct subsidies, governed by global prices, and steered by political decisions. A 45% fall in under-recoveries, as CareEdge noted, is the result of careful adjustments: modest price hikes, softening import costs, and targeted welfare. It signals that the system is stabilizing.

But, how will things pan out in the future, we don’t know.

What’s happening with Indian Auto Giants?

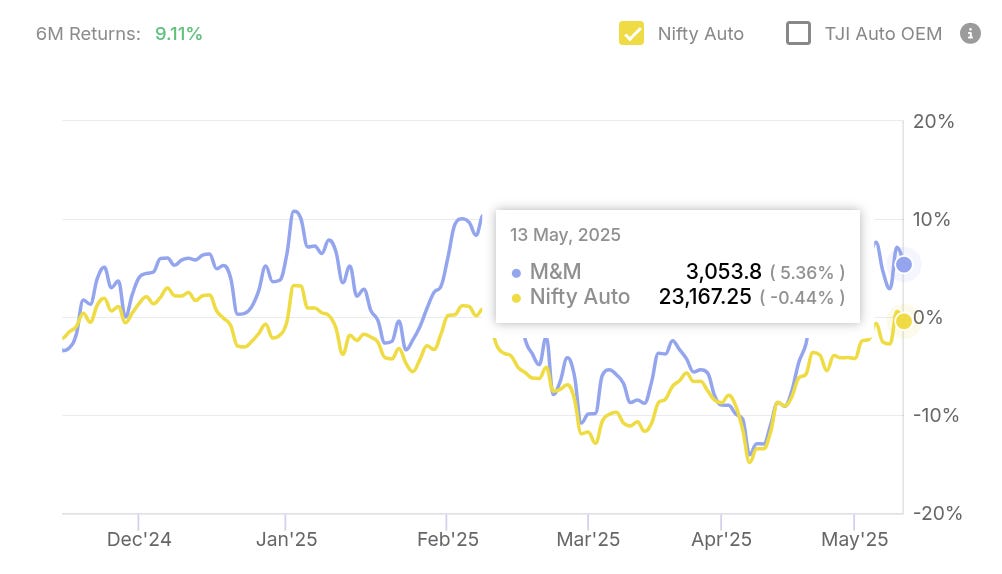

The Indian automobile industry, which is a decent proxy of our economic pulse, presented a complex, fascinating and somewhat bearish picture, as the biggest car manufacturers came up with their results for Q4FY25 lately.

The slowdown in the Indian auto sector around Q4 FY25 stems from a confluence of factors, including a high base effect after strong post-pandemic recovery which naturally makes current year-on-year growth percentages appear more moderate. Compounding this are persistent affordability concerns; vehicle prices have climbed due to stricter emission norms, increased raw material costs, and the addition of more safety and technology features, particularly squeezing the entry-level segments where buyers are most price-sensitive.

Sticky inflation further erodes disposable incomes, making consumers cautious about big-ticket discretionary spending. Concurrently, elevated interest rates, up until recently, have pushed up equated monthly installments (EMIs) for vehicle loans, directly impacting financing costs and deterring a segment of potential buyers or causing them to delay purchase decisions.

But, while the dust settles on a year of muted overall growth, three clear narrative emerges:

[i] the dominance of the Sports Utility Vehicle (SUV) against other categories is absolute; growing 11% YoY reaching 55% share in sales

[ii] the electric vehicle (EV) revolution in India is irrevocably underway,

[iii] the once-dominant small car segment is finding it hard to breathe degrowing by 12% YoY

For giants like Maruti Suzuki, Tata Motors, and Mahindra & Mahindra, FY25 was less about a smooth highway cruise and more about skillfully making its way through shifting consumer desires, margin pressures, and the high-stakes game of EVs.

The overall passenger vehicle market itself saw a modest uptick, with provisional estimates of sales around 4.3 to 4.34 million units in FY25, a growth of roughly 2-2.6%. This was a significant slowdown from the 8.4% growth witnessed in the last year, a cooling largely attributed to a high base and persistent affordability concerns, especially at the entry-level (read: hatchback).

