Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Rare conditioning

- The business of beauty

Rare conditioning

This story has taken us in directions we didn’t foresee.

Recently, Panasonic announced it wants to become the largest air-conditioner player in India within seven years. That got us peeking at some numbers about the penetration of ACs in India. Around 8% of Indian households own an AC. In China, that figure is over 150% — on average, a Chinese urban household owns more than one.

Right now, India is where China was in the mid-1990s. And China’s growth since then is staggering: urban AC penetration went from 5% to nearly 100% in just 15 years. They added over 200 million ACs in that window. India may be at the start of that same curve. We’re selling about 10-11 million ACs a year right now, and could double this by FY30.

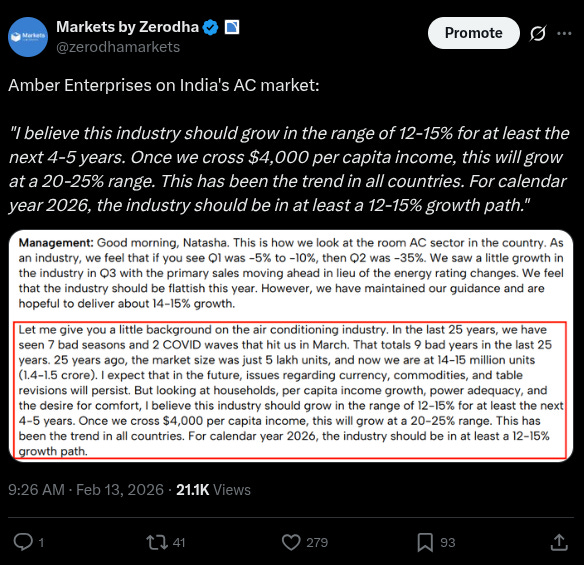

Amber Enterprises was particularly optimistic about this possibility in their recent earnings call:

However, this story isn’t really about projections and market sizes. Rather, it’s about one contingent factor that could shape the nature of this growth. And it has a lot to do with how ACs consume power.

The grid problem

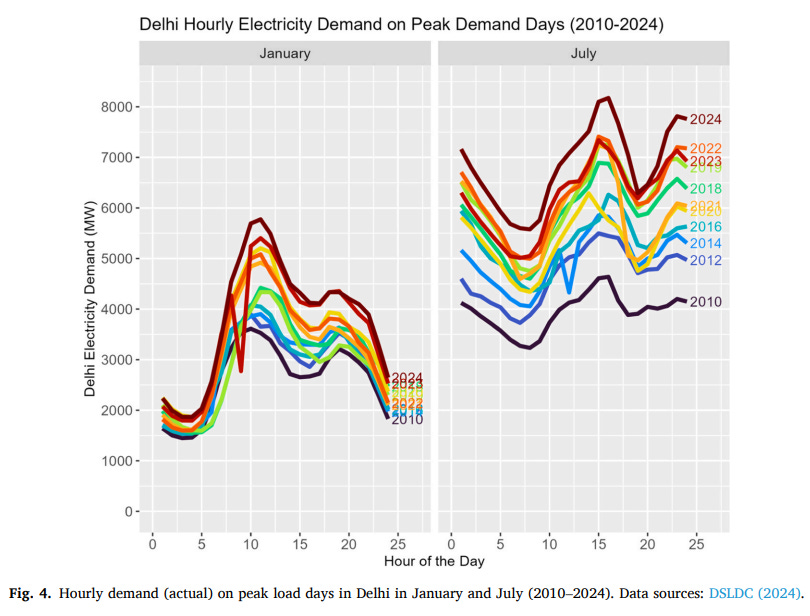

See, every time an AC is installed, it draws electricity from the grid. And when millions of people turn their ACs on at 3 PM on a hot May afternoon, the power grid takes a massive hit.

In 2024, India’s national peak electricity demand crossed 240 GW, to which room ACs alone contributed 40–50 GW. In just Delhi, peak electricity demand has nearly doubled between 2010-2024 to over 8,500 MW in 2024, driven primarily by cooling.

Now, India is expected to add about 130 million new ACs between 2025 and 2035. A study from UC Berkeley estimates that if the power efficiency standards improve at their current slow pace, room ACs alone could account for 180 GW of peak demand by 2035. That’s a third of the entire projected national grid. To put that in perspective, 180 GW is roughly comparable to the entire installed electricity generation capacity of Germany. Just from ACs.

