Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- A Closer Look at the Panama Port Deal

- How India’s port companies are changing

A Closer Look at the Panama Port Deal

The Panama Canal is one of the world’s busiest shipping lanes. And right now, it could be on the brink of a strategic shift.

Two ports at both gateways of the canal — Balboa and Cristóbal — might just change hands in a $22.8 billion deal. These ports handle nearly 39% of the canal’s container traffic — about 3.74 million TEUs annually — and oversee more than 12,000 ships that pass through the canal each year. If approved, the world’s largest shipping company, MSC, and BlackRock’s infrastructure fund will take them over from Hong Kong’s CK Hutchison.

Their sale, though, isn’t a mere commercial agreement. It’s a matter of global power dynamics .

These companies stand to buy a piece of one of the world’s most important geopolitical chokepoints. And that’s why this deal has landed up at the center of a major international diplomatic tussle.

Why Panama is central to the world’s supply chains

The Panama Canal is one of the world’s most important trade shortcuts.

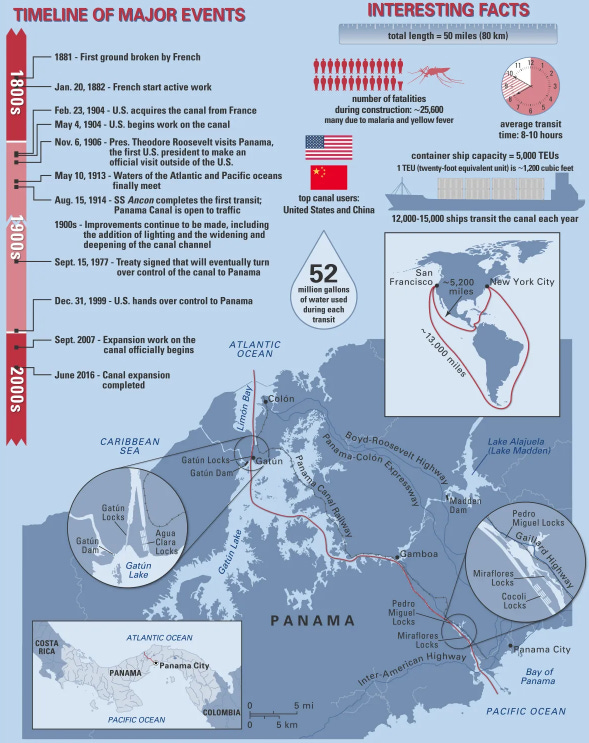

The canal cuts through the heart of Central America. In doing so, it creates a shortcut between the Pacific and Atlantic oceans: where any ship can quickly pass between the Eastern and Western sides of the Americas. Without it, ships would have to travel another 8,000 nautical miles for the voyage — all the way around South America’s Cape Horn.

If you ever need to by-pass the Americas — if you’re transporting something from Japan to New York, or from Europe to San Francisco, or even within the United States, between its two coasts — the 8,000 nautical miles you save can shave off weeks in transit times, and millions of dollars in fuel.

This is why the canal is always in such heavy use. Today, around 5% of global maritime trade — roughly 423 million tons of goods every year — passes through this single, narrow corridor.

The importance of the canal is all the more obvious when the Suez canal — a similar shortcut by-passing Africa — is out of action. Earlier this year, for instance, tensions in the Red Sea disrupted traffic through the Suez Canal. Cargo from Asia to the American East Coast was re-routed through the Pacific ocean, via the Panama Canal. Suddenly, the canal saw a large spike in rerouted traffic. The canal was, in essence, a pressure valve for global shipping.

But there’s a flip side to this. If the Panama canal ever stops flowing, global trade takes a severe beating. Trade to and from the Americas, in particular, can suddenly stall. In 2023, for instance, a severe drought made it difficult to operate the canal, forcing authorities to limit daily ship transits. Overnight, this created long queues outside the canal, driving up freight rates.

A shipping traffic jam stuck outside the canal

The canal is, in short, a chokepoint . And as we’ve often mentioned on The Daily Brief , in the cut-throat world of international trade, any chokepoint is simultaneously a point of leverage.

The two mouths of the canal

Panama has drawn geopolitical interest for more than a century.