Let’s talk about the big three players in the listed space one at a time.

Mahindra’s SUV Juggernaut gives it profits and power

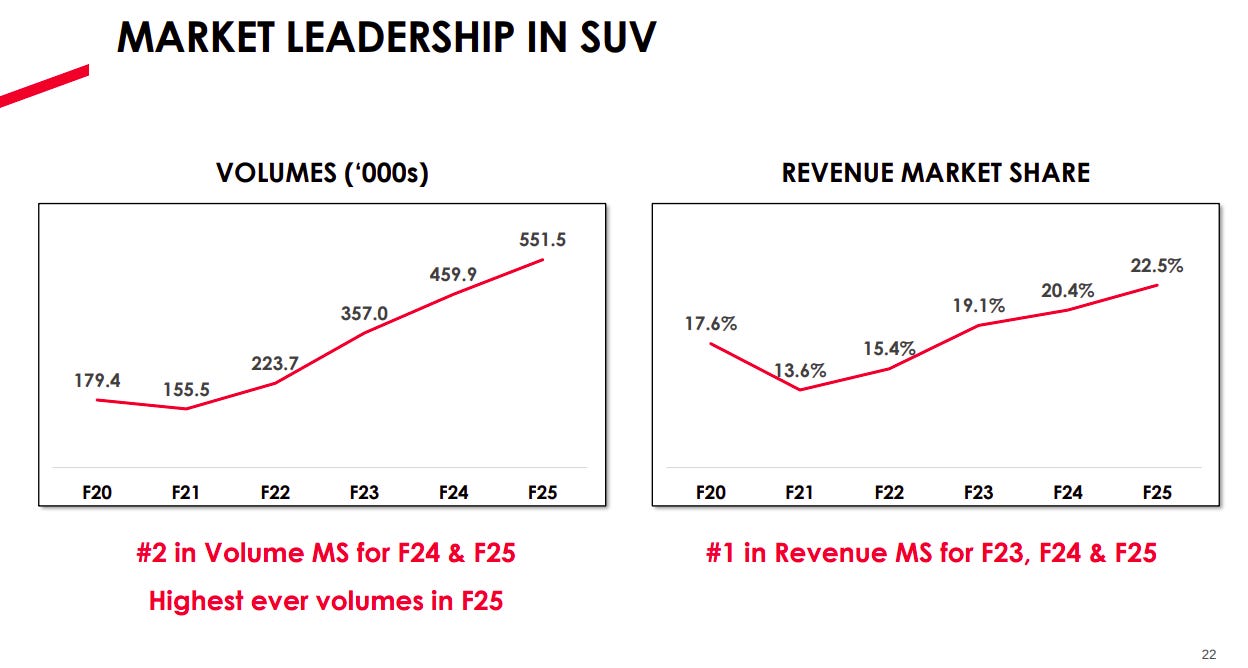

If there was one clear victor in the current market scenario, it was Mahindra & Mahindra (M&M). The company’s automotive segment, powered by its arsenal of popular SUVs like the Thar, Scorpio-N, and XUV700, was firing on all cylinders. Since it doesn’t have a product portfolio in hatchbacks, it was immune to the muted growth in that segment that affected the rest of the Indian auto players.

M&M reported a stellar 20% year-on-year growth in SUV volumes for FY25. This translated into a commanding SUV revenue market share of 22.5% for the full year, an increase of 210 basis points, which further climbed to 23.5% in Q4FY25.