This isn’t just a problem for 2035. India could face a 26 GW peak-capacity shortfall as early as 2028, leading to actual power shortages.

The AC market is going to boom regardless. But will those ACs be efficient enough that the grid can handle them?

Power efficiency

That question brings us to the real heart of this story: how efficient is your air conditioner?

An AC’s job is to move heat from inside your room to outside. An “efficient“ AC does the same cooling but uses less electricity to do it.

India measures this using something called the Indian Seasonal Energy Efficiency Ratio, or ISEER. The metric answers a simple question: for every unit of electricity your AC consumes, how many units of cooling does it produce on average across an entire season? A higher ISEER number means more cooling per unit of electricity, and therefore better efficiency.

Right now, the least efficient AC you can legally sell in India has an ISEER of about 3.3. The most efficient AC on the Indian market today — a specific Daikin model — has an ISEER of 6.3. Both cool your room to the same temperature, but the Daikin uses roughly half the power to do it.

That’s a big gap. And what most people end up buying sits somewhere in the middle.

Now, you’ve seen the BEE star labels on ACs — the sticker that says 1-star, 3-star, 5-star. Most of us glance at it and move on. But the system is more important than people think.

The Bureau of Energy Efficiency (BEE), which sits under the Ministry of Power, takes the ISEER scale and slices it into five bands. Each band gets a star rating. So if your AC has an ISEER between, say, 3.3 and 3.5, it’s 1-star. Between 3.5 and 3.8, it’s 2-star. And so on, all the way up to 5-star. The star rating hopes to tell consumers how much they could save in their electricity bills.

Now, the 1-star band — the very bottom of the star system — is effectively India’s Minimum Energy Performance Standard, or MEPS. Any AC that falls below 1-star efficiency simply cannot be legally sold in India. In an ideal scenario, as ACs become more efficient over time, the MEPS should increase in order to reflect how much better the baseline AC has become.

Except, that’s where the problems begin for India.

The fault in our stars

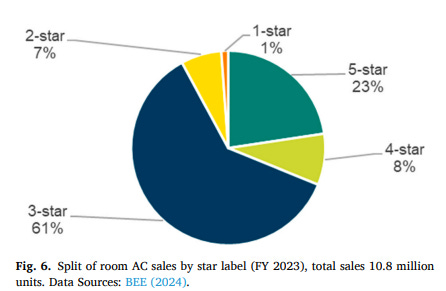

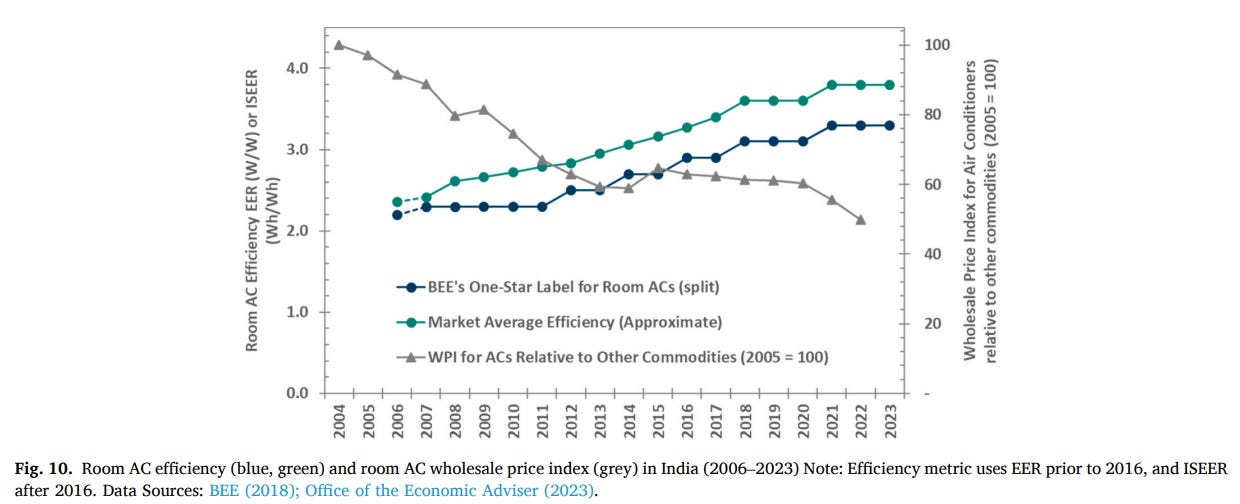

India’s MEPS has been rising, but very, very slowly. Over the past decade, it has improved by just 2–3% a year. The current 1-star minimum sits at an ISEER of around 3.3. Remember, the best AC in India today is at 6.3. The best AC sold anywhere in the world — a Samsung model — is at 7.4.