The canal was never a local, Panamanian project. From the very beginning, it was conceptualised, and then constructed, by hegemonic powers — it began as a French project, which was taken over by the United States. The United States always saw it as a passage for its naval and commercial ships. For over 80 years from the point the canal was first constructed, it was entirely under US control. America also built a large number of military bases flanking the canal, to remind the world of who held sway over this vital maritime artery.

That grip began to loosen in the 1970s. Panama had always been sore about how America controlled something so strategically important, which ran right through its territory. Those tensions hit a boiling point over the 1960s and 1970s. The two sides eventually signed the Torrijos-Carter Treaties of 1977, which promised full Panamanian control over the canal by 1999. This came with an obligation, however: Panama was to keep the canal open to ships from any country at all times — even in a case of war.

That shift wasn’t smooth . In 1989, for instance, the U.S. invaded Panama — supposedly in “self-defence”. One of its key goals was to ensure its control over the canal.

For around 25 years now, however, the canal has stayed in Panamanian hands. But that peaceful interregnum might be ending. Global powers once again vie for influence over the canal. China, in particular, has been courting Panama under its belt-and-road initiative. And that has raised concerns in the United States.

A lot of this international interest, currently, targets its two access points.

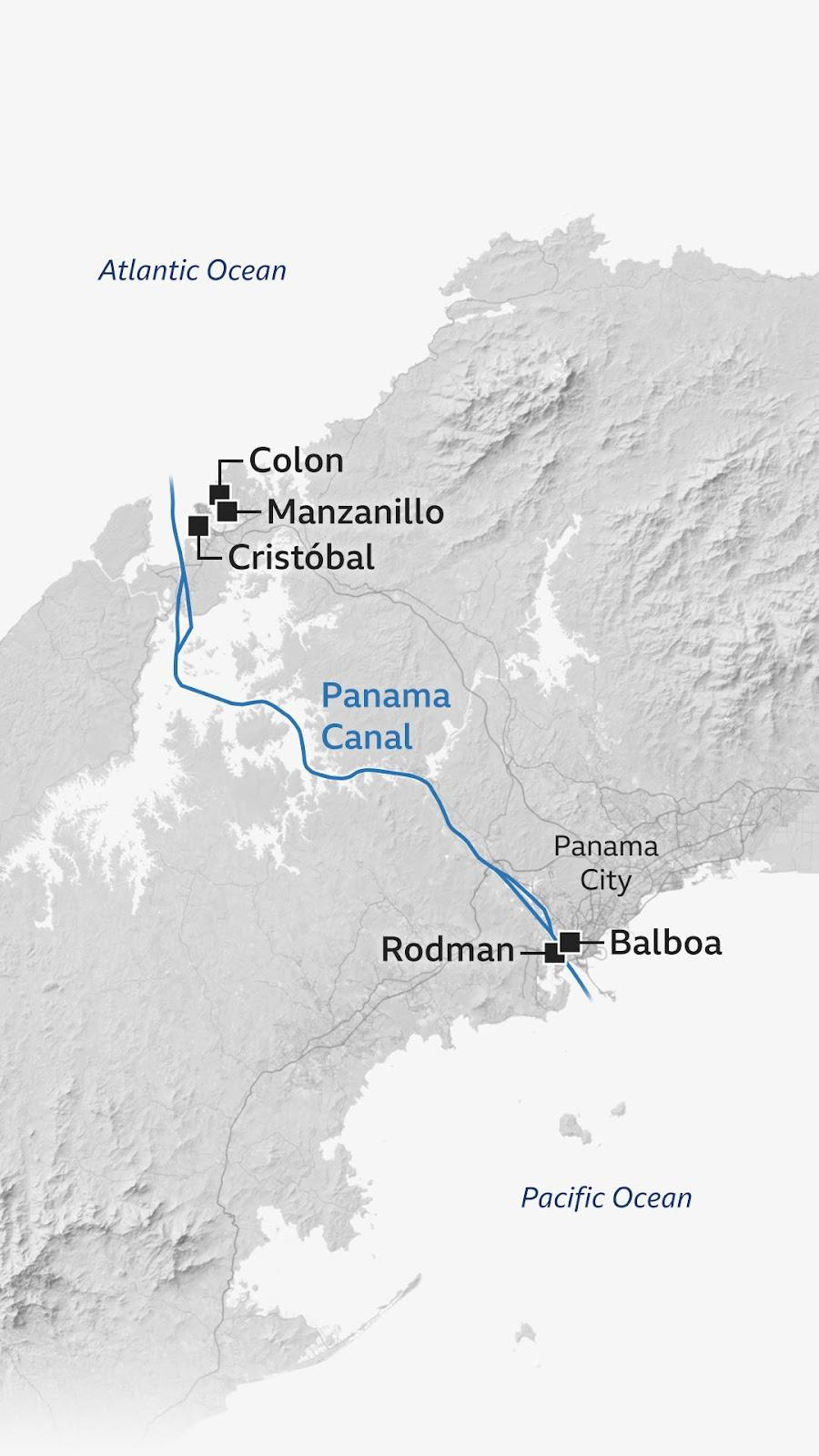

At the Pacific entrance of the Panama Canal is the Port of Balboa. At the other end, guarding the Atlantic mouth of the canal, is the port of Cristóbal. Together, both are critical access points to the canal.

To be fair, these don’t have a monopoly . Panama has other terminals, like PSA Rodman or Manzanillo. But none of them match the geographic and operational importance of Balboa and Cristóbal. Between them, the two ports control nearly half of the country’s container traffic. They’re effectively the entry and exit points of the Panama Canal.

A large part of their business, in fact, revolves around “transshipment” — that is, ships unload their cargo at these ports, where it is then redistributed to other vessels. These ports are frequented by large ships from all over the world, that pick goods up from, and deposit goods to, these points. Then, that cargo moves to a network of small feeder ships that serve ports all across the Americas. This puts them at the very heart of American maritime trade.

The deal

It is these critical ports that might now change hands. At stake is control over one of the world’s busiest trade routes.