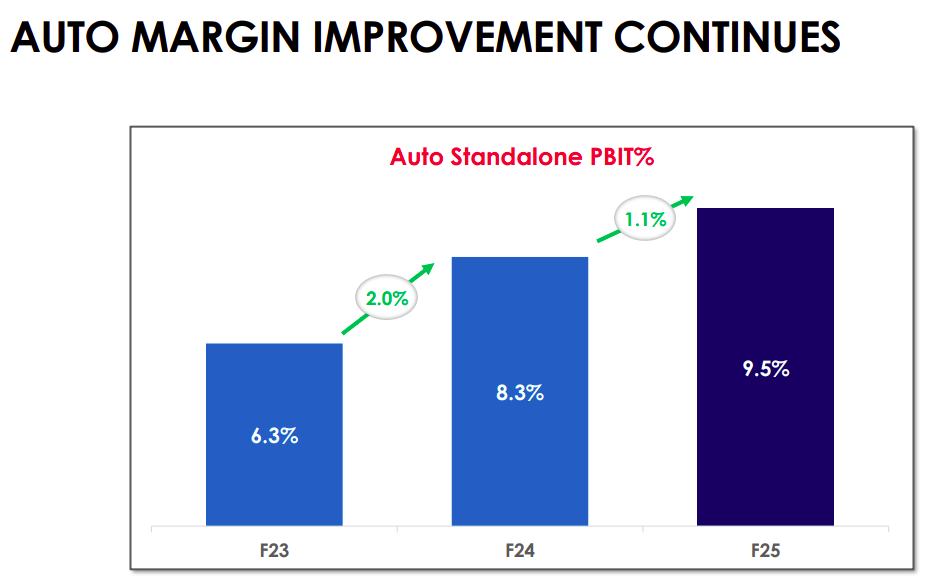

The financial muscle accompanying this volume growth was equally robust. M&M’s standalone auto segment PBIT (Profit Before Interest and Tax) margin for FY25 stood at a healthy 9.5%, an improvement of 110 basis points year-on-year.

Perhaps most tellingly, the automotive segment delivered an exceptional Return on Capital Employed (ROCE) of 45.2% in FY25, showcasing highly efficient capital utilization, compared to ~17% for Tata Motors and ~22% for Maruti Suzuki.

“We continued our outstanding performance… with significant gain… in SUV revenue share,” stated Mr. Rajesh Jejurikar, Executive Director & CEO (Auto and Farm Sector), M&M, reflecting the company’s confidence.

The EV story for Mahindra also sparked considerable excitement. Its “Born Electric” (BE) range of eSUVs garnered a staggering 30,179 bookings on the very first day of launch, with 6,300 eSUVs delivered during FY25. But it is far from perfect, as it struggles with software bugs.

While the company is investing ₹12,000 crore in the PV-EV space by 2027, the immediate challenge lies in ramping up production to meet this electrifying demand and managing waiting periods for its blockbuster ICE models.

Maruti Suzuki got saved by the export shield but suffered from the small car squeeze