The market reflects the low MEPS. In FY23: ~60% of all ACs sold were 3-star, and 23% were 5-star.

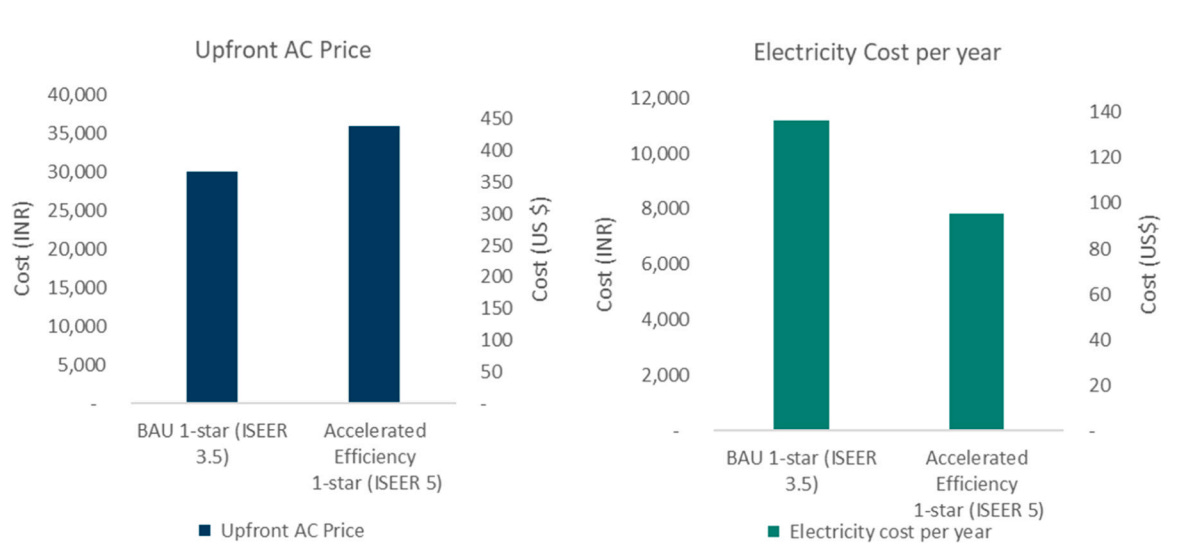

Most consumers walk into a shop and make a decision based on the upfront price. The ₹30,000 AC looks more attractive than the ₹37,000 one, even if the cheaper one will cost ₹3,000 more every year in electricity bills. People don’t do that math at the billing counter. The cheaper AC cools the room, and that’s good enough. “Bas AC chalna chahiye”.

This is exactly why MEPS matters so much. You can’t rely on consumers to always pick the most efficient option. But if you raise the floor, the inefficient options simply disappear from the shelf. The consumer doesn’t need to make the “right” choice because the wrong choice no longer exists.

China just does things

China is the most dramatic example of what happens when you raise the MEPS floor aggressively.

By the mid-2000s, China’s AC penetration was already climbing fast. Incomes were rising, cities were expanding, and hundreds of millions of people were buying their first ACs. By 2008, urban penetration had hit nearly 100%, and by 2023, it crossed 150%. The growth was happening regardless of any regulation.

But here’s what China recognized: the type of ACs people were buying mattered enormously for their power grid. Most of the ACs being sold were cheap, fixed-speed models. To understand why that matters, you need to know the difference between fixed-speed and inverter ACs.

A fixed-speed AC has a compressor that works like a light switch — it’s either fully on or fully off. When you turn it on, the compressor runs at full blast until the room hits the target temperature. Then it switches off completely. The room slowly heats up again, the compressor kicks back on at full blast, and the cycle repeats. This constant on-off cycling wastes a lot of energy.

An inverter AC, in contrast, works more like a dimmer switch. Once the room approaches the target temperature, the compressor doesn’t switch off, but slows down. It keeps running at low speed, maintaining temperatures with minimal energy. This is why inverter ACs are typically 30–50% more efficient than fixed-speed ones.