MSC’s Terminal Investment Ltd. (TiL), the port-operating arm of shipping giant MSC, has teamed up with BlackRock’s Global Infrastructure Partners (GIP) to acquire control of the two ports, for the headline-grabbing price tag of $22.8 billion. At the other end is Hong Kong-based CK Hutchison.

The deal, in fact, goes deeper than these two key ports alone. If the deal goes through. TiL and GIP will also gain minority stakes in 41 other port-related assets around Panama, including valuable land parcels, rail connections, and associated infrastructure — essentially giving them influence over the broader logistics and transport ecosystem surrounding the canal. Hutchison retains only a minor residual stake.

But there’s the problem. CK Hutchison is a company based in Hong Kong. While it doesn’t have a direct connection to the Chinese state, it still operates under the shadow of the Chinese Communist Party. Both MSC and Blackrock, on the other hand, are decidedly oriented towards the West.

And so, to China, this looks like strategic encroachment by Western interests. Chinese state media and strategic commentators have framed the deal as a loss of critical infrastructure. And China is doing whatever it can to grind the deal down.

Right now, the mega-transaction hinges on approval from Panama’s Maritime Authority and the Panama Canal Authority (ACP), which are caught in a cross-fire between the United States and China. Chinese authorities, meanwhile, have been putting considerable pressure on CK Hutchison to cancel the sale. It might try using anything from antitrust laws to its national security laws to try and scuttle the deal.

The parties have set a deadline of July 27 for the deal to be finalised. Beijing is actively trying to collapse the deal before that date, or is at least threatening to do so in order to extract tariff concessions from the United States.

Why is Beijing so worried

Not very long ago, Beijing would have thought it had a strong hand in Panama.

For many years, Panama didn’t recognise China as a legitimate country — preferring to maintain formal relations with Taiwan instead. But things began to thaw in 2017. Panama withdrew its relations from Taiwan, embracing China. The two countries began trade talks, and a year later, in 2018, Panama became the first country to join China’s Belt-and-Road Initiative. It quickly became a symbolic cornerstone in the initiative’s expansion into the Western Hemisphere.

It was during this time that Panama extended CK Hutchison’s contracts over the Balboa and Cristóbal ports for 25 years, beginning in 2021.

But when Donald Trump became the American President, he immediately pushed the country to abandon its ties with the Chinese. The two super-powers began a tug-of-war for the country’s loyalty. Under pressure, Panama formally exited the Belt and Road Initiative — much to China’s dismay.