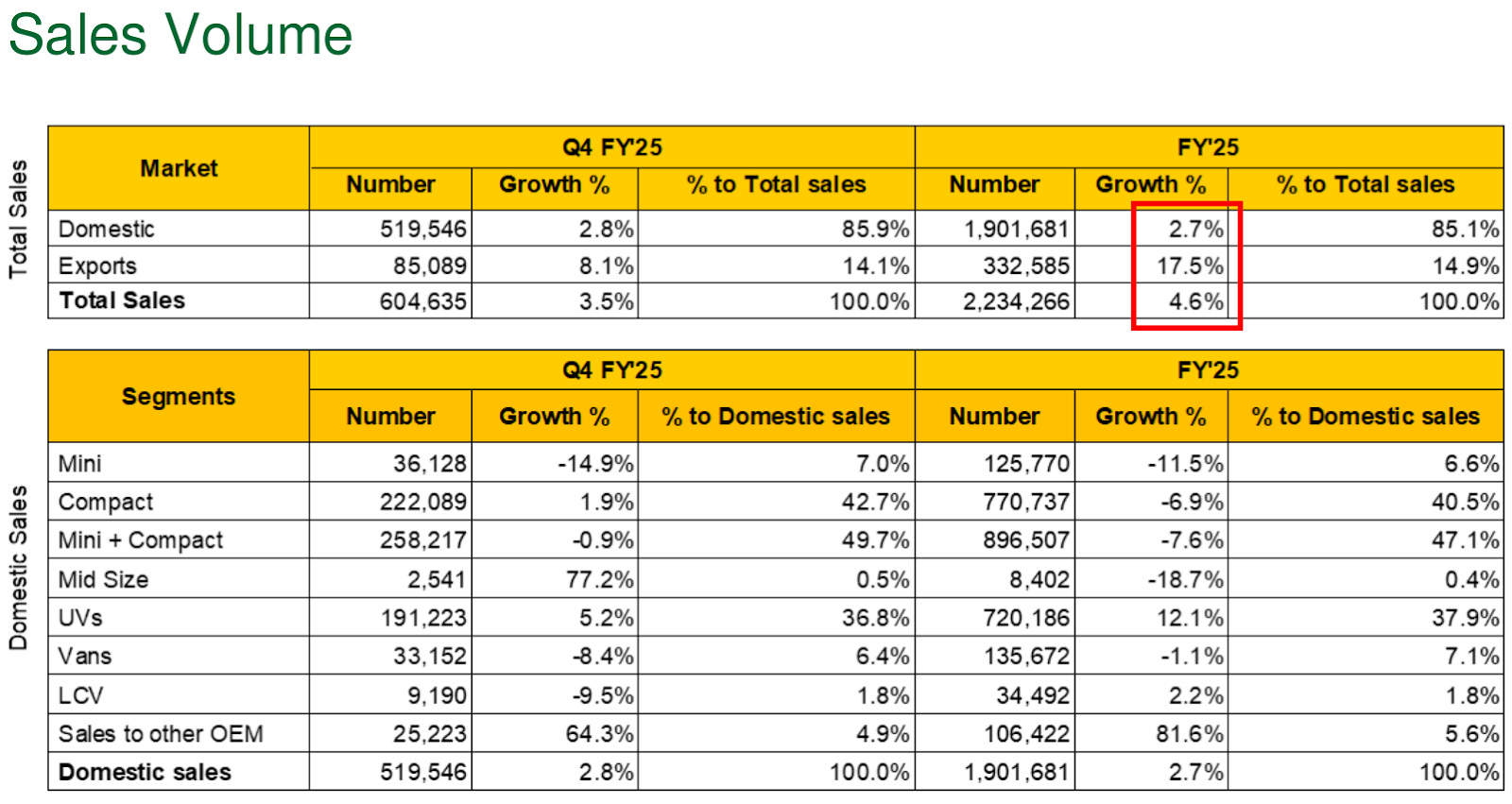

Maruti Suzuki India Ltd. (MSIL), the long-standing market leader, experienced a year of contrasts. The company achieved its highest-ever overall sales of 2.23 million vehicles in FY25, a 4.6% aggregate growth. This was significantly achieved by a record export performance growing 17.5% YoY. Had it not been for this export performance, the results

“The company continues to be the top exporter for the fourth consecutive year, now contributing nearly 43 per cent of total passenger vehicle exports from India,” MSIL stated, highlighting this crucial buffer.

However, the domestic story was more subdued, with a modest 2.7% growth. The shrinking hatchback segment, once Maruti’s undisputed kingdom, continued to be a pressure point. These are smaller and affordable cars, compared to the Utility Vehicle (UC) segment, which cater more to the premium segment.