Around 2019, China dramatically overhauled its AC efficiency standards. Basically, they changed their version of MEPS, and set the new minimum so high that fixed-speed ACs couldn’t meet it anymore. As a result, inverter ACs went from occupying ~60% of the market to 98% almost overnight. The old “5-star” equivalent became the new baseline.

Importantly, AC prices didn’t go up. As manufacturers shifted production entirely to inverter models, economies of scale kicked in and manufacturing processes improved, while competition also increased. The “premium“ product became commoditized, and mass-market products got even cheaper. During the period when efficiency more than doubled, average AC prices fell steadily for China.

In India’s own market, between 2007 and 2023, AC efficiency improved by about 60%, while inflation-adjusted prices nearly halved. The pattern is quite consistent across countries at this stage of their growth. For us, inverter ACs now make up about 75% of sales, up from essentially zero in 2015. But that still leaves 1 in 4 new ACs being sold as fixed-speed.

Moving the goalpost

Meanwhile, India hasn’t been standing completely still on this. BEE does revise the star rating thresholds every few years. The most recent revision took effect in January 2026: the ISEER values needed for each star went up. So, an AC that was 5-star last year might now be labeled 4-star. A 3-star might now be a 2-star. Basically, the goalposts move.

This is a good thing, as it pushes manufacturers to keep improving. But some argue it’s not enough. And the reason is that while these revisions raise all the star thresholds, the floor — the 1-star minimum — has still not significantly moved over time. As a result, the market keeps clustering around “good enough” rather than “actually efficient.”

A research paper by Nikit Abhyankar et al. proposes that making a big, deliberate jump in the minimum standard could potentially make a radical difference. That, the paper says, is what countries like China and Japan have done. Specifically, the study proposes a staircase that spans the next few years:

- In 2027, set the 1-star minimum at ISEER 5.0 — that’s equivalent to today’s 5-star level. This sounds aggressive, but over 600 AC models already on the market today exceed this level. 20% of models are already there.

- In 2030, set 1-star at ISEER 6.3 — the most efficient AC currently sold in India — the Daikin model we mentioned earlier.

- In 2033, set 1-star at ISEER 7.4, matching the best AC sold anywhere in the world. This would need supporting measures like government bulk procurement programs to drive costs down.

All of this could potentially triple the pace of efficiency improvement from about 3% a year to about 8%.

If India follows this accelerated path, by 2035, we could potentially save 118 TWh of electricity per year, and avoid about ₹7.5 trillion in grid investments. The same 200 million ACs would cool the same rooms to the same temperatures at far less power than they do today.

Conclusion

Clearly, power standards can play a huge role in shaping the domestic AC market. But one lens we couldn’t focus on as well is that of the power grid itself. How it is managed by India or China would also play a huge role in determining how ACs get adopted. While we can’t address those differences here, we have covered how India’s power grid has plenty of bottlenecks to resolve.

[

India’s state discoms are at the cusp of a big change

](India’s state discoms are at the cusp of a big change)

·

18 December 2025

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

India added 50 million ACs in just the five years between 2019 and 2024. Another 130 million are coming in the next decade. The AC boom already has plenty of tailwinds supporting it. The only question is whether we’ll be smart about it before the grid forces us to be.

The business of beauty

Warren Buffett famously stuck to a core principle while investing: he would only invest in things he understood. That is generally sage advice. Occasionally, though, it can also leave you with glaring blindspots.

Here is one such: to our team of male writers, the beauty and wellness industry, so far, seemed distant and alien. Although it’s one of the largest parts of the consumer market, with space for several billion-dollar businesses, The Daily Brief has been more comfortable talking about rockets and computer chips than, well, a simple moisturising lotion.

But no more. Today, we’re looking at the fascinating world of beauty and personal care products.

To understand this industry, we’ll look at three companies that occupy three very different nodes. We begin upstream, looking at Galaxy Surfactants to understand the chemicals and ingredients that make this industry possible. Then, we turn to Honasa, the parent company of Mamaearth, which has built a bustling business around routine personal care products. Finally, we look at the largest of the three — FSN E-Commerce Ventures, more popularly known as Nykaa, which runs a complex, multi-faceted retail and distribution machine.