To the United States, the deal is a diplomatic and strategic win. It diminishes China’s operational influence in its geopolitical backyard. China, meanwhile, is deeply unhappy.

What is it afraid of? Primarily, it’s this: while the Panama canal is neutral in theory , anyone that controls the ports at Balboa and Cristóbal can influence all the trade that flows through.

This influence can be subtle. Port operators influence key decisions: from berth scheduling, to terminal fees, to cargo processing times. They can play favourites here, prioritising certain shipping lines or countries, while squeezing competitors by slowing them down. If a future port owner slaps high terminal charges on a country, or only gives it inconvenient berthing schedules — it can penalise that country while technically staying within the bounds of neutrality.

In a more extreme scenario, however, these could become points of hard power projection. If there’s ever a geopolitical flashpoint — operators could deny vessel access outright under various pretexts, effectively cutting countries off the trade route. We’ve seen this before: the chokepoints at Djibouti and the Suez Canal have previously been used for political leverage.

Ports could also become intelligence-gathering hubs. Infrastructure and tech installed for port operations could quietly collect data, monitor rival supply chains, or even, in theory, enable cyber disruptions.

This is why, at the very least, China wants a seat at the table. Even if it can’t stop the sale from going through, it wants some point of leverage. For instance, recent leaks suggest China’s state-owned shipping giant COSCO is in advanced talks to buy a minority stake in the MSC-led consortium. If successful, China could reinsert itself into the ports’ governance, preserving at least partial access to the two chokepoints.

The bottomline

Under the guise of a commercial deal, what we’re seeing, perhaps, is a strategic realignment .

Control over Balboa and Cristóbal means influence over how the Panama canal operates in practice, even if not in name. That’s why it has received so much attention from Beijing and Washington. The United States sees this as an opportunity to reassert control in its hemisphere. China, on the other hand, faces a loss of leverage in a critical corridor.

Stuck between the two is Panama, for whom this has become a brutal test: of whether it can stay neutral when the ports at both ends of its canal become pawns in a global power contest.

How India’s port companies are changing

Yesterday, we had looked at India’s ports industry, and its crucial role as “the lungs of our economy”. The vast majority of the goods we bought and sold as a country — 90% by volume, in fact — touched our ports at some point.

But knowing that ports matter is one thing. Understanding the actual businesses that run them is quite another. So, like we promised last time, we’ll dive into two companies that sit behind the scenes as cargo moves in and out of India: Adani Ports , and JSW Infrastructure .

These entities are at an interesting juncture. As we’ll soon see, some of our biggest port players aren’t just running ports anymore. They’re building something much more ambitious.

Adani Ports

Adani Ports and Special Economic Zone Ltd (APSEZ) is India’s largest private port operator. It runs 15 ports and terminals across the Indian coastline, capturing 27% share of all cargo handled in the country.

Its flagship port, at Mundra in Gujarat, is now the first port in India to cross 200 million metric tonnes (MMT) in a year.

That is impressive in itself. But it only scratches the surface. See, Adani Ports is in the process of re-writing its entire business.

Adani is coming for the entire supply chain

For decades, port operators made money in a fairly straightforward way. When a ship arrived, they charged for letting it dock. When cargo needed unloading, they charged for that too. And maybe they would store some containers for a few days and collect storage fees.

This was a volume game. The more ships that came, the more money you made. Your fortunes rose and fell with global trade cycles.

But about a decade ago, APSEZ started thinking about this differently. They began asking: why only touch cargo when it’s at the port ? Why not control its entire journey?

Think about what happens when a container arrives from, say, China.

- First, it gets unloaded at the port.

- Then, a truck picks it up and takes it to a railway yard.

- Then, a train carries it to an inland depot.

- From there, another truck takes it to a warehouse.

- And eventually, yet another vehicle delivers it to its final destination — maybe a factory in Haryana or a distribution centre in Pune.

Here’s what it looks like:

At each step, different companies handle the cargo, and each takes their cut. But what if one company could do it all?