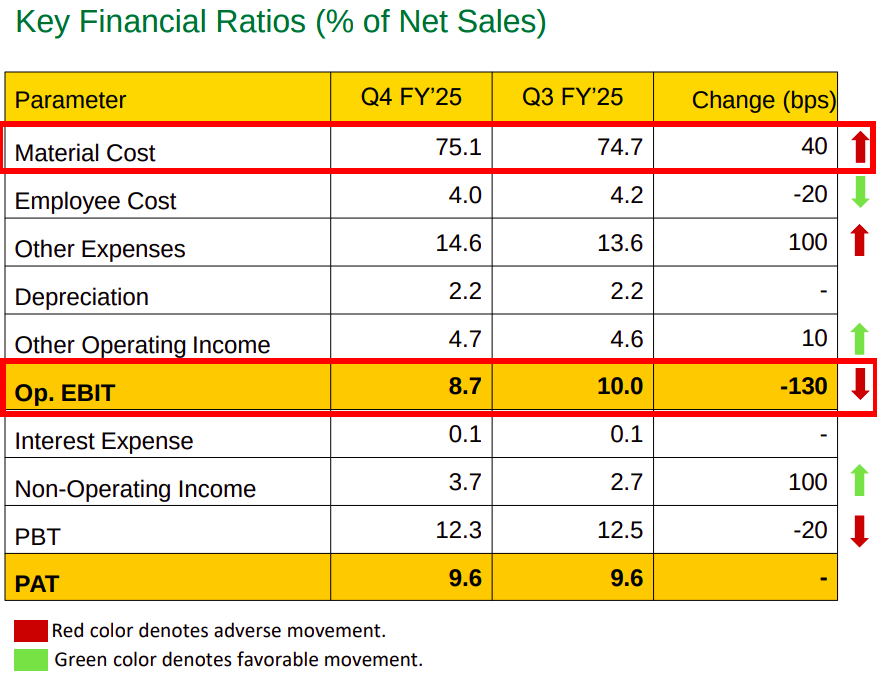

Industry-wide, hatchback share plummeted to about 23.5% in FY25 from 46% in FY19. This structural shift, coupled with rising input costs and overheads from its newly commissioned Kharkhoda plant, caused the company’s operating profit (EBIT) margin contract to 8.7% in Q4FY25 from 10% in the preceding quarter.

Commodity price increases, particularly steel, also played spoilsport, creating an adverse impact of about 20 basis points in the quarter.

On the bright side though, the company is pinning significant hopes on its upcoming electric SUV, the e VITARA, scheduled for launch in H1FY26. A substantial portion of its projected 70,000 annual units are earmarked for export.

Chairman R.C. Bhargava acknowledged the domestic challenges, stating, “Maruti’s domestic growth at 3% in FY25. Overall automotive penetration is still worrying,” and pointed to the high cost of regulations making small cars unaffordable. We covered this in depth in our episode of “Who Said What” some time back.

Tata Motors had their EV leadership tested and saw volumes dip

Tata Motors’ overall automotive story in Q4 FY25 and the full fiscal year was one of contrasting performances across its key divisions. Its Indian Passenger Vehicle (PV) business, encompassing both Internal Combustion Engine (ICE) and Electric Vehicles (EVs), presented a complex narrative of segment-specific successes amidst overarching volume challenges.