Galaxy Surfactants

Let’s begin with a company that isn’t visible in the industry, but is critical to how it runs: Galaxy Surfactants.

Galaxy Surfactants is an ingredient supplier for consumer beauty and personal-care brands. Every shampoo or sunscreen you buy, after all, is fundamentally a chemical formulation. Galaxy’s trade lies in supplying those chemicals.

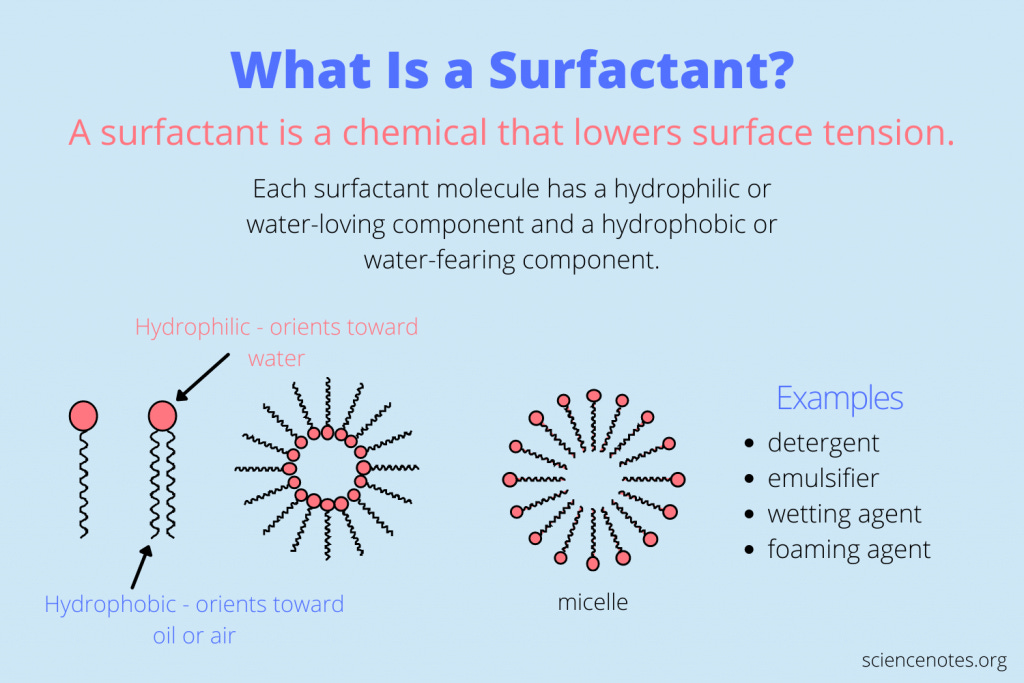

It has two main business lines. The first is surfactants: which, at its simplest, are chemicals that force oil and water to work together. That solves the core problem of cleaning anything: it’s hard to clean grease with water. Surfactants bridge that divide; they make it possible to wash away grease. That’s why they’re the key ingredient in everything from shampoo to detergent.

Galaxy also sells a range of other chemicals, which it calls “specialty care products”. For one example, Galaxy has a range of “sunclipse” molecules, which is what makes it possible for “leave-on” products to last when worn outdoors.

Behind everything that a beauty brand promises you: from performance, to gentleness, to long-lasting protection, there’s a company like Galaxy which provides the molecules that make it possible.

Even though it’s in the orbit of the beauty and wellness industry, Galaxy’s business plays by different rules. Where consumer-oriented beauty businesses live and die by their ability to tell a story that draws customers to a brand, upstream, the competition is one of reliably making large quantities of something in bulk, while surviving commodity cycles.

That was on full display this quarter.