This is what APSEZ is trying. They started expanding beyond the waterfront, to buy their own trains: 132 rail rakes to be precise. They also built inland logistics parks in cities far from the coast, setting up 3.1 million square feet of warehousing. At the other end, they acquired a fleet of 115 vessels for marine services. And they even created tech platforms to manage trucking and freight forwarding.

A company that once just ran ports, in short, is slowly turning into what they now call an “integrated transport utility.” In the words of Mr. Divij Taneja, the CEO of Adani Logistics:

“You’re seeing us move from custodians to exhibiting control over cargo. ”

The financial logic behind this transformation is fairly intuitive. Let’s say unloading a container earns you ₹100. That’s what a traditional port operator would make. But if you also move that container on your own train, store it in your warehouse, and deliver it using your trucking network, you could earn, say, ₹500 from the same container. More touchpoints mean more revenue, and crucially, higher margins as well.

Adani’s business in numbers

You can see this shift in their numbers. In FY 2025, Adani Ports handled 450 million metric tonnes of cargo, which is about 7% more than the previous year. But their revenue jumped 23% , while their profit surged 50% . How does a 7% growth in volumes translate to a 50% profit growth?

That is the story of Adani’s changing business model.

Three things are driving this transformation.

- First, the type of cargo is shifting. We spoke about this yesterday: as our economy grows more sophisticated, containers, which carry higher-value goods like electronics, textiles, or auto parts, are growing faster than bulk cargo like coal or iron ore. That’s what Adani is seeing. Containers now make up 45.5% of Adani’s total cargo, up from 44% a year ago. And because container cargo involves more steps in the supply chain, it offers more opportunities to earn revenue.

- Second, its ‘non-port businesses’ are taking off. That’s the shift we were referring to. Their logistics arm grew revenue by a massive 39%, to ~₹2,881 crore last year. Marine services, which include things like dredging harbors, supporting offshore operations, and guiding ships, grew even faster, jumping by an incredible 82% to ~₹1,144 crore. What used to be side businesses, in essence, is now becoming a major revenue driver.

- Third, they’re getting better at squeezing profits from existing operations. Even with modest volume growth, they’ve expanded margins through smarter pricing, while controlling costs. Equally, the company is focusing on making sharper investments that generate quicker returns. Their domestic ports, in fact, are returning all the capital they’ve invested in less than five years — in an industry where returns would previously come in as long as a decade.

Impressively, these improvements in their business have coincided with them slashing down their debt. Their net debt relative to earnings has fallen from 2.3 times to 1.9 times over the last year. They repaid ₹5,500 crore of debt last year and ended with nearly ₹9,000 crore in cash.

Their future investments — slated to be around ₹11,000-12,000 crore next year — will come entirely from their own profits, and not any new borrowing.

Internationalisation

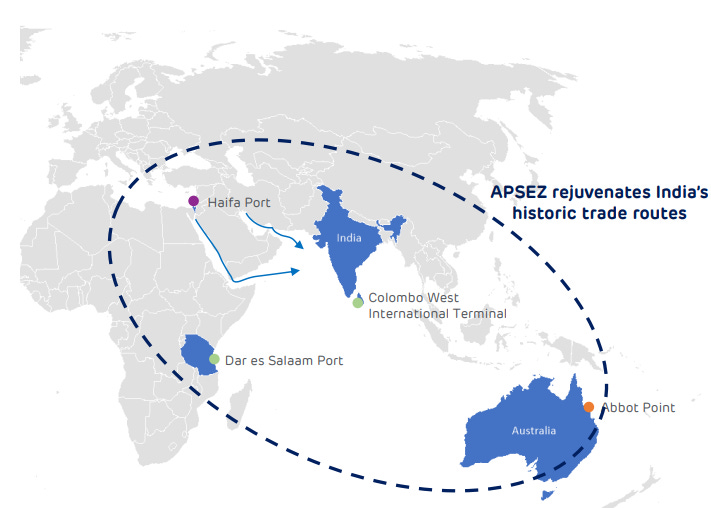

Adani’s ambitions aren’t just limited to India. They’ve also been building an international network.

For one, they run Haifa Port in Israel. Many initially thought this was a risky bet, given the region’s tensions. But they’ve managed to stabilize those operations. They’ve signed long-term union agreements, and are now seeing double-digit profit growth.