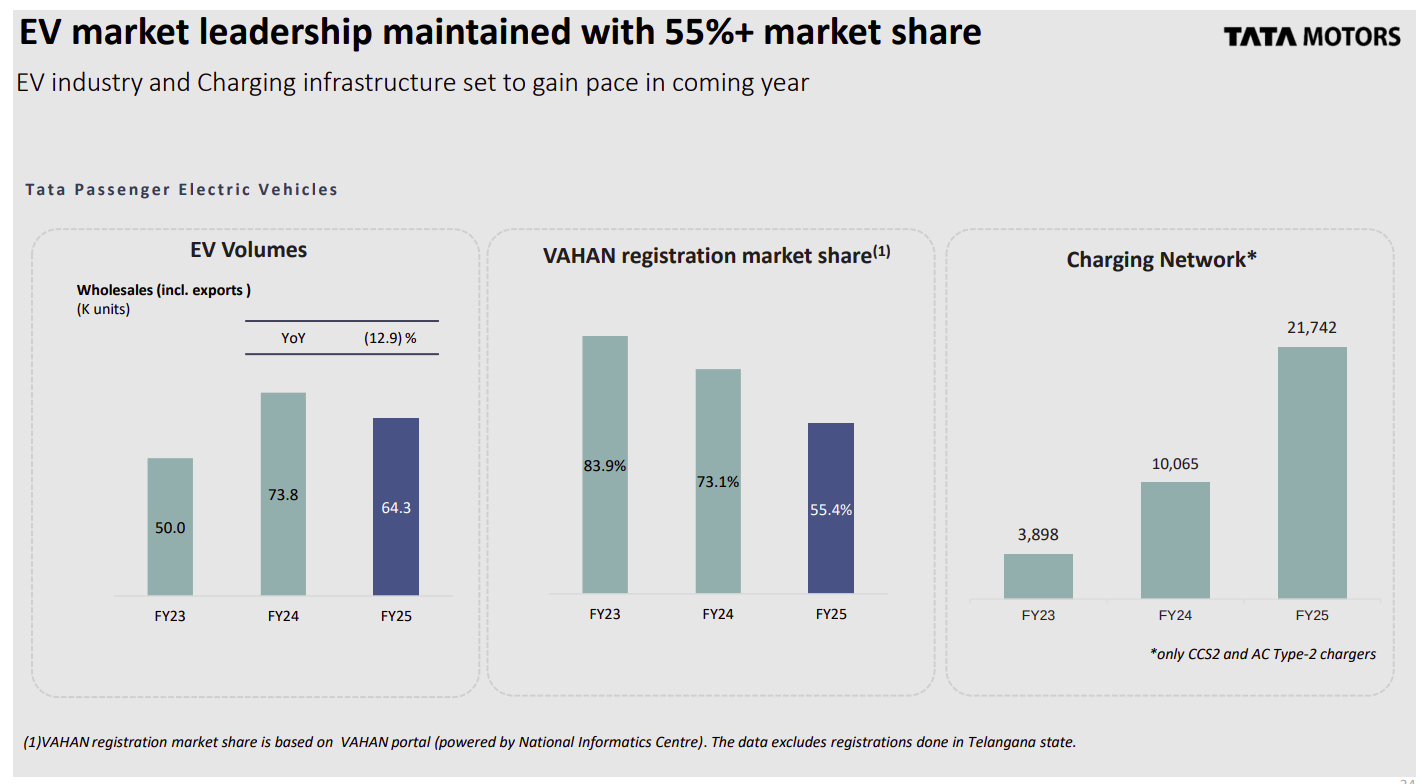

The company maintained its leadership in the Indian EV market, with a 55.4% share in FY25, and saw its CNG segment sales surge by over 50%. The Tata Punch notably emerged as India’s top-selling SUV among private buyers in FY25.