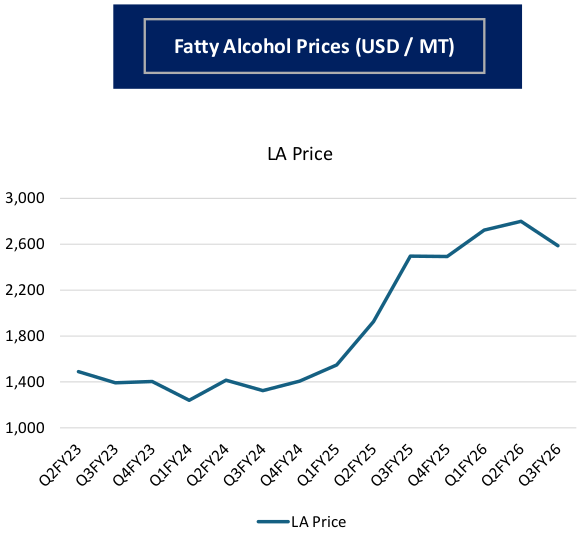

On the surface, Galaxy reported an almost 28% year-on-year surge in its revenues last quarter. But that’s deceptive. The volumes it sold were flat. What changed was the price of its inputs, which forced the company to charge more per ton. While the company’s revenues went up by roughly ₹290 crores this quarter, the cost of its materials went up by ₹280 crores as well. Accounting for that, the company’s operating earnings inched up by a mere ~₹15 crore since last year. And its after-tax profits actually declined by roughly ₹5 crore.

The real story, this quarter, was that global prices for “fatty alcohols” have been unusually high. These are the building blocks behind the surfactants in your soap or shampoo (even if “fatty alcohols” sounds like the opposite of anything beauty).

When prices change like this, it creates a new challenge: customers “reformulate”. That is, they change the recipes of their products. They might, for instance, use slightly less surfactant in a shampoo. Or they might shift to something more synthetic, such as chemicals derived from petroleum. As Galaxy’s management said on their investor call, one of its biggest customers — a tier one personal care brand — did precisely that.

Meanwhile, even customers that stuck to the same formulations changed their buying behaviour. Some delayed purchases, with the hope that prices would eventually come down. Some switched to smaller purchases, entering shorter-term contracts.

This was a problem for Galaxy. It sold marginally less surfactants, by volume, than it did last year. Two things, however, blunted the shock. One, Galaxy’s line of specialty care products became a shock absorber, making up for some lost volumes. Two, as big customers pressed the brakes, a range of smaller, more niche companies — D2C players and the like — stepped in.

Honasa

Lets turn to things you can actually buy in your local market, beginning with Honasa — the company behind Mamaearth. Honasa’s niche is everyday, “routine” products: skin care products like face cleansers and sunscreen, hair care products, and the like.

The company made some major accounting adjustments this quarter, which makes year-on-year comparisons rather confusing. But by all accounts, the company turned in a decent performance last quarter. It grew its revenues by a solid 16%, year-on-year. This, in turn, led to its after-tax profit nearly doubling, to around ₹50 crores.

In a business like this, making a good product is just part of the puzzle. Equally, you need to excel at bringing customers’ attention to your product. And you need to make sure your products reach those customers, wherever they might be.

Think of it like this: Honasa’s total revenue, last quarter, was roughly ₹600 crore. It spent less than one-third of that — or ₹190 crore — for the cost of its goods. Roughly the same amount went into advertising and promoting its products: everything from paying influencers to running in-store promotions. Clearly, this is a category where attention costs as much as products themselves.

But Honasa’s slowly changing this story — becoming a more efficient machine at reaching customers.

Over the last year, the company’s advertising intensity has come down. In the December quarter last year, over 34 paisa of every rupee it earned went into advertising and promotions. Now, that has come under 31 paisa. It’s still spending heavily on reaching customers, but crucially, it isn’t buying its way into incremental growth. It’s spending less on each new rupee of sales.

To the company, this came from “channel mix improvement”. That’s a jargon-y way of saying: Honasa changed how it sold its products, so that each individual sale cost less. Think of it like this: if your products are stocked at the local supermarket, someone might just come across them in their weekly shopping run. To sell that same product online, you might have to pay for visibility. When a store has Mamaearth’s products on display, that is, in itself, an advertisement.

Mamaearth has been focusing heavily on such offline sales. It’s now available at over 2.7 lakh stores across India. On top of this, the company is also perfecting how offline distribution happens.

For one, only its most tried-and-tested products go offline, so that retailers don’t get stuck with unsold inventory. Two, over 80% of its revenue comes from “direct distribution”. That is, for all those sales, it doesn’t compete for the attention of independent whole-sellers. Instead, its dedicated distributors that focus on getting their products to stores — giving it more control over how it reaches customers.

Nykaa

Let’s turn, now, to a juggernaut of beauty retail in India — Nykaa.

Nykaa is a retail machine. It is, at one level, a distribution platform, selling a wide variety of beauty and wellness brands — both online and offline. It’s also added clothing to the mix. Recently, the company also rolled out its own quick commerce offering — Nykaa Now — promising deliveries under two hours across tier-1 cities.