That’s just one of their foreign forays. They’ve also started operations at a terminal in Colombo, Sri Lanka, have won a 30-year concession to run Dar es Salaam port in Tanzania, and are acquiring a major coal terminal in Australia that could handle 50 million tonnes annually.

This international expansion is like an insurance policy for the business — allowing it to diversify its bets in a heavily capital-intensive sector. If India’s trade slows down due to a recession or policy changes, having ports in other high-growth regions provides stability.

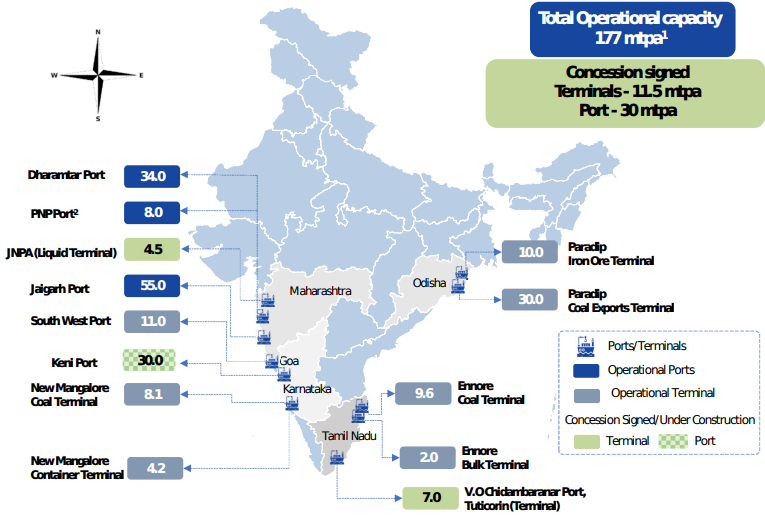

JSW Infrastructure

JSW Infrastructure is India’s second-largest private port operator. At the end of FY 2025, the company had 177 million tonnes per annum of operational port capacity – across 10 ports and terminals strategically located on both the east and west coasts of India. These ports aren’t just piers and cranes; many are deep-draft facilities capable of handling large ships.

Right now, JSW Infrastructure is taking an approach which is very different from Adani’s, but equally interesting: it plans on becoming a full-stack logistics enabler for heavy industries.

JSW’s heavy industry play

While Adani is building a global, multi-modal network that can handle any type of cargo, JSW Infra is sharpening its scope instead, focusing on becoming the go-to logistics partner for India’s heavy industries.

That is why, unlike Adani Ports, which is slowly moving towards containerised cargo, the strength of JSW Infra’s ports lies in bulk cargo — things like coal, iron ore, and liquid cargo. (If this sounds alien to you, check out yesterday’s edition.)

What distinguishes their business, though, is their integration . Many of JSW’s ports are connected directly to steel plants, power stations, and mines through dedicated rail lines and also slurry pipelines.

Imagine this: you’re in the business of exporting iron ore, but you don’t have to load it all onto trucks which drive all the way to the coast, killing your already razor-thin margins. What if, instead, you can grind it into a fine powder, mix it with water, and pump it through a 302-kilometer pipeline to the port directly ? That’s exactly what JSW is building in Odisha. While this might sound almost absurd, this is actually one of the most efficient ways to move bulk materials over long distances.

This tight integration creates customer stickiness for them, because customers’ operations are now built around the infrastructure that JSW provides. For instance, imagine you’re running a steel plant. If your coal arrives at a specific port, and your iron ore comes through a particular pipeline, then your entire operation is designed around your logistics provider’s network. Switching to someone else would mean rebuilding everything from scratch, which you would want to avoid doing unless absolutely necessary.

JSW has built this network out in the recent past. They started out serving only their parent company’s steel and power plants. But today, half their cargo comes from outside customers who’ve built their operations around JSW’s infrastructure.

