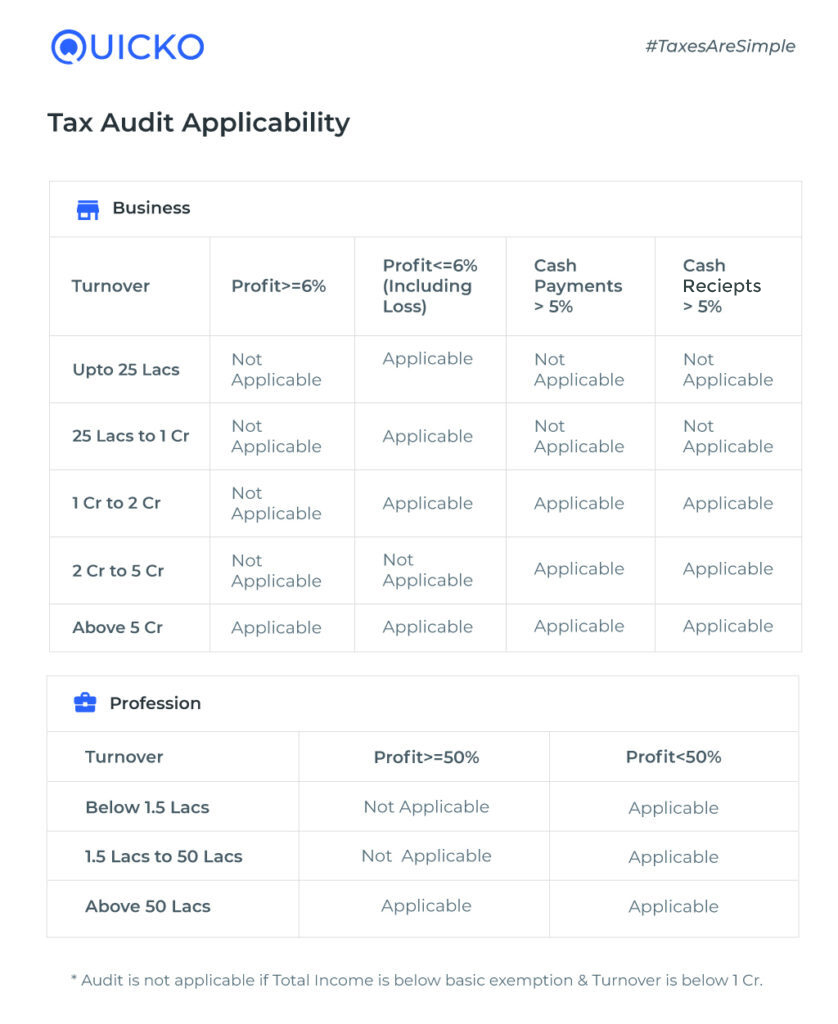

When Section 44AB and Section 44AD are read together, tax audit is applicable in the following situation - when the trading turnover is up to INR 1 Cr, there are losses or profits are less than 6% of turnover, total income is more than basic exemption limit and the taxpayer has opted out of presumptive taxation scheme by not following the five year rule as per Section 44AD(4).Tax Audit is recommended for such taxpayers for the following reasons:

It is difficult to check whether the taxpayer had opted out of presumptive taxation scheme in any of the previous five assessment years.

There are taxpayers who have received a tax notice for claiming losses without going for Tax Audit.

Based on our practical experience, the taxpayer should claim and carry forward trading loss by opting for tax audit so as to avoid chances of receiving a notice from the tax department. Further, we always advise with a clearer answer once we look at the income situation and trading statements.

We would be glad to explain and resolve your questions if you can share your contact details on [email protected]

Quicko is an online tax filing platform. However, when our customers have audit requirements, we connect them with Chartered Accountants who could conduct tax audit if you want.

Great, it is always a good practice to file your ITR, even if your income is below the basic exemption limit. It reduces the chances of getting a notice from the ITD, especially after the SEBI & CBDT Data partnership.

F&O trading is treated as non-speculative business income and should be reported under the head business income when filing ITR.

In case your total income is below the basic exemption limit and turnover is below INR 1cr, you do not need to get tax audit done.

You can use this tool to check if tax audit is applicable to you.

Turnover is more than the threshold

You can use this tool to determine if tax audit is applicable to you.

If you miss submitting a tax audit report when a tax audit is applicable to you, there are chances of receiving a notice from the ITD. In such a case, you need to get your books of accounts audited and file a revised ITR with the tax audit report prepared by a practicing CA.

@Quicko a little different query , my relative had a loss of 4 lakh in AY18-19 and in AY19-20 he made profit of same amount. So will his 18-19 loss should be set off with AY19-20 profits or not , however he did not want to set off this loss since his income is already below exemption limit so can he carry forward loss to subsequent years as well without offsetting it in this year.

Hope you got what i am trying to ask.

No, the Income Tax Department does not allow to carry forward the loss to future years without setting it off against the income of the current financial year.

Learn more about set off and carry forward of losses here.

Hey @Quicko

I have used your tax audit calculator and it shows me the audit required as per section 44AB.

But If I consider section 44AA that is for maintaining the book of account, I do not fall into the criteria of maintaining a book of account due to lower turnover.

So If I do not have the book of accounts then how will the audit apply to me.

My turnover/profit/receipt for the last 3 years is less than the required limit for Audit. I have intraday losses and turn over for current year too is less than 1 lakh.

Quicko follows a conservative approach when determining tax audit applicability u/s 44AB and hence tax audit is recommended whenever the turnover is less than INR 25 Lakhs and has losses. However, if you have never opted for the presumptive taxation scheme and your turnover is less than INR 25 Lakh you can file ITR 3 without tax audit.

So, sir, if someone has more than 5 crore turnover, he only needs to get his books and trades audited by a CA, right? He need not pay any penalty to the taxman, right?

Yes. However, if your don’t file tax audit form within the specified due date, then there is a penalty which is lower of

A] 0.5% of turnover or

B] Rs 1.5Lacs