Meanwhile, it’s also a beauty brand in its own right, with many products it sells under its own name. It’s also tying up with major foreign brands for their India businesses, like its new agreements with the French brand, Kiehl’s, and the sporting giant, Nike.

Nykaa had an incredible December quarter. Its sales were up by roughly 28% over last year — with operational revenues touching nearly ₹2,900 crore. Of course, a complex business like this has heavy costs beyond goods alone. Nykaa spends on everything from warehousing, to delivery, to marketing. After all of this, just ₹68 crore shows up in its after-tax profits. That said, it has surged 160% from last year — from a base of just ₹26 crore. And that is after a one-time hit of ₹16 crore it took because of the new labour codes. Without that, its profit would have tripled.

Where is this growth coming from?

For one, Nykaa’s reach is improving. It received 34% more online hits than it did last year — 538 million, to be specific. That, in turn, translated to more business. It had 18.7 unique customers over the quarter; one-fourth more than last year.

Notably, Nykaa isn’t sacrificing the health of its business in search of this growth. The intensity of its marketing is roughly where it was a year ago. And notably, so are its order values. Usually, new customers begin with small orders, and then slowly work their way to larger purchases. With so many new customers, Nykaa should have seen its average order value size drop. But it actually grew by 2%.

Complementing its better reach, Nykaa is also earning more out of each rupee it generates in revenue. This is, in part, because it’s selling more from its own “House of Nykaa” line. Instead of making a mark-up alone, the company’s increasingly earning a brand-owner’s keep.

Interestingly, a lot of their “House of Nykaa” sales are escaping the captive ecosystem. From 18% last year, nearly a quarter of these sales now happen via third party channels. This signals that Nykaa’s own brands are maturing. They can now survive outside its ecosystem.

Miscellaneous

This is a rough snapshot of three corners of India’s beauty industry. Before we leave, though, we wanted to briefly touch on a few interesting nuggets we caught along they way, that didn’t quite fit a brand story:

‘Murica!

One of Galaxy’s big markets — especially for high value specialty chemicals — was the United States. Then, Trump’s tariffs came in. American customers rammed the brakes, and briefly refused to look for new formulations. That problem, it appears, is now solving itself, with our revised 18% tariff rate. But there’s a new, longer term problem: at least if Galaxy is to be believed, tariffs or otherwise, America’s consumer demand is softening. This is a key signal to watch — not just for Galaxy, but for anyone else that does business there. The world’s largest consumer market, it seems, could be weakening.

Two and a half men(‘s brands)

The next frontier for beauty and wellness brands, it appears, is men. Mamaearth, for instance, just acquired Reginald Men, which targets its products at men. According to the company, men’s skincare is at an “inflection point” — with online searches for things like “sunscreen for men” and “face wash for men” jumping six-fold in the last five years. Nykaa, too, has seen an incredible 45% growth, year-on-year, on its range of men’s perfumes.

Offline sales: what are they good for?

Nykaa and Mamaearth, interestingly, look at the offline game very differently. Mamaearth, as we saw, is focusing on getting distribution out to general trade — to kirana stores and the like. Nykaa, on the other hand, sees offline sales as an lever to pull people to expensive products, which they want to sample personally before committing. Take perfumes: Nykaa, it appears, considers perfumeries as places where it can invest in the trial and education that it needs to convert customers.

Tidbits

- India’s unemployment rate rose to a three-month high of 5% in January from 4.8% in December, per the latest PLFS data. The uptick was largely rural-driven due to post-harvest slack and winter slowdowns, with female unemployment climbing to a seven-month high of 5.6%. Source: ET

- Wholesale inflation hit a 10-month high of 1.81%, more than doubling from 0.83% in December, driven by a sharp rise in manufactured goods prices—up to 2.86% from 1.82%—led by costlier basic metals. Core inflation surged to a 38-month high of 3.2%, signalling building input-cost pressures. Source: ET

- Reliance Consumer Products, the FMCG arm of Reliance Industries, has signed a deal to form a majority-owned joint venture with Lagos-based Tropical General Investments Group to sell its consumer products in Nigeria. RCPL’s gross revenue grew 60% YoY to ₹5,065 crore last quarter. Source: Fortune

- This edition of the newsletter was written by Krishna and Pranav

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()