The numbers

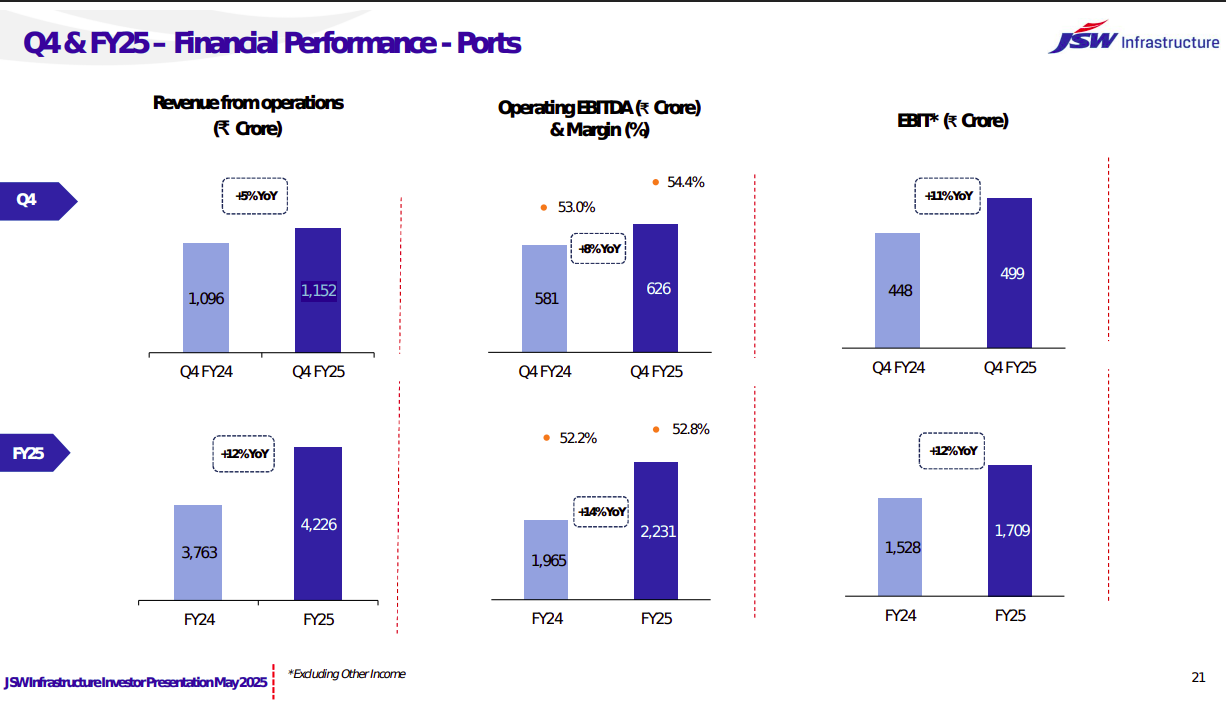

The company’s fourth-quarter results show how this model is working.

Over Q4 last year, its revenue grew 5% to ~₹1,152 crore. But the company’s net profit for Q4, on the other hand, jumped 57% to ₹516 crore.

Now, don’t let that figure fool you. The operating profits of the company were nowhere as impressive. The company’s EBITDA for the quarter grew by a far more modest 8% — to ₹626 crore. Some of the profit jump came from one-time currency gains, while the company essentially had to tax outgo over the quarter.

Expansion plans

Regardless, the underlying business is clearly strengthening. The company is bringing more capacity online: with ~1 million tonnes of new capacity coming up over the quarter. This is slated to grow over the coming quarters.

The company is ramping up the capacity of its existing ports. At South West Port in Goa, for instance, the company expanded from 8.5 to 11 million tonnes per annum. It’s in the process of getting regulatory approvals for a further expansion — all the way to 15 MTPA.

Meanwhile, JSW Infra is expanding beyond ports as well. They recently bought 70% of Navkar Corporation, which runs inland container depots and freight stations. Here, containers can be sorted, stored, and distributed, en route to whatever destination it must finally get to. It’s basically one more way to capture more value from each shipment.

The bottomline

What we’re witnessing right now with both these companies is a fundamental shift in how the logistics business works in India. The old model was simple — you owned a piece of key infrastructure, and you used it to charge tolls. But these players are now thinking about owning the entire journey.

This transformation matters for several reasons. Their customers need to deal with fewer vendors, while getting more predictable service. For these companies, meanwhile, it means higher margins and more stable revenues. For India’s economy, it means more efficient trade infrastructure that can handle growing volumes without proportional increases in cost.