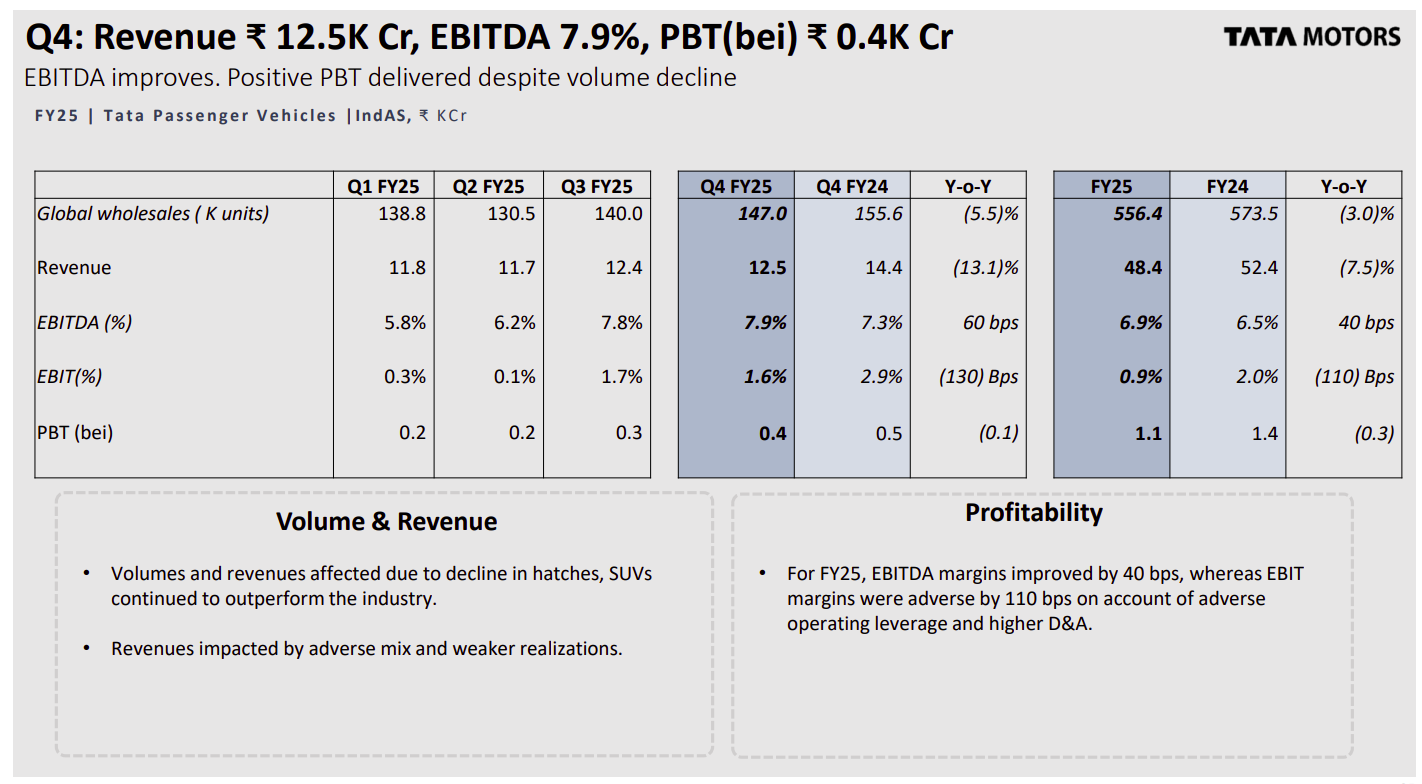

However, these bright spots were overshadowed by a 3% YoY decline in total PV sales for FY25, down to 5.5 lakh units. Domestically also, sales dipped by approximately 3%.

The company attributed this primarily to a sharp fall in hatchback sales. This volume dip impacted financials, with PV segment revenue for FY25 falling 7.5% YoY. While EBITDA margins for the segment showed a slight improvement to 6.9% for FY25, EBIT margins contracted to 0.9%.

Why? Due to adverse operating leverage and higher depreciation. As companies sold lesser cars this year, on the same base of fixed cost as the last year, margins are likely to depress.

Also, they are continually investing in refreshing its existing PV portfolio and developing new models along with substantial capital expenditure in R&D, tooling, and manufacturing setups in EV. This shoots up depreciation and amortization costs by a huge leap.

When comparing the powertrain performance within the Indian PV business for FY25, the ICE business delivered an EBITDA margin of 8.2% in FY25, while the EV business was EBITDA positive at a slender 1.2%. If we exclude the product development expenses, margin goes up to 6.8%.

So overall, the things are looking really bleak for them, but Tata Motors aims to “regain its winning momentum” with new launches like the Curvv.ev and Harrier.ev. Another pivotal moment awaits with the planned demerger of its PV and EV businesses from the commercial vehicle arm, approved by shareholders and expected to be effective from October 1, 2025. We covered this too earlier in The Daily Brief .

The Road Ahead

The Q4FY25 results paint a clear picture: the Indian car buyer’s love affair with SUVs is intensifying, forcing all players to double down on this segment. Maruti, despite its small car legacy, is aggressively launching UVs, while M&M continues to reap the rewards of its focused SUV strategy.

All this while, the hatchback segment remains “the lost child” of the Indian automobile industry, which once was the star of the show in the previous decade. This makes us question, what is causing this? Is this the “premiumization” trend play out as people shift preference from hatchback to SUVs, or is this more an affordability problem which makes even hatchbacks out of reach of millions of Indians as Maruti’s boss pointed out.