Both Adani Ports and JSW Infrastructure are betting that India’s trade ambitions will keep growing. And they’re positioning themselves to capture not just a slice of that growth, but the entire pie, right from the moment a ship appears on the horizon to the moment its cargo reaches its final destination.

Tidbits

- Dassault Expands India Partnership, to Manufacture Falcon 6X and 8X Jets with Reliance

Source: Business Standard

Dassault Aviation has announced a significant expansion of its joint venture with Reliance Aerostructure Ltd at the Paris Air Show, marking a first in Falcon jet manufacturing outside France. The Dassault Reliance Aerospace Ltd (DRAL) facility in Mihan, Nagpur—already responsible for delivering over 100 major subsections of the Falcon 2000 since 2019—will now be upgraded to a Centre of Excellence. This facility will handle manufacturing and assembly for the Falcon 2000, as well as the upcoming Falcon 6X and flagship 8X models. DRAL is a 51:49 joint venture between Dassault and Reliance, originally set up in 2017. Dassault’s decision positions India as a core part of its global supply chain and marks a notable milestone in the country’s ambitions to scale high-value aerospace manufacturing under the Make in India initiative.

- Welcure Secures ₹517 Cr Sourcing Deal with Thai Firm, Eyes ₹26 Cr in FY26 Service Income

Source: Business Line

Welcure Drugs & Pharmaceuticals Ltd. has signed a ₹517 crore third-party sourcing agreement with Thailand-based Fortune Sagar Impex Company. Under the ex-works model, Welcure will earn a fixed 5% commission on the transaction value, translating to an expected service income of ₹26 crore in FY26. The deal involves procurement of multiple finished-dosage SKUs, with all downstream responsibilities—including packaging, freight, and regulatory clearances—handled by the Thai partner. The structure allows Welcure to avoid inventory risk and manufacturing commitments, supporting an asset-light model with high-margin potential. The company aims to leverage this agreement to scale its fee-based services without straining its balance sheet.

- India’s $89 Billion Clean Industrial Pipeline Sees Slow Progress, Only One Project Reaches Final Investment Decision

Source: Reuters

India’s clean industrial transition faces a critical slowdown as only one out of 41 announced projects, worth a cumulative $89 billion, has reached Final Investment Decision (FID) in the past six months. Despite a strong pipeline in sectors like green ammonia, hydrogen, and sustainable aviation fuel, just $13 billion has been committed so far. In comparison to global figures, 83% of the 826 clean industrial projects worldwide are still awaiting financing, highlighting a broader investment challenge. Key obstacles include high capital costs, underdeveloped commodity markets, and policy uncertainty. The report flags that India’s progress is significantly behind countries like China and the U.S. in terms of actual capital deployment. Without timely financial closure and execution, India’s goal to decarbonize hard-to-abate sectors risks being delayed.

- This edition of the newsletter was written by Pranav Manie and Krishna.

Join our book club

Join our book club

We’ve started a book club where we meet each week in JP Nagar, Bangalore to read and talk about books we find fascinating.

If you think you’d be serious about this and would like to join us, we’d love to have you along! Join in here.

Have you checked out The Chatter?

Have you checked out The Chatter?

Every week we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Go check out The Chatter here.

“What the hell is happening?”

We’ve been thinking a lot about how to make sense of a world that feels increasingly unhinged - where everything seems to be happening at once and our usual frameworks for understanding reality feel completely inadequate. This week, we dove deep into three massive shifts reshaping our world, using what historian Adam Tooze calls “polycrisis” thinking to connect the dots.

Frames for a Fractured Reality - We’re struggling to understand the present not from ignorance, but from poverty of frames - the mental shortcuts we use to make sense of chaos. Historian Adam Tooze’s “polycrisis” concept captures our moment of multiple interlocking crises better than traditional analytical frameworks.

The Hidden Financial System - A $113 trillion FX swap market operates off-balance-sheet, creating systemic risks regulators barely understand. Currency hedging by global insurers has fundamentally changed how financial crises spread worldwide.

AI and Human Identity - We’re facing humanity’s most profound identity crisis as AI matches our cognitive abilities. Using “disruption by default” as a frame, we assume AI reshapes everything rather than living in denial about job displacement that’s already happening.

What the hell is happening?

What the hell is happening?{kind=link}

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()