The EV transition is the other major undercurrent. While Tata Motors has an early lead, its market share is being challenged as competitors like M&M enter with strong initial responses, and Maruti prepares for its EV debut. Profitability in the EV segment remains a critical hurdle for all, as acknowledged by Maruti’s management, while EVs continue to get affordable abroad.

Looking towards FY26, the industry anticipates modest single-digit growth, with much depending on macroeconomic factors, a favorable monsoon boosting rural demand, and the successful rollout of new models. Cost pressures from volatile commodity prices and the capital-intensive nature of the EV shift will continue to test these automotive titans. The journey ahead is undeniably electric and increasingly dominated by the high-riding stance of SUVs, but it’s a road that promises more twists and turns before a clear long-term winner emerges.

Tidbits

Hero MotoCorp Q4 Profit Rises 24%, FY25 Sees Record Revenue and Dividend

Source: Business Line

Hero MotoCorp reported a 24% year-on-year rise in consolidated net profit to ₹1,169 crore for Q4 FY25, up from ₹943.46 crore in the same quarter last year. Revenue from operations during the quarter increased by 4% to ₹9,970 crore. For the full financial year, the company posted a net profit of ₹4,376 crore, marking a 17% increase over FY24, while annual revenue grew 8.29% to ₹40,923.42 crore. Unit sales for FY25 stood at 58.99 lakh, up 5% from 56.21 lakh units in FY24, although Q4 sales dipped slightly to 13.81 lakh units from 13.92 lakh units in the previous year. The company credited its performance to premium segment growth, stronger scooter sales, and cost efficiencies. Hero MotoCorp also declared a total dividend of ₹165 per equity share for FY25, including a final dividend of ₹65 and an interim of ₹100, translating to a payout of 8,250%.

India’s Retail Inflation Eases to 3.16% in April, Lowest Since July 2019

Source: Reuters

India’s retail inflation slowed to 3.16% in April 2025 from 3.34% in March, marking its lowest level since July 2019 and staying below the Reserve Bank of India’s 4% target for the third consecutive month. Food inflation, which accounts for nearly half of the consumer basket, dropped to 1.78%—the lowest since October 2021—compared to 2.69% in March. Vegetable prices saw an annual decline of 11%, sharper than the 7.04% fall recorded a month earlier. Cereal inflation eased to 5.35% from 5.93%, while prices of pulses fell 5.23%, widening from a 2.73% drop in March. Core inflation remained stable at around 4% to 4.1%, indicating steady underlying demand. Following this trend, economists expect the RBI to consider another 25 basis point rate cut in its June policy review. The central bank has already shifted its stance to ‘accommodative’ and revised its inflation outlook to 4%, down from 4.2%, while lowering GDP growth estimates for the current fiscal year from 6.7% to 6.5%.

Airtel Posts 432% Jump in Q4 Profit to ₹11,022 Crore, ARPU Steady at ₹245

Source: Business Standard

Bharti Airtel reported a 432% year-on-year rise in net profit for Q4 FY25 at ₹11,022 crore, compared to ₹2,071.6 crore in the same period last year. The sequential net profit, however, declined by 25.4% from ₹14,781 crore in Q3 FY25. Consolidated revenue rose 6.08% YoY to ₹47,876 crore, with India revenue up 28.8% to ₹36,735 crore. The mobile services segment grew 20.6%, driven by tariff hikes and premiumisation efforts. Average revenue per user (ARPU) remained flat at ₹245 quarter-on-quarter, maintaining the highest level in the industry. The customer base in India expanded by 10 million to reach 424 million in Q4. EBITDA stood at ₹25,404 crore with a margin of 57.2%. The quarter also included gains from Airtel’s increased stake in Indus Towers, approved by the CCI in October.

- This edition of the newsletter was written by Krishna and Kashish.

Have you checked out The Chatter?

Have you checked out The Chatter?

Every week, we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Have you checked out One Thing We Learned?

Have you checked out One Thing We Learned?

It’s a new side-project by our writing team, and even if we say so ourselves, it’s fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That’s all. It’s chaotic, it’s unpolished - but it’s honest.

So far, we’ve written about everything from India’s state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you’re looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()